Mortgage Switching Calculator

If you are paying more than the going rate on your home loan, switching to a sharper deal could save you thousands over the years you keep the loan. Use this mortgage switching calculator to estimate the difference between your current loan and a new one, after the switching costs, so you can see the real net saving rather than just a headline rate cut. Whether you are weighing up a refinance to chase a lower rate or simply checking whether it is worth the paperwork, the tool below gives you a number to start from.

How to use the Mortgage Switching Calculator

- Enter your current loan balance and remaining term. Use the amount you still owe, not the original loan, and how many years are left to run.

- Enter your current interest rate. The rate you are paying right now on the loan you are thinking of leaving.

- Enter current ongoing fees. The fees that you are paying right now.

- Enter the End Fee. This is the discharge fee charged by your existing lender when you discharge your mortgage. It is typically $300 to $500.

- Enter the new rate. This switching tool asks for both an introductory rate (or fixed rate) and the standard rate it reverts to. Use current illustrative rates as a starting point, then confirm the real numbers with a broker.

- Add the Upfront Refinance Fees. The application or establishment fee on the new loan, plus the government registration fees. You can find the government registration fees in the Stamp Duty Calculator (the Mortgage Registration Fee X 2). Leave fixed-rate break costs out for now, because those need an actual figure from your lender.

- Review the result. The calculator shows your new repayment, the savings over the remaining term, and the additional savings you could make by making extra repayments. The bar chart shows the accumulated savings each year of the loan term.

Switching and refinancing mean the same thing here: moving your home loan to a better deal, either with a new lender or your current one.

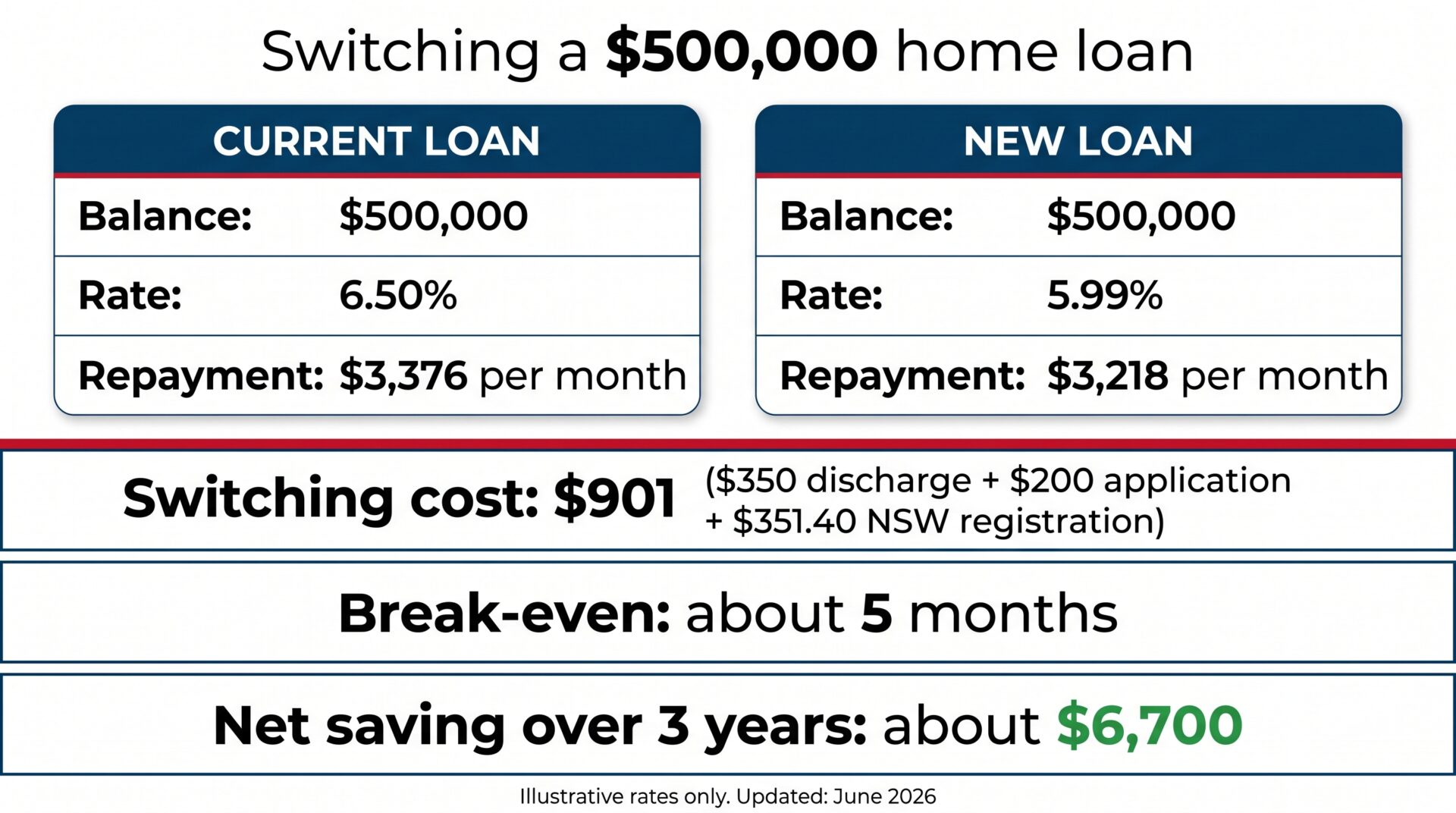

Worked example: switching a $500,000 loan to a lower rate

Take a $500,000 home loan with 25 years left to run. Here is what switching from an illustrative 6.50% to 5.99% looks like once the costs are in.

