Investment Property Loans Australia: A Broker’s 2026 Guide

Investment Property Loans in Australia: The Broker’s Guide for 2026

On this page ▾

- What Is an Investment Property Loan?

- How Investment Property Loans Work in Australia

- Investment Loan Interest Rates: Why Investors Pay More

- How Much Can You Borrow? (And Why Your Bank’s "No" Isn’t the Market’s "No")

- Interest-Only vs Principal & Interest for Investors

- Loan Structuring: Splits, Cross-Collateralisation, Equity Release

- Negative Gearing and Tax Implications (General Information Only)

- How an Investment Property Loan Broker Helps

- Costs and Fees Beyond the Interest Rate

- How to Apply for an Investment Property Loan

- Frequently Asked Questions

- Speak to a Broker Who Has Seen This Before

If you have already spoken to your bank about an investment property loan and walked away with a number that does not work, this guide is for you. An investment property loan is a residential mortgage written for a property you intend to rent out. The product is similar to an owner-occupier loan, but the rate is higher, the assessment is tighter, and the answer you get from one lender can be very different from the answer at the next. After 25 years and 52+ lenders, the single most useful thing we can tell most investors is this: your bank’s “no” is not the market’s “no”. For investors who have been priced out by their own bank’s serviceability calculator, that distinction is worth tens of thousands of dollars in additional borrowing capacity.

The 2026 Federal Budget introduced significant changes to negative gearing that affect both your tax position and your borrowing capacity. For a full explanation of what the Budget means for new investors, including the 12 May 2026 cut-off and how lenders are already adjusting their serviceability assessments, see our dedicated guide.

If you are weighing up the strategy itself before the loan, our guide on the rentvesting strategy covers when investing makes sense before you buy your own home.

What Is an Investment Property Loan?

An investment property loan is a residential mortgage used to purchase a property you intend to rent out. The lender treats the property as an income-producing asset, not your home, and prices the loan accordingly. Most Australian residential investment loans are full-doc, secured by the investment property itself, and follow the same product types as owner-occupier loans (variable rate, fixed rate, split, principal and interest, interest only).

If you are buying a freestanding house, townhouse, unit or duplex with a residential lender, you are inside the residential investment loans category. If you are buying a commercial property (retail, office, industrial, mixed-use over a certain commercial component), you are in commercial investment loans territory, which is a different product set with different rates, terms, and assessment rules.

How It Differs From an Owner-Occupier Home Loan

The mechanics are the same. The differences sit inside how lenders price and assess the loan:

- Higher interest rate. Investor rates typically sit 15 to 55 basis points above the owner-occupier rate at the same lender, same LVR, same product family. We work through the actual 2026 numbers below.

- Tighter LVR caps at higher tiers. Some lenders cap investor LVR at 90% where they would lend to 95% for an owner-occupier.

- Different serviceability treatment. Rental income is shaded (typically 70 to 80% of gross rent counted toward serviceability) and existing investment debt is assessed under stress.

How Investment Property Loans Work in Australia

You apply to a lender, the lender assesses your borrowing capacity (we will get to how that calculation actually works later in this guide), they value the property and confirm the LVR, and they fund the purchase against the property as security. The repayment structure (P&I or interest only) and rate type (fixed or variable) are choices you make at the structuring stage. Most investors take a combination of variable and a partial split, sometimes with the variable portion on interest only.

Before you settle, you will want to understand what kind of rental yield the property is likely to deliver, since rental income flows directly into the lender’s serviceability calculation.

Deposit and LVR Requirements (Including LMI)

Australian lenders generally accept three deposit pathways for investment property:

- 20% deposit (80% LVR). The clean path. No Lenders Mortgage Insurance (LMI), broadest lender choice, and the best rate tier with most lenders.

- 10 to 15% deposit (85 to 90% LVR). Achievable but you will pay LMI. The premium can be $6,000 to $15,000 or more on a $560,000 loan, depending on the LMI provider and your specific risk profile. The good news for investors: LMI on an investment property is generally tax-deductible as a borrowing expense over five years.

