Construction Loan Australia: How It Works & Rates (2026)

Construction loan Australia: how they work, rates, and how to get approved (2026 guide)

On this page ▾

- What is a construction loan?

- How a construction loan works: progress payment drawdowns

- The progress payment schedule trap

- Construction loan deposit and LVR

- Construction loan rates compared: CommBank, NAB, ANZ, Westpac

- The conditional approval catch-22

- Funding a build without a construction loan

- Owner-builder construction loans in Australia

- Knockdown-rebuild and building on vacant land

- NSW transfer duty on land-only purchases

- The construction loan application process

- Common pitfalls and how to avoid them

- How a mortgage broker helps with construction loans

- Frequently asked questions

- Talk to a mortgage broker who builds with you

You’ve bought land in Kellyville, your builder has quoted the house for $620,000, and now your lender is asking about progress payment schedules, fixed-price contracts, and whether your deposit counts against the land, the build, or both. A construction loan is not a standard home loan with a different name. It moves money differently, prices risk differently, and turns on details most borrowers never see until they’re already committed.

This guide covers how a construction loan actually works in Australia, how the big four compare, and the two operational traps we see clients fall into most often. Written for NSW buyers, with a Western Sydney worked example.

By Patrick O’Brien, Director and Home Loan Specialist since 2001

What is a construction loan?

A construction loan is a home loan designed to fund a new build or major renovation. Instead of releasing the full loan amount at settlement, the lender pays the money out in stages as the build progresses, and you only pay interest on what has been drawn. Once the home is finished, the loan converts to a standard home loan with principal-and-interest repayments.

The mechanics solve one problem: on day one, there is no house yet. Staged drawdowns protect the lender (money is only released against completed work) and they protect you (the builder has to earn each payment).

Construction loan vs standard home loan

| Feature | Construction loan | Standard home loan |

|---|---|---|

| How funds are released | In stages (progress payments) as the build advances | Full amount at settlement |

| Repayments during construction | Interest-only on drawn funds | Principal-and-interest from day one |

| Security | The land, with the house being built on it | The finished property |

| Term of the construction phase | Typically 24 months | Not applicable |

| What happens at completion | Rolls over to a standard home loan | Already on a standard structure |

Who uses construction loans

Three borrower profiles dominate the application queue. The first is buyers building through a registered builder on a fixed-price contract, typically a project home on a newly released estate or a knockdown-rebuild on an existing block. The second is owner-builders managing their own build under an owner-builder permit. The third is buyers on a house-and-land package, where the land and build are separate contracts but most lenders can fund them together. House and land package loan advice covers the package-specific process in more detail.

