How much deposit for a house: 2026 guide

How much deposit do you need for a house in Australia?

On this page ▾

- Minimum deposit requirements in Australia

- House deposit calculator: how much do you need by property price?

- First home buyer deposit options

- Low deposit home loan programs

- What counts as genuine savings?

- Lenders mortgage insurance (LMI) and low deposit loans

- Frequently asked questions

- Ready to move forward?

Minimum deposit requirements in Australia

Your deposit is your financial commitment to the purchase. Lenders use this to assess your ability to save and manage money. The minimum deposit requirement depends on three factors: the lender’s policy, your borrowing profile, and whether you qualify for government support.The standard benchmark is 20%. At this level, your Loan-to-Value Ratio (LVR), the amount you’re borrowing divided by the property’s value, sits at 80%. No mortgage insurance is required, and you’ll access the best interest rates.Below 20%, you’ll pay Lenders Mortgage Insurance (LMI). LMI is insurance that protects the lender if you default. You pay the premium, but the protection benefits the lender. LMI costs typically range from 0.5% to 6% of the borrowed amount, depending on your loan size, LVR, and lender. For a $500,000 property with a 10% deposit, LMI is approximately $8,200 (Helia estimate, excluding stamp duty on the premium).Government schemes now allow deposits as low as 5%. The Australian Government 5% Deposit Scheme (expanded and rebranded 1 October 2025) lets eligible first home buyers purchase with just 5% down. There’s no LMI, no income caps, and no government contribution required. You must provide the full 5% yourself.For single parents with dependent children, a separate stream offers a 2% deposit option.The minimum deposit for a house in Australia is typically 5% for eligible first home buyers using government-supported schemes, or 10–20% with standard lenders. At 20%, you avoid mortgage insurance entirely. Government schemes offer pathways to purchase with lower deposits but come with specific eligibility criteria and property price caps.House deposit calculator: how much do you need by property price?

To make this concrete, here’s how deposits work across different property prices:

To make this concrete, here’s how deposits work across different property prices:| Property price | 5% deposit | 10% deposit | 20% deposit |

|---|---|---|---|

| $300,000 | $15,000 | $30,000 | $60,000 |

| $500,000 | $25,000 | $50,000 | $100,000 |

| $700,000 | $35,000 | $70,000 | $140,000 |

| $1,000,000 | $50,000 | $100,000 | $200,000 |

Deposit for a $300,000 house

At $300,000, the deposit decisions are:- 5% deposit ($15,000): Borrow $285,000. Eligible first home buyers can use the government scheme to avoid LMI.

- 10% deposit ($30,000): Borrow $270,000. Pay LMI (approximately $3,900 based on Helia estimates, excluding stamp duty on premium).

- 20% deposit ($60,000): Borrow $240,000. No LMI; access best rates.

Deposit for a $500,000 house

At $500,000, deposit choices have real financial weight:- 5% deposit ($25,000): Borrow $475,000. Government scheme eliminates LMI. Total monthly repayment (6% rate, 30 years) approximately $2,850.

- 10% deposit ($50,000): Borrow $450,000. LMI approximately $8,200. Total monthly repayment approximately $2,750.

- 20% deposit ($100,000): Borrow $400,000. No LMI. Total monthly repayment approximately $2,400.

