Should I Fix My Home Loan in 2026?

Should I fix my home loan in 2026? A mortgage broker’s view after the May RBA hike

On this page ▾

- What the May 2026 RBA hike actually means for borrowers

- How to read lender fixed-rate movements as an RBA signal

- Fixed vs variable in a hiking cycle: when each wins

- Split loans: the hedge most borrowers don’t ask about

- Break costs: the trap if you fix and then need out

- Which borrower profiles should fix now – and which shouldn’t

- Rate lock: a 90-day insurance policy worth knowing about

- What to do this week if you’re worried

- Frequently asked questions

The RBA raised the cash rate to 4.35% on 5 May 2026. That’s the third hike this year, and it brings rates back to exactly where they were in late 2023.

What makes this moment unusual isn’t the rate itself. It’s the journey. The RBA cut three times in 2025, taking the cash rate down to 3.60%, before inflation picked back up in the second half of 2025 and forced a reversal. Three hikes later, we’re back to 4.35%.

If you were on a variable rate through all of that, you’ve had a rough ride. And if you’re now asking whether to fix, you’re asking the right question.

Here’s my honest take after working through five rate cycles since 2001: this is one of the more interesting moments I’ve seen for the fix-or-stay decision. Short-term fixed rates at the major banks are currently sitting very close to, or below, what most borrowers are actually paying on a packaged variable rate. That’s not typical. It means you can buy certainty today without paying a premium for it.

This article gives you a framework. I’ll show you the current numbers, explain what they signal about the RBA’s path, walk through split loans and break costs, and tell you which borrower profiles I’d steer toward a fixed rate right now.

What the May 2026 RBA hike actually means for borrowers

The cash rate path: three hikes in 2026 and where the market sees it next

Here’s the full 2026 rate timeline:

| Date | Decision | New Rate |

|---|---|---|

| 3 February 2026 | +0.25% | 3.85% |

| 17 March 2026 | +0.25% | 4.10% |

| 5 May 2026 | +0.25% | 4.35% |

The March decision was close – a 5-4 split on the RBA Board. The May decision passed 8-1. So the hiking cycle has strengthened its footing, not weakened it.

Market pricing as of May 2026 implies roughly another 0.60% of increases before the cycle peaks, potentially reaching 4.70% by late 2026. Rate cuts? The RBA’s May 2026 Statement on Monetary Policy projects underlying inflation above 3% until mid-2027. Cuts are a 2027 story at the earliest.

What “rate cut expectations walked back” means in plain language

Twelve months ago, most forecasters had rate cuts locked in for 2025. Some happened. Three cuts took the cash rate to 3.60%. Then inflation picked back up, and everything changed.

For borrowers, this is important context: the rate environment has not simply been rising. It fell, then reversed hard. Anyone waiting for “rates to settle” before deciding to fix has been waiting through a cycle that has now turned twice. The decision point is here.

How to read lender fixed-rate movements as an RBA signal

Why fixed rates lead the variable rate

Variable rates track the RBA cash rate. When the RBA hikes 0.25%, your bank passes it on (usually within a few weeks).

Fixed rates work differently. Banks price them off the interest rate swap market – specifically off 1-year, 2-year, and 3-year swap rates that reflect where the market thinks rates will be, not where they are today.

This means fixed rates are a real-time market forecast. When 2-year fixed rates climb sharply, the swap market is pricing in more hikes. When 2-year fixed rates hold steady while the variable rate rises, the market is signalling the hiking cycle is close to its end.

When the gap between fixed and variable narrows or inverts – what it tells you

In a normal rate environment, fixed rates sit above variable rates. You pay a premium for certainty.

Right now, that premium has almost disappeared for short-term fixed rates.

Today’s snapshot: big four 1-, 2-, and 3-year fixed vs variable

Current rates as at 7 May 2026, owner-occupier principal and interest:

