LMI Waivers for Nurses: Lender-by-Lender Guide 2026

LMI Waivers for Nurses and Healthcare Workers: Lender-by-Lender Guide for 2026

On this page ▾

- What is an LMI waiver, and why nurses now qualify

- Which lenders waive LMI for nurses in 2026

- Which healthcare professions qualify

- How much can you save by skipping LMI?

- Income evidence: what lenders actually want to see

- Should you take the LMI waiver or the federal 5% Deposit Scheme?

- The application process step by step

- When an LMI waiver is not the best option

- Frequently asked questions

Most articles about home loans for nurses come from a single bank’s product page or from a niche specialist with a reason to push you toward one outcome. This one comes from a broker with access to 52+ lenders, and it tells you something the bank pages don’t: only one of the big four banks publicly waives Lenders Mortgage Insurance for registered nurses. The rest either exclude nurses outright or trialled an inclusion that has since ended.

If you are a nurse, midwife, paramedic or other healthcare worker buying your first home or refinancing, an LMI waiver can save you somewhere between roughly $10,000 and $25,000 on a typical purchase. But the eligibility rules vary lender by lender, and the difference between getting the waiver and missing out can come down to whether your income evidence fits a specific lender’s policy. We have written this guide to give you the lender-by-lender comparison, the income rules nobody publishes clearly, and an honest view of when an LMI waiver isn’t the right option.

What is an LMI waiver, and why nurses now qualify

Lenders Mortgage Insurance (LMI) applies when you borrow more than 80% of a property’s value. It protects the bank if you default. The borrower pays the premium. The policy protects the lender. On a $700,000 purchase with a 10% deposit, the LMI premium is typically around $11,000 to $15,000, and most banks add it to the loan amount, so you pay interest on it for the life of the mortgage.

An LMI waiver removes that premium for borrowers in occupations the lender considers low default risk. The eligible cohort started with doctors and dentists in the 1990s, expanded to allied health and finance professionals through the 2000s and 2010s, and broadened further in 2024 when Westpac formally extended its program to registered nurses and midwives earning at least $90,000 a year. Other major banks have moved at different speeds. As of May 2026, the public-facing position for nurses is this: Westpac waives LMI for registered nurses on its consumer pages; CBA piloted a frontline-worker waiver that ended on 30 April 2025; NAB and ANZ explicitly exclude nurses from their medico programs; and a handful of mutual and tier-2 lenders offer nurse-specific or essential-services packages.

A waiver isn’t an exemption. The borrower still needs to meet the lender’s serviceability test, provide AHPRA registration evidence, and stay inside the lender’s loan-size and property-type limits. But on a 90% LVR purchase, a successful waiver application is typically the single biggest cost saving available to a healthcare worker buying a home.

Which lenders waive LMI for nurses in 2026

This is where the public information gets thin. A lot of nurse LMI waiver activity happens through the broker channel rather than on a bank’s public website. We have audited every major lender’s consumer pages, and only three currently advertise an active nurse-eligible LMI waiver to the public.

The big four reality: Westpac waives LMI for nurses, NAB and ANZ do not, CBA’s pilot ended

Westpac is the only big-four bank that publicly advertises a nurse LMI waiver on its consumer-facing site. Registered nurses and registered midwives can borrow up to 90% of a property’s value without paying LMI, provided they earn at least $90,000 a year gross and hold AHPRA general registration. Doctors, dentists, GPs and medical specialists qualify at up to 95% LVR with no minimum income. The maximum loan size is $5 million, or $7.5 million where the LVR is over 80%.

NAB publishes an 18-profession list for its LMI waiver program. The eligible medical occupations are anaesthetists, chiropractors, dental practitioners, dermatologists, GPs, obstetricians and gynaecologists, ophthalmologists, optometrists, paediatricians, pathologists, pharmacists, physicians, physiotherapists, psychiatrists, radiation oncologists, radiologists, surgeons and veterinary practitioners. Registered nurses, enrolled nurses and midwives are not on the list. NAB’s program also includes finance professionals (chartered accountants, CPAs, IPA members, actuaries, CFA charterholders) and lawyers.

