Mortgage Broker vs Bank: Which Is Better for You?

Mortgage broker vs bank: which gets you the better home loan?

On this page ▾

- The core difference: one lender vs a panel of 52+

- How do mortgage brokers get paid? The commission breakdown in dollars

- Clawback explained, and why it actually protects you

- What Best Interests Duty (BID) legally requires that a bank employee can never match

- Worked example: same borrower, four banks, one broker

- When going direct to your bank IS the right choice

- Choosing a broker: the questions to ask before you sign anything

- Frequently asked questions

In most cases, a broker. The reason is simple: a bank can only sell you its own loans, while a broker can compare your scenario across an entire panel of lenders. The Mortgage and Finance Association of Australia (MFAA) reported that 76.7% of all new residential home loans in the December 2025 quarter were settled through brokers. That is the highest December-quarter share on record since the MFAA began tracking the series in 2013.

There are caveats worth knowing about, and we will get to them. There are also four scenarios where going directly to your bank is the right call.

This article covers what a broker actually does behind the scenes, how brokers get paid (with dollar figures on a $500,000 loan), what Best Interests Duty legally requires of a broker that a bank employee is not subject to, a worked example using current big four rates, and a clear list of when going direct still makes sense.

Since 2001, the team at Mortgage World Australia has settled loans through five interest rate cycles. We have sat on both sides of this question. You can read more about Patrick and how MWA works for the full background.

The core difference: one lender vs a panel of 52+

What a bank can and can’t offer you

A bank is a single lender. CBA can only sell you a CBA loan. Westpac can only sell you a Westpac loan. The branch lender or mobile lender will quote their best advertised rate, sometimes apply a discount that their pricing tier allows, and sometimes not. They cannot show you what NAB, Macquarie, Bankwest, or any of the dozens of smaller lenders are offering for the same scenario.

Suncorp Bank’s own piece on this question puts it directly: “A broker can potentially offer you a broader range of products.” That is a competitor admitting the structural point.

What a broker actually does behind the scenes

A broker holds a panel of lenders. At MWA we work with 52+ lenders through our aggregator, Specialist Finance Group. When you sit down with us, we look at your income, your deposit, your credit profile, your loan type, and your goals, then we filter the panel down to the lenders who will actually approve and price you well.

The work the bank rep does not do, because they cannot, is the comparison work. We do it for you. That is the full home loan service we run.

Why “more options” is not the same as “better outcome”

A panel of 52 only matters if it is used well. The job is not to drown you in options. It is to filter the panel down to two or three loans that fit your scenario, then explain the trade-offs in plain language so you can decide. Any broker who hands you a 12-page comparison and asks you to choose has not done their job.