- 5% deposit (95% LVR including capitalised LMI). Available, but only at a handful of lenders. The 95% is calculated inclusive of the LMI premium (the LMI gets capitalised into the loan rather than paid up front), the premium is materially higher at this LVR, and the rate is typically priced at the lender’s highest investor tier. Workable when no other deposit path is available; rarely the best option when one is.

- Equity release (no cash deposit). If you already own a property with usable equity, you can use that equity as the deposit on the new investment loan and avoid drawing down savings. The standard formula: usable equity = (current property value × 80%) minus the existing mortgage. Most lenders will release equity up to 80% of the existing property’s value without triggering LMI on the equity-release leg.

Professional waivers are available at most major lenders for select categories (medical, legal, accounting, and a small group of others), allowing investor borrowing up to 90% LVR without LMI subject to income and membership thresholds. We can usually tell you within a phone call whether your profession qualifies.

Using Equity From Your Existing Home

Equity release is the most common path to a second or third property. The equity is drawn down as a separate loan split against your existing home, then used as the deposit on the new investment property. This keeps both properties on stand-alone security where possible. For a deeper walk-through, see our guide on how to use equity to buy your next property.

Investment Loan Interest Rates: Why Investors Pay More

Lenders price investor loans higher than owner-occupier loans for two main reasons. First, investors have historically had a higher default rate during downturns, since selling the family home is a last resort and selling an investment is not. Second, APRA-driven macroprudential measures over the past decade have applied differential capital and lending requirements to investor lending, which feeds into lender pricing decisions. The spread is structural.

The 2026 Investor vs Owner-Occupier Rate Spread

As at April 2026, NAB’s Base Variable Home Loan sits at 6.19% for owner-occupiers (comparison rate 6.19%) and 6.71% for investors (comparison rate 6.71%) on the same product family. That is a like-for-like spread of 52 basis points. Westpac’s Premier Advantage Package and Flexi First Option products show a similar pattern in discount terms (35 to 40 bps wider for investors than owner-occupiers at matching package tiers).

Industry-average rate databases (Finder’s investor variable average sits near 7.02% in April 2026, against Canstar’s owner-occupier variable average near 6.01%) read closer to a 100 bps gap, but those compare different product mixes and LVR tiers. For an apples-to-apples like-for-like figure, 40 to 55 basis points is the realistic 2026 spread between investor and owner-occupier rates at the same lender, same product, same LVR.

Rates as at April 2026, sourced from NAB and Canstar. Both NAB and CommBank moved variable rates by 0.25% in March 2026, so any figure in this section will date itself within a few months. Always verify a current quote at application.

How Much Can You Borrow? (And Why Your Bank’s “No” Isn’t the Market’s “No”)

This is the section that matters most to a borrower who has been told no, capped, or asked to wait twelve months by their existing bank. The honest answer is that “how much can I borrow” is not a single number. It is a different number at every lender, and at the margin the gap between the highest and lowest lender for the same applicant on the same financials can run into the hundreds of thousands of dollars.

There is no income multiple in modern Australian lender serviceability. Lenders calculate a net surplus: net (after-tax) household income, plus shaded rental income, minus living expenses (the higher of declared or HEM), minus existing debt commitments at stress rate, equals the surplus available to service the new loan repayment, with that repayment also stress-tested at a buffer above the actual rate. The variables that move the surplus, and therefore the loan size, are different at every lender.

For a deeper look at the calculation in plain numbers, see our how much can I borrow guide.

The Income Salary Required for Common Loan Sizes

Using April 2026 inputs (investor variable rate 6.71%, 30-year P&I, 80% LVR, $3,500 monthly declared living expenses, 80% rental shading at a 3% gross yield, no other debts), here is the indicative combined gross PAYG income required to qualify:

| Loan size | APRA-regulated lender (3% buffer) | Non-APRA lender (2% buffer) |

|---|---|---|

| $500,000 | ~$100,000 combined gross | ~$94,000 combined gross |

| $700,000 | ~$125,000 combined gross | ~$115,000 combined gross |

These figures are illustrative, derived using April 2026 rates and APRA’s current 3% buffer (with non-bank lenders at a representative 2% buffer). Real-world capacity depends on your individual circumstances, lender policy, credit profile, employment basis, dependants, and existing portfolio exposure. Speak to a broker for a figure tailored to you.