How a construction loan works: progress payment drawdowns

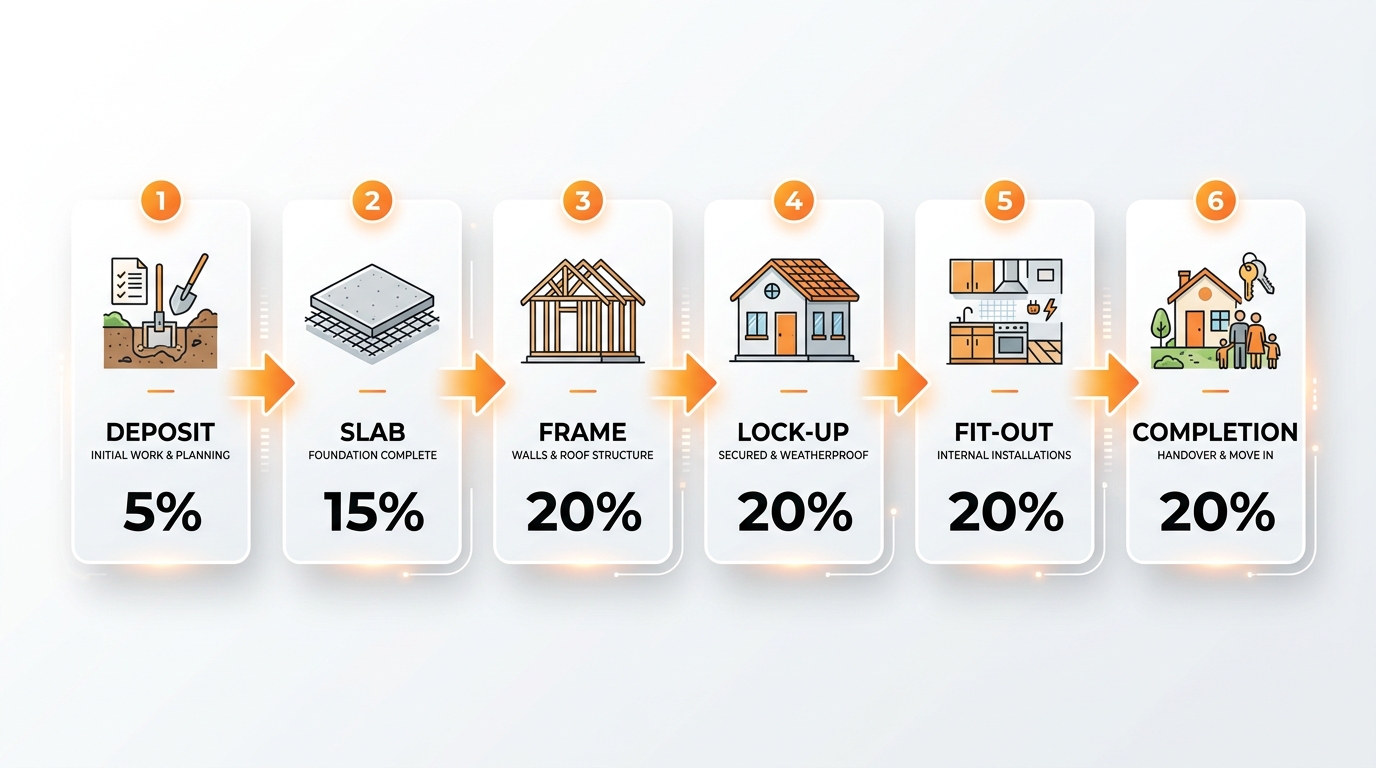

The five standard progress payment stages

Most Australian lenders and builders use a five- or six-stage progress payment structure. The exact split varies by builder and contract, but the typical range across CommBank, NAB, ANZ, and Westpac lands in this band:

| Stage | Typical % of build contract | What triggers payment |

|---|---|---|

| Deposit | ~5% | Signed fixed-price contract |

| Slab (base) | 10–20% | Slab poured and inspected |

| Frame | ~20% | Wall frames and roof trusses up, inspected |

| Lock-up | 15–20% (some contracts up to 25%) | External walls, roof, doors, windows complete |

| Fit-out (fixing) | ~20% | Kitchen, bathroom, flooring, internal fixtures installed |

| Practical completion | 10–15% | Final inspection passed, ready for handover |

Your builder invoices the lender at each stage. The lender may send a valuer to confirm the work has been done to the stage the invoice claims, and then releases the funds directly to the builder. You don’t see the money hit your account. It moves from the lender to the builder with your authorisation.

Interest-only on drawn funds during construction

Repayments during the build are interest-only on the amount actually drawn, not on the full approved loan. On a $600,000 build loan at a 6.5% rate, monthly interest at slab stage (around $105,000 drawn) sits near $570. By lock-up, with roughly $315,000 drawn, monthly interest is around $1,706. At practical completion with the full $600,000 drawn, interest is around $3,250. The loan then rolls to principal-and-interest and repayments step up again.

How a valuer inspects before each drawdown

Before each progress payment, the lender may order a short-form inspection. The valuer confirms the stage the builder is claiming is genuinely complete. If the valuer can’t verify the work (for example, the builder has claimed lock-up but the windows haven’t gone in), the drawdown is refused until the stage is actually finished.

The progress payment schedule trap

This is the first operational angle we spend real time on with construction-loan clients. Every borrower is told to review the total contract price. Very few are told to read the progress payment schedule line by line, and that’s where the damage usually hides.

Why builders sometimes front-load the contract

Some builders structure the payment schedule so a disproportionate amount is due at the earliest stages. The commercial reason is cashflow. The builder wants funds in early to cover materials, subcontractors, and overheads. The problem is structural. If the builder has 60% of the contract value in hand by the end of frame stage, their incentive to finish the remaining 40% drops. And if they hit financial trouble mid-build, the lender’s ability to recover drops with it, because the remaining work no longer justifies the remaining funds.

