Rentvesting in Australia: A 2026 Strategy Guide

The complete rentvesting strategy guide for Australian property investors

On this page ▾

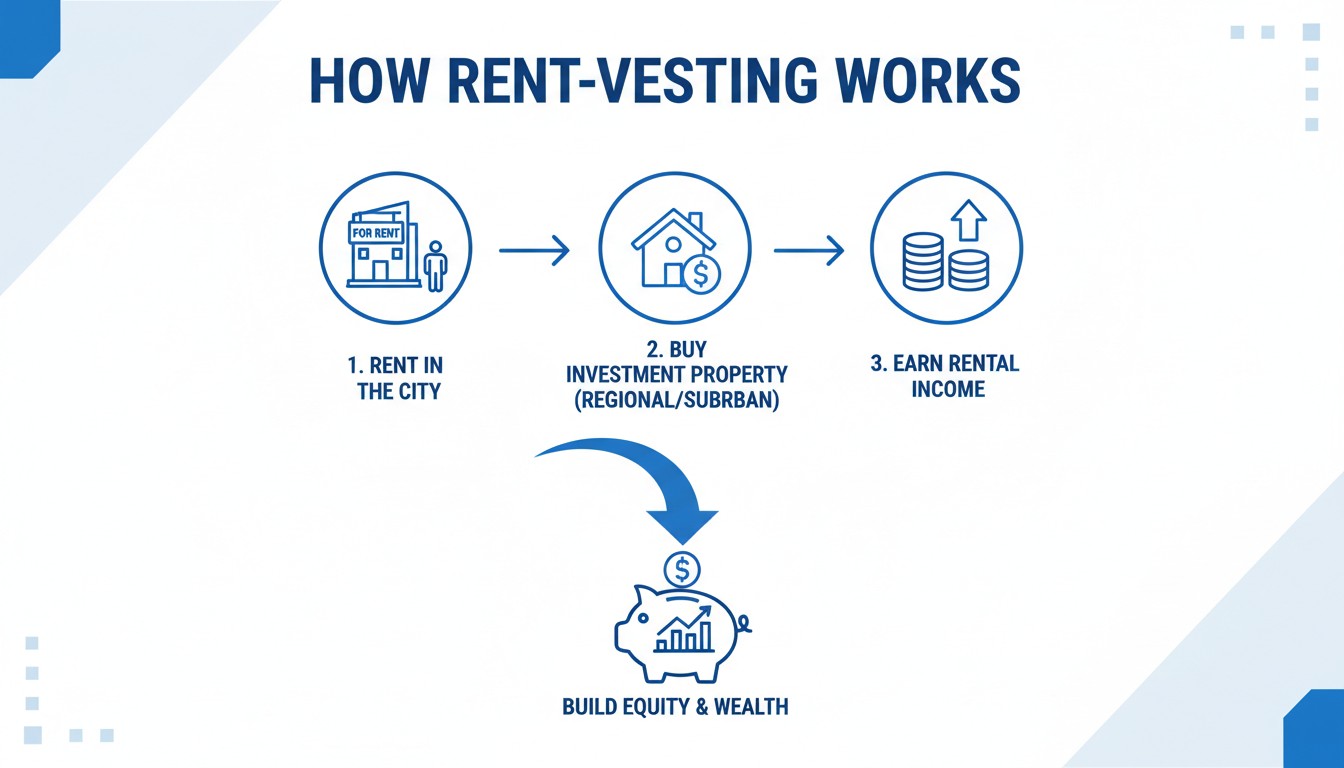

What is rentvesting?

Rentvesting means renting the home you live in while investing in a rental property elsewhere, usually in a more affordable market. Rather than saving for a large deposit on a home in the city where you work, you rent locally and use your available capital to purchase an investment property that generates rental income.The strategy appeals to buyers who want to invest in property wealth without waiting years to save a massive deposit, and who are willing to be landlords while still renting themselves. In Australia’s property market, where capital cities command high prices and growth potential varies by location, rentvesting is increasingly used as a way to access both lifestyle choices and investment returns.How rentvesting differs from buy-to-live investing

When most people talk about buying property, they mean owner-occupier purchases. You save a deposit, get a home loan, and buy a place to live. Your mortgage is tied directly to where you spend your life.Rentvesting flips this. You separate the property you occupy from the property you own. This gives you two key differences:First, you can choose where to invest based purely on growth potential and rental yield rather than where you want to live. A rentvester might rent an apartment in Sydney’s inner west but buy an investment property in a regional growth corridor where yields are higher and capital is more efficient.Second, you’re managing a rental property while being a tenant yourself. This means you have a landlord relationship with someone else, and you have tenants in your investment property. It adds complexity compared to simply buying and living in your own home.The rise of rentvesting in Australia