ANZ restricts its LMI waiver to medical practitioners, specialists and dentists with AHPRA general or specialist registration. Up to 95% LVR is available for the eligible cohort, and individual properties are capped at $5 million for houses and townhouses or $4 million for units. Nurses are AHPRA-registered but ANZ’s published eligibility scope excludes them.

CBA ran a frontline-worker pilot in 2024 and 2025 that briefly included nurses, paramedics, police and firefighters at up to 95% LVR. That pilot ended on 30 April 2025. CBA’s current Medical Professionals package targets doctors, specialists and dentists. There is no public-facing CBA nurse LMI waiver as of May 2026.

Tier-2 and mutual lenders that publicly waive LMI for nurses

BankVic offers up to 90% LVR with no LMI to “police, emergency

services, health workers and government employees” purchasing in certain postcodes. The eligible cohort includes any registered health practitioner with AHPRA registration, and any employee or contractor of an Australian public or private hospital.

People First Bank (formed by the Heritage Bank and People’s Choice merger) advertises an Essential Services Package at up to 90% LVR with no LMI, on loans up to $1.2 million. The published eligibility scope is narrow: registered nurses, fully qualified paramedics, and sworn state or federal police officers. Midwives are not listed. Owner-occupier and investment purchases both qualify, and there is a useful joint-applicant rule. People First Bank’s page states it directly: only one applicant in a joint application needs to be an essential services worker for the whole loan to qualify.

A handful of other lenders, including the Westpac Group sister brands (St.George, Bank of Melbourne, BankSA), operate similar policies through the broker channel. None of them publishes a nurse-specific page on their consumer sites, so we don’t name them as nurse-waiver lenders here. If you are working with a broker, those broker-channel options widen the pool considerably.

