Reverse Mortgage Australia: How It Works & 2026 Rates

Reverse mortgage Australia: how it works, what it costs, and whether it’s right for you (2026 guide)

On this page ▾

- What is a reverse mortgage?

- How a reverse mortgage works in Australia

- How much can you borrow?

- Reverse mortgage interest rates in Australia (2026)

- Which lenders offer reverse mortgages in Australia?

- Worked Sydney example — a $1.4M family home

- Reverse mortgage vs Home Equity Access Scheme (HEAS) — head to head

- How a reverse mortgage affects the Age Pension and Centrelink

- Negative equity protection — Australia’s borrower safety net

- Risks and downsides — the honest list

- When a reverse mortgage makes sense — five use cases

- Alternatives to a reverse mortgage

- Is a reverse mortgage right for you? A decision framework

- How a mortgage broker helps with a reverse mortgage

- Frequently Asked Questions

Australians aged 60 and over hold roughly $3 trillion in home equity, according to a Deloitte survey released in March 2026. Only about 1% of that equity is currently being accessed through reverse mortgages or other equity-release products.

That gap — $3 trillion sitting idle while many retirees struggle to fund aged care or top up a shrinking pension — is what makes reverse mortgages worth understanding properly, not as a product to fear, and not as a magic solution. It is a tool that works well in specific circumstances and badly in others.

We see this regularly: clients in their late 60s who are asset-rich and cash-poor, sitting on $1.2 million in Sydney property equity and genuinely unsure whether a reverse mortgage is a trap or a lifeline. This article covers how these products work, what lenders are charging right now, and the questions worth answering before you sign anything.

What is a reverse mortgage?

The plain-English definition

A reverse mortgage is a loan secured against your home that you do not repay until you sell, move into aged care, or pass away. Instead of making monthly repayments, the interest compounds and is added to your loan balance. You continue to own your home throughout.

Australian reverse mortgages are regulated under the National Credit Code, and since July 2012, all new loans carry a statutory no-negative-equity guarantee, meaning you can never owe more than your home is worth. ASIC’s Moneysmart describes it as access to equity without requiring you to sell.

Why only ~1% of eligible home equity is accessed this way

The Deloitte March 2026 survey found 40,000+ households across Australia currently hold reverse mortgages, with $5.5 billion in outstanding balances. For a country with $3 trillion in housing equity held by over-60s, that is a remarkably small uptake.

Two factors explain the gap. The product carries a complicated reputation, some of it deserved from pre-2012 products that lacked negative-equity protection, much of it based on a misunderstanding of how Australian law works now. And the compounding maths genuinely does erode equity over time, which most lender pages don’t present honestly. This article does.

How a reverse mortgage works in Australia

Step 1 — Eligibility check (age, property type, LVR cap)

You must be at least 55 years old (Heartland Bank’s minimum) or 60–65 depending on the lender. The property must be your principal place of residence, owned outright or with a small remaining mortgage. A lender will order a valuation. Your loan-to-value ratio (LVR) — the amount you can borrow expressed as a percentage of the property’s value — is capped based on your age at application.

Step 2 — Choose your drawdown (lump sum, income stream, line of credit, combination)

You can receive funds as a lump sum, a regular income stream (fortnightly or monthly), a line of credit to draw on as needed, or a combination of these. Most borrowers opt for a lump sum or a combination, according to the Deloitte survey. The drawdown structure affects both how quickly the balance grows and how your Centrelink entitlements are affected.

Step 3 — Interest compounds monthly (no repayments while you live in the home)

No monthly repayments are required while you live in the property. Interest accrues on your outstanding balance and is added to the loan each month. At 8.79% per year, a balance compounds hard over a decade or two — and that compounding is the part most lender websites gloss over. The scenarios later in this article show the real numbers.

Step 4 — Loan repaid when you sell, move into aged care, or pass away

The full balance — original principal plus all accumulated interest — is repaid from sale proceeds when you leave the home permanently or your estate is settled. Any remaining sale proceeds belong to you or your estate.

How much can you borrow?

The 15-to-50 percent rule

The maximum you can borrow on a reverse mortgage is determined by your age and the lender. The LVR increases as you get older, reflecting the shorter period over which interest compounds.

