Lenders Mortgage Insurance (LMI): Complete Guide 2026

Lenders Mortgage Insurance (LMI): How It Works & How to Avoid It

By Patrick O’Brien, Director and Home Loan Specialist at Mortgage World Australia — in the industry since 2001.Most borrowers find out about lenders mortgage insurance (LMI) at exactly the wrong moment: deep into a loan application, emotionally committed to a property, and suddenly facing a cost that can run to $15,000 or more. In 25 years, I’ve sat across from more first-time buyers facing that shock than I can count.It feels like a hidden tax — and the frustration is understandable. But understanding LMI before you start looking at properties changes everything. You can price it accurately, decide whether to absorb the cost or wait, and in many cases avoid it entirely through strategies that most people never hear about.This guide explains what lenders mortgage insurance is, when it applies, how much it costs, and the concrete strategies available to reduce or eliminate it.What is lenders mortgage insurance?

On this page ▾

Definition, purpose, and who it protects

LMI is a contract between your lender and an LMI provider. In Australia, there are two main providers: Helia (operating since 1965 and the country’s leading LMI provider) and QBE. You don’t get to choose which insurer your lender uses — that’s determined by the lender’s existing arrangements with each insurer.The loan-to-value ratio (LVR) is central to how LMI works. It’s the amount you’re borrowing as a percentage of the property’s value. If you’re borrowing $400,000 for a $500,000 property, your LVR is 80%. The higher your LVR, the lower your deposit and the higher the risk the lender takes on.LMI exists to allow lenders to extend credit at higher LVR levels — say, 90% or 95% — without carrying that additional risk on their own balance sheet. For you, LMI is the price of entering the market sooner without a full 20% deposit. It’s a trade-off: pay the insurance premium now, or wait to save 20%.One practical detail: LMI premiums are typically added to your home loan balance rather than paid upfront. This means you’ll pay interest on the LMI premium over the life of the loan. A $15,000 LMI premium added to a 30-year loan at current standard rates adds considerably more than that headline figure to your total borrowing cost.When do you need to pay LMI?

Lenders mortgage insurance applies when your deposit is less than 20% of the property’s purchase price — specifically, when your LVR exceeds 80%.The 80% LVR threshold

LMI isn’t triggered at exactly 80% LVR. A 20% deposit produces an LVR of exactly 80%, and no LMI is charged. The requirement kicks in the moment you borrow more than 80% of the property’s value.Example: You’re purchasing a property for $650,000. You have $90,000 saved — about 13.8% of the purchase price. Your LVR would be 86.2%, so LMI applies. If you had $130,000 saved — 20% — your LVR would be 80% and LMI would not be required.Here’s a reality check: the lender uses their own valuation of the property, not the purchase price. If the lender’s valuation comes in lower than the price you’ve agreed to pay, your effective LVR is higher than you calculated. This is more common in markets where prices are moving quickly or in property types lenders view cautiously. It’s worth asking your broker to flag this risk early.Investment versus owner-occupied property

LMI applies to both owner-occupied and investment property loans, with the same 80% LVR threshold. But here’s where it diverges: the rates are higher for investment properties.Investment property loans attract higher LMI premiums than owner-occupied loans at the same LVR. Lenders and insurers classify investment borrowers as carrying greater risk, partly because investors are more likely to sell under financial pressure, which can mean the lender recovers less from a distressed sale.Some lenders also cap the maximum LVR for investment loans below the 95% limit available on owner-occupied products. If you’re buying an investment property with a small deposit, verify both the LMI premium and the maximum LVR limit with your broker before committing.How much does LMI cost?

