SMSF Property Loan Australia: 2026 Broker’s Guide to LRBAs

SMSF Property Loans in Australia: A Broker’s Guide to Limited Recourse Borrowing

On this page ▾

- What an SMSF Property Loan Actually Is (And Why It’s Structurally Different)

- Who Can Use One: Compliance Gates and the Sole-Purpose Test

- SMSF Property Loan Rates in 2026 (And Why They’re Higher Than a Standard Investor Loan)

- How Lenders Assess SMSF Loan Serviceability (The Underexplained Piece)

- Which Lenders Actually Do SMSF Loans in 2026

- Refinancing an Existing LRBA in the May 2026 Rate Cycle

- Deposit, Costs, and What the Fund Pays for Upfront

- How an SMSF Property Loan Broker Helps (And the BID Context)

- How to Apply: The 8-Step LRBA Application Path

- Tax outcomes inside the fund

- Frequently Asked Questions

Most SMSF loan articles tell you what an SMSF loan is. This one shows you what each lender does with your fund’s numbers, because the gap between two lenders on the same SMSF can be $200K to $400K of borrowing capacity. We see it every week.

One scope statement before we go further. Australian mortgage brokers can advise on the credit product (the SMSF property loan itself). Advice on whether using a self-managed super fund to buy property is appropriate for your retirement strategy is licensed financial product advice and sits with your licensed financial adviser. This article covers the credit side only.

This guide is written for the SMSF trustee actively researching whether to buy property in the fund, or the existing LRBA holder reviewing their loan as the May 2026 RBA cycle reshapes the rate environment. You already have or are setting up an SMSF, and you have an accountant. Here are three facts I discuss on this one page:

- The big four banks (CommBank, NAB, ANZ, Westpac) do not offer SMSF loans in 2026. New SMSF lending comes from a panel of nine specialist non-bank lenders plus Bank of Queensland.

- SMSF serviceability is calculated on fund cash flow, not personal income, and each lender’s liquidity rule and minimum-fund-balance test changes the answer.

- The May 2026 RBA cycle is opening refinance windows on LRBAs written through 2024 and 2025.

What an SMSF Property Loan Actually Is (And Why It’s Structurally Different)