LVR by age — the standard Australian schedule

Heartland Bank, Australia’s market leader with 40%+ market share, publishes this schedule:

| Age | Maximum LVR |

|---|---|

| 55 | 15% |

| 60 | 20% |

| 65 | 25% |

| 70 | 30% |

| 75 | 35% |

| 80 | 40% |

| 85 | 45% |

| 90 | 50% |

On a $1.4 million Sydney property, a 65-year-old could borrow up to $350,000 ($1.4M × 25%). Other lenders use different schedules: P&N Bank caps at 35% regardless of age; Unity Bank caps at 40% or $400,000, whichever is lower.

The Moneysmart Reverse Mortgage Calculator lets you model different ages, drawdown amounts, and time horizons before speaking to a lender.

How couples and joint borrowers are treated

For joint applications, the LVR is based on the younger borrower’s age. A couple where one partner is 68 and the other is 72 would have their LVR set at the 68-year-old’s rate — typically the 65-age-band rate of 25%. Each lender applies this rule slightly differently, so ask explicitly when comparing.

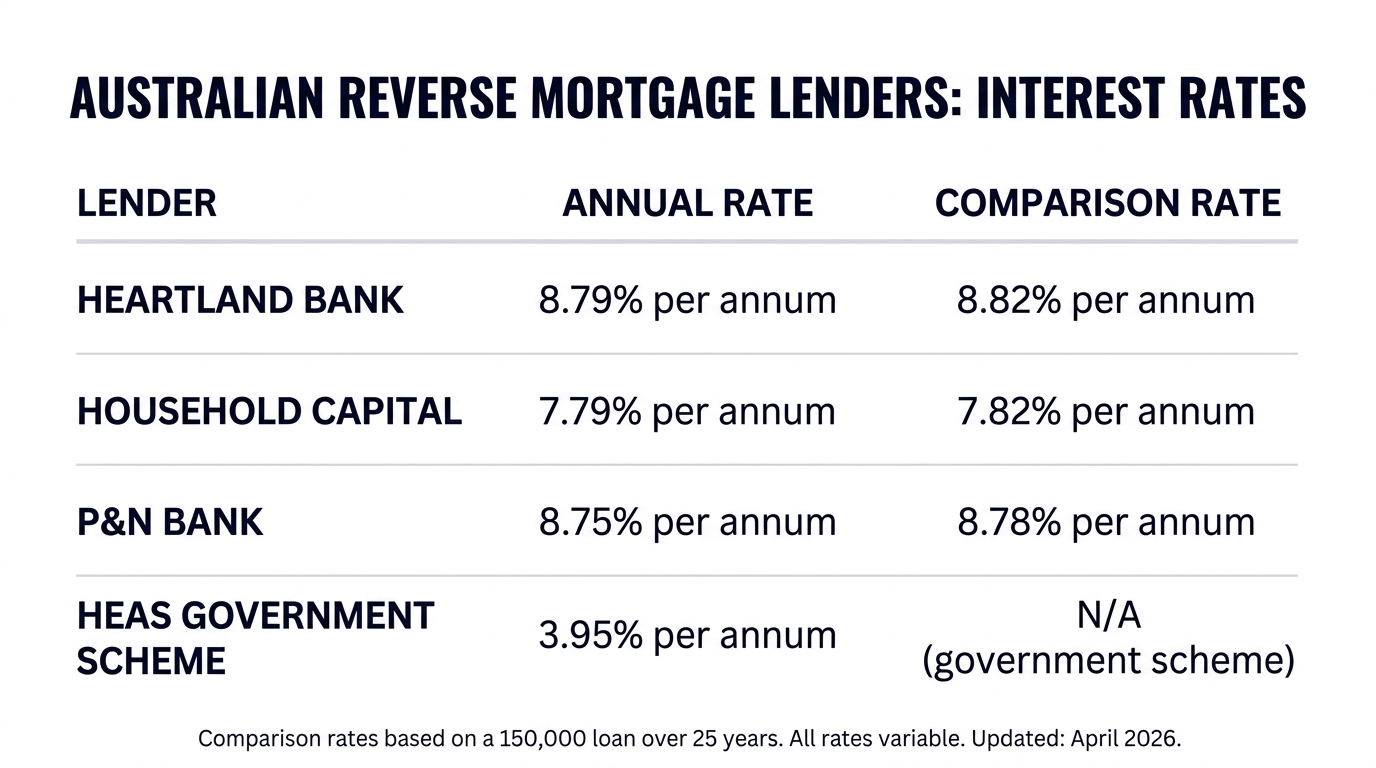

Reverse mortgage interest rates in Australia (2026)