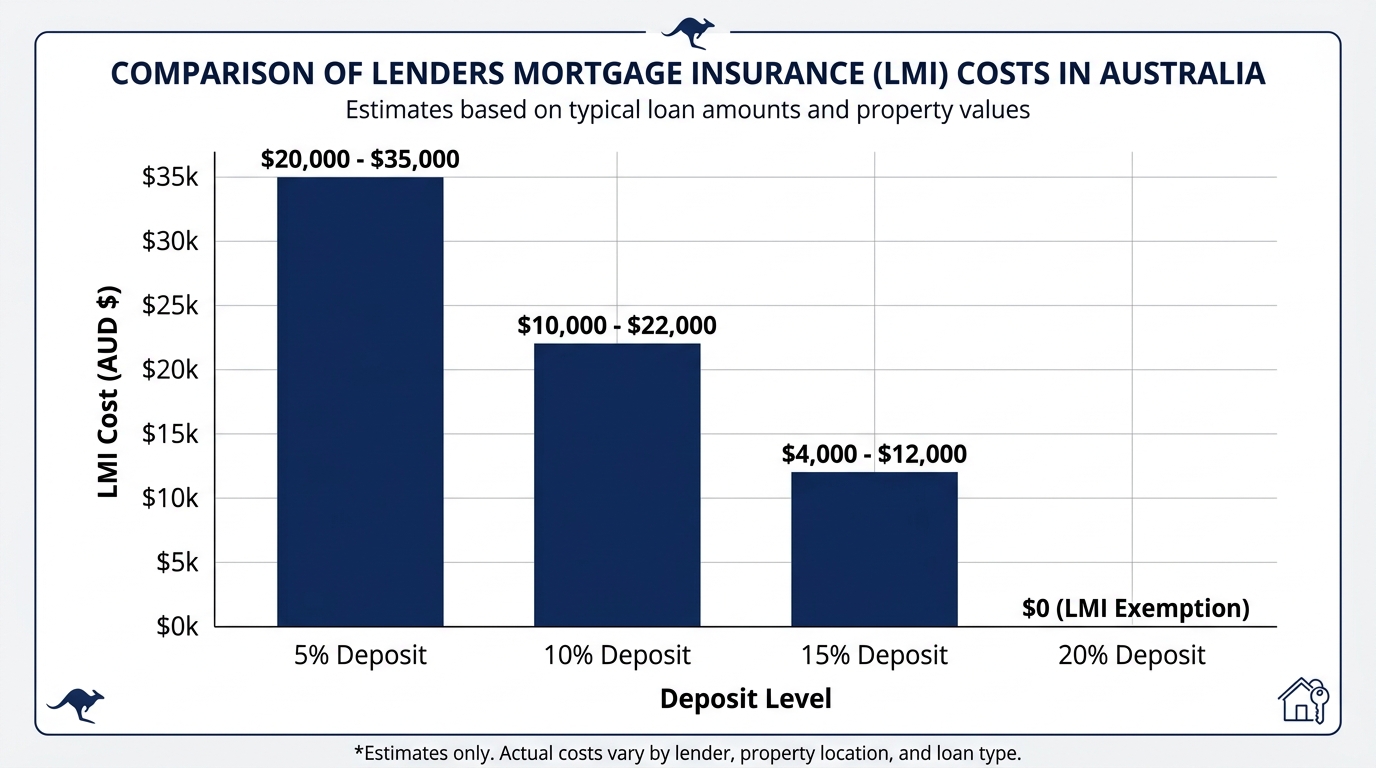

LMI can cost anywhere from a few thousand dollars to well over $30,000, depending on your loan amount, LVR, and property type. Behind the deposit itself and stamp duty, it’s one of the largest upfront costs in a home purchase.On a $500,000 purchase with a 5% deposit, LMI typically costs between $15,000 and $19,000, depending on your lender, which insurer they use, and whether the property is owner-occupied or investment. On an $800,000 property at the same deposit level, the cost scales considerably higher — into the $24,000–$30,000 range.