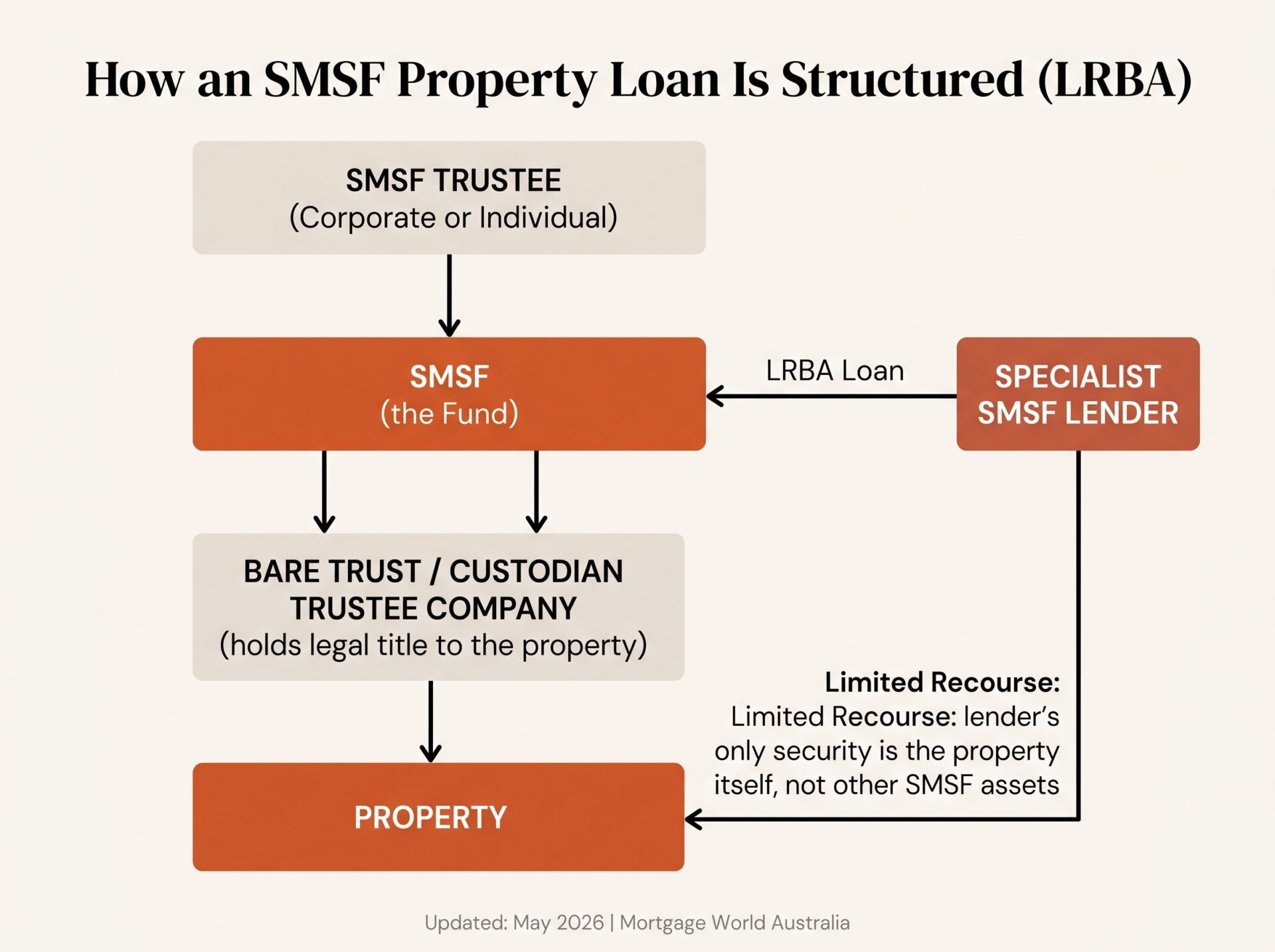

An SMSF property loan is a special-purpose mortgage that lets a self-managed super fund borrow money to buy a single property without putting the rest of the fund’s assets at risk if the loan defaults. The structure has a name and a section number: it’s a limited recourse borrowing arrangement, or LRBA, and it sits in section 67A of the Superannuation Industry (Supervision) Act 1993. Section 67 of the same Act prohibits SMSFs from borrowing in general; section 67A is the only carve-out that lets an SMSF take on debt for property.

This is not an investment property loan in the ordinary sense. It is structurally different from a standard investor loan in three ways: a separate trust holds the legal title to the property until the loan is paid out, the lender’s recourse is limited to the property itself rather than every asset in the fund, and the entire deal must comply with sections of the SIS Act that don’t apply to a personal investor mortgage.

The LRBA: What “Limited Recourse” Really Means for the Trustee

“Limited recourse” is the protective wrap around the deal. If the SMSF defaults on the loan, the lender can sell the property and keep the proceeds to clear the debt, but they cannot pursue the rest of the fund’s assets. The shares, the cash, the other property, all of it sits behind a wall. The single acquirable asset, in section 67A’s exact phrasing, is the only collateral on the table.

That protection cuts both ways. Specialist SMSF lenders price their products to reflect the absence of cross-collateralised security, which is why SMSF rates run roughly 30 to 100 basis points above standard investor rates at the same loan-to-value ratio. The fund, not you personally, bears that interest cost.

Bare Trust / Custodian Trustee, Who Arranges It and What It Costs

The bare trust (also called a holding trust or custodian trust) sits between the SMSF and the property. Its sole job is to hold the legal title to the asset until the LRBA is paid out, at which point title transfers to the SMSF trustee. The bare trustee should function passively: ideally, no separate ABN, no TFN, no bank account, no decisions of its own.

In practice, your accountant or SMSF lawyer arranges the bare trust deed alongside the loan application. Setup costs sit between $1,500 and $3,500 for the deed and corporate trustee company, plus stamp duty on the bare trust deed itself in some states (NSW charges a nominal $50 to $500, depending on structure). The deed wording matters because some lenders only accept their own template. We always confirm the lender’s deed requirements before the trust is settled, because redoing a deed after settlement is expensive and slow. For the broader sequence of steps to buying property with SMSF, the bare trust is step three of seven, not the last move.

Offset, Redraw, and Why SMSF Loans Trade Flexibility for Structure

A standard investor loan typically gives you a redraw facility. SMSF loans typically don’t. Under section 67A, the loan must fund “the acquisition of a single acquirable asset,” which most lenders interpret to mean principal is drawn at settlement and only paid down from there. La Trobe Financial’s SMSF product page explicitly states “Redraw Available: No”.

What several panel lenders now offer instead is a linked 100% offset account. The fund’s surplus cash, rental income, and pending contributions can sit in the offset and reduce monthly interest without paying down the principal. As of May 2026, two panel lenders publicly disclose 100% offset on their SMSF product:

- AMP Bank (SuperEdge Loan) offers an offset deposit account at no additional cost, on P&I and IO variants. AMP requires a corporate trustee.