Rate ranges by lender — Heartland, P&N, Unity, Household Capital

Commercial reverse mortgage rates sit well above standard home loan rates. Current published rates as at April 2026:

| Lender | Rate (p.a.) | Comparison Rate | Notes |

|---|---|---|---|

| Household Capital (ORIO 100) | 7.79% | 7.82% | Lowest available — specific drawdown structure required |

| Household Capital (Retirement Refi) | 8.29% | 8.32% | — |

| P&N Bank | 8.75% | 8.78% | Perth metro only; age 65+ |

| Heartland Bank | 8.79% | 8.82% | Market leader; age 55+ |

| HEAS (government) | 3.95% | N/A | See HEAS section below |

Comparison rates are based on $150,000 over 25 years. All commercial rates are variable.

WARNING: This comparison rate applies only to the example given and may not include all fees and charges. Different terms, fees or other loan amounts might result in a different comparison rate.

Why reverse mortgage rates sit above standard home loan rates

Standard variable home loans averaged 6–7% in April 2026. Reverse mortgage rates are 8.75–8.79% because lenders carry considerably more risk: no monthly repayments, unpredictable repayment timing, and a compounding balance that could approach property value over a long period. That risk premium is built into the rate — and it’s the reason comparing lenders matters more here than on a standard home loan.

Fixed vs variable

Most Australian reverse mortgage products are variable-rate only. Heartland Bank and Household Capital both offer variable rates exclusively. If rate certainty matters, the Home Equity Access Scheme’s 3.95% government rate has been unchanged since January 2022 — though its drawdown limits are strict.

ASIC’s reverse mortgage projections calculator is a useful tool for modelling rate scenarios. Lenders are legally required to use it before entering into a contract.

Which lenders offer reverse mortgages in Australia?

Active in 2026 — Heartland Bank, P&N Bank, Unity Bank, Household Capital

The market has contracted from its peak. Lenders currently accepting new applications:

| Lender | Min. Age | Geographic Restriction | Max. LVR | Type |

|---|---|---|---|---|

| Heartland Bank | 55 | National | 50% (age 90) | Specialist |

| Household Capital | 60 | National | Contact lender | Specialist non-bank |

| P&N Bank | 65 | Perth metro only | 35% | Credit union |

| Unity Bank | 60 | National | 40% or $400,000 | Credit union |

| HEAS (government) | 67 | National | ~150% max pension rate | Government scheme |

Exited or withdrawn — Commonwealth Bank, NAB, Pepper Money, Westpac

Several lenders have left the market in recent years:

- Commonwealth Bank / Bankwest — withdrew effective 1 January 2019

- NAB — withdrew 2018–2019

- St George, Bank of Melbourne, BankSA (all Westpac group) — withdrew around July 2017

- Westpac direct — withdrew around the same time as its subsidiaries

- IMB Bank — no longer accepting new reverse mortgage applications (existing customers retained)

- Pepper Money — not currently offering

If you’ve searched “NAB reverse mortgage” or “Commonwealth Bank reverse mortgage”, you’ll find plenty of legacy results — but neither institution offers the product in 2026. The major banks’ exits followed the banking royal commission and increased ASIC scrutiny of the sector.

How a broker compares across all of them

Heartland, Household Capital, P&N Bank, and Unity Bank all use different LVR schedules, rate structures, and drawdown rules. A broker who works with reverse mortgages can compare all active lenders in one conversation. If P&N Bank’s Perth-only restriction rules you out, or Household Capital’s ORIO 100 structure suits your drawdown needs, that’s a five-minute conversation rather than four separate lender calls.

Worked Sydney example — a $1.4M family home

The numbers below are what we actually model when a client asks, “How bad can the compounding get?” They use Heartland Bank’s current 8.79% variable rate and assume 3% annual property growth — conservative for Sydney. All figures are illustrative; they assume no additional draws after the initial amount, and a constant rate over the period.