The repayment drop

At 6.50%, the repayment is about $3,376 a month. Drop the rate to 5.99%, and it falls to about $3,218, roughly $158 less every month. That is the cash-flow side: $158 back in your pocket each month for doing the paperwork once.

The interest saved

The bigger number is the interest. In the first year alone, the lower rate saves about $2,550 in interest on a $500,000 balance. Over three years, the gross interest saving comes to around $7,600, worked out on a reducing balance at the two rates.

The cost of switching

On a variable loan, the costs are modest. Say a $350 discharge fee on the old loan, a $200 application fee on the new one, and government registration fees totalling $351.40 in New South Wales. About $901 all up. Subtract that from the three-year interest savings, and you are left with a net saving of roughly $6,700 over three years. The $901 is recovered in about five months, and everything after that is yours.

Break costs scare people off, but on a variable loan, there usually are not any. The only real costs are a small discharge fee, government registration fees and the new lender’s setup fee. What actually matters is the rate gap multiplied by your balance over the years you keep the loan. On a $500,000 balance, half a per cent is real money. A broker also checks whether a sharp new rate survives once any introductory period ends, and whether a cashback offer tips the maths further in your favour.

Rates shown are illustrative only and current as at June 2026; your actual rates will depend on your lender, loan size and profile.

It is the same core maths the government’s own MoneySmart mortgage switching calculator uses, so the tool above gives you a view across 52+ lenders rather than a single bank’s pitch. CommBank, ANZ and Westpac each run their own refinance calculator, and NAB has its own home loan calculators, but a bank’s tool models a switch to that bank, not the genuine market-wide savings a broker can find.

What this calculator can’t tell you

The calculator compares two rates you type in. A real switch has moving parts it cannot see:

- Fixed-rate break costs. If your current loan is fixed, leaving it early can trigger a break cost. The lender works it out from how rates have moved since you fixed and how much fixed term is left, so it can be large or close to nothing. The calculator cannot predict it, and a broker gets the actual figure from your lender before you commit. If you are weighing this up, see should I fix my home loan.

- Whether the new rate lasts. Some sharp advertised rates are introductory or honeymoon rates that step up to a higher ongoing rate after a year or two. The calculator compares the rate you enter, but it does not know if that rate sticks. A broker models the revert rate, not just the teaser.

- Cashback offers. Some lenders pay $2,000 to $4,000 or more to refinance to them, though these days the offers come mostly from smaller and mutual lenders rather than the big four. A cashback only helps if the ongoing rate is genuinely competitive; paired with a higher rate it can cost you more over a few years. The calculator ignores cashbacks entirely. See cashback offers for the catch.

- Headline rate versus comparison rate. The headline rate is not the true cost. The comparison rate rolls the interest rate together with most fees and charges into a single figure, and switching to a lower headline rate that carries a worse comparison rate can leave you behind.

- Whether you will actually qualify. Refinancing is a fresh loan application. Your servicing, loan-to-value ratio, LMI (if you have slipped above 80% LVR), and credit conduct all get re-assessed. APRA-regulated lenders test you at your new rate plus 3% (with some exceptions), so a switch that obviously saves money can still be knocked back on paper. A valuation fee, and rarely stamp duty, can also apply on top of the discharge and application fees. A broker checks you qualify before you pay anything.

- Pricing across every lender. The calculator compares two rates. A broker compares your loan against the live pricing of more than 50 lenders, cashbacks and all, to find the genuine best switch, not just one bank’s number.

The calculator is your starting point. A broker models your real switching benefit across more than 50 lenders, break costs, revert rates and cashbacks included, so the saving on screen is the saving you actually pocket.

Related calculators

- Loan Repayment Calculator: work out the repayment on the new loan once you have settled on a rate.

- Home Loan Offset Calculator: see how an offset account on the new loan cuts the interest you pay even further.

- Comparison Rate Calculator: compare the true cost of two loans, not just their headline rates.

FAQs

Not sure? Have additional questions? Try here

This article contains general information only and does not constitute financial advice. Your personal financial situation, objectives and needs have not been considered. Before acting on any information, you should consider its appropriateness to your circumstances. Speak to a qualified mortgage broker for advice tailored to your situation. Mortgage World Australia Pty Ltd is a credit representative (CR No. 396946) of Mortgage Specialists Pty Ltd (Australian Credit Licence No. 387025).

Important information

Calculator disclaimer. The results from this calculator should be used as an indication only. Results do not represent either quotes or pre-qualifications for a loan. The specific details of your loan will be provided to you in your loan contract. It is advised that you get in touch with us before taking out a loan so that we can provide you with advice that is tailored to your situation.

Assumptions. This calculator uses the information you enter together with standard assumptions; figures are estimates only, are not an offer of credit, and do not take into account your objectives, financial situation or needs.

Comparison rate. Where an interest rate or repayment is shown, the comparison rate is based on a loan amount of $150,000 over a term of 25 years. WARNING: This comparison rate is true only for the example given and may not include all fees and charges. Different terms, fees or other loan amounts might result in a different comparison rate. For variable interest only loans, comparison rates are based on the initial 5-year interest only period. For fixed interest only loans, comparison rates are based on an initial interest only period equal in length to the fixed period. During an interest only period, your interest only payments will not reduce your loan balance. This may mean you pay more interest over the life of the loan. Interest rates are shown per annum (p.a.).