Why Banks Differ on Borrowing Capacity (Buffers, Shading, Exposure Limits)

The same borrower can get five different answers from five lenders because of five separate variables:

- The assessment buffer applied to the new repayment. APRA-regulated banks (every ADI, including the big four) must apply at least a 3 percentage point buffer above the actual rate when stress-testing serviceability, per APG 223. Non-APRA-regulated lenders (Liberty, Pepper Money, Resimac, Firstmac, La Trobe and others) are not bound by APG 223 and typically apply 1 to 2 percentage point buffers. On a $700,000 loan, a 1% lower buffer can lift borrowing capacity by tens of thousands of dollars.

- Rental income shading. Some lenders count 80% of gross rent as servicing income; some count 70%; a few accept 90% in narrow circumstances. For a portfolio investor with three properties, a 10% shading difference reshapes the entire serviceability picture.

- Treatment of existing debt commitments. Some lenders use your actual repayment, some use a stressed repayment, some apply a “floor rate” that is higher again. Credit card limits are usually shaded as if fully drawn at a punitive monthly minimum.

- Existing-customer exposure ceilings. Major banks often cap total exposure to a single household at a portfolio-wide limit. A borrower at their CBA or Westpac maximum may have hit that bank’s ceiling without being anywhere near their actual market capacity.

- Treatment of negative-gearing tax effect. Some lenders add the notional tax saving from a negatively geared property back into assessable income. Some do not. For an investor with two existing rentals, this can swing capacity by $50,000+.