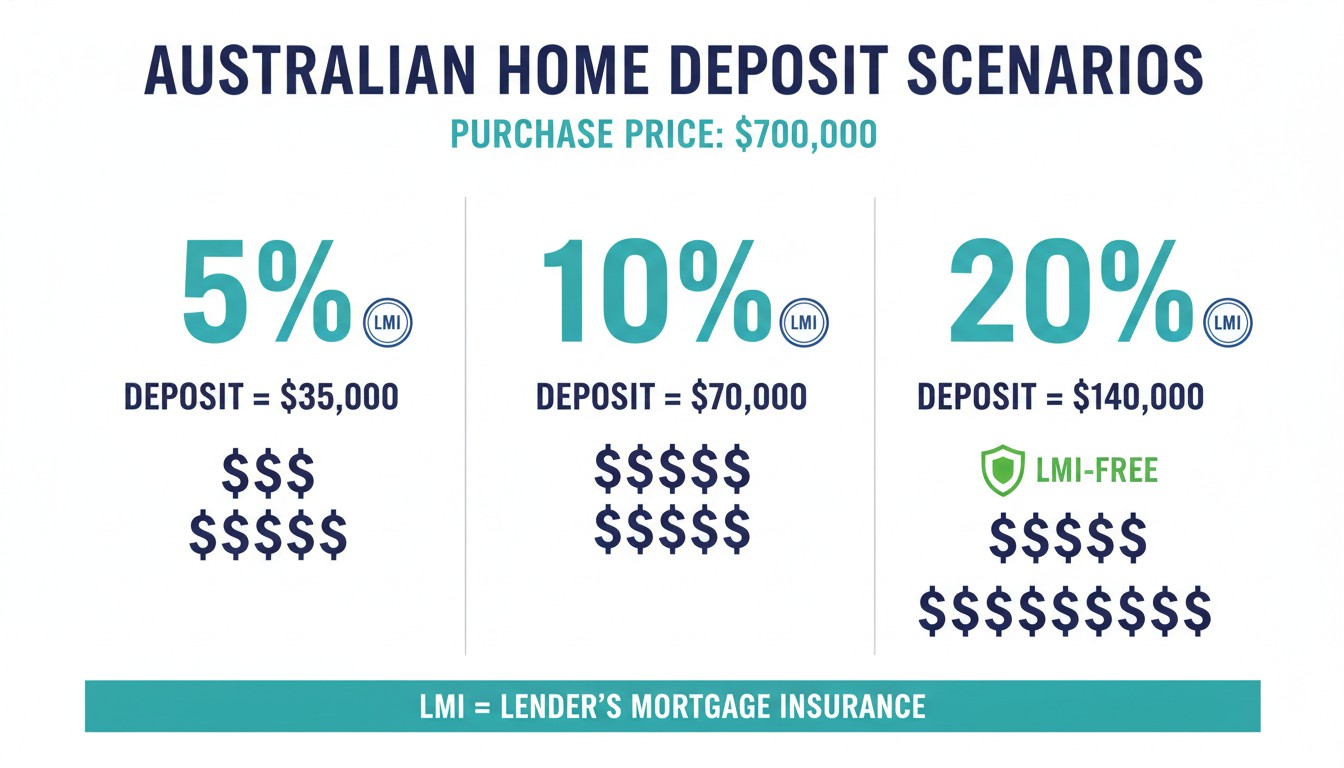

Deposit for a $700,000 house

At higher price points, deposit timing becomes a longer-term strategy:- 5% deposit ($35,000): Borrow $665,000. Government scheme available to eligible first home buyers (no LMI). Monthly repayment (6% rate) approximately $3,990.

- 10% deposit ($70,000): Borrow $630,000. LMI $14,000–$18,000. Monthly repayment approximately $3,780.

- 20% deposit ($140,000): Borrow $560,000. No LMI. Monthly repayment approximately $3,360.

First home buyer deposit options

If you’re buying your first home, you have access to deposit-reducing pathways unavailable to other buyers.Australian Government 5% Deposit Scheme

The 5% Deposit Scheme is the most powerful option for first home buyers right now. Here’s what you need to know:- Deposit: 5% of the property price (or 2% for eligible single parents with dependent children)

- No LMI: Government guarantee replaces the insurance premium, saving you thousands

- No income caps: Universal eligibility regardless of salary (from 1 October 2025)

- Owner-occupier only: Investment properties don’t qualify

- Property price cap (NSW): $1,500,000 for capital city areas including Sydney and Parramatta (from 1 October 2025). Regional NSW has a separate lower cap. Check your eligibility at nhfic.gov.au before purchasing.

- Application: Through participating lenders only. Not all brokers can access this scheme.

- Pre-approval requirement: You must have a 90-day search window after pre-approval to apply

- Loan term: Maximum 30 years

NSW First Home Buyers Assistance Scheme (transfer duty exemption)

Beyond the federal scheme, NSW offers a separate benefit: transfer duty (stamp duty) exemption for first home buyers.- Properties up to $800,000: Full exemption from transfer duty

- Properties $800,001–$999,999: Partial concession (graduated reduction as price increases)

- Requirement: You must move into the property within 12 months and live there continuously for at least 12 months

- Eligibility: Australian citizen or permanent resident aged 18+

Low deposit home loan programs

If you don’t qualify for government schemes, several lender programs can help you buy with less than 20% down.Lender low-deposit programs (typically 10% minimum):- Commonwealth Bank, NAB, Westpac, and ANZ all offer 5% deposit home loans with LMI payable

- LMI is factored into the loan and paid off over the life of the mortgage

- Interest rates may be slightly higher than 20% deposit borrowers

- Some lenders require genuine savings evidence (6–12 months of deposit accumulation) before approval

What counts as genuine savings?