The slab-stage rule lenders apply

When a lender reviews a progress payment schedule for front-loading, they don’t look at the slab invoice in isolation. They look at how much of the total building contract has been paid to the builder by the time slab is finished — that means the upfront deposit (typically 5%) plus the slab-stage invoice. The industry-standard accepted range for the slab-stage invoice itself is 10–20% of the total building contract. CommBank’s own guide puts slab at 15–20%. NAB and Westpac sit in the 10–20% band.

Add the deposit and you get a cumulative paid-by-slab figure of around 15–25%. That’s the figure the lender’s credit team is actually testing against. If the deposit is 5% and the slab invoice is 25%, you’re 30% paid out before the slab cures — which is where lenders push back and ask the builder to amend the schedule.

We’ve had clients come to us with builder contracts where 25–30% was due at slab on top of a 5% deposit, and another 30%+ due at frame. Cumulatively, 55–65% of the contract was paid out by the end of frame stage. The lender wouldn’t fund it until the schedule was renegotiated. The client hadn’t read the schedule closely, and hadn’t realised a “standard” contract was a lender-declined contract.

How a broker gets the schedule amended

Before the borrower signs anything, we ask for the progress payment schedule, compare the percentages to the range lenders will accept, and flag anything outside it. If the schedule is front-loaded, we either raise it with the builder directly (most will adjust rather than lose the job) or flag to the borrower that the contract as written won’t be funded. The time to do this is before signatures, not after.

Construction loan deposit and LVR

Deposit from cash vs using existing equity

For a build on land you already own, the equity in the land counts toward your deposit. If your block is worth $600,000 and you paid $480,000 with $120,000 in equity, that $120,000 can form part of your 20% deposit on the combined land-plus-build position. For a knockdown-rebuild, the equity in the existing property can cover the deposit on the build entirely.

For buyers purchasing land and building in one project, the deposit typically covers the land purchase plus the LMI (if applicable) plus any cash contribution toward the build. Our guide to how much deposit you need for a house covers the broader deposit picture.

LMI on construction loans above 80% LVR

As with any home loan, borrowing above 80% loan-to-value ratio triggers Lenders Mortgage Insurance (LMI). LMI protects the lender, not you, and is either added to the loan or paid upfront. On a $600,000 build at 90% LVR, LMI can run into the five-figure range depending on the insurer and the specifics.

CommBank raised its maximum LVR for construction loans to 95% (inclusive of LMI) from 24 May 2025, in line with its standard home-loan cap. The other big-four lenders sit at different ceilings: NAB caps owner-occupied construction (BICOE) at 90% — a step-down from NAB’s standard 95% home-loan cap. ANZ runs a debt-to-income-driven cap of 92% (DTI ≥6) or 97% (DTI <6), but drops the cap to 80% if the loan is owner-occupied with interest-only repayments. Westpac matches CommBank at 95% for licensed-builder construction. We confirm the policy position with the specific lender at application because these caps move.