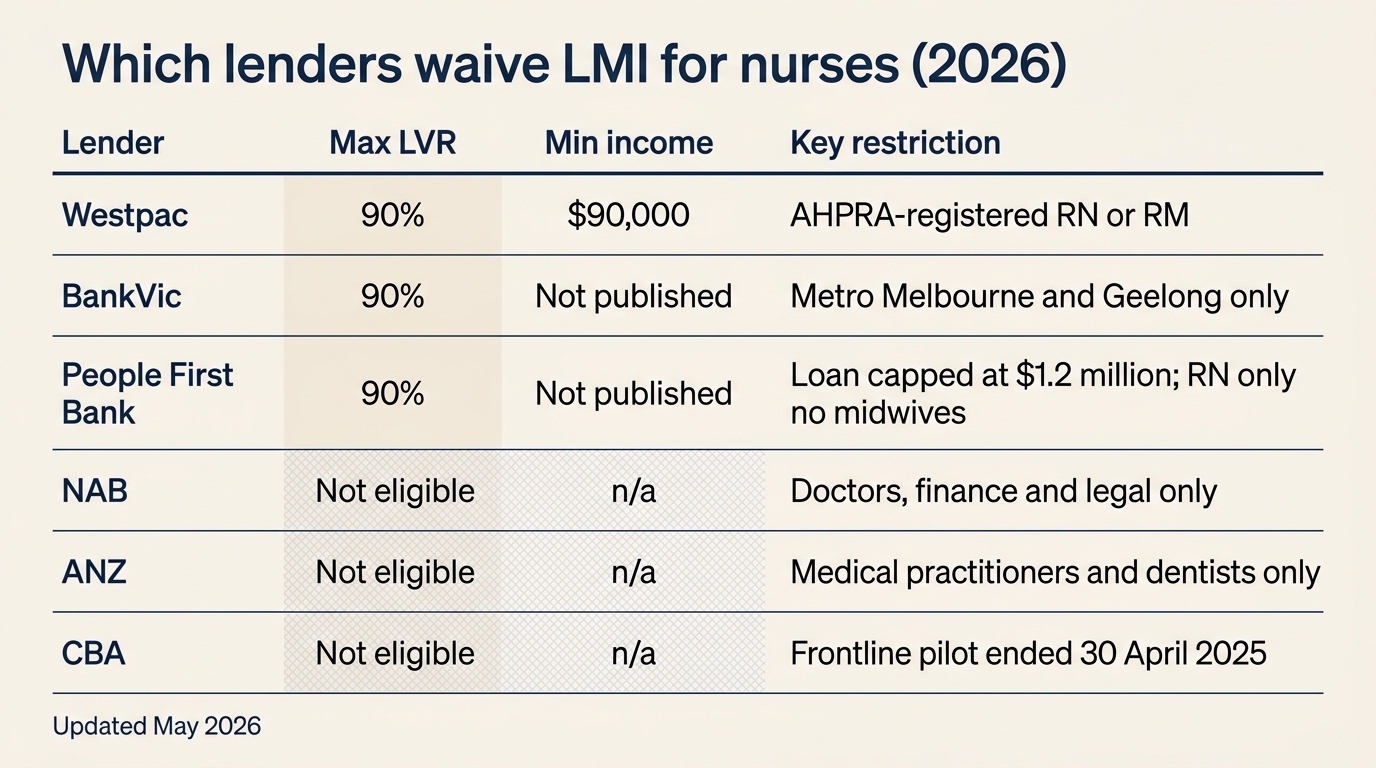

Maximum LVR by lender (current public offers)

| Lender | Max LVR | Min income | Eligible nurse cohort | Key restriction |

|---|---|---|---|---|

| Westpac | 90% | $90,000 p.a. | Registered nurses, registered midwives | National; AHPRA general registration |

| BankVic | 90% | Not published | Any AHPRA-registered health practitioner | Metro Melbourne and Geelong only; owner-occupier |

| People First Bank | 90% | Not published | Registered nurses (no midwives) | Loan capped at $1.2 million; joint applicant rule applies |

| NAB | Not eligible for nurses | n/a | n/a | Doctors, finance, legal only |

| ANZ | Not eligible for nurses | n/a | n/a | Medical practitioners and dentists only |

| CBA | Not eligible for nurses | n/a | n/a | Frontline pilot ended 30 April 2025 |

Income figures and product policies are reviewed by lenders periodically and can change without notice. Always verify the current rule with the lender or your broker before relying on it.

Which healthcare professions qualify

Even with a narrow public-page list, the broader healthcare LMI waiver market sits across roughly four tiers, anchored by Westpac’s published policy and supported by the broker-channel offers we see across the panel.

Doctors, surgeons and dentists (95% LVR, often no minimum income)

GPs, hospital-employed doctors (intern, resident, registrar, staff specialist), medical specialists registered with the Medical Board of Australia, and dentists typically qualify at 95% LVR with no minimum income. ANZ matches this scope at up to 95% LVR. NAB and CBA both extend their medico waivers to similar specialties.

Allied health: physios, pharmacists, vets, optometrists, psychologists (90% to 95% LVR)

Physiotherapists, pharmacists, veterinary practitioners, optometrists, psychologists, chiropractors, audiologists, occupational therapists, osteopaths, podiatrists, radiographers, sonographers and speech pathologists are eligible at Westpac at 90% LVR with the $90,000 minimum income. NAB includes physiotherapists, pharmacists, optometrists, chiropractors, vets and a wider list of specialists in its program. The scope and LVR cap vary lender by lender.

Registered nurses, midwives and nurse practitioners (90% LVR, $90,000 income at Westpac)

Westpac’s offer is the headline: registered nurses and registered midwives at 90% LVR with the $90,000 income threshold. Nurse practitioners hold endorsed registration and are typically treated as registered nurses for the waiver. People First Bank covers registered nurses (not midwives) at 90% LVR. BankVic covers any AHPRA-registered health practitioner at 90% LVR within Metro Melbourne and Geelong.