Scenario A — Age 65 single: $200,000 lump sum + $1,000/month income

Maximum available at age 65: $1,400,000 × 25% = $350,000. The borrower takes $200,000 immediately and draws $1,000/month as an income stream.

| Year | Loan Balance | Property Value (3% growth) | Remaining Equity |

|---|---|---|---|

| 10 | ~$672,000 | ~$1,882,000 | ~$1,210,000 |

| 15 | ~$1,116,000 | ~$2,181,000 | ~$1,065,000 |

| 20 | ~$1,804,000 | ~$2,529,000 | ~$725,000 |

Over 20 years, the borrower receives $200,000 upfront plus $240,000 in income stream payments — $440,000 total drawn. The estate retains an estimated $725,000 in equity at that point.

Scenario B — Age 70 couple: $400,000 lump sum

Maximum available at age 70: $1,400,000 × 30% = $420,000. The borrower takes $400,000 as a lump sum.

| Year | Loan Balance | Property Value | Remaining Equity |

|---|---|---|---|

| 10 | ~$961,000 | ~$1,882,000 | ~$921,000 |

| 15 | ~$1,488,000 | ~$2,181,000 | ~$693,000 |

| 20 | ~$2,307,000 | ~$2,529,000 | ~$222,000 |

At 20 years, the no-negative-equity guarantee is still intact — the balance ($2.3M) sits below the property value ($2.5M). If property growth were slower or rates moved higher, that margin would narrow considerably.

Scenario C — Age 75 single: $250,000 lump sum

Maximum available at age 75: $1,400,000 × 35% = $490,000. The borrower takes $250,000.

| Year | Loan Balance | Property Value | Remaining Equity |

|---|---|---|---|

| 10 | ~$600,000 | ~$1,882,000 | ~$1,282,000 |

| 15 | ~$930,000 | ~$2,181,000 | ~$1,251,000 |

| 20 | ~$1,442,000 | ~$2,529,000 | ~$1,087,000 |

How the numbers look after 10, 15, and 20 years

The pattern across all three scenarios: the loan balance grows faster in later years, because interest is charged on a larger base. Property growth at 3% partially offsets this, but not fully at 8.79%. Taking a smaller draw, or drawing as an income stream rather than a lump sum, extends the time before equity is meaningfully eroded. Starting at 75 rather than 65 with the same property produces noticeably better estate outcomes since the compounding simply has less runway.

Reverse mortgage vs Home Equity Access Scheme (HEAS) — head to head

What HEAS is (and why it used to be called the Pension Loans Scheme)

The Home Equity Access Scheme is a government loan administered by Services Australia. It was called the Pension Loans Scheme until 1 January 2022, when it was renamed and its eligibility expanded to include Australians who don’t receive a pension at all. Many search results for “Centrelink reverse mortgage” or “government reverse mortgage scheme” are referring to HEAS.

Eligibility, rates, drawdown — side by side

| Feature | Commercial Reverse Mortgage | Home Equity Access Scheme (HEAS) |

|---|---|---|

| Minimum age | 55 (Heartland); 60–65 others | Age Pension age (67 for most) |

| Who can apply | Any eligible homeowner | Pensioners and non-pensioners (age 67+) |

| Interest rate | 8.75–8.79% p.a. (variable) | 3.95% p.a. (compound fortnightly) |

| Maximum draw | Up to 50% LVR (age-based) | Up to 150% of max pension rate |

| Drawdown options | Lump sum, income, line of credit | Fortnightly payments; limited lump sum |

| Lump sum advance | Yes — any amount within LVR | Capped at ~$15,323 per 26-fortnight period |

| Administered by | Private lender | Services Australia |

See Services Australia’s HEAS page for current eligibility, rates, and drawdown limits.

When HEAS is the better choice

If you’re at least 67 and need a modest but regular income supplement, HEAS at 3.95% is almost always the cheaper path — roughly half the rate of any commercial product available in 2026. The government rate has been unchanged since January 2022. For someone drawing $500–$800 per fortnight as a pension top-up, that rate difference adds up to tens of thousands of dollars in preserved equity over a decade.

When a commercial reverse mortgage is the better choice

HEAS has strict drawdown limits — you cannot access large lump sums through it. If you need $300,000 for an aged-care bond (Refundable Accommodation Deposit, or RAD), a commercial reverse mortgage is typically the only equity-release vehicle that can deliver that amount. And if you’re under 67 and not yet at Age Pension age, HEAS is not available to you.

How a reverse mortgage affects the Age Pension and Centrelink

The income test (drawdowns treated as loan proceeds, not income)

Reverse mortgage loan proceeds are not treated as income under the Centrelink income test. Money borrowed against your home is classified as a loan, not earnings, and does not reduce your pension payment on that basis alone.