- WLTH (Investment SMSF) offers an optional E-Offset Account on its variable-rate product, up to 90% LVR residential.

A handful of broker-distributed lenders, including Mortgage Ezy on certain product variants, offer offset features through accredited broker channels. We confirm offset availability product-by-product at quote time because lender policy moves quietly. For most trustees, the offset workaround is more useful than redraw would have been: cash stays inside the fund, the SMSF still controls it, and the interest saving is automatic.

Who Can Use One: Compliance Gates and the Sole-Purpose Test

Before any lender will touch an SMSF deal, three sections of the SIS Act have to line up.

Section 62, the sole-purpose test. Fund investments must be maintained for the sole purpose of providing retirement benefits to members. No fund member, and no relative of a fund member, can live in the residential property at any time, not even at peppercorn rent. The narrow exception is business real property (commercial premises used wholly and exclusively for a business), which can be leased to a related-party business at arm’s length market rates.

Section 67A, the LRBA carve-out, covered above. One bare trust, one asset, one loan. Multiple titles qualify as a single asset only where there’s a physical or legal impediment to dealing with them separately.

Section 71, the in-house assets rule (the “5% rule”). The SMSF can’t end up holding a related-party asset, loan, or lease that breaches the 5% cap once the LRBA is in place.

For the broader question of investing in property through SMSF, these three sections are the floor. If your accountant has walked you through them and your trust deed allows borrowing, the credit conversation can begin.

Single Acquirable Asset and the In-House Assets Rule

The single-acquirable-asset language has teeth. An SMSF can use one LRBA to buy one apartment, but not the apartment plus a parking space on a separate title (unless physically and legally inseparable). It cannot buy a duplex on one title and split it later, or fund renovations that change the character of the asset (section 67B, the replacement asset rule, blocks this).

The 5% in-house assets rule under section 71 caps investments in, loans to, and leases with related parties to 5% of total fund assets. For SMSF property:

- A residential LRBA property cannot be leased to a fund member or their relatives at any price. The sole-purpose test catches that before in-house assets do.

- Business real property used wholly and exclusively for a related-party business can be leased to that business at arm’s length market rent and is exempt from the 5% cap.

- The rule is a year-end test as well as a current-state test. If asset values shift the fund above 5%, you have until the end of the next financial year to bring it back below.

This is where the structure of your investment property ownership decision matters. Holding a property personally, in a trust, or in an SMSF produces very different tax and asset-protection outcomes, and the SMSF route is the most rule-bound.

SMSF Property Loan Rates in 2026 (And Why They’re Higher Than a Standard Investor Loan)

As of May 2026, the SMSF residential loan rate band sits at approximately 6.64% to 7.5% advertised variable, with comparison rates from roughly 6.7% to 7.9%. The lowest published rates on the panel come from Mortgage Ezy (from 6.64% variable on residential), La Trobe Financial (from 6.79%), Pepper Money, Bluestone and WLTH (each from 6.84%), and Liberty Financial (from 6.85% variable, 7.26% comparison). Specific rates depend on LVR, loan size, and whether the deal is residential or commercial.

The spread above standard investor rates reflects two things. First, the limited-recourse structure means the lender’s security is narrower, so they price for risk. Second, the SMSF lending market is concentrated in non-bank specialists and a small number of regional banks, which means less rate competition than the mainstream investor space. As a rough comparison, the standard investor variable rate sat around the low to mid 6% range in April 2026, so SMSF rates were running 30 to 100 basis points higher at like-for-like LVR.

The 2026 SMSF Rate Band vs Investor IO and P&I Rates

On a $500,000 SMSF loan, that 30 to 100 basis point spread is roughly $1,500 to $5,000 a year in extra interest, paid by the fund. Interest-only periods (commonly available up to 5 years on SMSF loans before reverting to P&I) reduce the fund’s monthly cash outflow, which matters because LRBA repayments must come from fund cash flow, not personal income. Most panel lenders allow IO up to 5 years; La Trobe and Pepper extend to 5 years and revert to P&I for the remaining loan term (commonly up to 30 years).

If you’re an existing LRBA holder weighing the rate environment, the question of whether to fix your home loan in 2026 plays out slightly differently for SMSFs because fund cash flow stability often matters more than rate optimisation, but the underlying logic on fixed versus variable still applies.

How Lenders Assess SMSF Loan Serviceability (The Underexplained Piece)

This is the centre of gravity for the article and the most misunderstood part of SMSF lending. SMSF serviceability is not your serviceability. It is the fund’s. The fund’s income, the fund’s expenses, and the fund’s buffer.