Rentvesting gained momentum in the 2010s as Australian property prices, particularly in Sydney and Melbourne, climbed beyond what many buyers could realistically save for. Rental markets also became more stable and competitive, making long-term renting a viable option for people who wanted flexibility.The strategy accelerated further post-2020, as remote work became more common and younger investors started questioning whether they needed to buy in their local market at all. Today, rentvesting is common among professionals, investors building portfolios, and first home buyers who prefer to keep their options open rather than commit to a mortgage at the top of the market.How rentvesting works: the fundamentals

Let’s work through the practical side of how rentvesting actually functions from a borrowing and tax perspective.

Let’s work through the practical side of how rentvesting actually functions from a borrowing and tax perspective.The deposit and loan requirements

To purchase an investment property, you’ll need a deposit. Most Australian lenders require a minimum 20% deposit for investor loans. If you put down less, typically 10-15%, you’ll pay lenders mortgage insurance (LMI), which protects the lender against default risk. LMI is a one-off premium added to your loan, and it’s non-refundable even if you later increase equity.Here’s a rough example. If you’re buying a $500,000 investment property with a 20% deposit:Deposit required: $100,000 Loan amount: $400,000 LMI: None Total cash needed: $100,000 + purchase costs such as stamp dutyIf you put down 15%:Deposit required: $75,000 Loan amount: $425,000 LMI: Approximately $4,500-$5,500 (added to loan) Total cash needed: $75,000 + LMI + purchase costs such as stamp dutyMost rentvesting investors target the 20% mark to avoid LMI costs, especially if they’re planning to negatively gear the property. Every dollar counts when you’re subsidising the shortfall from your salary.Mortgage and borrowing capacity as a rentvestor

Here’s where rentvesting gets interesting. When you apply for an investment property loan, lenders assess your serviceability differently than they do for owner-occupier loans.Lenders will stress-test your ability to service the loan at a higher interest rate, often assuming rates rise 2-3% above the current rate. If the current interest rate is currently 6.1%, a lender might assume you can service the loan at 9.1%. This is designed to ensure you can meet the repayment requirements if rates spike during your loan term.They’ll also consider your rental income. If your investment property is expected to generate $25,000 per year in rent, many lenders will count 80% of this as actual income when assessing your application. This can lift your borrowing capacity compared to an owner-occupier scenario, where no rental income applies.Your living costs still matter. If you’re renting your own home, the lender will factor in your rental expense.If you still live at home with your parents rent-free, your borrowing power will be substantially higher. In this case, most lenders will factor in a nominal notional rent of $150 per week.The net result is that being a rentvestor doesn’t necessarily hurt your borrowing capacity, especially if your rental income is strong. It just adds another variable to the calculation.Rentvesting pros and cons

Like any strategy, rentvesting has genuine advantages and real downsides. Understanding both is critical before you commit.| Advantages | Disadvantages |

|---|---|

| Access to property investment without waiting years to save a deposit in an expensive market. | You’re paying rent and a mortgage simultaneously, which requires strong cash flow. |

| Potential for capital growth in an investment property purchased in a different, potentially better-performing market. | Tenant problems, vacancy periods, and maintenance costs reduce rental income unpredictably. |

| Tax benefits through negative gearing, where rental losses offset your salary income. | You don’t benefit from paying down equity in the property you live in. Rent is gone once paid. |

| Flexibility to move without being locked into a mortgage in a particular location. | Interest rates on investment loans are typically 0.25-0.5% higher than owner-occupier rates. |

| Ability to build multiple investment properties while keeping lifestyle options open. | Being a landlord from a distance (managing tenants, repairs, contractors) adds stress and time. |

| Rental income can help service the investment loan, improving your serviceability. | If the investment property doesn’t perform, you’re stuck subsidising a loss on top of paying rent. |

Tax benefits and financial mechanics

This is where rentvesting starts to make financial sense for many investors. The tax advantages are significant and often misunderstood.Negative gearing and tax deductions