Enrolled nurses: what to do if you don’t qualify for the waiver

Enrolled Nurses (Division 2, Diploma of Nursing) are AHPRA-registered but are not eligible for the medico-tier waiver at major banks. The published program at Westpac names registered nurses or registered medical practitioners only. If you are an EN, the most efficient pathway is usually the Australian Government 5% Deposit Scheme, which removes LMI through a federal guarantee rather than a lender waiver.

Paramedics, ambulance officers and other front-line essential services

Paramedics, ambulance officers, fire officers and police officers are eligible at Westpac for the same 90% LVR / $90,000 income tier as registered nurses, and they get Westpac’s 100% overtime and allowances treatment when employed by a hospital or emergency service. People First Bank’s Essential Services Package covers fully qualified paramedics and sworn police officers. BankVic covers Victoria Police and Emergency services employees.

How much can you save by skipping LMI?

The dollar savings on an LMI waiver move with the property price, the deposit size, and which LMI provider the lender uses. Here is an indicative comparison for a 10% deposit, owner-occupier, 30-year principal-and-interest loan, based on current Helia and lender-internal LMI estimates for an owner-occupier first home buyer profile:

| Property price | Loan amount (90% LVR) | Indicative LMI premium | Saving with a waiver |

|---|---|---|---|

| $600,000 | $540,000 | $9,000 – $13,000 | $9,000 – $13,000 |

| $800,000 | $720,000 | $12,000 – $17,000 | $12,000 – $17,000 |

| $1,000,000 | $900,000 | $15,000 – $22,000 | $15,000 – $22,000 |

These are indicative only. Premiums vary materially between LMI providers (Helia, QBE and lender-internal cards each price the same scenario differently), and most banks add the premium to the loan, so the long-run interest cost is higher than the headline. The saving from a waiver compounds over the life of the mortgage. We can run a precise comparison once we know the lender, the LMI provider, and your borrower profile.

Income evidence: what lenders actually want to see

Where most healthcare LMI waiver applications stall is in income evidence. Hospital-employed nurses typically have four income components: base salary, shift allowances, overtime and casual loadings. Lenders treat each differently.

Base salary, payslips and PAYG summaries

The standard documentation is two recent payslips, a year-to-date YTD figure, and the most recent PAYG payment summary or Notice of Assessment. Permanent full-time and permanent part-time roles are the easiest cases. Lenders typically need to see at least three to six months in the role at the same employer.

Casual, part-time and multi-employer nursing income

Casual nursing income is the most common pain point. Lender practice varies. Most lenders look for 12 months of continuous casual employment in the same role or industry, but several shade this to six months for healthcare, given the workforce shortage. Casual loading (typically 15% to 25% on top of base) is included in the assessable income, provided the pattern is ongoing. Multi-employer nurses (one shift at a public hospital, another at a private one) need each employer’s payslips and a clean attendance pattern.

Agency and locum nursing income

Agency and locum income is treated as a hybrid of casual and contract income. Some lenders require 24 months of agency ABN history; others accept 12 months of continuous payslips from the agency. If you are a locum nurse, talk to a broker before you apply, because the differences between lenders are large enough to change which lender is the right fit.

Shift allowances and overtime (100% counted at eligible lenders)

Westpac publishes the strongest rule we can quote: hospital-employed registered nurses, doctors, specialists, ambulance officers, paramedics, fire officers and police officers have 100% of overtime and allowances assessed as income, provided they have payslips covering a full financial year with the same employer. That is materially better than the 80% haircut some lenders apply to overtime. It is also a powerful borrowing-capacity lever for shift workers, who often have $20,000 to $40,000 a year in allowances on top of base salary.

Borrowing capacity is a serviceability calculation, not a salary multiple. The lender takes your net income, subtracts your living expenses and existing debts at a stress-tested interest rate, and lends against the surplus. Banks regulated by APRA add a 3% stress buffer; some non-bank lenders run a 1% to 2% buffer. That gap is one of the biggest reasons broker advice changes the outcome on healthcare worker loans: matching the right shift-allowance treatment to the right serviceability buffer is what unlocks the borrowing capacity, not just hunting for the lowest rate.