SMSF Income vs Personal Income, Why the Calculation Differs

A standard investor borrowing capacity calculation runs your salary, plus rental income at a haircut, minus living expenses, existing debt at stress rate, and HELP debt, multiplied through the lender’s net surplus formula. An SMSF calculation runs:

- The fund’s concessional contributions (employer 12% Super Guarantee plus any salary sacrifice up to the $30,000 FY 2025-26 cap)

- The fund’s investment income (rental from the LRBA property, dividends, interest)

- Expected rental income on the new property at a haircut (commonly 70% to 80% of gross rent)

- Less the loan repayments at stress rate (usually 1% to 3% above the actual rate, depending on lender)

- Less fund operating costs (audit, accounting, ASIC, insurance)

- Less the minimum pension drawdown if any member is in pension phase

The net result has to be positive, with a margin most lenders set at 1.05x to 1.15x of repayments. The trustee’s personal income is not in this calculation at all, which is why a high-income earner with a modest SMSF and a low-income earner with a well-funded SMSF can get very different answers from the same lender.

Liquidity Tests and Minimum-Fund-Balance Rules Each Lender Adds

On top of serviceability, some lenders layer a liquidity or minimum-balance rule. These are the levers that move borrowing capacity by $200K to $400K between lenders on the same fund. Some examples drawn from current panel policy as of May 2026:

- Pepper Money requires a minimum of $150,000 net SMSF assets at application.

- Bluestone publishes a $200,000 minimum net SMSF assets pre-purchase, but explicitly states “no minimum SMSF liquidity requirement” beyond that, which is unusual and is a Bluestone differentiator.

- AMP Bank requires a corporate trustee structure, which excludes funds running individual trustees unless they convert before application.

- La Trobe Financial deems contributions at 3.9% and shades rental income to 80% gross.

- Liberty Financial does not publicly disclose a minimum fund balance but applies a fund cash-flow buffer that adapts to the deal structure.

Beyond the public lines, every lender has internal policies on post-settlement liquidity (commonly 6 to 12 months of repayments held in cash inside the fund), member age (some lenders restrict LRBAs that would mature beyond age 75), and deed wording (the SMSF trust deed must permit borrowing, and the bare trust deed must match the lender’s template).