Variable rates

| Bank | Product | Rate | Comparison Rate |

|---|---|---|---|

| CommBank | Digi Home Loan | 5.84% | 5.97% |

| ANZ | Simplicity PLUS | 6.14% | 6.14% |

| Westpac | Flexi First Option | 6.14% | 6.51% |

| NAB | Base Variable | 6.19% | 6.19% |

| NAB | Tailored Variable | 6.54% | 6.63% |

1-year fixed rates

| Bank | Product | Rate | Comparison Rate |

|---|---|---|---|

| NAB | Tailored Fixed | 6.34% | 6.60% |

| ANZ | Fixed Rate | 6.34% | 6.93% |

| Westpac | Fixed Rate (pkg) | 6.39% | 6.54% |

| CommBank | MAV Package | 6.49% | 8.06% |

2-year fixed rates

| Bank | Product | Rate | Comparison Rate |

|---|---|---|---|

| Westpac | Fixed Rate (pkg) | 6.29% | 6.54% |

| CommBank | MAV Package | 6.34% | 7.89% |

| NAB | Tailored Fixed | 6.39% | 6.60% |

| ANZ | Fixed Rate | 6.39% | 6.87% |

3-year fixed rates

| Bank | Product | Rate | Comparison Rate |

|---|---|---|---|

| NAB | Tailored Fixed | 6.49% | 6.61% |

| Westpac | Fixed Rate (pkg) | 6.49% | 6.61% |

CBA and ANZ 3-year fixed rates were not competitively positioned at the time of writing – check directly with each lender for current offerings.

Rates verified 7 May 2026. Note: CBA announced a variable rate increase effective 15 May 2026.

Comparison rate based on a secured loan of $150,000 over 25 years. WARNING: This comparison rate applies only to the example or examples given. Different amounts and terms will result in different comparison rates. Costs such as redraw fees or early repayment fees, and cost savings such as fee waivers, are not included in the comparison rate but may influence the cost of the loan.

Two important caveats on the rates above

1. Fixed rates are based on a 70% LVR. If your LVR is above 70%, the fixed rates at Westpac and St.George, in particular, are higher than the table shows. Always confirm the rate that applies to your specific LVR with your broker or your lender.

2. Variable rates are negotiable. The variable rates in the table are the standard advertised rates. As a broker, I negotiate variable rates with the major banks directly. As at 7 May 2026 (before the May 0.25% hike has been fully passed through), the variable rates I’m currently securing for clients on a $500,000 loan at 70% LVR are:

| Bank | Negotiated package variable rate |

|---|---|

| Westpac | approx. 5.93% |

| ANZ | approx. 5.95% |

| CommBank | approx. 5.97% |

| NAB | approx. 6.03% |

All of these will rise by approximately 0.25% as the banks pass on the May 2026 hike. Even after that pass-through, fixed and well-negotiated variable rates are within 0.05%-0.30% of each other for short fixed terms.

What this means in practice: if you’re comparing fixed against your current advertised variable rate, the case for fixing looks straightforward – the premium for certainty has almost disappeared. If you’re comparing against a rate a broker can actually negotiate, the gap narrows but doesn’t reverse. Fixed for 1-2 years still removes the rate-rise risk for very little, if any, premium – but the case is strongest if you haven’t already had your variable rate sharpened.

Fixed vs variable in a hiking cycle: when each wins

The case for fixing now

The strongest arguments for fixing right now:

- You know your repayments for 1-3 years. No budget recalculations after each RBA meeting.

- Short-term fixed rates are roughly equal to or below what most borrowers are paying on variable. You’re not paying a premium for certainty.

- The market is pricing in at least one more hike. If that happens, variable rates go up again. Your fixed rate stays put.

- Mortgage stress is real. If rate uncertainty is affecting your household, fixing buys peace of mind – and at current pricing, you’re not giving anything up to get it.

The case for staying variable

The argument against fixing is legitimate, too:

- Fixed rates lock you in. If you need to sell, refinance, or make large extra repayments, you could face break costs.

- The hiking cycle may be close to its end. If rates peak at 4.35%-4.70% and the RBA starts cutting in 2027, locking in now means you miss the first round of cuts.

- Extra repayment caps are real. Most lenders limit extra repayments on fixed loans to $10,000-$30,000 per year. If you’re aggressively paying down principal, a variable rate with an offset account gives more room.

- 100% offset accounts generally aren’t available on fixed loans. Most lenders restrict offset to variable products. Of the big four, ANZ is the only one that offers a 100% offset on a 1-year fixed term. A few smaller lenders allow it too. If you’ve been using your offset balance to bring down the interest you pay, switching to fixed will end that benefit on the fixed portion, which is one more reason a split structure is often the right answer.