When you own a rental property, you can claim deductions for expenses directly tied to earning rental income. This includes:Mortgage interest (not principal repayments) Property management fees Land tax and council rates Insurance Repairs and maintenance Depreciation of fixtures and fittings Advertising for tenants Accountancy and legal feesIf these expenses exceed your rental income in a given year, you’ve made a loss. That loss can be deducted from your other income, like your salary. If you earn $80,000 and your rental property makes a $15,000 loss, your taxable income drops to $65,000.At a marginal tax rate of 37% (plus Medicare levy), that $15,000 loss saves you around $5,550 in tax. In effect, you’ve reduced your negative gearing cost by nearly 37%. The Australian Taxation Office (ATO) allows this because you’re genuinely operating the property as a rental investment.For rentvesting, negative gearing is often the reality in early years. Rent might cover 70-80% of your mortgage interest plus expenses. The gap is subsidised from your salary, but that subsidy is partly offset by tax savings.Capital gains tax on investment property

When you sell your investment property at a profit, the difference between what you paid and what you sold it for is a capital gain, and it’s taxable.Here’s the important part: if you’ve owned the property for 12 or more months, you get a 50% capital gains tax discount as an individual investor. This means only half of your gain is added to your assessable income.Example. You buy for $500,000 and sell for $650,000 three years later. Capital gain is $150,000. With the 50% discount, your assessable gain is $75,000. At 37% tax, you’d owe about $27,750 in tax, compared to $55,500 if the discount didn’t apply.This discount applies to most investment property scenarios and makes a significant difference to your net proceeds. It’s one of the reasons property is popular as a long-term investment vehicle.Is rentvesting right for you?

Rentvesting requires a specific financial situation and mindset. If you don’t meet these criteria, it’s probably not the right strategy.Income and credit requirements

To rentvest successfully, you need:A stable, reasonably high income. Most lenders want to see at least $60,000-70,000 per year before they’ll seriously consider an investment property loan. The higher your income, the more you can borrow for investment properties. If your income is modest, you will be limited on how much you can spend on an investment property.Strong credit history. Any defaults, missed payments, or court judgments will hurt your application. Lenders scrutinise investment loan applications more heavily than owner-occupier ones, so your credit file needs to be clean.Cash flow discipline. You’ll be paying rent and a mortgage from the same income. This requires budgeting carefully and having a buffer for unexpected costs. If your investment property needs roof repairs mid-year, can you cover it without going into credit card debt? Many rentvesting investors set aside $200-400 per month for maintenance and vacancy.An emergency fund. Beyond the deposit, you should have 3-6 months of expenses saved. Rentvesting amplifies financial stress if unexpected costs hit.Best suburbs and locations for rentvesting

The logic of rentvesting is that you rent in an expensive market (where you want to live) and invest in a more affordable, high-growth market (where capital appreciation potential is better).This works best if there’s a meaningful gap between rental markets and investment opportunities. For example:A professional working in inner Sydney might rent a place in the inner west ($800+ per week) while investing in a regional growth area like the Riverina or North Coast, where properties cost $550,000-750,000 with rental yields of 4-5%.Someone in Melbourne might rent locally while investing in growth suburbs in regional Victoria or even across into Queensland, where entry prices are lower.The key is finding a market where you can build equity and rental income without huge price tags. Regional Australian property markets often offer this, but do your own research. Not all regional areas have strong rental demand or population growth.Rentvesting strategy checklist

If you’ve decided rentvesting is worth exploring, here’s a step-by-step framework to get started.Step 1: Define your investment goals

Start by asking what success looks like. Are you aiming for capital growth, rental yield, or a blend? Are you building a portfolio of three properties, or just one? What’s your timeline? Do you need cash flow now, or can you subsidise negative gearing for five years and expect capital gains to be the payoff?Write these goals down. They’ll guide every decision that follows, from location choice to deposit size.Step 2: Assess your financial position

Do a real audit of your cash flow. How much can you genuinely afford to put down as a deposit without stripping your emergency fund? What’s the gap between your salary and your rental costs, and how much of that gap can absorb a negatively geared property?Calculate your borrowing capacity. Talk to a mortgage broker before you start seriously looking at properties. They can tell you exactly how much you can borrow for an investment property given your income, expenses, and existing debts.Review your credit report. If there are issues, fix them before applying for a loan. A single missed payment can cost you thousands in serviceability.Step 3: Research markets and properties

Once you know how much you can spend, identify regions where that money goes furthest. Look at rental yields, population growth, employment data, and recent price trends. PropertyShark, Real Estate Institute data, and ABS census information are all good sources.In your chosen market, look at actual properties. What condition are they in? Do they attract quality tenants easily? What’s the typical maintenance cost? A cheap property that needs constant fixing will eat your cash flow.Connect with local property managers. They understand rental demand, typical tenant profiles, and which properties perform best. Their insights are invaluable.Step 4: Secure pre-approval and finance

Once you’ve found a property you’re serious about, get pre-approval from a lender. Pre-approval tells sellers you’re a genuine buyer and gives you certainty about how much you can borrow.When you’ve found the right property, your broker will help you navigate the full loan application. Be prepared to provide payslips, tax returns, bank statements, and rental history. Investment loan applications are scrutinised more closely than owner-occupier ones.Common rentvesting questions

Is rentvesting a good idea?