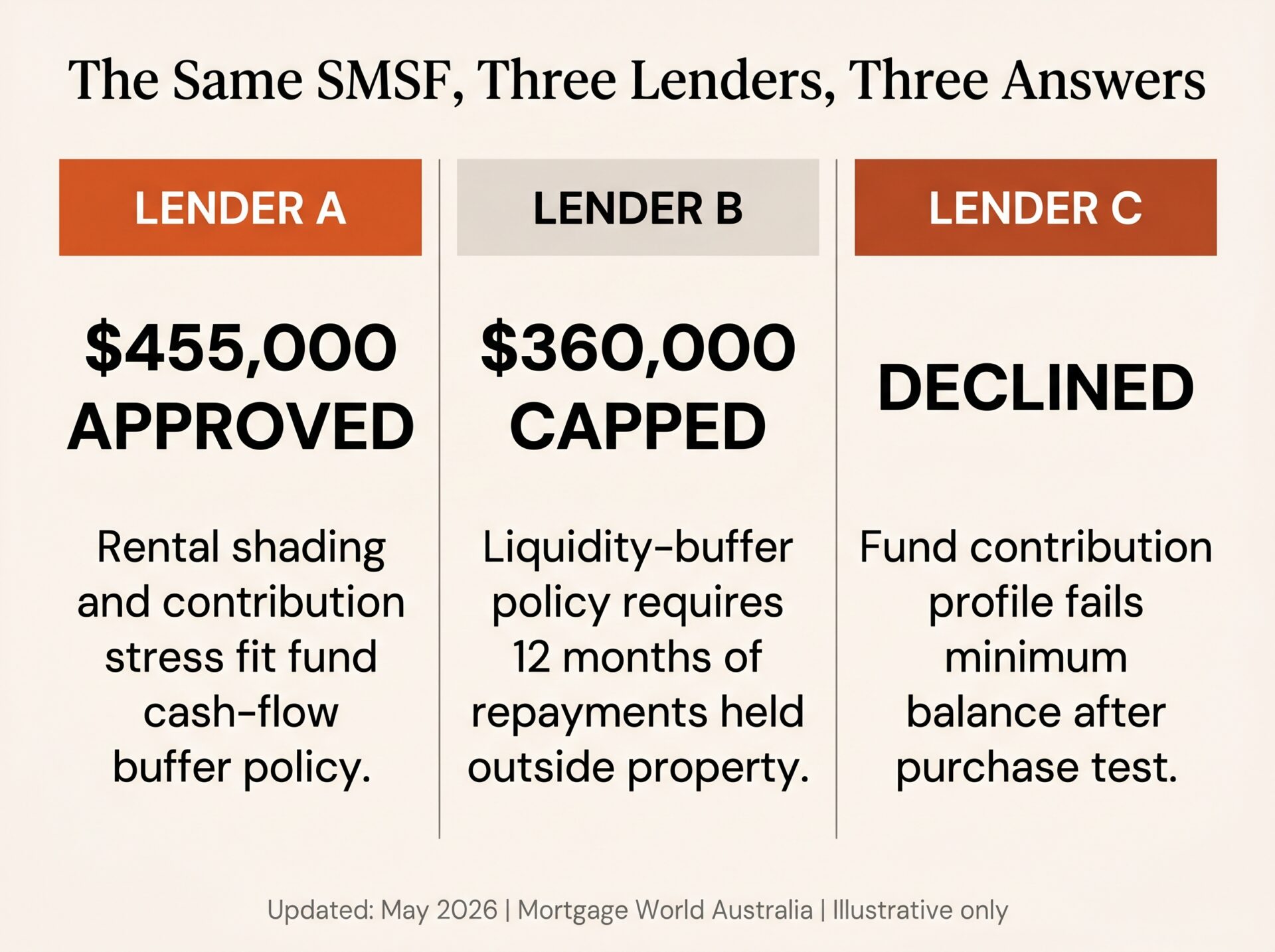

Worked Example: Same Fund, Three Lenders, Three Answers

Take the Smith Family SMSF. $400,000 fund balance, 30% in growth assets. Two members, ages 47 and 49, both employed with $30,000 in combined annual employer concessional contributions. Looking at a $700,000 residential investment property at 65% LVR (a $455,000 loan).

Lender A: Approves $455,000. Lender A’s residential SMSF product accommodates up to 90% LVR (so 65% is comfortably inside the cap). Their fund cash-flow buffer test fits the Smith fund’s contribution and rental profile, and the deal lands inside the standard policy lane.

Lender B: Caps the loan at approximately $360,000. Lender B’s $150,000 minimum fund balance is met, but their internal liquidity-buffer policy (understood at May 2026 to require approximately 12 months of repayments held outside the property) tightens the maximum loan once the fund’s likely post-settlement cash position is calculated. The Smith fund could revisit at a higher LVR once contributions build the fund balance over the next financial year.

Lender C: Declines as currently structured. Lender C’s minimum-balance-after-purchase test (10% to 15% of loan held post-settlement) is failed by the Smith fund’s contribution profile, even though the LVR and rental yield are otherwise acceptable. The deal could revive with a smaller property, a higher deposit, or a lump-sum non-concessional contribution to lift the fund balance.

Same fund, same property, same LVR. Three different policy lanes, three different answers, an approval-to-decline spread of $455,000 to nil. The numbers and policies above are illustrative as of May 2026, and current lender positions must be confirmed at application time. This is the gap a broker closes.

Which Lenders Actually Do SMSF Loans in 2026

Why the Big Four Banks Don’t Do SMSF Loans (And What That Means for Borrowers)

CommBank, NAB, ANZ, and Westpac. None of them offers SMSF home loans on their consumer-facing pages as of May 2026. NAB’s Super Lever was the most visible big-four SMSF product and has been wound back; the only SMSF reference on the NAB site now sits in the investments platform menu, which is for SMSF investing rather than lending. CommBank, ANZ, and Westpac show no SMSF or LRBA product at all.

SMSF loans are a niche, low-volume, high-compliance product. The credit policy work, trust-deed scrutiny, audit trail, and regulatory exposure don’t justify the volume for institutions writing tens of billions in mainstream investor loans. The big four exited the market quietly between 2018 and 2023, and have not signalled a return.

For borrowers, the practical effect is that no walk-in branch experience exists for SMSF lending. New SMSF loans flow through a panel of specialist non-bank lenders plus one regional bank. Bank of Queensland is the only mainstream bank in the Google top-10 organic results for “SMSF property loan” in 2026 (currently #3) and treats SMSF as a business term loan to 80% LVR where the fund runs a corporate trustee.

Macquarie Bank exited promoted SMSF home lending around 2018 and does not actively market SMSF loans through retail channels in 2026. Existing back-book customers retain their loans; new lending sits with the specialist panel.