How do mortgage brokers get paid? The commission breakdown in dollars

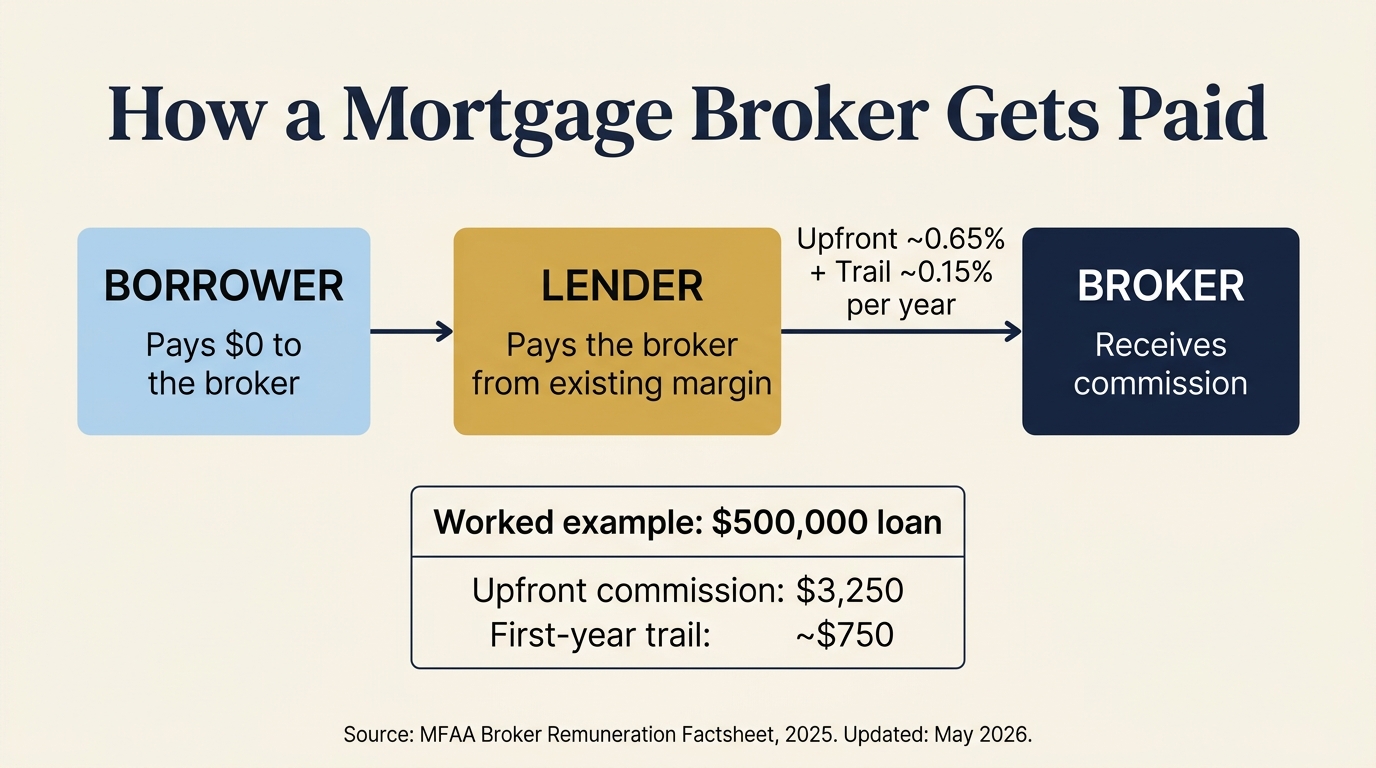

Upfront commission (around 0.65% of the loan amount)

The lender pays the broker an upfront commission once your loan settles. You do not pay it. The MFAA’s most recent broker remuneration data sets the industry standard at around 0.65% to 0.70% of the loan amount.

Trail commission (around 0.15% per year)

Trail is paid monthly by the lender on the outstanding balance for the life of the loan. The industry standard is around 0.15% per year. Trail is what pays the broker for staying involved years after settlement: rate reviews, structure changes, refinances when the market shifts.

Worked example: commission on a $500,000 and a $700,000 loan

| Loan amount | Upfront (0.65%) | First-year trail (0.15%) |

|---|---|---|

| $500,000 | $3,250 | around $750 |

| $700,000 | $4,550 | around $1,050 |

Trail reduces over time as you pay the principal down. The borrower never sees these amounts on a bank statement. They are paid lender-to-broker.

“Are mortgage brokers free?”

Yes, for the borrower in almost all standard residential cases. The lender pays the broker out of the same margin they would otherwise keep. You do not pay more for going via a broker. In many cases, you pay less because the broker found a sharper rate. Some complex commercial or SMSF loans may carry a fee, which the broker has to disclose to you in writing before you proceed.

Clawback explained, and why it actually protects you

Clawback is a provision that lets the lender reclaim some or all of the upfront commission from the broker if the loan is discharged or refinanced within a set window. You never pay clawback. It is a lender-to-broker mechanism.

The four big bank clawback rules (all different now)

For years, “typical 24 months, with 50% in year two” was the industry shorthand. That is no longer accurate. Each big four bank now applies its own rule:

| Lender | Year 1 (months 0-12) | Months 12-24 | After 24 months |

|---|---|---|---|

| CBA | 100% | Continuous taper from 50% down to 0% across months 13-24. | Nil |

| Westpac | 100% | 50% in months 12-18. Nil from month 18. | Nil |

| ANZ | 100% | Tapers from 50% down to 25% across months 12-18. Nil from month 18. | Nil |

| NAB | 100% | Sliding scale from around 50% at month 13 down to around 6% at month 24. | Nil |

Why this aligns the broker’s incentives with yours

A broker who churns a loan in month 6 to capture another upfront commission elsewhere loses the entire first commission. The structure makes long-tenure recommendations rational. When MWA recommends you refinance to a better rate two or three years later, we are doing it because the rate or product genuinely improves your position, not because there is a quick commission in it for us. You can estimate the repayment difference a better rate makes before you commit.

When clawback could create a conflict

A BID-compliant broker discloses the clawback risk if it might shape the recommendation. For example, a borrower mentioning they plan to sell within 12 months should be told that any refinance recommendation over the next year would trigger a clawback hit on the broker. The disclosure is in writing.