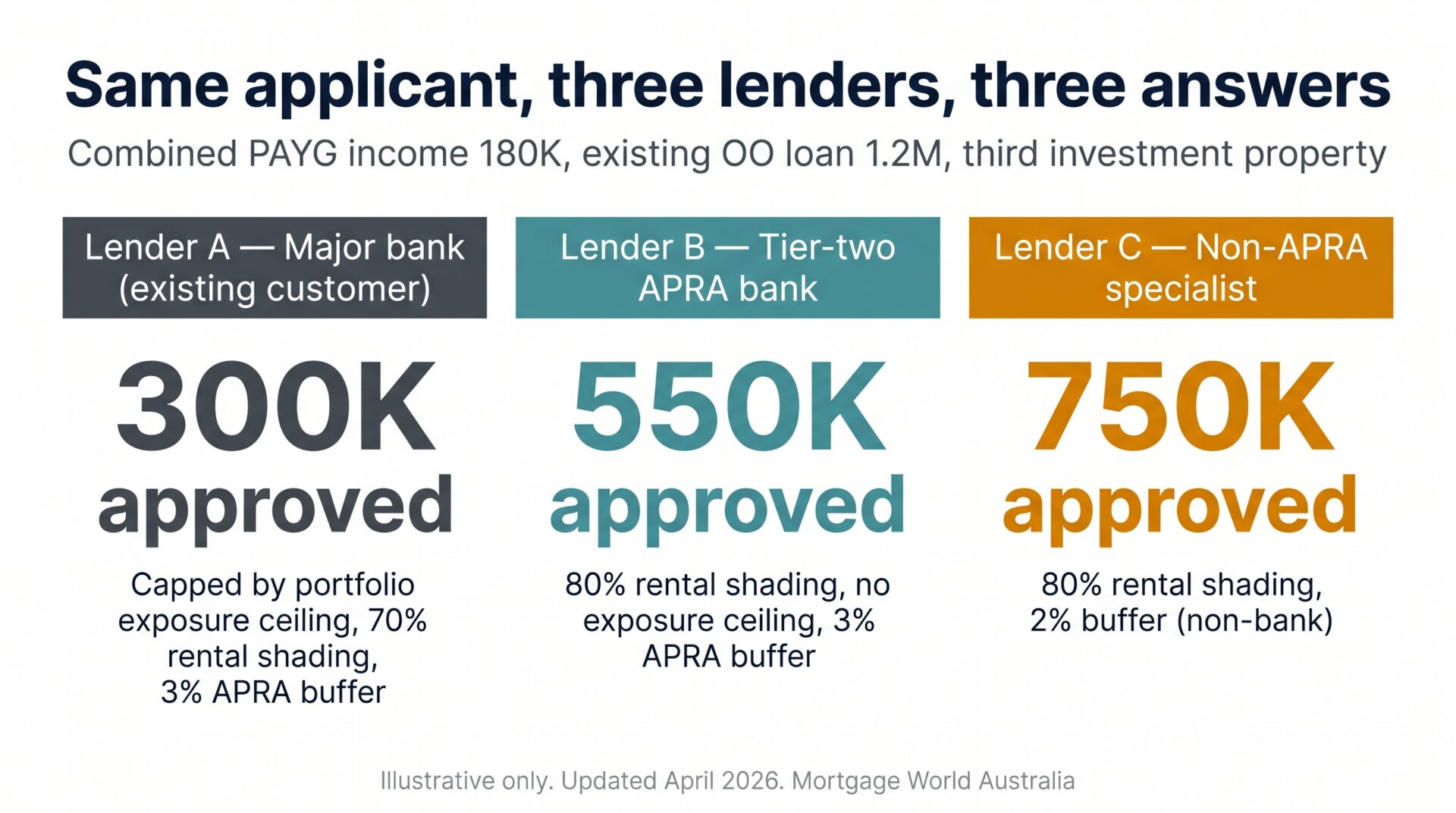

Worked Example: Same Borrower, Three Different Lender Answers

Consider Sarah and Tom: combined PAYG income $180,000 a year, an existing $1.2 million owner-occupier loan, and one established investment property already in the portfolio. They are looking for finance on a third property.

- Lender A (their existing major bank). Capped at $300,000 of additional borrowing. Reason: portfolio exposure ceiling for an existing customer with $1.2M of OO debt and a current investment loan, combined with a 70% rental shade on the existing rental and a 3% buffer on the new repayment.

- Lender B (a tier-two lender, also APRA-regulated). Approves $550,000. Same APRA 3% buffer, but rental income shaded at 80%, the existing OO debt assessed at actual rate plus 3% (not a higher floor rate), and no portfolio exposure ceiling against an unrelated lender.

- Lender C (a non-APRA-regulated specialist lender). Approves $750,000. APRA 3% buffer drops to a 2% buffer (non-bank), rental income shaded at 80%, and the existing OO debt assessed at a more moderate stress rate. The structural buffer differential alone explains most of the gap.

These outcomes are illustrative, not policy quotes. They reflect the type of variation we see weekly. The underlying point is structural: the same financials produce different answers, and the answers are not random. They follow the lender-side rules listed above.

Interest-Only vs Principal & Interest for Investors

For owner-occupiers, principal and interest is almost always the right answer. For investors the choice is more nuanced, because tax treatment, cash flow, and portfolio strategy all push and pull differently.

Principal and interest pays down the loan from day one. Interest payments are still tax-deductible against rental income, but the principal portion is not. P&I is the disciplined long-term path: lower lifetime interest cost, building equity inside the loan as you repay.

Interest only keeps repayments lower (sometimes 25 to 30% lower in the early years) by pausing the principal repayment for an interest-only term, typically one to five years for an investment loan. The repayment is fully tax-deductible. Interest only suits investors who are still acquiring properties and need maximum cash flow flexibility, or who want to direct surplus cash flow toward debt on a non-deductible owner-occupier loan rather than the tax-deductible investment loan. The trade-off is that the loan does not amortise during the IO term, repayments step up sharply when the IO period ends, and lenders often charge a higher rate for IO than P&I. For more on this product specifically, see our explainer on interest-only investment property loans. To compare the P&I and interest-only repayment on your own loan size, estimate your repayments at each rate.

Loan Structuring: Splits, Cross-Collateralisation, Equity Release

How the loan is structured matters as much as the rate. Three structural choices recur across investor portfolios:

Splits. Splitting one loan into multiple loan accounts allows fixed and variable portions, P&I and IO portions, and cleanly separated tax treatment for properties used differently (mixed personal-and-investment usage, for example). At the application stage, splits are functionally free at most lenders.