The Specialist and Non-Bank Panel: Mortgage Ezy, Firstmac, Liberty, La Trobe, Pepper Money, Bluestone, WLTH, Resimac, AMP

These are the nine specialist lenders we place SMSF clients with. Each one occupies a different policy lane:

- Mortgage Ezy (broker-distributed). SMSF Lender of the Year 2023 at the SMSF Adviser Awards. Strong on alt-doc and trustee-company structures. Specific rate and LVR available via accredited broker channels.

- Firstmac. SMSF Home Loan to 80% LVR, $50K to $2M loan range, $0 ongoing fees, no application or settlement fee on refinances. A clean, low-fee proposition for vanilla LRBAs.

- Liberty Financial. Residential SMSF to 90% LVR, commercial to 80%. $10M residential / $4M commercial maximum loan amounts. The most rate-transparent of the panel.

- La Trobe Financial. Residential SMSF to 80% LVR. $100K minimum loan, up to 30-year term, 5-year IO. Application fee from 1.25%. No offset, no redraw.

- Pepper Money. Residential SMSF to 90% on purchase, 80% on refinance. $150K minimum net SMSF assets at application. Full-doc and alt-doc product variants.

- Bluestone. Residential and commercial SMSF to 80% LVR. $200K minimum net SMSF assets pre-purchase. Up to six SMSF members on a single deal. “No minimum SMSF liquidity requirement,” which is unusual on the panel.

- WLTH (Investment SMSF). Residential SMSF to 90% LVR. Optional 100% offset account. One of two panel lenders publicly offering offset on SMSF.

- Resimac. Currently active in SMSF lending per broker-channel listings. Specific rate and LVR available via accredited broker channels.

- AMP Bank (SuperEdge Loan). Returned to SMSF lending in Q1 2026. Residential SMSF to 80% LVR (zone-based, with high-density zones lower). $200,000 minimum loan amount. Corporate trustee only. 100% linked offset account at no additional cost. The other of the two panel lenders publicly offering offset.

For borrowers searching for “Macquarie Bank SMSF loan” or “BOQ SMSF loan,” the panel above is what’s actually available. Macquarie is functionally absent for new lending. BOQ remains a viable option for residential and commercial SMSF deals where the fund runs a corporate trustee. BOQ aims their products at applicants who work in the medical field.

What Each Lender’s LRBA Looks Like at a Glance (LVR, Min Fund Balance, Rate Band)

The summary above is the at-a-glance version. The interaction effects, where the deal structure favours one lender’s policy lane over another, are what change borrowing capacity by hundreds of thousands of dollars. We confirm the current rate sheet, LVR caps, and policy positions on every deal at quote time.

Refinancing an Existing LRBA in the May 2026 Rate Cycle

LRBAs written through 2024 and 2025 are sitting on rates between 7.5% and 8.5%. The May 2026 RBA cycle has begun pulling those down. We’re seeing 50 to 100 basis points of refinance savings on LRBAs placed two and three years ago, paid back to the SMSF as cash flow.

The mechanics are straightforward, but the documentation is heavier than a standard refinance. The new lender takes the same single acquirable asset on new terms, the bare trust stays in place (most lenders accept the existing deed if it matches their template), and lender-to-lender stamp duty is usually avoided because legal title doesn’t move out of the bare trustee company. ATO PCG 2016/5 (the related-party LRBA safe harbour) only applies if the original loan was related-party; commercial-lender refinances don’t trigger it. The general principles of refinancing a home loan carry over (break costs, valuation timing, application fees), but the fund-cash-flow servicing test runs again from scratch, and the bare trust deed wording is re-checked against the new lender’s template.

Why Most SMSF Loans Never Get Refinanced (And What That Costs)

Compliance overhead is the reason. Trustees without a broker assume the refinance is too complex, the bare trust will need redoing, the audit will throw up issues, and they leave 50 to 100 basis points on the table. On a $500,000 SMSF loan, that’s $2,500 to $5,000 a year forgone by the fund, every year. Across a typical 20-year LRBA term, the leakage runs into six figures.

The overhead is not zero, but it’s not what the fear suggests. We refinance LRBAs every quarter. The bare trust stays where it is, legal title doesn’t move, and the audit picks up cleanly because the structure hasn’t changed.

Deposit, Costs, and What the Fund Pays for Upfront

The minimum deposit on a residential SMSF loan sits at 20% to 30% of the property price (70% to 80% LVR). Liberty, Pepper, and WLTH will go to 90% LVR on residential at higher rates and tighter policy. Commercial SMSF deals usually cap at 70% to 75% LVR.