LMI can cost anywhere from a few thousand dollars to well over $30,000, depending on your loan amount, LVR, and property type. Behind the deposit itself and stamp duty, it’s one of the largest upfront costs in a home purchase.On a $500,000 purchase with a 5% deposit, LMI typically costs between $15,000 and $19,000, depending on your lender, which insurer they use, and whether the property is owner-occupied or investment. On an $800,000 property at the same deposit level, the cost scales considerably higher — into the $24,000–$30,000 range.LMI cost examples by deposit level

The table below shows approximate LMI costs for owner-occupied properties at various deposit levels. These are estimates; actual costs vary by lender, insurer, and your individual profile.| Property Value | Deposit | Deposit % | LVR | Approx. LMI Cost |

|---|---|---|---|---|

| $500,000 | $25,000 | 5% | 95% | $15,000–$19,000 |

| $500,000 | $50,000 | 10% | 90% | $8,000–$12,000 |

| $500,000 | $75,000 | 15% | 85% | $3,000–$5,500 |

| $500,000 | $100,000 | 20% | 80% | $0 |

| $800,000 | $40,000 | 5% | 95% | $24,000–$30,000 |

| $800,000 | $80,000 | 10% | 90% | $13,000–$19,000 |

How is LMI calculated?

LMI isn’t a flat fee or a simple percentage of your deposit shortfall. It’s calculated using five factors, and each one can swing your final bill significantly.LVR and deposit amount impact

Your LVR is the primary driver. LMI providers apply a tiered rate schedule: the higher the LVR, the higher the rate applied to the loan amount. Moving from 95% to 90% LVR — an additional 5% deposit — can reduce LMI cost by 30–50%, depending on the loan size.This non-linear structure means the last few percentage points of deposit saving are often the most valuable. Going from 8% deposit to 10% deposit saves more in LMI than going from 5% to 8%.Loan amount and property type

The LMI premium is calculated as a percentage of the total loan amount — not the deposit shortfall. A higher loan means a higher premium, even at the same LVR. A $900,000 loan at 90% LVR attracts substantially more LMI than a $500,000 loan at the same LVR, even though both borrowers have a 10% deposit.Property type adds another layer. Investment loans carry a higher LMI rate than owner-occupied loans at the same LVR and loan amount. This is a fixed structural difference — both Helia and QBE apply higher rates to investment borrowing.Employment status and lender selection

Employment status affects how insurers assess risk. Full-time employees are the lowest risk. Casually employed, self-employed, or contract workers may face higher LMI premiums, stricter maximum LVR limits, or both. Some lenders won’t accept certain employment types above specific LVR thresholds.The lender you choose also matters. Your lender determines which insurer underwrites your LMI — Helia or QBE — and both operate their own rate schedules. On top of that, individual lenders negotiate their own terms with each insurer, meaning the LMI cost for the same borrower and property can vary meaningfully across lenders. This isn’t visible to you when applying directly to a bank; it’s the kind of comparison a broker with access to multiple lenders can surface.Ways to avoid or reduce LMI

There are five practical approaches to avoiding or reducing LMI. Which is right for you depends on your deposit, timeline, income profile, and whether you’re buying owner-occupied or investment. Over 25 years, these are the only five strategies that actually move the dial for our clients.

There are five practical approaches to avoiding or reducing LMI. Which is right for you depends on your deposit, timeline, income profile, and whether you’re buying owner-occupied or investment. Over 25 years, these are the only five strategies that actually move the dial for our clients.Growing your deposit to 20%

The straightforward approach: save until your deposit reaches 20% of the purchase price. At an LVR of 80%, LMI does not apply.The trade-off is time in the market. In Sydney and western Sydney, property prices can move faster than a deposit grows. A mortgage broker can model both paths — paying LMI now and entering the market versus waiting to hit 20% — so you can compare the actual cost difference over a 5- or 10-year horizon. Sometimes paying LMI and buying two years earlier is substantially cheaper than waiting, even accounting for the premium.Finding lenders that discount or waive LMI

Some lenders offer LMI waivers for borrowers in certain professions — typically medical practitioners, dentists, lawyers, and accountants — based on the view that their income stability and earning trajectory represent a lower default risk. These arrangements can allow eligible borrowers to purchase with deposits as low as 10%, and in some cases, lower, with no LMI payable.Profession waivers vary significantly between lenders. The professions covered, the maximum LVR, and the loan size limits differ from one lender to the next.Our mortgage brokers have access to 52+ lenders and can identify which LMI waiver options apply to your specific situation. See our dedicated page on LMI waivers through broker networks for more details.Using a family guarantor