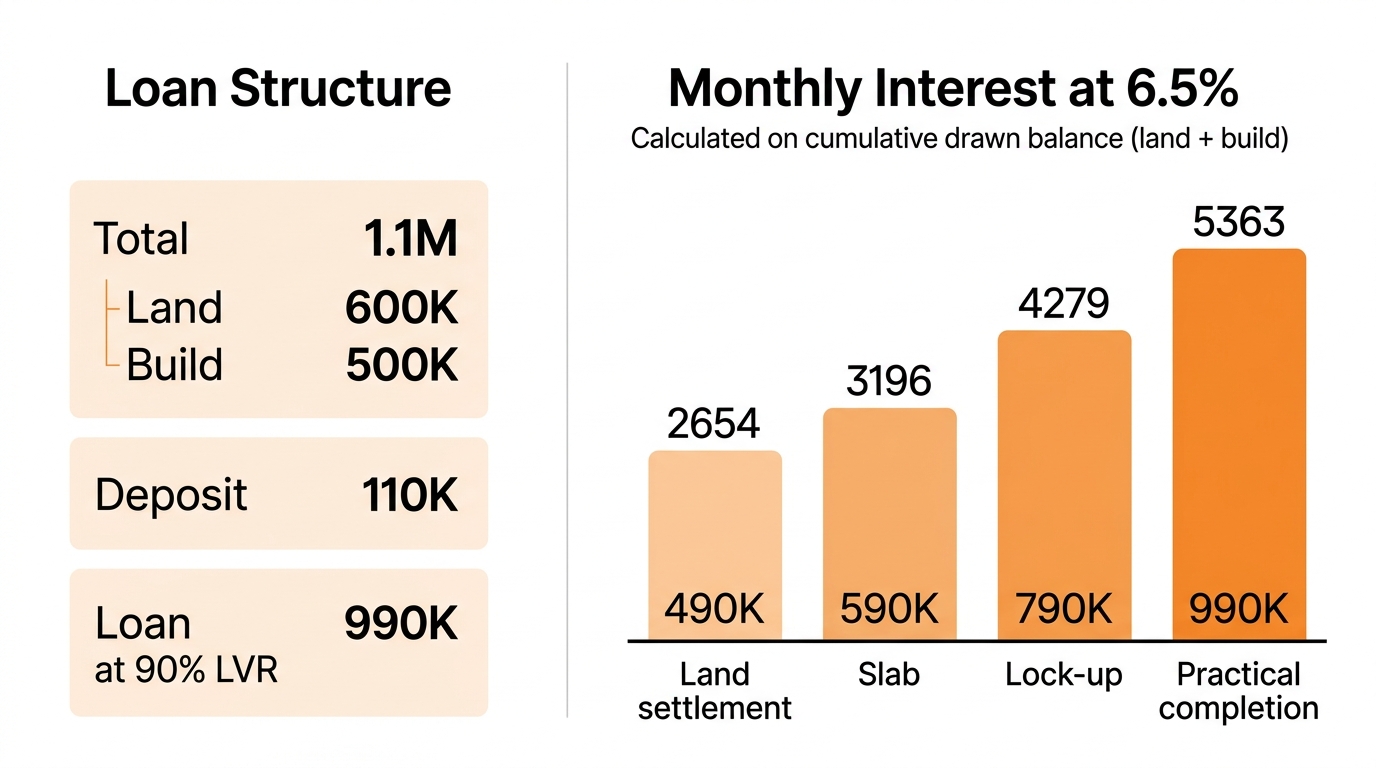

Worked example — 90% LVR construction loan, Western Sydney build

Total project: $1.1M (Western Sydney land $600,000 + build contract $500,000). Deposit at 10% of total is $110,000. Loan required is $990,000 at 90% LVR with LMI added. Transfer duty on the land at $600,000 (general rate) comes to $22,207. The first home buyer vacant land concession caps at $450,000, so a $600,000 land purchase falls outside it. No concession applies, and the buyer pays the general rate.

A construction loan in this scenario funds two things: the land purchase and the progressive build payments. At land settlement, $490,000 of the loan is drawn to settle the land alongside your $110,000 deposit. The remaining $500,000 funds progress payments to the builder during the build.

Interest is charged on the full cumulative drawn balance of the loan — the land portion plus whatever has been progressively drawn for the build to date — not just the build component on its own. This is the point where most people miscalculate.

At land settlement, $490,000 is drawn (the land), so monthly interest at 6.5% is around $2,654. By slab stage (cumulative 20% of the build contract paid out), the drawn balance has grown to $590,000 — interest steps to around $3,196. By lock-up (cumulative 60% of the build paid), the drawn balance is $790,000 — interest around $4,279. At practical completion, the full $990,000 is drawn — interest around $5,363. The loan then converts to principal-and-interest on the full $990,000 and repayments step up again. The borrowing capacity you use when qualifying needs to cover that post-rollover repayment, not just the interest-only phase. Our borrowing capacity guide covers the full calculation. For more on this, see our depreciation deep-dive guide.

Construction loan rates compared: CommBank, NAB, ANZ, Westpac

Rates change quickly and we don’t quote live rates in content. Your broker confirms current offers at application. The structural differences between the big-four construction products are more useful anyway.

| Feature | CommBank | NAB | ANZ | Westpac |

|---|---|---|---|---|

| Max LVR incl. LMI (owner-occupier, security <$3M) | 95% (security <$3M; 80% for $3M–$6M). Must be Standard Variable; LMI/LDP waivers not available | 90% (BICOE loans). NAB’s standard home loan goes to 95%, construction is a step-down. Owner-builders not eligible | 92% (DTI ≥6) or 97% (DTI <6). Drops to 80% if the loan is owner-occupied with interest-only repayments | 95% (licensed builder). Owner-builder caps at 60% with no LMI available |

| Interest during construction | Interest-only on drawn funds | Interest-only on drawn funds | Interest-only on drawn funds | Interest-only on drawn funds |