Genuine savings refers to evidence that you’ve accumulated your deposit through regular saving, not through gifted funds or loans. Some lenders require 6–12 months of bank statements showing consistent deposits into a savings account. Others waive this requirement for strong borrowers.Lenders ask for genuine savings to demonstrate financial discipline. A borrower who has saved $50,000 over two years shows different financial behaviour than one who received the deposit as a gift.What typically qualifies:- Funds held in your own savings account for at least 3 months

- Term deposit or managed funds held for at least 3 months

- First Home Super Saver Scheme (FHSS) withdrawals

- Equity in an existing property

- Gifted funds (typically require a letter from the gift giver confirming the funds are a gift and not a loan — some lenders still require a statutory declaration)

- Tax refunds deposited less than 3 months before application

- Sale proceeds from assets with no savings history

- Rental history as savings

Lenders mortgage insurance (LMI) and low deposit loans

Lenders mortgage insurance (LMI) is a one-off premium paid when your LVR exceeds 80% (deposit less than 20%). It protects the lender, not you, but you pay the cost.LMI is typically capitalised into your loan rather than paid upfront. For a $500,000 property with a 10% deposit ($50,000) and LMI of approximately $8,200, you’d borrow approximately $458,200 total.Approximate LMI costs by deposit (on a $500,000 property):| Deposit | LVR | Approximate LMI |

|---|---|---|

| 5% ($25,000) | 95% | ~$14,000 |

| 10% ($50,000) | 90% | ~$8,200 |

| 15% ($75,000) | 85% | ~$4,400 |

| 20% ($100,000) | 80% | None |

Frequently asked questions

What’s the average home deposit in Australia? Most first-time buyers aim for 20% to avoid mortgage insurance. Government schemes have shifted this trend, with many first home buyers now purchasing with 5–10%.Can I use a gift for my deposit? Yes. Most lenders accept gifted deposits and no longer require a statutory declaration — a letter from the gift giver confirming the funds are a gift (not a loan) is usually sufficient, though some lenders still require a declaration. A small number of lenders will treat a gifted amount as genuine savings once it has been sitting in your account for as little as one day. Policies vary significantly, so it is worth checking early.What if I can’t save 20%? The Australian Government 5% Deposit Scheme is your fastest path if you’re a first home buyer. If you don’t qualify, a 10% deposit with LMI is common. We can help you access lenders with flexible policies.Does a larger deposit guarantee a better interest rate? Generally, yes. A 20% deposit is more attractive to lenders than 10%. However, rates vary by lender, loan purpose, and your personal profile. It’s worth comparing offers at your specific deposit level rather than assuming you need 20%.How long does it take to save a deposit? For a $500,000 property, saving $100,000 (20%) at $1,000/month takes over eight years. Saving $25,000 (5%) under a government scheme takes roughly two years at the same rate. Starting early and automating savings helps.Can I use superannuation for my deposit? Under the First Home Super Saver Scheme rules, eligible first home buyers can release up to $50,000 from super to use as a deposit. Specific conditions apply around contribution history and loan timing. Check with a tax advisor before exploring this option.Is a deposit the same as a down payment? In Australia, these terms are used interchangeably. Your deposit is your upfront payment toward the purchase; the remainder is the loan.Ready to move forward?

The deposit you save determines your borrowing capacity, your interest rate, and the total cost of your home. Understanding your options (government schemes, genuine savings strategies, guarantor arrangements, and lender programs) puts you in control.Speak to our mortgage brokers today. We’ll assess your situation, show you the deposit pathways available to you, and connect you with lenders offering real value for your specific profile. Since 2001, we’ve helped Australians navigate this decision with tailored guidance based on 25+ years of lending insight.Explore your home loan options with us.This article contains general information only and does not constitute financial advice. Your personal financial situation, objectives and needs have not been considered. Before acting on any information, you should consider its appropriateness to your circumstances. Speak to a qualified mortgage broker for advice tailored to your situation. Mortgage World Australia Pty Ltd is a credit representative (CR No. 396946) of Mortgage Specialists Pty Ltd (Australian Credit Licence No. 387025).

Patrick is a Director and a Home Loan Specialist. He has been helping Australians with home loans since 2001. Prior to working as a mortgage broker Patrick was employed by Macquarie Bank for 3 years and also worked as an accountant for a publicly listed company. Patrick’s qualifications include:

Bachelor of Business, UTS Sydney. Majored in accounting and sub-majored in Finance and Marketing.

Diploma of Finance and Mortgage Broking Management FNS50310

Certificate IV in Financial Services (Finance/Mortgage Broking) FNS40804

Ready to Take the Next Step?

Whether you’re looking to buy your first home, refinance, or explore investment opportunities, Mortgage World Australia is here to help.

Fill out the contact form below, and one of our expert mortgage brokers will be in touch shortly to discuss your needs and guide you through your options.

Get Started Today!