The assets test (the $40,000 lump-sum rule and why it matters)

The assets test works differently. Under Services Australia rules:

- The first $40,000 you receive is exempt from the assets test for up to 90 days

- After 90 days, or for amounts above $40,000, unspent loan proceeds become assessable financial assets

- Assessable financial assets are subject to deeming — treated as earning income at current deeming rates even if held in cash

Spending the funds on your principal home (renovations, modifications) generally removes them from assessment entirely.

Worked example — how a $200k drawdown changes pension entitlements

A single homeowner on the full Age Pension draws $200,000 as a lump sum. In the first 90 days, the first $40,000 is exempt from the assets test. From day 91, the remaining $160,000, and the original $40,000 if unspent, become an assessable financial asset. At current deeming rates, that triggers deemed income and could reduce the fortnightly pension by hundreds of dollars.

The exact impact varies by situation. Services Australia’s Financial Information Service (FIS) offers free consultations — use it before drawing.

Negative equity protection — Australia’s borrower safety net

The 2012 statutory guarantee (no negative equity)

The National Credit Code (as amended in 2012) includes a statutory no-negative-equity guarantee for all reverse mortgages entered into from 18 September 2012. Credit providers are prohibited from requiring repayment of more than the market value of the mortgaged property. This applies across all Australian lenders, not just individual lender policy.

Loans taken out before that date may not have this protection — relevant for existing borrowers considering refinancing an older product.

How it differs from the US “95% rule”

US reverse mortgages (FHA-insured HECMs) operate under a “95% rule” — the borrower owes up to 95% of the property’s appraised value, with FHA insurance covering the rest. Australian reverse mortgages work differently: the no-negative-equity guarantee is statutory and unconditional, and there is no mortgage insurance premium equivalent to the US HECM.

What happens if your home’s value falls below the loan balance

In theory, this is the guarantee in action. If your home sells for $800,000 and your loan balance is $950,000, the lender absorbs the $150,000 shortfall. In practice, lenders set conservative LVR caps precisely to make this unlikely, particularly at younger ages, where compounding has more time to work.

Risks and downsides — the honest list

Compounding interest erodes the estate

The interest charged in year 15 is far larger than in year 1, because it’s charged on a much larger balance. The scenarios earlier in this article show a $200,000 lump sum growing to $1.15 million over 20 years. That growth comes directly from the equity your estate would otherwise receive. It is the defining risk of these products, and it’s worth spending time with the numbers before signing.

Reduced inheritance for children and beneficiaries

Families where adult children expect to inherit the family home should understand the compounding impact in dollar terms before the borrower signs. The conversation is far easier before the loan than after, and a broker-run projection gives you real figures to share with your family, not rough estimates.

Ongoing costs (council rates, insurance, maintenance) are still yours

Council rates, strata levies, home insurance, and maintenance remain your responsibility throughout the loan. Failing to maintain the property or keep insurance current is a condition of default under most reverse mortgage agreements.

Restrictions on renting, sub-letting, and long-term absence

Most lenders require the property to remain your principal place of residence. Extended absences, typically more than 12 months, may trigger a loan condition review. Renting the property without lender consent is a breach of contract under most agreements.

That said, there are genuine cases where a reverse mortgage is the right tool. Here’s an honest summary:

Pros and cons at a glance:

| Pros | Cons |

|---|---|

| Access equity without selling | Compounding interest erodes equity quickly |

| No monthly repayments required | Rates 8.75–8.79% — well above standard home loans |

| Remain in your home | Reduces inheritance for the estate |

| No-negative-equity guarantee (post-2012) | Ongoing obligations: insurance, maintenance, council rates |

| Flexible drawdown: lump sum, income, line of credit | Restrictions on renting or extended absences |

| Can fund aged-care bonds, home modifications | Centrelink assets test impact on unspent drawdowns |

When a reverse mortgage makes sense — five use cases

Topping up retirement income. An income stream of $1,000–$2,000 per month can meaningfully supplement a pension or super drawdown for someone who is asset-rich but cash-poor. This is the most common scenario we see, and often the least risky. Smaller regular draws compound more slowly than a large lump sum.

Paying for an aged-care bond (RAD). Refundable Accommodation Deposits for residential aged care regularly run $400,000–$700,000 in Sydney. A reverse mortgage can fund the RAD without forcing a sale of the family home, particularly where a spouse remains living in it.