| Fixed rate during the build | No (fixed available from rollover) | No (fixed available from rollover) | No (fixed available from rollover) | Yes — on the Fixed Rate Home Loan with construction option |

| 100% offset during construction | Yes — available on a Standard Variable Rate home loan during construction | Yes — Tailored Variable with Offset (variable portion only) | Yes — Construction Standard Variable with Optional Offset ($10/month account fee) | Yes — 100% offset on variable-rate construction loans (e.g. Rocket Repay), up to 10 offset accounts |

| Max build window | 24 months from first drawdown; commencement within 12 months of disclosure date | 24 months from loan settlement | 24 months from commencement of construction; commencement within 12 months of land settlement | 24 months from offer date (first drawing within 12 months) |

| Notable extras | First big four to fund prefab offsite (up to 80% during offsite build); “as if complete” valuation required | Must use MBA or HIA fixed-price building contract; “as if completed” valuation | DTI-driven LVR; Tentative-On-Completion valuation | Fixed Price and Cost-Plus contracts both accepted; split contracts excluded |

Policies and rates change. Confirm current terms with a broker at application. The 24-month windows are the standard policy positions — extensions can usually be requested through the lender’s relationship team if council delays or builder issues push the build out. We’ve had clients extend an ANZ construction loan three times past the original 24 months, which is unusual but does happen.

Fixed vs variable during construction

This is the question where the big-four diverge most. CommBank, NAB, and ANZ construction loans sit on variable rates during the build, with the option to fix at rollover to a standard home loan. Westpac is the outlier. Its Fixed Rate Home Loan can be paired with the construction option, which lets you lock in a fixed rate during the build itself. The catch is that rate lock is not available on progress-draw loans, so the fixed rate is set at settlement rather than pre-locked at application.

Outside the big four, most lenders default to variable during construction. A borrower who specifically wants rate certainty during an 18–24 month build has a short list of viable options. Our fixed vs variable home loan guide walks through the broader trade-off.

Why construction loan rates sit above standard home loan rates

Construction loans carry more operational risk for the lender: incomplete security, a forward-looking valuation, and heavier drawdown administration. That premium gets priced in. Expect a construction loan to sit 20–50 basis points above the equivalent standard home loan rate at the same LVR.

The roll-over at practical completion

At practical completion, the construction loan converts automatically to a standard home loan. You don’t need to reapply. What you can do, and often should, is review the rate it’s rolling to. Standard home loan lenders compete harder than construction loan lenders, so there’s usually a sharper rate available post-handover by refinancing.

The conditional approval catch-22

This is the second operational angle that trips borrowers up. A construction loan is secured against a home that doesn’t exist yet. Most lenders can’t fully assess security or confirm the final loan amount until the building contract is signed and the fixed price is known. Until then, approval is generally conditional.

The problem is that signing a building contract is a six-figure commitment, and most borrowers sensibly don’t want to sign until they know the bank will fund the build. If the loan falls through after the contract is signed, the builder’s deposit and the borrower’s cash position are both exposed.

Not every lender plays it the same way. Some lenders will issue formal (unconditional) loan approval based on an unsigned building contract — they just won’t issue the commencement letter that releases progress payments until the signed contract is in. ANZ is the example we lean on most often: ANZ can issue an unconditional construction loan approval before the building contract is signed, which removes the catch-22 entirely. Lender choice matters here.

How a broker bridges the gap

For lenders that do require a signed contract before unconditional approval, the workaround is the structure of the conditional approval itself. We get the borrower’s financial position fully assessed first, with the lender issuing a conditional approval where the only remaining condition is the signed building contract. Everything else (income, credit, deposit, land valuation, borrowing capacity) is already cleared. The borrower signs with real confidence, the lender formalises unconditional approval immediately after receiving the signed contract, and the deal moves. If the lender is still asking for income confirmation, bank statements, credit checks, and a signed contract all at once, the deal stalls.

For borrowers nervous about signing without an unconditional, the cleaner path is often to apply with a lender that doesn’t require a signed contract for unconditional approval in the first place. That’s the kind of policy-level call we make at the lender-selection stage.

Funding a build without a construction loan

Construction loans aren’t the only way to fund a build. If you have enough equity in your land or another property, some lenders will approve an equity release (a single drawdown loan increase) for the full amount needed for the build. The funds land in your account, and you pay your builder directly. There’s no progress payment schedule sitting between you and the build, and no lender invoices to send.