Cross-collateralisation. Cross-collateralisation means securing one loan against more than one property. Banks like it because it simplifies their security position. Most experienced investors avoid it because it creates one tangled portfolio that is hard to refinance, hard to sell from in pieces, and hard to extract equity from without re-valuing the whole thing. We cover this in detail in our guide on cross-collateralisation explained, and we cover the wider question of how to structure investment property ownership.

Equity release for the next deposit. The cleanest structure for a portfolio investor is stand-alone security on each property, with equity released from one to fund the deposit on the next as a separate loan split.

When to Avoid Cross-Collateralisation

Avoid cross-collateralisation when you intend to grow the portfolio past two properties, when you might want to sell one property without disturbing the others, when the properties are with different lenders or in different ownership structures, and when you may want to extract equity selectively from one property at a future date. The short rule we use with clients: cross is acceptable only when you are confident you will hold both properties for the long term and refinance them together. Otherwise, keep them separate.

Negative Gearing and Tax Implications (General Information Only)

Negative gearing applies when the deductible expenses on your investment property (interest, rates, insurance, property management, repairs, depreciation, capital works) exceed the rental income, producing a tax loss. Under current ATO rules, that loss can be offset against your other assessable income (salary, business income, other investment income), reducing your tax liability for the year. We cover the mechanics in detail in our negative gearing in Australia guide. For more on this, see our depreciation deep-dive guide.

Two important changes from the May 2017 federal budget reshaped the deductibility landscape and still apply in 2026:

- Second-hand depreciating assets. From 9 May 2017 onwards, you cannot claim Division 40 depreciation on second-hand plant and equipment in a residential investment property. New plant and equipment installed after purchase remains depreciable. Pre-9 May 2017 acquisitions are grandfathered.

- Travel deductions. Travel expenses to inspect, maintain, or collect rent on a residential investment property have not been deductible since 1 July 2017, regardless of distance.

Capital works deductions (Division 43, the building shell) are unaffected and continue under the construction-cost rules.

When you eventually sell, you will face capital gains tax on the gain. Holding for more than 12 months gives you access to the 50% CGT discount as an individual. We cover the mechanics in detail in our investment property capital gains tax guide.

NSW also charges land tax on investment properties (your principal place of residence is exempt). For the 2026 land tax year, the general threshold sits at $1,075,000 of combined NSW landholdings, with a rate of $100 plus 1.6% above the threshold. The premium threshold is $6,571,000. Both thresholds were frozen at these values from the 2024-25 NSW State Budget and have not moved with valuation creep.

This article contains general information only. Tax outcomes depend on your specific circumstances and the structure used to hold the property (individual, joint, trust, SMSF). For investors using a self-managed super fund to hold property, see our SMSF home loans guide for the lender shortlist and Limited Recourse Borrowing Arrangement (LRBA) structuring rules. Speak to your accountant before relying on any tax outcome described here. For more on this, see our how SMSF property loans work in 2026 guide.

How an Investment Property Loan Broker Helps

A mortgage broker compares lender policies and products on your behalf, then prepares and submits the application to the lender most likely to approve the loan structure you need. For a straightforward owner-occupier purchase at a major bank, the value-add over walking into the bank yourself is real but modest. For investment property finance, the gap widens significantly, because the lender-side variables we covered in the borrowing capacity section above are not visible to the borrower or to bank-employed lenders.

What a Broker Actually Does That a Banker Can’t

A bank-employed lender can sell you that bank’s product. They cannot tell you that the same application will service for $200,000 more at a different lender. They cannot benchmark a tier-two lender’s rental shading policy against a non-bank’s buffer rate. They cannot tell you when their own bank’s exposure ceiling is the constraint and another lender would not see that constraint at all.

A broker does all of those things, structurally. With access to 52+ lenders across major banks, second-tier lenders, and non-bank specialists, our role is to map your specific borrowing profile (income type, existing portfolio, ownership structure, credit profile, deposit source) against the lenders most likely to give you the best outcome on borrowing capacity, rate, and structure. For investors specifically, that mapping is where most of the value is.

Brokers are also bound by the Best Interests Duty (BID) under the National Consumer Credit Protection Act, which legally requires us to recommend a loan that is in your best interests, not the broker’s. Banks have no equivalent obligation to their customers.