Home modifications for ageing in place. Bathroom modifications, stairlifts, and ramps are a common use case in the $50,000–$100,000 range. Spending on the principal home typically does not increase your assessable asset position, which makes this one of the cleaner drawdown scenarios from a Centrelink perspective.

Clearing an existing mortgage at retirement. If a small mortgage remains at retirement, a reverse mortgage lump sum can clear it and eliminate repayment obligations. Read more about strategies to pay off your home loan early before reaching this point.

Living inheritance — helping adult children into the market. Some borrowers draw a lump sum to contribute to a child’s deposit while they can still see them buy. The amount drawn reduces the estate accordingly. That conversation needs to happen openly with the family before signing, not after.

Alternatives to a reverse mortgage

Downsizing (and the $300,000 downsizer super contribution)

Selling a larger home and buying something smaller releases equity without a loan. Since 1 January 2023, homeowners aged 55 or older who sell a home they’ve held for 10+ years can contribute up to $300,000 per person ($600,000 for couples) of the sale proceeds to superannuation as a downsizer contribution, outside normal contribution caps. The scheme has been available since July 2018, with the eligible age progressively lowered from 65 to 60 (July 2022) and then to 55 (January 2023).

Home Equity Access Scheme

Covered in detail earlier. If you’re 67 or older and need a modest regular income, HEAS at 3.95% is almost always cheaper than any commercial product.

Standard refinance or equity release loan (if you’re still working)

For borrowers who still earn income and can service a standard loan, a refinance or line of credit gives access to equity at 6–7% rather than 8.79%. Read more about how an equity loan works and using existing equity to buy an investment property. If serviceability isn’t a constraint, refinancing your home loan is the more cost-effective path.

Family loan or joint ownership arrangement

Some families structure a private loan from adult children, or add a family member to the title in exchange for a cash payment. These arrangements need careful legal structuring to avoid stamp duty issues, title complications, and the kind of family friction that becomes difficult to untangle if circumstances change.

No-interest loans (Good Shepherd / NILS) for specific purposes

For smaller, targeted needs (up to $3,000), the Good Shepherd No Interest Loan Scheme provides interest-free credit for specific essential items. Not a substitute for a reverse mortgage, but worth knowing when the need is modest and specific.

Is a reverse mortgage right for you? A decision framework

The five conditions that usually need to be true

A reverse mortgage tends to work well when most of these apply:

- You own your home outright (or have a small remaining mortgage that the drawdown can clear)

- You’re at least 60–65 and plan to stay in the home long-term

- You genuinely need the equity — a pension shortfall, aged-care costs, or a modification you can’t otherwise fund

- Your family understands and accepts the estate implications

- You’ve compared it to HEAS and downsizing, and those don’t fit your circumstances

If you’re leaning toward a reverse mortgage but fewer than three of these apply, the product may be solving the wrong problem.

Conversations to have with your family before signing

Adult children’s expectations about inheritance can create real friction after the fact. Having the conversation before, with the actual dollar projections from a broker, is far better than the estate discovering a $1 million loan balance later.

Independent legal and financial advice (statutory requirement)

The National Credit Code (as amended in 2012) requires independent legal advice before you enter into a reverse mortgage contract. Lenders cannot proceed without written evidence that you’ve completed this step. It is a statutory obligation, not a soft suggestion, and for good reason. The compounding structure is complex, and having a lawyer outside the transaction walk you through the numbers before you sign is time well spent.

How a mortgage broker helps with a reverse mortgage

We work with borrowers across some active lenders — Heartland & Household Capital — and we model multiple scenarios before recommending anything.

The value of using a broker here isn’t just rate comparison. It’s knowing which lender’s LVR schedule gives you the most capacity at your specific age, which drawdown structure fits your cash flow needs, and which loan conditions will cause problems down the track. We also run the HEAS numbers before putting any commercial product in front of you. If HEAS covers your situation at 3.95%, that’s the first conversation, not the last.

We work with borrowers in Western Sydney and Parramatta and nationally. For the full range of home loan and equity products we can access, speak to our team.

Book a free call with us or submit an online enquiry, and we’ll model the numbers for your property and age.

Frequently Asked Questions

How does a reverse mortgage work in Australia?