This structure works well in a few scenarios. If you own your land outright or have substantial equity in another property. If you want to control the timing and amount of payments to your builder yourself, rather than have a lender’s progress payment template dictate them. If your builder’s preferred payment schedule doesn’t fit a lender’s standard slab/frame/lock-up structure. Or if you simply want to skip progress payment valuation fees and the back-and-forth of inspections.

The structure can be set up to mimic a construction loan’s cashflow. If you take the equity release as an interest-only loan with a 100% offset account, you can park the full loan amount in the offset on day one. Interest is then only charged on the portion you’ve drawn out of the offset to pay the builder. As you make each builder payment, the offset balance drops and the interest charge steps up — the same scaling pattern as a true construction loan, but without the lender’s progress payment process sitting between you and your builder.

The real trade-off is oversight, not cashflow. With an equity release, there’s no lender’s valuer signing off each stage as an independent sanity check on the builder’s progress claims. If you trust your builder and want flexibility on payment timing, that’s an upside. If you’d rather have a third party verifying that what’s being invoiced has actually been built, the standard construction loan’s progress payment process is the safer structure.

We can run the numbers both ways — equity release versus construction loan — and show you which structure costs less in interest over the build period for your specific position. For renovations, granny flats, knockdown-rebuilds with strong equity, or builds on land owned outright, the equity release path is often cheaper and simpler.

Owner-builder construction loans in Australia

NSW owner-builder licensing (Fair Trading)

In NSW, you need an owner-builder permit from NSW Fair Trading if the building work is valued at more than $10,000 and the work requires development consent (either a DA or a CDC). If the value of the work is more than $20,000, you must complete an approved owner-builder education course before applying for the permit. An owner-builder can only hold one permit every five years for a principal place of residence.

The Home Building Compensation Fund (HBCF), which is the NSW equivalent of home warranty insurance, is statutory for residential building work valued over $20,000 and is held by the licensed builder, not the owner-builder. Because an owner-builder doesn’t carry HBCF cover for their own work, some of the statutory consumer protections don’t apply to an owner-builder build. Lenders factor that into their risk assessment.

Why lenders tighten LVR caps for owner-builders

Most lenders that accept owner-builder construction loan applications cap LVR at 50–70%, with 60% being the most common ceiling. A small number of lenders will stretch to 80% for strong applicants with a full-doc income, building experience, and a solid equity position. The tightening reflects higher risk: no fixed-price contract from a licensed builder, no HBCF cover on the owner-builder’s work, no professional site management.

If your LVR needs to be above 70%, our guarantor home loan guide covers one of the alternatives: using a family guarantor to boost the effective deposit without stretching the LVR.

Which lenders accept owner-builder applications

The pool of lenders is smaller than most borrowers expect. Among the big four, policies are conservative and often bespoke by branch. Specialist and second-tier lenders typically have more defined owner-builder policies, but with tighter LVR caps. We check the live panel at the time of application because owner-builder policy changes more often than standard home loan policy.

Knockdown-rebuild and building on vacant land

Using existing home equity for a knockdown-rebuild

If you already own the home being knocked down, the equity in the property funds the deposit on the rebuild. Total project cost (existing home equity + demolition + new build) is assessed against the expected end value of the completed home. The existing mortgage either rolls into the construction loan or is refinanced into the new structure at settlement.

Buyers building on a different block while still living in their current home sometimes need to fund both properties for a period before the old one sells. A bridging loan can cover the gap until settlement on the sale.

Demolition costs and progress payment timing

Demolition is typically funded as the first progress payment stage on a knockdown-rebuild, before slab stage. Demolition costs in Sydney run $15,000–$30,000 for a standard single-storey home, more if the site has asbestos or complex access. The lender will want confirmation that demolition has happened before releasing slab-stage funds.

Buying vacant land: two-part vs combined settlement

For buyers purchasing land and building separately, there are two structures. A two-part settlement: settle the land first on a standard vacant-land loan, then apply for the construction loan once the builder contract is signed. Or a combined land-plus-build loan under one facility. The combined structure is faster and cheaper but requires the land title to be registered and the builder contract near-finalised at the same time. If the land title hasn’t registered yet, a two-part structure is often the only option. Our article on getting a mortgage on recently registered land covers the timing issue.