A guarantor arrangement lets a family member — most commonly a parent — use the equity in their own property as additional security for your loan. When structured correctly, this can eliminate the need for LMI entirely. The lender’s risk is secured against two properties rather than one, removing the need for LMI to cover the gap.The arrangement carries genuine obligations on the guarantor’s side. Their property is pledged as security, which affects their own borrowing capacity and creates real financial risk if you default. The guarantee is typically limited — structured to cover only the deposit gap, not the whole loan — which reduces (but does not eliminate) the guarantor’s exposure.If you’re considering this path, work through the structure with a mortgage broker who can explain the obligations clearly to both parties. See our detailed guide on the guarantor loan option before committing.Government 5% Deposit Scheme

The Australian Government 5% Deposit Scheme allows eligible first home buyers to purchase a property with a 5% deposit without paying LMI. Instead of requiring LMI, Housing Australia provides a guarantee of up to 15% of the property’s value to the lender — covering the gap between your 5% deposit and the 80% LVR threshold. For eligible single parents, the scheme extends to a 2% deposit with a guarantee of up to 18%.From 1 October 2025, the scheme underwent a significant expansion. Income caps were removed entirely. Waitlists were eliminated. And place limits became unlimited, meaning any eligible first home buyer can now apply without competing for a finite number of spots. This was a material change — in previous years, annual place limits meant many eligible applicants missed out.The key ongoing condition: you must live in the property as owner-occupier. If that condition isn’t met, the guarantee may lapse and LMI could become payable.For a full overview of what’s available to first home buyers in NSW — including grants and stamp duty concessions alongside this scheme — see our guide to Australian Government 5% Deposit Scheme.Comparing quotes across lenders

LMI costs are not uniform across the market. Because Helia and QBE each operate separate rate schedules, and because individual lenders negotiate different terms with each insurer, the LMI cost for the same borrower on the same property can vary by thousands of dollars depending on which lender you use.A borrower applying directly to a single bank sees one quote. A broker working with a network of 52+ lenders can compare LMI costs across lenders who use different insurers under different rate structures. The lender with slightly higher interest rates might offer substantially lower LMI — making the total cost of borrowing lower despite the apparent rate disadvantage.For a full breakdown of available approaches, see our complete guide to avoiding LMI.LMI and government schemes

Government home ownership programs interact with LMI in different ways. Some eliminate it; others sit alongside it. Understanding the distinction matters when you’re comparing options.Australian Government 5% Deposit Scheme

As described above, the Australian Government 5% Deposit Scheme is the most direct LMI alternative available to first home buyers. The government guarantee replaces LMI — you get the benefit of a low-deposit loan without paying the insurance premium that would otherwise apply.The scheme is administered by Housing Australia through a panel of participating lenders. Not every lender in Australia is on that panel, which means your choice of lender is constrained when using this scheme. If you want to use the scheme but also compare rates across participating lenders, a mortgage broker who works with multiple panel lenders is the most efficient way to do that.Property price caps apply to scheme purchases and vary by location. For buyers in western Sydney and surrounding areas, the NSW price caps determine the maximum property value eligible under the scheme. These caps are set by the government and updated periodically — confirm the current figures via Housing Australia or with your broker before making an offer.How schemes interact with LMI

The Help to Buy scheme operates differently from the 5% Deposit Scheme. Under Help to Buy, the federal government co-purchases a share of your property — up to 40% for new builds, up to 30% for existing homes — reducing the loan amount you need to borrow. The idea is to lower your monthly repayments by reducing your loan size.Unlike the 5% Deposit Scheme, Help to Buy does not automatically waive LMI. Whether LMI applies depends on the LVR on the portion you’re borrowing. If the loan amount you take out — after accounting for the government’s co-purchase contribution — results in an LVR above 80%, LMI may still be payable on that loan.This is a meaningful structural difference. When comparing these two schemes, how they treat LMI is one of the variables to understand before deciding which path fits your situation.Frequently asked questions

Can you get lenders mortgage insurance refunded?