The fund pays upfront for, at a minimum:

- The deposit (20% to 30% of property price)

- A post-settlement liquidity buffer (commonly 10% to 15% of the loan amount, held as fund cash)

- Stamp duty on the purchase. NSW transfer duty figures are based on rates effective 1 July 2025, sourced from Revenue NSW. There is no general SMSF concession; SMSF transfers attract standard transfer duty unless a narrow concession applies (section 62A of the Duties Act 1997 (NSW) covers a small set of member-to-fund transfers). For the broader picture of land tax in NSW on SMSF holdings, the fund is treated as a separate landowner.

- Bare trust deed and corporate trustee setup ($1,500 to $3,500)

- Conveyancing and legal review of trust deeds ($1,500 to $3,000)

- Lender application or establishment fees (La Trobe from 1.25% of the loan amount; Firstmac waives most fees on refinance)

The cash all comes from the SMSF. None can be lent in by a member or relative outside the related-party loan rules under PCG 2016/5, which has its own pricing and term safe-harbour conditions. We run the deposit-plus-buffer numbers before any property is named, because that combination is the practical floor on whether a deal is even viable.

How an SMSF Property Loan Broker Helps (And the BID Context)

Under the National Consumer Credit Protection Act and the ASIC Best Interests Duty, a broker’s job on an SMSF deal is to structure the credit to fit the fund’s profile and the trustee’s stated objectives. We compare lender policy across the panel, model the serviceability and liquidity tests against each lender’s rules, structure the application for the best chance of approval, and manage the back-and-forth between the lender, the bare trust drafter, and the SMSF accountant.

To repeat the scope: brokers advise on the credit product. Advice on whether using an SMSF to buy property suits your retirement strategy is licensed financial product advice and sits with your adviser. We work with the adviser on the fund-strategy side; we own the credit conversation.

The deal-volume edge matters. Brokers see policy movement across lenders that no individual borrower or generalist banker sees. Which lender approved 90% LVR last week? Which tightened its liquidity rule this quarter? Which changed its bare-trust deed template? The patterns drive better outcomes than any one lender’s product page.

What a Generalist Banker Can’t Do for an SMSF Deal

A branch home loan officer typically writes one or two SMSF deals a year, if any, and leans on a documented procedure for a product the bank may not even offer (for the big four, the answer is zero). They cannot quote across nine specialist lenders, read a bare trust deed against multiple lender templates, or tell you that the fund’s contribution profile fails Lender C’s minimum-balance test before you spend $2,500 on a deed that has to be redone. A specialist SMSF broker writes SMSF deals every month. The pattern recognition is the value.

How to Apply: The 8-Step LRBA Application Path

The path from “I want to buy property in my SMSF” to settlement runs through eight stages. We map the timeline at the start of every engagement:

- Strategy sign-off with your licensed financial adviser. Decide whether SMSF property is the right strategy for the fund. This is the adviser’s call, not the broker’s.

- Trust deed review. Your SMSF trust deed must permit borrowing. If it doesn’t, your accountant or SMSF lawyer amends the deed before the lender will engage.

- Bare trust setup. The bare trust is created with a corporate trustee, and the deed is drafted against the chosen lender’s template (or kept generic until the lender is selected).

- Pre-approval with the lender. We submit the SMSF financials, fund balance, contribution history, member ages, and indicative property profile to the chosen lender. Pre-approval gives the trustee a firm number to shop with.

- Property selection. With pre-approval in hand, the trustee chooses the property. The bare trust holds the contract; the SMSF trustee signs as the controller of the bare trustee company.

- Valuation and unconditional approval. The bank’s valuation confirms the lender’s LVR. Unconditional approval follows.

- Settlement. The lender funds the loan, the fund pays the deposit and stamp duty, and legal title vests in the bare trustee company until the LRBA is paid out.

- Ongoing compliance. Annual SMSF audit, annual lodgement, ongoing trustee oversight of the property’s lease, condition, and rental income. The audit picks up the LRBA structure every year.

The full path takes 8 to 14 weeks for a clean deal, longer where the trust deed needs amendment or where the fund needs a contribution top-up to clear the lender’s minimum-balance test.

Tax outcomes inside the fund

The tax side is where SMSF property differs most from personally held investment property. Concessional contributions (employer 12% SG plus salary sacrifice, up to the $30,000 FY 2025-26 cap) are taxed at 15% in the fund. Non-concessional contributions sit under a separate $120,000 cap. Investment income (rental, dividends, interest) is taxed at 15% in accumulation and 0% on income supporting a pension. Capital gains on assets held over 12 months get a one-third discount, producing an effective 10% CGT rate in accumulation. None of that resembles negative gearing for a personally held investor: an SMSF can report a tax loss on the property, but the loss only offsets fund income, not the trustee’s personal income. The investment property capital gains tax interaction is also different: an SMSF that sells in pension phase pays 0% CGT, which is the structural advantage of holding property to retirement inside the fund.