NSW transfer duty on land-only purchases

Buying vacant land in NSW triggers transfer duty at the standard general rate unless an exemption or concession applies. Transfer duty figures are based on rates effective 1 July 2025, sourced from Revenue NSW.

| Land value | Duty payable |

|---|---|

| Up to $17,000 | $1.25 per $100 (minimum $20) |

| $17,001 – $32,000 | $212 + $1.50 per $100 over $17,000 |

| $32,001 – $85,000 | $445 + $1.75 per $100 over $32,000 |

| $85,001 – $319,000 | $1,372 + $3.50 per $100 over $85,000 |

| $319,001 – $1,064,000 | $9,562 + $4.50 per $100 over $319,000 |

| $1,064,001 – $3,721,000 | $43,087 + $5.50 per $100 over $1,064,000 |

| Over $3,721,000 | $186,667 + $7.00 per $100 over $3,721,000 (premium rate) |

On a $600,000 Western Sydney block, duty is $9,562 + 4.50% × $281,000 = $22,207 at the general rate.

First home buyer concession on vacant land (NSW)

Under the First Home Buyers Assistance Scheme, NSW first home buyers get a full transfer duty exemption on vacant land purchases up to $350,000, with a tapered concessional rate up to $450,000. Above $450,000, no concession applies and duty is charged at the general rate. Western Sydney land prices in 2026 routinely sit above the $450,000 threshold, which means most first home buyers building new in the area pay the full general rate on their land. The concession still helps borrowers buying smaller lots or building in more affordable regional areas.

Thresholds are indexed to CPI annually from 2025–26, so they step up each year.

Sydney and Western Sydney build cost benchmarks

Build costs per square metre in Sydney sit in four rough tiers:

- Budget / project builder (basic inclusions): $2,200 – $2,800/m²

- Mid-range (Western Sydney project home): $2,800 – $3,800/m²

- Mid-range (middle-suburb spec): ~$5,000/m²

- High-end / architect-designed: $5,500 – $7,600/m²

A typical 4-bedroom, 180–200m² build in Sydney’s middle suburbs runs $640,000–$880,000 for construction alone, excluding land. Source: Cotality Cordell Construction Cost Index (Dec 2025), Rider Levett Bucknall 2025, and Rawson Homes 2026.

The construction loan application process

Documents lenders require

The document pack for a construction loan is longer than a standard home loan. Expect to provide: signed fixed-price building contract with detailed progress payment schedule, council-approved plans (DA or CDC), builder’s licence, builder’s HBCF certificate (NSW) and contract works insurance certificate, soil test report, BAL (bushfire attack level) rating where required, and a valuation on the finished property done by the lender’s panel valuer. If you’re an owner-builder, add the NSW Fair Trading owner-builder permit and proof of the education course.

How long approval takes

From first application to unconditional approval, the typical timeline is three to six weeks, assuming the document pack is complete. Delays usually come from three places: council approval taking longer than expected, the builder being slow to finalise the contract, or the valuation coming in below the expected end value. The build itself is generally capped at 24 months from first drawdown, which is enough for most single-dwelling projects.

What happens at practical completion

At practical completion, the lender orders a final valuer inspection. Once the valuer confirms the home is built to plan, the final progress payment is released to the builder and the loan converts to a standard home loan. Repayments switch from interest-only on drawn funds to principal-and-interest on the full balance. The borrower arranges home and contents insurance to start from handover.

Common pitfalls and how to avoid them

Going over budget during the build

Overruns usually come from variations, which are changes you agree to during the build that add cost. The contract price you signed does not include variations unless they’re formally added to the contract. Keep variations to a minimum, price them before approving, and build a 5–10% contingency into your deposit to absorb legitimate overruns without a top-up.

Builder variations and progress claim disputes

A progress claim dispute usually means the builder has invoiced for a stage the valuer says is incomplete. Funds don’t release until the dispute is resolved. Document everything: dated photos of each stage, copies of every variation, written confirmation of approvals.

What happens if your builder goes under

Builder insolvency does happen. In NSW, HBCF cover (held by the licensed builder) protects the homeowner if the builder dies, disappears, becomes insolvent, or fails to rectify defects, up to the statutory limits. The claim process is run through icare, now the sole HBCF provider in NSW. If your builder loses HBCF eligibility mid-build, the lender will pause drawdowns until the situation is resolved. That’s why we check builder eligibility before the contract is signed.