Should you take the LMI waiver or the federal 5% Deposit Scheme?

This is the single most common question we get from healthcare workers buying their first home. The two pathways are alternatives, not additives. You don’t stack them.

The Australian Government 5% Deposit Scheme (renamed from the Home Guarantee Scheme on 1 October 2025) lets eligible first home buyers purchase with a 5% deposit and no LMI, because the federal government guarantees the difference. From 1 October 2025, the scheme removed its income caps and place limits, and lifted property price caps materially: $1.5 million in Sydney and the NSW capital region, $1 million in Brisbane and Queensland regional centres, $950,000 in Melbourne, and $1 million in the ACT, with lower caps in regional areas. First home buyers in NSW may also be exempt from stamp duty on a home under $800,000. See our guide to NSW stamp duty exemptions.

A nurse choosing between the two pathways is really choosing between three variables: deposit size, property price relative to the scheme cap, and lender flexibility. The 5% Deposit Scheme is the better fit when you have a 5% deposit (not 10%), the property is inside the scheme price cap, and you need maximum flexibility on lender choice. The Westpac nurse waiver is the better fit when you have a 10% deposit, the property exceeds the scheme cap, or you want to stay with a specific lender for a feature like an offset account, professional package pricing, or a higher loan limit.

For households with one nurse and one non-eligible partner, the People First Bank joint rule is a useful third option: the eligible nurse qualifies the whole loan for the LMI waiver, regardless of the partner’s profession.

The application process step by step

Most healthcare LMI waiver applications take four to six weeks from pre-approval to settlement, but the front end is where the work happens.

AHPRA registration and proof of profession

Lenders verify eligibility against the AHPRA public register, which is free and searchable on ahpra.gov.au. You’ll need to provide your AHPRA registration number on the application, and the lender will cross-check that you hold a current general registration (not provisional, limited or non-practising). Have a recent screenshot or PDF of your AHPRA registration record on hand.

Documents to gather before pre-approval

Standard documents for a healthcare LMI waiver application include two recent payslips, your most recent PAYG payment summary or Notice of Assessment, three months of bank statements covering both transaction and savings accounts, identification (driver’s licence and passport or Medicare card), evidence of genuine savings (typically 5% of the purchase price held for at least three months), and AHPRA registration evidence. If you have shift allowances or overtime, ask your employer for a year-to-date letter confirming the pattern.

Pre-approval to settlement timeline

Pre-approval typically takes one to two weeks once the documents are submitted. Once you have an accepted contract, formal approval takes another two to three weeks for the lender to value the property and confirm the loan terms. Settlement follows the contract date, which in most states is six weeks from contract exchange. Build in a week of buffer for AHPRA verification on the lender’s side.

When an LMI waiver is not the best option

LMI waivers are an enormous saving for the right borrower, but they are not always the right tool for the job. We sometimes recommend healthcare worker clients skip the waiver in four scenarios.

The first is when the property price exceeds the lender’s nurse-waiver cap. Westpac’s program permits high loan sizes, but BankVic and People First Bank cap loans at lower thresholds, and a property purchase outside specified postcodes is outside BankVic’s scope entirely. The second is when the borrower can’t comfortably meet the $90,000 income threshold. A part-time nurse on $70,000 might do better via the 5% Deposit Scheme than chasing a Westpac waiver they don’t qualify for. The third is investment-property purchases. Most public nurse waivers are owner-occupier only; for investment property loans for healthcare workers, the broker-channel options widen significantly, and the waiver is sometimes a smaller factor than the rate and offset structure. The fourth is when the nurse is already on a competitive home loan and considering refinancing to a lender that recognises healthcare income more favourably. In that case, the loan is already under 80% LVR (no LMI applies) and the conversation is about rate, structure and serviceability buffer, not waivers.

