What Is a Comparison Rate? The True Cost of Home Loans

What Is a Comparison Rate? The True Cost of Your Home Loan, Explained

On this page ▾

- What is a comparison rate?

- Comparison rate vs interest rate: what’s the difference?

- How comparison rates are calculated in Australia

- What’s included in a comparison rate, and what’s not

- Worked example: when the lowest interest rate isn’t the cheapest loan

- Three reasons comparison rates can mislead you

- How to actually compare home loans, a broker’s checklist

- Frequently asked questions

When you scan home-loan ads, two numbers sit side by side: the interest rate, and the comparison rate. The comparison rate is the bigger of the two, and it is the one most borrowers ignore. That is a mistake, but so is treating it as the final answer. This guide explains what the comparison rate includes, what it leaves out, and the three places it routinely misleads Australian buyers.

What is a comparison rate?

A comparison rate is a single percentage that combines a home loan’s interest rate with most of its mandatory fees, expressed as an annual rate on a standard $150,000 loan over 25 years. It is designed to give borrowers one number to compare two loans against, instead of weighing fees and interest rates separately. Australian lenders are required by law to publish it next to every advertised rate.

The number is always equal to or higher than the headline interest rate, because the headline rate ignores fees and the comparison rate adds them in.

Comparison rate vs interest rate: what’s the difference?

The interest rate is the cost of borrowing the money. The comparison rate is the cost of borrowing plus most of the fees the lender charges to set up and run the loan.

A 5.99% interest rate with a 6.35% comparison rate tells you the loan carries roughly 0.36 percentage points of fees baked in once the standard formula is applied. If two loans show a wider spread between the two numbers, the loan with the wider gap is the more fee-heavy product, even when its headline rate looks cheaper. For first-time buyers working through our first home buyer guide, this gap is the first sanity check on any rate that looks too sharp to be true.