Three rate scenarios: what happens to your repayments on a $600,000 loan

Here’s what the next 12-18 months could look like on a $600,000, 30-year principal and interest loan. Using NAB’s Base Variable (6.19%) as the reference:

| Scenario | Rate | Monthly repayment | Annual repayment |

|---|---|---|---|

| Current variable | 6.19% | $3,671 | $44,052 |

| One more hike (+0.25%) | 6.44% | $3,769 | $45,228 |

| Two more hikes (+0.50%) | 6.69% | $3,868 | $46,416 |

| Three more hikes (+0.75%) | 6.94% | $3,968 | $47,616 |

Each 0.25% hike adds roughly $98 per month on a $600,000 loan. If the market’s 0.60% forecast is right, that’s approximately $235 per month more than today by the time the cycle peaks. That’s real money. To see what each rate scenario does to your own repayment, see your repayments at each rate.

Run the numbers on your repayments with your actual balance – the calculator on our site handles different loan sizes and terms.

For a deeper comparison of fixed and variable loan structures, read the long-form fixed vs variable comparison.

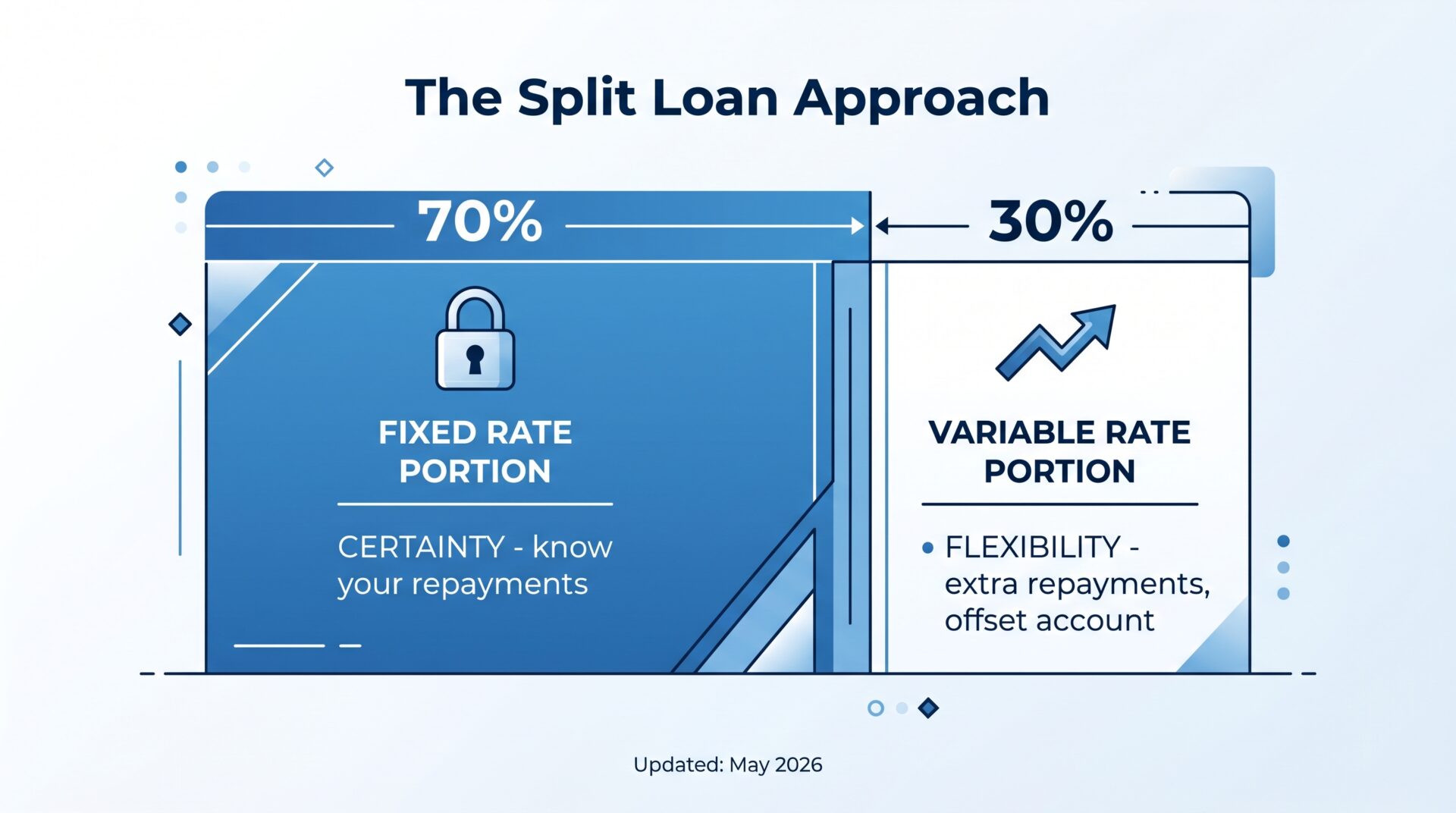

Split loans: the hedge most borrowers don’t ask about

How a split loan works in practice

A split loan divides your mortgage into two portions: one on a fixed rate, one on a variable rate. You pay a different rate on each portion, and they’re typically held with the same lender under one account structure.