The honest answer here is that the right pathway is borrower-specific. We see healthcare workers across the panel every week, and matching the right lender to the right income profile is what we do all day. If you are trying to work out which option fits, contact us on 1300 66 12 11 and we’ll work through the lender-by-lender comparison with you.

Frequently asked questions

Do nurses get cheaper home loans?

Sometimes. Eligible nurses can access an LMI waiver, which removes a $10,000 to $30,000 cost on a typical 90% LVR purchase. Some lenders also offer professional-package interest rate discounts for healthcare workers, but the discount is usually smaller than the LMI savings.

Are nurses exempt from LMI?

Nurses aren’t exempt from LMI. A handful of lenders waive the premium for eligible registered nurses (and other AHPRA-registered health practitioners) at up to 90% LVR. The most established public offer is Westpac’s, which requires registered nurses to earn at least $90,000 a year. BankVic and People First Bank offer narrower public alternatives, and the broker channel widens the pool further.

Which banks waive LMI for nurses?

As of May 2026, Westpac, BankVic and People First Bank publicly advertise a nurse-eligible LMI waiver on their consumer pages. NAB and ANZ explicitly exclude nurses from their medico programs. CBA’s frontline-worker pilot ended on 30 April 2025. Several Westpac Group sister brands and other lenders offer similar policies through the broker channel.

Can enrolled nurses get an LMI waiver?

Most major-bank LMI waivers are restricted to registered nurses (Division 1, Bachelor of Nursing). Enrolled nurses (Division 2, Diploma of Nursing) typically don’t qualify for the published programs, but the Australian Government 5% Deposit Scheme is an alternative no-LMI pathway that is open to enrolled nurses meeting first-home-buyer eligibility.

How much deposit do nurses need?

With a Westpac nurse LMI waiver, you need a 10% deposit (90% LVR). With the Australian Government 5% Deposit Scheme, you need a 5% deposit. Without either, the standard requirement is a 20% deposit to avoid LMI. With smaller deposits, LMI applies.

What salary do you need for a $500,000 loan?

Borrowing capacity is a serviceability calculation, not a salary multiple. As a rough guide, a single applicant with no other debts and modest living expenses typically needs $80,000 to $100,000 of gross income to qualify for a $500,000 loan, but the exact figure depends on the lender’s stress buffer (3% at APRA-regulated lenders, 1% to 2% at some non-bank lenders), the rate, and the household’s expenses. Healthcare workers with strong overtime and allowances often borrow more than their base-salary peers because lenders like Westpac assess 100% of overtime and allowances as income.

How much do you need to earn for a $700,000 mortgage?

On the same broad principles, a $700,000 mortgage typically needs around $115,000 to $140,000 of gross income for a single applicant with no other debts, and less per applicant for a joint application where both incomes are assessable. The shift allowances and overtime treatment are decisive at this loan size, which is where having the right lender matters most.

Patrick O’Brien, Director and Home Loan Specialist since 2001

This article contains general information only and does not constitute financial advice. Your personal financial situation, objectives and needs have not been considered. Before acting on any information, you should consider its appropriateness to your circumstances. Speak to a qualified mortgage broker for advice tailored to your situation. Mortgage World Australia Pty Ltd is a credit representative (CR No. 396946) of Mortgage Specialists Pty Ltd (Australian Credit Licence No. 387025).

Patrick is a Director and a Home Loan Specialist. He has been helping Australians with home loans since 2001. Prior to working as a mortgage broker Patrick was employed by Macquarie Bank for 3 years and also worked as an accountant for a publicly listed company. Patrick’s qualifications include:

Bachelor of Business, UTS Sydney. Majored in accounting and sub-majored in Finance and Marketing.

Diploma of Finance and Mortgage Broking Management FNS50310

Certificate IV in Financial Services (Finance/Mortgage Broking) FNS40804

Ready to Take the Next Step?

Whether you’re looking to buy your first home, refinance, or explore investment opportunities, Mortgage World Australia is here to help.

Fill out the contact form below, and one of our expert mortgage brokers will be in touch shortly to discuss your needs and guide you through your options.

Get Started Today!