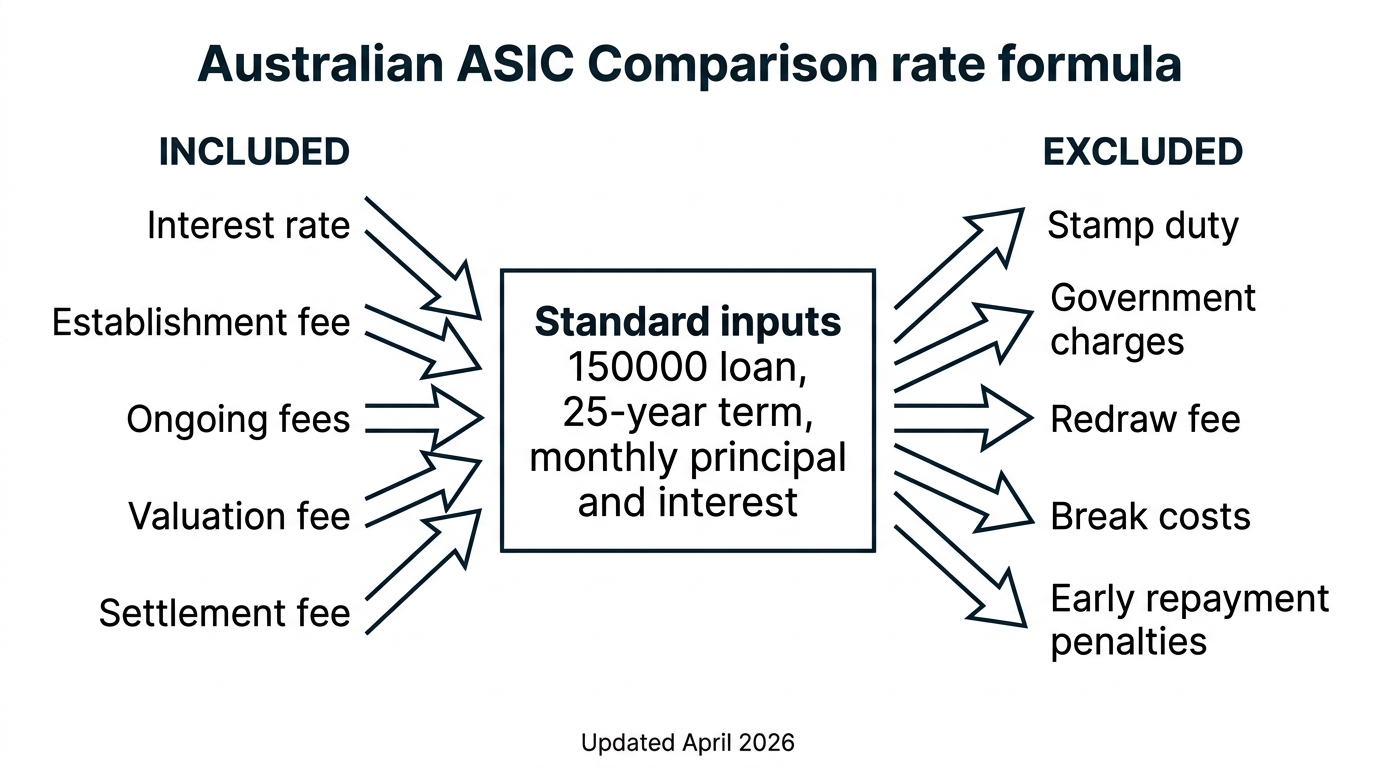

How comparison rates are calculated in Australia

The standard $150,000 / 25-year formula

The comparison rate is calculated on a single ASIC reference loan: $150,000 borrowed over 25 years, with monthly principal-and-interest repayments. Every lender in Australia uses the same inputs. That is the only way two products from two different lenders can be compared on a single number.

The formula takes the advertised interest rate, layers on the loan’s mandatory fees (one-off and ongoing), and solves for the effective annual rate that would produce the same total cost. It is essentially an internal rate of return calculation, run on a standardised scenario.

Why disclosure is mandatory (the NCCP Act)

Comparison-rate disclosure is required under the National Consumer Credit Protection Act 2009 (NCCP) and the National Credit Code that sits within it. Lenders cannot advertise an interest rate on a regulated consumer credit product without also publishing the comparison rate alongside it, and they cannot show the comparison rate in smaller font or weaker contrast than the headline rate. The rule applies across home loans, car loans, and personal loans.

The Act also forces lenders to publish a statutory warning next to every comparison rate: the rate is true only for the example given, and different loan amounts or terms will produce different numbers. Most borrowers skim past that warning. It is the one sentence on the page worth re-reading.

What’s included in a comparison rate, and what’s not

Fees included

The standard comparison rate calculation includes the headline interest rate plus the loan’s mandatory establishment and ongoing costs. On a typical home loan, that means:

- The interest rate itself

- Application or establishment fees

- Ongoing service or monthly account fees

- Valuation fees the lender charges directly

- Settlement fees

Fees and costs excluded

These costs are real but sit outside the calculation, which is why the published comparison rate is a partial picture, not a complete one:

- Government charges, including stamp duty and mortgage registration

- Redraw fees

- Break costs on fixed-rate loans

- Early repayment penalties

- Late-payment fees and default charges

- Fees that depend on loan-specific events (rate-lock, switching from interest-only to principal-and-interest, package fees that activate only when you take certain features)

The exclusions matter because some of them, particularly break costs and package fees, can be the largest cost a borrower faces over the life of a loan.