Rentvesting can be a solid wealth-building strategy, but it depends entirely on your financial goals, cash flow, and market conditions. It works best for those who can afford to subsidise a loss through negative gearing and want to access better property markets without settling down geographically. However, it comes with ongoing vacancy risk and being a landlord at a distance. We recommend getting pre-approval before committing to this strategy so you understand exactly how much you can borrow and what your serviceability looks like with investment property rates factored in.What deposit do I need to start rentvesting?

Investment properties typically require a minimum 20% deposit. You can go lower with lenders mortgage insurance, with some lenders now lending up to 95% of the property value for investment properties, but this adds cost and reduces your equity buffer. First-time investors often go the 20% route to avoid LMI, especially if they’re committing to negative gearing and want lower monthly outgoings.How does tax work for rentvestors?

You can claim rental expenses like mortgage interest, property management, maintenance, and insurance against your rental income. If expenses exceed rental income, the loss can be deducted against your other income, like salary, reducing your taxable income. When you sell, if the property has gained in value and you’ve owned it for 12 or more months, you get a 50% capital gains tax discount as an individual investor.Can first home buyers rentvest?

Yes, first home buyers can rentvest, but government schemes like the Australian Government 5% Deposit Scheme do not apply to investment properties. These schemes are exclusively for first home buyers purchasing their primary residence. You’ll need to fund an investment property with traditional borrowing and a 5% deposit plus purchase costs as a minimum.Do I need to declare rentvesting to my mortgage lender?

Absolutely. When applying for an investment property loan, you must disclose your rental situation to your lender. Many lenders take rental income into account when assessing serviceability on your investment loan, which can actually help your borrowing capacity if your rent covers a portion of your living costs.How Mortgage World Australia can help

Rentvesting works best when you have expert guidance on borrowing and loan structuring. At Mortgage World Australia, we’ve helped hundreds of investors navigate rentvesting over 25 years.We have access to 52+ lenders, which means we can find competitive rates and terms tailored to your situation. We can also help you structure your loan efficiently, using tools like interest-only periods (allowing you to offset rental losses more effectively) and redraw facilities (giving you flexibility when your investment property performs well).Most importantly, we’ll stress-test your finances realistically and make sure you understand the cash flow impact before you commit. Rentvesting only works if you can genuinely afford the shortfall. We’ll help you figure out if you can.If you’re considering rentvesting and want to explore your options, get in touch. We’ll run through your numbers, show you what you can borrow, and discuss how to structure your portfolio for long-term wealth.This article contains general information only and does not constitute financial advice. Your personal financial situation, objectives and needs have not been considered. Before acting on any information, you should consider its appropriateness to your circumstances. Speak to a qualified mortgage broker for advice tailored to your situation. Mortgage World Australia Pty Ltd is a credit representative (CR No. 396946) of Mortgage Specialists Pty Ltd (Australian Credit Licence No. 387025).

Author: Patrick O’Brien, Director and Home Loan SpecialistPatrick has been helping Australians finance property purchases and grow their wealth through property investment for over 25 years. He is the owner of Mortgage World Australia and brings direct experience in structuring investment loans, managing negative gearing, and helping rentvesting investors build portfolios.

Patrick is a Director and a Home Loan Specialist. He has been helping Australians with home loans since 2001. Prior to working as a mortgage broker Patrick was employed by Macquarie Bank for 3 years and also worked as an accountant for a publicly listed company. Patrick’s qualifications include:

Bachelor of Business, UTS Sydney. Majored in accounting and sub-majored in Finance and Marketing.

Diploma of Finance and Mortgage Broking Management FNS50310

Certificate IV in Financial Services (Finance/Mortgage Broking) FNS40804

Ready to Take the Next Step?

Whether you’re looking to buy your first home, refinance, or explore investment opportunities, Mortgage World Australia is here to help.

Fill out the contact form below, and one of our expert mortgage brokers will be in touch shortly to discuss your needs and guide you through your options.

Get Started Today!