What Best Interests Duty (BID) legally requires that a bank employee can never match

BID in plain English

On 1 January 2021, Best Interests Duty came into force under Pt 3-5A of the National Consumer Credit Protection Act 2009. ASIC’s compliance guidance is set out in Regulatory Guide 273. BID requires mortgage brokers to act in your best interests, prioritise your interests over their own where conflicts exist, and document the reasoning behind every loan recommendation.

How “best interests” differs from the bank standard

Banks are subject to responsible lending obligations: they cannot recommend a loan that is “not unsuitable” for you. That is a lower bar. A loan can be “not unsuitable” without being the best loan available for your situation.

BID is an additional, higher duty that applies only to mortgage brokers. Bank lender staff are not credit assistance providers and are not subject to it. The structural consequence is direct: a bank rep can be 100% compliant and still recommend a worse loan than a broker is legally required to deliver.

What this means in practice

Your broker has to put their reasoning in writing. The written assessment shows the lenders considered, the products compared, the rate, the features, and why the recommended loan is in your best interests. If you ask to see it, you are entitled to. Most clients never do, but the document exists. A broker who hesitates when asked is a broker to walk away from.

Worked example: same borrower, four banks, one broker

The borrower profile

$850,000 purchase, 20% deposit, dual PAYG income, no children, owner-occupier loan, principal and interest, looking for variable. A clean, low-risk file. You can check your borrowing power for a comparable scenario.

What the big four offered direct (snapshot 7 May 2026)

| Bank | Variable rate | Comparison rate | Max LVR |

|---|---|---|---|

| CBA Simple Variable Home Loan | 6.34% | 6.59% | 60% |

| ANZ Simplicity PLUS | 6.14% | 6.14% | 60% |

| Westpac Flexi First Variable | 6.14% | 6.51% | 70% |

| NAB Base Variable | 6.19% | 6.19% | 90% |

WARNING: This comparison rate is true only for the examples given and may not include all fees and charges. Different terms, fees or other loan amounts might result in a different comparison rate. Comparison rate based on a secured loan of $150,000 over a term of 25 years.

Rates effective 7 May 2026. All four major banks announced a +0.25% increase to variable home loan rates effective 15 May 2026, following the May 2026 RBA cash rate decision. Add 0.25% to each rate above for the post-15 May position.

The headline-rate trap

Read the “Max LVR” column carefully. Three of the four cheapest rates only apply at 60% to 70% LVR. Our example borrower has a 20% deposit, which puts them at 80% LVR. That disqualifies the CBA Simple Variable, the ANZ Simplicity PLUS, and the Westpac Flexi First Variable. The only headline rate they actually qualify for is NAB Base Variable at 6.19%.

This is one of the most common things we see at MWA. A borrower walks in expecting the advertised rate, and the bank quotes a higher tier rate that matches their actual LVR. The headline never applied to them.

What MWA’s 52+ lender panel surfaced

For an 80% LVR owner-occupier P&I loan, our panel includes non-bank and second-tier lenders (Macquarie, ING, Bankwest, Bendigo, Pepper, and others) who routinely price below the big four headline rates for this borrower profile. We also negotiate the broker pricing tier each big four bank holds above the advertised rate. That tier is rarely volunteered at the branch counter.

The broker’s value on this file is twofold: filter for the lenders who will actually price you at your real LVR, and access the broker pricing tier that the bank does not advertise.

When going direct to your bank IS the right choice

There are some scenarios where going directly to your bank might be the right call.

You are an existing customer with a deep package discount

If you already have a strong negotiated rate with your current bank, switching to a broker for a marginal improvement may not be worth the application paperwork. Always ask your bank what they will offer to retain you before you start a broker conversation. Banks have retention pricing tiers that are not advertised, and a phone call can sometimes match what a broker would otherwise need to source.

Loyalty matters more to you than the rate margin

Some borrowers value a long-standing banking relationship and the convenience of having their offset, credit cards, and home loan with the same institution. That is a valid preference, and rate is not the only consideration in a financial decision.

Anything more complex

For self-employed income, recent career changes, smaller deposits, investment property structures, SMSF loans, or any scenario where lender policies vary materially, a broker has the edge. The reason is simple: lender policies are uneven. One lender may not lend to your industry, another may not accept your income type, a third may price the same scenario 0.4% sharper than the other two. You will not see that at the branch counter.

If your scenario falls into any of those categories, book a 15-minute rate review. The call is free, and at the end of it you will know whether your existing bank is competitive or not.