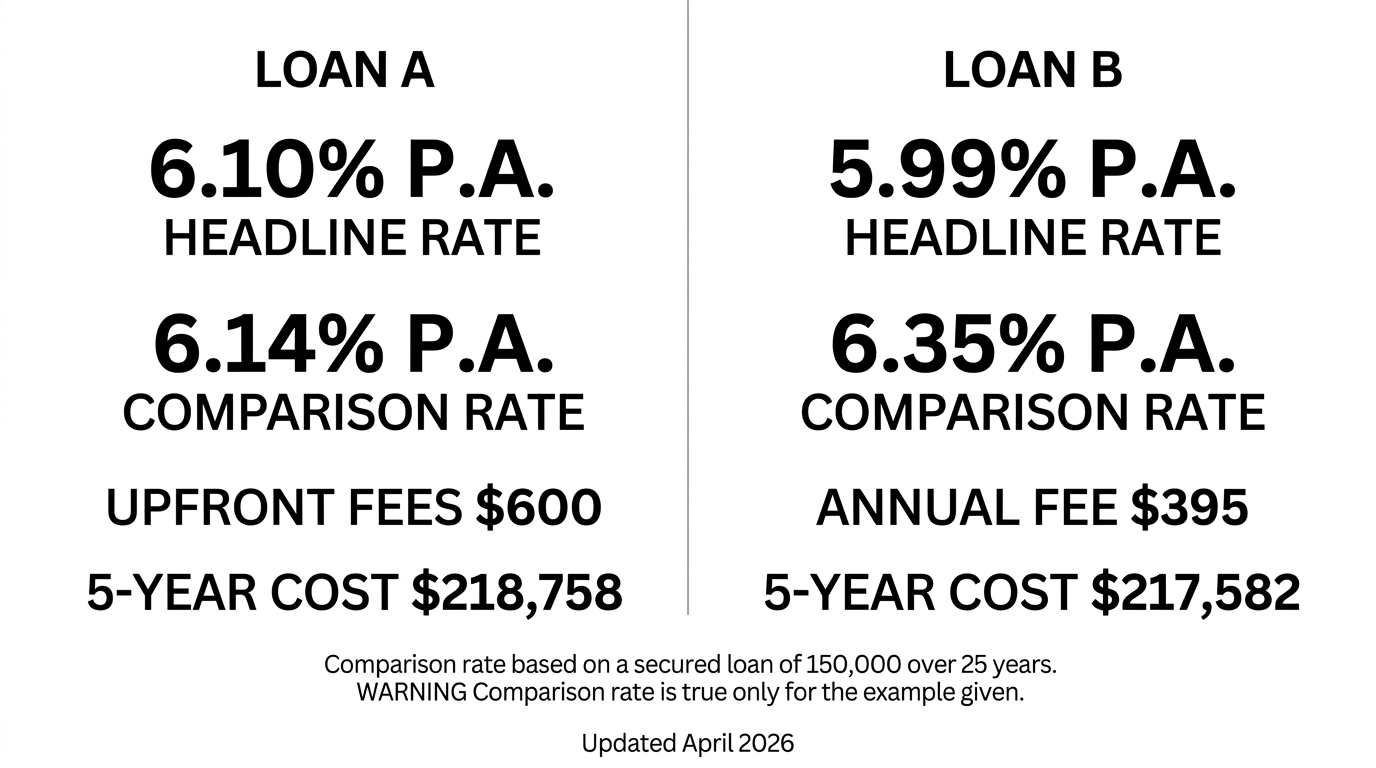

Worked example: when the lowest interest rate isn’t the cheapest loan

Two real-world loan offers, lined up on the standard ASIC formula, then on a real Sydney loan size.

| Loan A | Loan B | |

|---|---|---|

| Headline interest rate | 6.10% | 5.99% |

| Establishment fee (one-off) | $600 | $0 |

| Annual package fee | $0 | $395 |

| Comparison rate ($150k / 25yr) | 6.14% | 6.35% |

On the published comparison rate, Loan A wins. Loan B’s lower headline rate is more than wiped out by its $395-per-year package fee once it is amortised across the small $150,000 reference loan.

Now run the same two loans on a $600,000 owner-occupier loan over 30 years, which is closer to the average Sydney home loan today. Five years of monthly principal-and-interest, plus the upfront and ongoing costs each loan attracts:

| Loan A | Loan B | |

|---|---|---|

| Monthly P&I | $3,635.97 | $3,593.45 |

| Establishment fee | $600 | $0 |

| Package fees over 5 years | $0 | $1,975 |

| Total cost over 5 years | $218,758 | $217,582 |

The result flips. Loan B costs $1,176 less over five years, even though its comparison rate looked worse. The 0.11 percentage-point rate difference dominates the fee gap once the loan size is realistic. If you are weighing a switch on rate, see your real switching saving on your own balance.

Now flip it again. On a $250,000 loan over 15 years, where the package fee is amortised across a smaller and shorter loan, Loan A returns to being cheaper, this time by about $482 over five years.

The comparison rate gave you a single answer. Reality gave you three different answers depending on the loan size and term. That is the trap. For a deeper look at why two borrowers can be quoted very different effective rates on the same product, a reason why you may not get the best interest rate is worth reading.

Three reasons comparison rates can mislead you

The $150k baseline doesn’t match a real Sydney loan

The ASIC formula was set when an average Australian home loan was closer to $150,000. According to ABS Lending Indicators, by the end of 2025 the average new owner-occupier loan was around $736,000 nationally and roughly $816,000 in Sydney. Most borrowers also take out loans over 30 years now, not 25.

That gap matters because comparison-rate amortisation spreads fixed-dollar fees, like a $600 establishment fee or a $395 yearly package fee, across the small $150,000 / 25-year baseline. Those fees take up a much bigger share of the standardised loan than they would on a real $650,000 / 30-year loan. The published comparison rate runs higher than the rate the borrower would experience in real life. The comparison rate routinely overstates the true cost of a modern Australian home loan. The outdated baseline biases the published number upward.