Are There Downsides to Using a Broker?

Yes. The honest list:

- Lender panel limits. Brokers do not have access to every lender. A typical aggregator panel covers 30 to 60+ lenders, but some smaller specialists, some direct-to-consumer products, and some mutual-only deals sit off-panel. Always ask what is on the panel.

- Commission disclosure. Brokers are paid by the lender, not the borrower (in almost all residential cases). The Royal Commission and ASIC have flagged that commission-based pay can in principle bias recommendations. BID is the legislative safeguard; commission disclosure on every application is the procedural safeguard. The perception of conflict remains a legitimate consumer concern to address openly.

- Clawback risk passed to the borrower. If you discharge or refinance the loan within one to two years of settlement, the lender claws back commission from the broker. Some brokers pass that clawback on to the borrower as a fee. Always ask upfront whether your broker has a clawback fee and what triggers it. We do not charge clawback fees at MWA.

- Variable broker quality. Brokers operate as individuals or small businesses. Outcomes vary by experience, lender knowledge, and willingness to fight escalations. A weak broker is worse than going direct. Ask how long the broker has been operating, what their lender panel is, and how many investment property loans they wrote last year.

The downsides are real. They are also addressable. Used well, a broker for an investment property loan is one of the highest-leverage relationships a portfolio investor has.

Costs and Fees Beyond the Interest Rate

The total cost of an investment property loan extends well beyond the headline rate:

- Lender application and settlement fees. Typically $0 to $750.

- Lender ongoing fees. $0 to $400 per year for package products; $0 for no-frills variable products.

- Lender Mortgage Insurance (LMI) if your deposit is under 20% ($6,000 to $15,000+ on a $560,000 loan, generally tax-deductible over five years).

- NSW transfer duty (stamp duty). Investors do not get the First Home Buyer Assistance Scheme concession. Standard residential rates apply from the first dollar. On a $700,000 investment property purchase the NSW duty is $25,912; on $850,000 it is $32,662; on $1,000,000 it is $39,412. Transfer duty figures are based on rates effective 1 July 2025, sourced from Revenue NSW.

- Conveyancer or solicitor. $1,500 to $3,500.

- Building and pest inspection. $400 to $700.

- Lender valuation. Sometimes free, sometimes passed through at $200 to $500. We cover the lender’s valuation process in our guide on how the bank values your property.

- Council rates, strata, and insurance. Holding costs from settlement onward.

- NSW land tax if your combined NSW landholdings exceed $1,075,000 unimproved value.

Account for these on top of the deposit when planning the purchase.

How to Apply for an Investment Property Loan

The application process for an investment loan is broadly the same as an owner-occupier loan, but the document load is heavier and the assessment is tighter. The process at a high level:

- Initial discovery. Map borrowing capacity against current portfolio, income, and structure. This is where we identify the right lender shortlist before any application is submitted.

- Pre-approval. Conditional approval from a lender against the verified borrower profile, valid for 60 to 90 days at most lenders.

- Property purchase and valuation. Once you have signed a contract, the lender orders a valuation against the property. The valuation outcome can change the LVR and the loan amount.

- Full assessment and unconditional approval. Lender re-assesses serviceability against the actual property and rental estimate. Unconditional approval is the green light to settle.

- Settlement. Funds drawn, security registered, property transferred to your name. Conveyancer and lender coordinate the date.

- Post-settlement. Property manager engaged, loan account active, first repayment scheduled. Tax-deductible expense tracking begins from settlement day.

Documents you will typically need: two recent payslips, two years of tax returns and notices of assessment (especially if self-employed or with rental income), current loan statements for any existing debts, three months of statements for transaction and credit accounts, a copy of the contract of sale, and any rental appraisal letter for the new property.

Frequently Asked Questions

How much deposit is required for an investment property?

The standard answer is 20% of the purchase price (an 80% LVR loan). This is the cleanest path and avoids Lenders Mortgage Insurance. A 10% deposit is achievable at most lenders with LMI applied (typically $6,000 to $15,000 in extra cost). There are also some lenders that will accept a 5% deposit, but the LMI premium becomes quite expensive as do the interest rates. If you already own a property with usable equity, you can use that equity as the deposit on the new investment loan with no cash deposit at all. The usable equity formula is current property value × 80% minus your existing mortgage balance.