Most borrowers think of it as a 50/50 compromise. It doesn’t have to be. Done right, a split loan lets you lock in certainty on the portion of your mortgage where rate rises hurt the most, while keeping flexibility on a smaller portion for extra repayments and offset savings.

Choosing the ratio: 50/50 vs 70/30 vs 30/70

The right split depends on your answers to two questions:

How much income buffer do you have if rates rise another 0.50%?

If the answer is “it would hurt but not break us,” lean toward a higher fixed proportion. If the answer is “we’d genuinely struggle,” fixing a larger share reduces your exposure.

Are you likely to sell, refinance, or make large lump-sum repayments in the next 2-3 years?

If yes, keep the fixed portion smaller (30-40%) to limit break cost exposure. If no, a 60-70% fixed split is worth considering.

A practical example: a borrower with a $600,000 loan who wants to pay down $40,000 over two years might do better with a 70/30 split (70% fixed at 6.34%, 30% variable with offset). The fixed portion protects $420,000 of repayments from rate rises. The variable portion on $180,000 with an offset account lets them park savings, earn interest credit, and avoid the extra repayment cap on the fixed side.

Which lenders allow flexible split structures

Most major banks and many second-tier lenders allow splits. Key questions before you decide:

- What is the minimum on each portion? (Some lenders require $50,000 minimum per split.)

- Can you have more than two splits? (Some allow three-way splits.)

- What is the extra repayment cap on the fixed portion?

Structures vary significantly between lenders. This is one of the areas where access to 52+ lenders produces real differences in outcomes – not all lenders offer the same split flexibility, and the right structure depends on your loan size and repayment plan.

Break costs: the trap if you fix and then need out

How break costs are actually calculated

When you break a fixed loan early, the lender can charge you for their lost revenue. The formula is based on the Bank Bill Swap Rate (BBSW) – the benchmark Australian banks use when pricing fixed products:

Break cost = (BBSW at origination minus BBSW at break) x remaining years x current balance

If the BBSW has risen since you fixed, the difference is zero or close to zero – the lender can re-lend your money at a higher rate, so there’s no loss to compensate.

If the BBSW has fallen since you fixed, that difference becomes a real cost.

Worked example: fixing today, rates later fall

Say you fix $500,000 at NAB’s 3-year rate (6.49%) today. One year in, the RBA begins cutting and the relevant swap rate has fallen by 1.25%. Two years remain on your fixed term.

Rough break cost estimate:

1.25% x 2 years remaining x $500,000 = $12,500

That’s illustrative. The actual calculation uses the precise BBSW figures at both dates, which only the lender can provide. The principle is what matters: the break cost is real, it can be material, and it’s hard to forecast.

Here’s the flip side for context: anyone who fixed at 3.00%-3.50% in early 2025 (during the cut cycle) and wants to break out now is likely facing zero or near-zero break costs. The RBA has hiked back to 4.35%, wholesale rates have risen, and the lender can re-lend at higher rates. Their gain from releasing you early is zero.

When break costs are low vs significant

Break costs are low (or zero) when:

– Rates have risen since you fixed (the 2026 reality for early-2025 fixers)

– Minimal time remains on your fixed term

– Your loan balance is smaller

Break costs are high when:

– Rates have fallen materially since you fixed

– Multiple years remain on the term

– Your balance is large

The practical rule: never fix for longer than your certainty horizon. If there’s any real chance you’ll sell in 12 months, fix for 1 year at most – or don’t fix that portion at all.

Which borrower profiles should fix now – and which shouldn’t

I’ve worked with clients through the 2008 financial crisis, the COVID rate crash to 0.10%, the 2022-2023 hiking cycle, the 2025 cuts, and now the 2026 reversal. Here’s my honest view on who should consider fixing in the current environment.

First home buyers in the first 12 months of repayments

If you’ve recently bought and are on a variable rate, the early years of ownership are the most budget-sensitive. You don’t yet have the equity buffer or the income growth that makes rate rises more manageable later. A 1 or 2 year fixed term at current rates gives you time to stabilise your cash flow before returning to a variable rate.