Frequently Asked Questions

Can an SMSF borrow to buy property?

Yes, but only through a limited recourse borrowing arrangement (LRBA), the carve-out set out in section 67A of the Superannuation Industry (Supervision) Act 1993. The fund can borrow to acquire a single acquirable asset, the loan is held in a separate bare trust until the debt is paid out, and the lender’s recourse is limited to the asset itself. The big four banks do not offer LRBA products in 2026; new SMSF loans come from a panel of specialist non-bank lenders plus Bank of Queensland.

Which banks do SMSF home loans in 2026?

None of the big four (CommBank, NAB, ANZ, Westpac) currently offer SMSF home loans on their consumer-facing pages, verified May 2026. NAB’s Super Lever product has been wound back. Bank of Queensland is the only mainstream bank actively writing SMSF loans. The supply for new SMSF lending sits with a specialist non-bank panel: Mortgage Ezy, Firstmac, Liberty Financial, La Trobe Financial, Pepper Money, Bluestone, WLTH, Resimac, and AMP Bank (which returned to SMSF lending in Q1 2026 after a multi-year withdrawal).

What is the minimum deposit for an SMSF loan?

Typically, 20% to 30% of the property price plus a fund liquidity reserve. Most SMSF lenders cap the loan-to-value ratio at 80% for residential and 70% to 75% for commercial. A few panel lenders, including Liberty, Pepper Money and WLTH, will go to 90% LVR on residential SMSF deals at higher rates. On top of the deposit, lenders expect the fund to keep a liquidity buffer (often 10% to 15% of the loan amount) in cash or equivalents after settlement. Stamp duty, legal fees and the bare trust setup come from fund cash, not the loan.

What is the 5% SMSF rule?

The 5% rule is the in-house assets rule under section 71 of the SIS Act, which limits an SMSF’s investments in, loans to, and leases with related parties to 5% of total fund assets. It is not the same as the 5% deposit scheme that applies to first home buyers. The rule matters for SMSF property because a fund cannot lease the residential property back to a member or their relatives at any price. Business real property is treated differently and can be leased to a related-party business at arm’s length terms, which is one of the few related-party exemptions.

Can an SMSF refinance a property loan?

Yes, an SMSF can refinance an existing LRBA, and in the May 2026 rate cycle, refinancing is one of the highest-value reviews a fund can run. The refinance must comply with ATO PCG 2016/5 (the safe harbour for related-party LRBAs) if the original loan was internal, and with section 67A more broadly. In practice, the fund refinances the same single acquirable asset on new terms with a new lender, the bare trust stays in place, and lender-to-lender stamp duty is generally avoided because the underlying legal title doesn’t move. We’re seeing 50 to 100 basis point savings on LRBAs written before the 2024-2025 hike cycle.

If you’d like to talk through the credit side of an SMSF property purchase or review an existing LRBA, MWA places SMSF clients with the nine-lender specialist panel covered above. The fund-strategy side stays with your licensed financial adviser. Patrick has been writing SMSF property loans across the panel for more than a decade and tracks the policy movements that change borrowing capacity by hundreds of thousands of dollars on the same fund. For the broader cluster, the SMSF home loans page gives a short overview of MWA’s SMSF service.

This article contains general information only and does not constitute financial advice. Your personal financial situation, objectives and needs have not been considered. Before acting on any information, you should consider its appropriateness to your circumstances. Speak to a qualified mortgage broker for advice tailored to your situation. Mortgage World Australia Pty Ltd is a credit representative (CR No. 396946) of Mortgage Specialists Pty Ltd (Australian Credit Licence No. 387025).

Patrick O’Brien, Director and Mortgage Broker since 2001.

Patrick is a Director and a Home Loan Specialist. He has been helping Australians with home loans since 2001. Prior to working as a mortgage broker Patrick was employed by Macquarie Bank for 3 years and also worked as an accountant for a publicly listed company. Patrick’s qualifications include:

Bachelor of Business, UTS Sydney. Majored in accounting and sub-majored in Finance and Marketing.

Diploma of Finance and Mortgage Broking Management FNS50310

Certificate IV in Financial Services (Finance/Mortgage Broking) FNS40804

Ready to Take the Next Step?

Whether you’re looking to buy your first home, refinance, or explore investment opportunities, Mortgage World Australia is here to help.

Fill out the contact form below, and one of our expert mortgage brokers will be in touch shortly to discuss your needs and guide you through your options.

Get Started Today!