Can I borrow 100% for an investment property?

Not as a stand-alone product from mainstream lenders in 2026. A true 100% LVR investment loan is not a current Australian bank product. Three structures get you close: a guarantor structure under a family security guarantee (Westpac, St.George, ANZ, and others), where a family member’s property equity provides additional security; an equity release from your existing property to fund the deposit (technically an 80% LVR loan with the deposit funded by equity); or, for select professionals, a 90 to 95% LVR product with an LMI waiver under a professional package. Talk to a broker about which structure fits your situation.

What is the 1% rule and does it apply in Australia?

The 1% rule is a US property heuristic: monthly rent should be at least 1% of the purchase price (implying about a 12% gross annual yield). It does not apply in Australia. As at April 2026, Sydney’s gross rental yield is approximately 3.0 to 3.1% annually, Melbourne sits near 3.5%, and the national gross rental yield is 3.57% (CoreLogic / Cotality data). On a Sydney median property, that translates to roughly 0.25% monthly rent-to-price, about a quarter of the 1% rule’s required ratio. Use Australian-specific yield benchmarks instead, and read our guide on rental yield calculator for the math that does apply locally.

How much do I need to earn for a $700,000 investment loan?

Using April 2026 inputs (investor variable rate 6.71%, 30-year P&I, 80% LVR, $3,500 monthly declared living expenses, 80% rental shading at a 3% gross yield, no other debts), the indicative combined gross PAYG income required is approximately $125,000 at an APRA-regulated lender (3% buffer) and approximately $115,000 at a non-APRA lender (2% buffer). The 8 to 10% gap reflects the buffer differential alone. Real-world capacity depends on your specific circumstances, and a lender-by-lender comparison is where a broker adds the most value.

Should I use a mortgage broker for an investment loan?

For most investors, yes. The reason is structural: the variables that determine borrowing capacity at any given lender (assessment buffer, rental shading, treatment of existing debt, exposure ceilings, treatment of negative-gearing tax effect) are not visible to the borrower and not negotiable when you walk into a single bank. A broker maps your profile against the lender shortlist most likely to deliver the best outcome on capacity, rate, and structure. The downsides (panel limits, commission perception, clawback risk, variable broker quality) are real and addressable. Ask any broker you are considering how many investment property loans they wrote last year, what is on their panel, and whether they charge a clawback fee.

Speak to a Broker Who Has Seen This Before

Investment property finance rewards experience. Patrick O’Brien has been writing residential and investment loans since 2001, and Mortgage World Australia has access to 52+ lenders across major banks, second-tier lenders, and non-bank specialists. If you have been told no, capped, or asked to wait by your existing bank, the next call is the most useful one.

Speak to a mortgage broker at Mortgage World Australia.

Patrick O’Brien, Director and Mortgage Broker since 2001.

This article contains general information only and does not constitute financial advice. Your personal financial situation, objectives and needs have not been considered. Before acting on any information, you should consider its appropriateness to your circumstances. Speak to a qualified mortgage broker for advice tailored to your situation. Mortgage World Australia Pty Ltd is a credit representative (CR No. 396946) of Mortgage Specialists Pty Ltd (Australian Credit Licence No. 387025).

Patrick is a Director and a Home Loan Specialist. He has been helping Australians with home loans since 2001. Prior to working as a mortgage broker Patrick was employed by Macquarie Bank for 3 years and also worked as an accountant for a publicly listed company. Patrick’s qualifications include:

Bachelor of Business, UTS Sydney. Majored in accounting and sub-majored in Finance and Marketing.

Diploma of Finance and Mortgage Broking Management FNS50310

Certificate IV in Financial Services (Finance/Mortgage Broking) FNS40804

Ready to Take the Next Step?

Whether you’re looking to buy your first home, refinance, or explore investment opportunities, Mortgage World Australia is here to help.

Fill out the contact form below, and one of our expert mortgage brokers will be in touch shortly to discuss your needs and guide you through your options.

Get Started Today!