How a mortgage broker helps with construction loans

Three things matter most on a construction loan, and banks don’t handle any of them from the borrower’s side. The first is reviewing the progress payment schedule before the contract is signed. The second is structuring the approval so you can sign the building contract with unconditional confidence. The third is picking the lender whose construction mechanics actually fit your build, not just the one with the sharpest headline rate.

Mortgage World Australia has been arranging construction loans for NSW clients since 2001, across 52+ lenders. We review your builder’s progress payment schedule before you sign, structure the approval so you’re never exposed, and pick the lender whose construction process fits the build you’ve actually contracted.

Frequently asked questions

How does a construction loan work in Australia?

A construction loan funds your build in stages rather than as a single lump sum at settlement. The lender releases progress payments to your builder after each stage is finished and inspected: typically deposit, slab, frame, lock-up, fit-out, and completion. You only pay interest on the amount drawn so far. Once the home is finished, the loan rolls over to a standard principal-and-interest home loan.

How much deposit do you need for a construction loan?

Most Australian lenders fund construction loans up to 95% LVR (including LMI), so a deposit of 5% of the total project cost is the practical floor. Borrowing above 80% LVR triggers LMI. If you already own the land, the equity in it can count toward your deposit.

Can I get a construction loan as an owner-builder?

Yes, but the pool of lenders is smaller and the rules are tighter. Most lenders cap owner-builder LVR at 50–70%, with 60% the most common ceiling. In NSW you also need an owner-builder permit from NSW Fair Trading if the work is valued over $10,000 and requires development consent, plus a completed owner-builder education course for work over $20,000.

Do you pay interest during construction?

Yes, on the portion of the loan that has been drawn down. Repayments during the build are interest-only on the drawn balance, so they start small and grow as each progress payment is released. At practical completion the loan converts to a standard home loan with principal-and-interest repayments.

What happens if construction goes over budget?

If the build goes over the contract price, usually because of variations, you either cover the overrun yourself or apply for a loan top-up. Top-ups are not guaranteed. Lenders will reassess your borrowing capacity and may require a fresh valuation. Avoid this with a fixed-price contract, a realistic contingency, and minimal variations once work starts.

Can you refinance a construction loan after it’s built?

Yes. Once the loan has rolled over to a standard home loan, you can refinance like any other mortgage. Construction loans from the big four usually sit above standard home loan rates, so many borrowers refinance soon after practical completion for a sharper rate.

How long does construction loan approval take?

Three to six weeks from application to unconditional approval in most cases. Timing depends on how fast you can supply the signed fixed-price contract, council-approved plans, builder insurances, and registered land title. The build itself is usually capped at 24 months from first drawdown.

Talk to a mortgage broker who builds with you

If you’re building in Western Sydney or anywhere in NSW and you want a broker who will review your builder’s progress payment schedule before you sign, and manage the conditional-to-unconditional approval bridge on your behalf, speak to Mortgage World Australia. We’ll structure the right construction loan for your build timeline and make sure the schedule works for you, not just your builder.

Speak to our mortgage brokers now — we have access to 52+ lenders and have been arranging construction finance for Australian buyers since 2001.

*This article contains general information only and does not constitute financial advice. Your personal financial situation, objectives and needs have not been considered. Before acting on any information, you should consider its appropriateness to your circumstances. Speak to a qualified mortgage broker for advice tailored to your situation. Mortgage World Australia Pty Ltd is a credit representative (CR No. 396946) of Mortgage Specialists Pty Ltd (Australian Credit Licence No. 38702

Patrick is a Director and a Home Loan Specialist. He has been helping Australians with home loans since 2001. Prior to working as a mortgage broker Patrick was employed by Macquarie Bank for 3 years and also worked as an accountant for a publicly listed company. Patrick’s qualifications include:

Bachelor of Business, UTS Sydney. Majored in accounting and sub-majored in Finance and Marketing.

Diploma of Finance and Mortgage Broking Management FNS50310

Certificate IV in Financial Services (Finance/Mortgage Broking) FNS40804

Ready to Take the Next Step?

Whether you’re looking to buy your first home, refinance, or explore investment opportunities, Mortgage World Australia is here to help.

Fill out the contact form below, and one of our expert mortgage brokers will be in touch shortly to discuss your needs and guide you through your options.

Get Started Today!