A reverse mortgage lets you borrow against your home equity without making monthly repayments. You receive funds as a lump sum, income stream, line of credit, or a combination. Interest compounds monthly and is added to your balance. The full balance is repaid when you sell, move into aged care, or pass away; you remain the homeowner throughout. All Australian reverse mortgages entered into from September 2012 carry a statutory no-negative-equity guarantee.

How much can a 70-year-old borrow on a reverse mortgage?

At age 70, Heartland Bank’s published schedule allows up to 30% of your property’s value. On a $1.4 million Sydney home, that’s up to $420,000. P&N Bank caps at 35% maximum regardless of age; Unity Bank caps at 40% or $400,000. A broker can compare what each active lender offers for your specific age, property, and drawdown needs.

Does a reverse mortgage affect the Age Pension?

Loan proceeds are not assessed as income. The assets test is the key interaction: the first $40,000 is exempt for up to 90 days. After that, unspent funds become assessable financial assets and may reduce your entitlement via the deeming rules. Speak to Services Australia’s Financial Information Service before drawing — the impact depends on your individual circumstances.

What is the biggest disadvantage of a reverse mortgage?

Compounding interest. At 8.79% per year, a $200,000 lump sum grows to approximately $480,000 after 10 years and $1.15 million after 20 years without a single repayment. That growth comes directly from your estate’s equity. The no-negative-equity guarantee protects you from owing more than the sale price, but the compounding effect is the number to understand before signing.

Which Australian banks still offer reverse mortgages in 2026?

Active lenders: Heartland Bank (market leader, 40%+ market share), Household Capital (from 7.79%), P&N Bank (Perth metro only; age 65+), and Unity Bank. All major banks have exited: Commonwealth Bank (January 2019), NAB (2018–19), and all Westpac-group brands — St George, Bank of Melbourne, BankSA — withdrew around July 2017. IMB Bank is no longer accepting new reverse mortgage applications.

What’s the difference between a reverse mortgage and the Home Equity Access Scheme?

A commercial reverse mortgage charges 8.75–8.79% per year. HEAS is a government loan at 3.95% — roughly half the rate. HEAS requires Age Pension age (67 for most Australians) and property ownership. The tradeoff: HEAS drawdowns are capped at 150% of the maximum pension rate, limiting accessible amounts. For modest regular income top-ups, HEAS is almost always cheaper. For large lump sums — aged-care bonds, major renovations — a commercial reverse mortgage is typically the only option.

Are reverse mortgage interest rates higher than standard home loans?

Yes, significantly. Commercial reverse mortgage rates are 8.75–8.79% per year in April 2026, against standard variable home loan rates averaging 6–7%. The higher rate reflects the lender’s risk from no monthly repayments and uncertain repayment timing. The government’s HEAS rate of 3.95% is much lower but comes with strict drawdown limits.

Can I lose my home with a reverse mortgage?

No, not from the loan balance exceeding the property’s value. The statutory no-negative-equity guarantee (in place since 2012, under the National Credit Code) means you or your estate will never be required to repay more than the property sells for. You can lose your home by breaching loan conditions — failing to maintain insurance, permanently vacating without notifying the lender, or renting without consent.

This article contains general information only and does not constitute financial advice. Your personal financial situation, objectives and needs have not been considered. Before acting on any information, you should consider its appropriateness to your circumstances. Speak to a qualified mortgage broker for advice tailored to your situation. Mortgage World Australia Pty Ltd is a credit representative (CR No. 396946) of Mortgage Specialists Pty Ltd (Australian Credit Licence No. 387025).

Reverse mortgage interest rates cited are based on published lender rates as at April 2026 and are subject to change. All worked examples are illustrative only and based on a constant rate and 3% annual property growth.

Patrick is a Director and a Home Loan Specialist. He has been helping Australians with home loans since 2001. Prior to working as a mortgage broker Patrick was employed by Macquarie Bank for 3 years and also worked as an accountant for a publicly listed company. Patrick’s qualifications include:

Bachelor of Business, UTS Sydney. Majored in accounting and sub-majored in Finance and Marketing.

Diploma of Finance and Mortgage Broking Management FNS50310

Certificate IV in Financial Services (Finance/Mortgage Broking) FNS40804

Ready to Take the Next Step?

Whether you’re looking to buy your first home, refinance, or explore investment opportunities, Mortgage World Australia is here to help.

Fill out the contact form below, and one of our expert mortgage brokers will be in touch shortly to discuss your needs and guide you through your options.

Get Started Today!