Investors with positively geared property and a 5-year horizon

If your rental income already covers the mortgage and you’re planning to hold for 5+ years, fixing reduces interest rate risk from your serviceability calculations. This matters for portfolio growth. Lenders assess investment loans against a stress rate, and a fixed rate locks in the contractual rate used for that assessment during the fixed term, which can improve your borrowing capacity for the next purchase.

Households planning to sell or upsize within 18 months

For this profile, my advice runs the other way: don’t fix, or fix only a small portion. Break costs when selling can eliminate any interest savings. If you have real certainty around a sale timeline, stay variable or use a short 1-year fix on part of the loan.

Self-employed borrowers with variable income

If your income fluctuates and you can’t predict your cash position 2-3 years out, a fixed rate gives you a fixed liability. This is particularly relevant when variable rates could still move up another 0.50% or more. The certainty value of a fixed payment is higher when your income isn’t certain.

People who broke a fixed loan in 2023 and are reluctant to fix again

This is a real pattern. In 2023, many borrowers broke their COVID-era fixed loans (set at 1.89%-2.29%) because they wanted flexibility – and many paid significant break costs to do it. The experience left a lasting reluctance to fix again.

The circumstances are different now. You’d be fixing near a potential rate peak, not near a rate floor. The mathematical case for fixing in 2026 is genuinely different from the case in 2021. The previous experience is worth acknowledging, but it shouldn’t override a fresh analysis.

Rate lock: a 90-day insurance policy worth knowing about

What rate lock is and what it costs

When you apply for a fixed rate loan, there’s often a gap between approval and settlement – particularly on new builds or off-the-plan purchases. The rate at settlement may be higher than the rate you were quoted at application.

Rate lock lets you reserve the rate quoted at application for a defined period, typically 90 days.

Rate lock costs at the big four:

– NAB: 0.15% of the approved loan amount, non-refundable. On a $600,000 loan, that’s $900. 90-day window.

– CBA: Flat fee of $750. 90-day window.

– Westpac: 0.10% of the fixed rate loan amount. On a $600,000 loan, that’s $600. 90-day window.

– ANZ: $750 per $1 million in lending (or part thereof). A $400,000 loan = $750. A $1.3 million loan = $1,500. Payable at application; rate held for up to 90 days.

When it’s worth paying for

Rate lock earns its cost when:

– Settlement is more than 30 days away

– Rates are in a clear upward trend

– The fee is small relative to the rate risk

A 0.25% hike on a $600,000 loan adds $98 per month to repayments. Rate lock costs $600-$900 across the big four for a typical loan. If the RBA hikes again before your settlement date, rate lock pays for itself in the first 6-10 months.

My current view in this market

For any client I’m helping fix a rate right now, particularly for 2 years or longer, I’m strongly recommending rate lock.

In a rising rate cycle, fixed rates can change at any time, sometimes between application and settlement. The cost of being wrong without rate lock – a 0.15-0.25% rate increase carried over the entire fixed term – is several times the lock fee. With the RBA still in hiking mode and lenders re-pricing fixed rates between meetings, the risk of a settlement-time rate change is real, not theoretical.

If you’re applying for a fixed rate loan in May or June 2026 and your settlement is more than two weeks out, the math on rate lock is straightforward.

What to do this week if you’re worried

A 4-step rate-review checklist

- Find your current rate. Check your most recent mortgage statement or log into your lender’s app. You need both the advertised rate and any package discount applied.

- Compare it against today’s fixed rates. The table earlier in this article is a starting point. Then call your existing lender and ask what fixed rates they can offer on your current loan.

- Request a break cost quote if you’re already on fixed. If you’re mid-way through a fixed term, your lender can tell you what it would cost to exit today. Get the number in writing.

- Talk to a broker. Your lender will only show you their own products. A broker with access to the full market can find the best structure for your situation – not just the best rate on one shelf.

Why working with a broker beats calling your bank in this market

When you call your bank about fixing, they’ll compare their own products. The comparison stops at their own product shelf.

A mortgage broker works under the Best Interests Duty (BID, effective 1 January 2021), which legally requires us to act in your best interest, not the lender’s. That’s not marketing language – it’s a legal obligation introduced after the Banking Royal Commission.

At MWA, our 52-lender panel includes banks, non-banks, and credit unions. In a market where rates between lenders vary by 0.50%-1.00% on comparable products, that breadth produces meaningfully different outcomes.

Read more about Patrick and our approach to understand how we work. Or skip straight to a conversation.