Choosing a broker: the questions to ask before you sign anything

How many lenders are on your panel?

A panel of 10 is not the same as a panel of 50+. Ask. We work with 52+ lenders through our aggregator, Specialist Finance Group.

What is your commission disclosure?

Every broker must give you a written commission disclosure that names the upfront and trail percentages and translates them into dollars on your specific loan size. Read it. Ask questions if any number is unclear.

Can I see your BID written assessment?

You are entitled to see the written reasoning behind the loan recommendation. A broker who hesitates is a broker to step back from.

How long have you been broking?

Industry tenure matters in a tightening rate cycle. Brokers who have settled loans through previous rate cycles know which lenders honour their pre-approvals when rates move and which lenders quietly walk back the assessment. That knowledge is built one cycle at a time.

Are you a member of the MFAA or FBAA?

Both bodies enforce codes of practice on top of NCCP licensing. Membership is a useful baseline indicator of professional standards.

Frequently asked questions

Is it better to use a mortgage broker or go direct to the bank?

In most cases, yes. A broker can compare loans across a panel of lenders, and is bound by Best Interests Duty to recommend the loan that suits your scenario. Direct still makes sense if you have a strong retention rate with your existing bank, a straightforward low-LVR loan, or you genuinely value the long-standing banking relationship.

Are mortgage brokers free?

Yes, for the borrower in almost all standard residential cases. The lender pays the broker around 0.65% upfront and 0.15% per year in trail. Some complex commercial or SMSF loans may carry a fee, which the broker discloses in writing before you proceed.

How much does a mortgage broker make on a $500,000 loan?

Around $3,250 in upfront commission (0.65%), plus around $750 in first-year trail (0.15% on the outstanding balance). On a $700,000 loan, the upfront is around $4,550, and the first-year trail is around $1,050. Trail reduces as the loan balance is paid down. The borrower never pays these amounts.

What are the disadvantages of using a mortgage broker?

There are three real ones. Panel size varies (a small panel limits the comparison). Personal rapport matters, and you may not click with the first broker you meet. Clawback can create a perception of conflict if a broker seems reluctant to recommend a refinance. A broker who discloses commission and clawback in writing is one you can trust.

Is it cheaper to go through a mortgage broker or bank?

Going via a broker is rarely more expensive and is often materially cheaper, because the broker compares loans across an entire panel rather than a single lender. The exception is when an existing customer negotiates a strong retention rate before approaching a broker.

Are mortgage brokers regulated in Australia?

Yes. Brokers operate under the National Consumer Credit Protection Act 2009, ASIC Regulatory Guide 273 (Best Interests Duty), and credit licensing through an Australian Credit Licence or as a credit representative.

What is mortgage broker clawback?

Clawback lets the lender reclaim some or all of the upfront commission from the broker if the loan is discharged or refinanced within a set window. All four big banks apply 100% clawback in year one. The taper after that varies by lender: Westpac and ANZ stop clawing back after month 18; NAB applies a sliding scale from around 50% at month 13 down to around 6% at month 24; CBA tapers continuously across months 13-24. The borrower never pays clawback.

Do mortgage brokers have access to better rates than banks?

Sometimes yes, through panel-only or aggregator-volume rates. Sometimes no, where a bank’s existing-customer retention rate matches the best broker offer. The broker’s value is in running the comparison across 52+ lenders, so you see the best rate available for your scenario.

This article contains general information only and does not constitute financial advice. Your personal financial situation, objectives and needs have not been considered. Before acting on any information, you should consider its appropriateness to your circumstances. Speak to a qualified mortgage broker for advice tailored to your situation. Mortgage World Australia Pty Ltd is a credit representative (CR No. 396946) of Mortgage Specialists Pty Ltd (Australian Credit Licence No. 387025).

Patrick is a Director and a Home Loan Specialist. He has been helping Australians with home loans since 2001. Prior to working as a mortgage broker Patrick was employed by Macquarie Bank for 3 years and also worked as an accountant for a publicly listed company. Patrick’s qualifications include:

Bachelor of Business, UTS Sydney. Majored in accounting and sub-majored in Finance and Marketing.

Diploma of Finance and Mortgage Broking Management FNS50310

Certificate IV in Financial Services (Finance/Mortgage Broking) FNS40804

Ready to Take the Next Step?

Whether you’re looking to buy your first home, refinance, or explore investment opportunities, Mortgage World Australia is here to help.

Fill out the contact form below, and one of our expert mortgage brokers will be in touch shortly to discuss your needs and guide you through your options.

Get Started Today!