In most cases, no. Helia — Australia’s leading LMI provider — no longer offers refunds through any of their lenders. If you repay your loan and move on, the LMI premium you paid is gone.QBE has a more limited refund window. A refund may apply if the insured mortgage is repaid in full within the first year after settlement, but the lender must notify QBE within 30 days of the loan being discharged. The refund goes to the lender, not directly to you as the borrower. Whether your lender passes that refund on is a separate question — many don’t.Is LMI refundable when you refinance?

Generally, no. When you refinance to a new lender, your existing LMI policy does not transfer. If your LVR at the time of refinancing is still above 80%, you’ll likely be charged a new LMI premium by the new lender. The premium you originally paid is not credited or refunded.Helia does offer a discount on LMI premiums for borrowers who refinance internally — staying with the same lender and restructuring their loan. That’s not available if you’re switching lenders.Before refinancing, while your LVR is still above 80%, calculate the cost of a new LMI premium. It can erode a significant portion — sometimes all — of the interest savings you were expecting from the rate difference.What happens if you default on your loan when LMI is in place?

LMI protects the lender, not you. If you default and the lender sells the property for less than the outstanding loan amount, the LMI insurer covers the lender’s shortfall. The insurer then has the legal right to pursue you for the amount they’ve paid out.This isn’t a theoretical risk. In practice, paying LMI does not protect you from financial consequences if your circumstances change and you can no longer service the loan. The insurance exists solely to protect the lender’s position.Do investment properties have different LMI rules?

Yes, in two ways. First, LMI premiums for investment loans are higher than for owner-occupied loans at the same LVR — this applies across both Helia and QBE. Second, some lenders cap the maximum LVR they’ll lend against for investment properties at 90% rather than 95%, which affects how small a deposit you can work with before being declined entirely.If you’re modelling an investment property purchase, factor in the higher LMI cost when calculating your net return. The cost difference between owner-occupied and investment LMI at the same LVR can run to several thousand dollars.Can you negotiate a lower LMI rate?

Not directly. LMI rates are set by the insurer — Helia or QBE — and you can’t negotiate with them. The insurer’s rate schedule is fixed for a given LVR, loan amount, and property type.What you can do is compare across lenders. Because different lenders negotiate different arrangements with each insurer, the LMI cost for the same borrower and property can vary across lenders — sometimes by thousands of dollars. A mortgage broker with access to 52+ lenders can compare these costs side by side. That’s exactly the kind of comparison that’s difficult to run yourself but straightforward with broker access.Ready to explore your options?

Here’s the reality: LMI can cost $15,000–$30,000 or more, but many of our clients avoid it entirely through one of the five strategies above. Whether it’s a government scheme, a profession waiver, a guarantor arrangement, or simply finding the lender with the lowest LMI cost for your deposit level, the right answer depends on your specific situation. The conversation that makes the difference happens before you commit to a lender.Our mortgage brokers have access to home loans in western Sydney across 52+ lenders and can map out the exact LMI cost and potential savings across your options. Talk to a mortgage broker in Parramatta or anywhere in western Sydney before committing to a lender. The right conversation upfront can save you thousands.Talk to Mortgage World Australia — we’ve been helping Australians navigate property finance since 2001.*This article contains general information only and does not constitute financial advice. Your personal financial situation, objectives and needs have not been considered. Before acting on any information, you should consider its appropriateness to your circumstances. Speak to a qualified mortgage broker for advice tailored to your situation.

Patrick is a Director and a Home Loan Specialist. He has been helping Australians with home loans since 2001. Prior to working as a mortgage broker Patrick was employed by Macquarie Bank for 3 years and also worked as an accountant for a publicly listed company. Patrick’s qualifications include:

Bachelor of Business, UTS Sydney. Majored in accounting and sub-majored in Finance and Marketing.

Diploma of Finance and Mortgage Broking Management FNS50310

Certificate IV in Financial Services (Finance/Mortgage Broking) FNS40804

Ready to Take the Next Step?

Whether you’re looking to buy your first home, refinance, or explore investment opportunities, Mortgage World Australia is here to help.

Fill out the contact form below, and one of our expert mortgage brokers will be in touch shortly to discuss your needs and guide you through your options.

Get Started Today!