Fixed rates look worse than they are

For a fixed-rate loan, the comparison rate has to assume what happens when the fixed period ends. The convention is to use the lender’s standard variable rate as the revert rate. That standard variable rate is almost always higher than what the borrower would realistically pay, because most borrowers refinance, refix, or negotiate at the end of the fixed term. The fixed-rate comparison rate ends up reflecting a worst-case path most borrowers never walk. For a side-by-side on the trade-off itself, our guide to fixed rate home loans walks through when each option fits.

Features that save you money are ignored (offset, redraw, package benefits)

The calculation ignores features that change real outcomes. An offset account that holds $50,000 in everyday savings can shave thousands of dollars off interest over five years. The comparison rate does not see that. A package loan with a higher headline rate but a free credit card and a fee waiver can deliver real savings the formula will not capture. A loan with no offset and no redraw shows up identically in the comparison rate but costs the borrower significantly more over time.

How to actually compare home loans, a broker’s checklist

The comparison rate is a fast filter. It is not a decision input. We work through this checklist with every client before we present a loan recommendation:

- Model the actual loan size and term, not the $150,000 / 25-year baseline

- Add up the fees you will actually pay (some of the excluded ones might apply to you, some included ones will not)

- Price the features you will actually use: offset, redraw, package benefits, free property valuations on refinance

- Calculate the break cost if you might refinance or refix in the next three years

- Compare on the Loan-to-Value Ratio (LVR) tier you actually qualify for, not the lender’s best advertised tier

This is what we do for every client. With access to 52+ lenders, we can run the real numbers on your actual loan before you sign anything, including for clients refinancing your home loan where break costs and feature gaps tend to dominate. Speak to a Mortgage World Australia broker and we will model the loans you are considering against your actual loan size, term, and goals. For the broader product set, our home loan options hub covers the main loan structures alongside this explainer.

Frequently asked questions

What does a 3.99% comparison rate mean?

A 3.99% comparison rate means the loan’s true annual cost works out to 3.99 percent on the standard ASIC example ($150,000 over 25 years, monthly P&I) once the headline interest rate plus mandatory fees are blended together. The interest rate itself sits below 3.99%; the comparison rate is always equal to or higher than the interest rate.

What does a 0% comparison rate mean?

A 0% comparison rate effectively does not exist in home lending. It appears in some car finance promotions where the lender recovers the rate cost in the vehicle price or in fees the formula does not capture. Treat any 0% rate on a credit product as a signal to ask exactly where the lender is making its money.

What does a comparison rate mean when buying a car?

The same definition applies. Under the National Consumer Credit Protection Act, comparison rate disclosure is required for all consumer credit, including car loans, personal loans, and home loans. The standard reference amount and term differ by product category, but the principle is identical: blend the rate with mandatory fees so two competing offers can be lined up against one number.

What is a good comparison rate?

In April 2026, a competitive variable owner-occupier comparison rate sits in the low-to-mid 6% range for borrowers with a strong deposit. The right answer for you depends on your loan size, deposit, loan term, and which features you actually need. Because the published comparison rate is calculated on a $150,000 / 25-year reference, your real rate on a $650,000 Sydney loan over 30 years will run lower than the published number.

Comparison rate vs variable rate, what’s the difference?

A variable rate is the live interest rate your lender charges and adjusts over time. A comparison rate is a separate disclosure number that blends the rate with mandatory fees on the ASIC standard $150,000 / 25-year reference loan. The variable rate tells you what the loan currently charges. The comparison rate tells you what the same loan plus its fees would cost on a standard scenario.

Patrick O’Brien, Director and Home Loan Specialist since 2001.

This article contains general information only and does not constitute financial advice. Your personal financial situation, objectives and needs have not been considered. Before acting on any information, you should consider its appropriateness to your circumstances. Speak to a qualified mortgage broker for advice tailored to your situation. Mortgage World Australia Pty Ltd is a credit representative (CR No. 396946) of Mortgage Specialists Pty Ltd (Australian Credit Licence No. 387025).

Patrick is a Director and a Home Loan Specialist. He has been helping Australians with home loans since 2001. Prior to working as a mortgage broker Patrick was employed by Macquarie Bank for 3 years and also worked as an accountant for a publicly listed company. Patrick’s qualifications include:

Bachelor of Business, UTS Sydney. Majored in accounting and sub-majored in Finance and Marketing.

Diploma of Finance and Mortgage Broking Management FNS50310

Certificate IV in Financial Services (Finance/Mortgage Broking) FNS40804

Ready to Take the Next Step?

Whether you’re looking to buy your first home, refinance, or explore investment opportunities, Mortgage World Australia is here to help.

Fill out the contact form below, and one of our expert mortgage brokers will be in touch shortly to discuss your needs and guide you through your options.

Get Started Today!