Book a free 15-minute rate review – no obligation, no sales pitch. We’ll look at your current rate, your loan structure, and whether fixing makes sense for your situation right now.

If you’re also evaluating a lender switch alongside the fix question, refinancing to a sharper rate may be worth exploring at the same time. You can work out what switching to a lower rate saves after the switching costs before you commit.

Frequently asked questions

Should I fix my home loan now in Australia in 2026?

The answer comes down to your borrower profile. First home buyers in early repayment, self-employed borrowers with variable income, and investors with long-hold strategies should seriously consider fixing. Short-term fixed rates currently sit at or below packaged variable rates at most major lenders, so you are not paying a premium for certainty. If you plan to sell or refinance within 18 months, the break cost risk outweighs the benefit.

Is it wise to fix my mortgage now?

For most owner-occupiers on a standard variable rate with stable employment and no plans to sell, a 1-2 year fix provides genuine budget certainty at a rate roughly equivalent to what they are currently paying. The risk – that rates fall faster than expected in 2027 – is real but manageable with a shorter term.

Should I go fixed or variable mortgage in 2026?

Neither is universally right. The most sensible position for many borrowers in this environment is a split loan: fix 60-70% for 1-2 years to protect the majority of repayments, and keep 30-40% variable for flexibility and extra repayment capability. This removes the all-or-nothing pressure from the decision.

Will mortgage rates ever be 4% again?

Not in the near term. The cash rate is already at 4.35%, and variable home loan rates are in the 6.14%-6.74% range. Market pricing implies rates could reach 4.70% by end-2026. For home loan rates to return to 4%, the cash rate would need to fall to around 1.5%-2.0% – a scenario not in any mainstream 2026-2027 forecast.

Will interest rates go back to 3% in Australia?

The RBA’s May 2026 Statement on Monetary Policy projects underlying inflation above 3% until mid-2027. Rate cuts in the short term would work against that goal. The earliest realistic path to significant cuts is late 2027, which might bring the cash rate to 3.5%-3.75% – not 3%.

What happens if I fix my rate and then need to sell?

Your lender calculates a break cost using the Bank Bill Swap Rate (BBSW) formula. If rates have risen since you fixed, break costs may be minimal or zero. If rates have fallen since you fixed, break costs can be material – potentially $5,000-$20,000 or more depending on loan size, remaining term, and the size of the rate movement. Always request a break cost quote from your lender before committing to a sale.

Can I make extra repayments on a fixed loan?

Most lenders cap extra repayments on fixed loans at between $10,000 and $30,000 per year. Above that cap, you may be charged a fee. If you plan to make large extra repayments from a bonus or lump sum, check the cap before fixing. Keeping a portion in a variable rate with an offset account is often the cleaner solution for active repayers.

What is rate lock and is it worth it?

Rate lock reserves the rate quoted at application for up to 90 days, protecting you from a rate rise before settlement. Big four pricing: NAB 0.15% of the loan amount, CBA flat $750, Westpac 0.10% of the loan amount, and ANZ $750 per $1 million in lending (or part thereof). In the current rising-rate environment, I’m strongly recommending rate lock for any client fixing – the cost of being wrong without it is several times the lock fee.

Once you have decided whether to fix, the next question is who to apply with. Read the broker’s case for fixing in 2026 for a side-by-side of the big four against a broker’s panel.

This article contains general information only and does not constitute financial advice. Your personal financial situation, objectives and needs have not been considered. Before acting on any information, you should consider its appropriateness to your circumstances. Speak to a qualified mortgage broker for advice tailored to your situation. Mortgage World Australia Pty Ltd is a credit representative (CR No. 396946) of Mortgage Specialists Pty Ltd (Australian Credit Licence No. 387025).

Patrick is a Director and a Home Loan Specialist. He has been helping Australians with home loans since 2001. Prior to working as a mortgage broker Patrick was employed by Macquarie Bank for 3 years and also worked as an accountant for a publicly listed company. Patrick’s qualifications include:

Bachelor of Business, UTS Sydney. Majored in accounting and sub-majored in Finance and Marketing.

Diploma of Finance and Mortgage Broking Management FNS50310

Certificate IV in Financial Services (Finance/Mortgage Broking) FNS40804

Ready to Take the Next Step?

Whether you’re looking to buy your first home, refinance, or explore investment opportunities, Mortgage World Australia is here to help.

Fill out the contact form below, and one of our expert mortgage brokers will be in touch shortly to discuss your needs and guide you through your options.

Get Started Today!