Rental Yield Calculator Australia: 2026 Formula + Benchmarks

Rental yield calculator: formula, benchmarks and lender rules

On this page ▾

- What is rental yield?

- Gross vs net rental yield: what’s the difference?

- How to calculate rental yield (the formula + worked example)

- What is a good rental yield in Australia? (benchmarks by state)

- How lenders treat rental yield in serviceability

- Rental yield vs capital growth: which should investors prioritise?

- 5 ways to improve the rental yield on an existing property

- Frequently asked questions about rental yield

- Ready to run the numbers on your next investment?

Rental yield is the first number most property investors learn to calculate. It’s also the first number lenders discount when they assess your next loan. Knowing both sides is what separates investors who buy well from investors who buy and hope.

This guide covers the gross and net rental yield formulas, benchmark yields across every Australian capital city as at March 2026, and how lenders actually treat rental income when they assess your borrowing capacity. You’ll also find a free calculator below so you can run the numbers on any property you’re looking at. For more on this, see our depreciation deep-dive guide.

The headline: rental yield is a starting point, not the finish line. It tells you whether a property pays its own costs. It doesn’t tell you whether the bank will lend on it, or whether it’ll grow in value. Both of those matter more over the life of an investment.

What is rental yield?

Rental yield is the annual rental income a property generates as a percentage of its value. It’s the clearest single measure of whether a property is a cash-flow play or a capital-growth play, and it’s the number every major data provider (Cotality, SQM Research, Domain) reports monthly.

Rental yield meaning in plain English

If a property is worth $600,000 and rents for $30,000 a year, the gross rental yield is 5%. That’s the rent divided by the price, expressed as a percentage. The higher the number, the more income the property throws off relative to what you paid for it. A yield alone doesn’t tell you if the deal is good. It tells you how the numbers lean.

Gross vs net rental yield: what’s the difference?

Gross yield uses the total rent. Net yield subtracts the costs of holding the property. Net is always lower than gross, and it’s the figure that actually matters once you’ve bought.

| Measure | What it includes | Best used for |

|---|---|---|

| Gross rental yield | Annual rent ÷ property price | Fast comparisons between properties or suburbs |

| Net rental yield | (Annual rent − annual holding costs) ÷ property price | True cash flow analysis before tax |

Most online calculators and real estate portals quote gross yield because it’s simple and consistent. Cotality and SQM Research publish gross yields for benchmarking. Net yield is the figure you run before you sign a contract. It’s the one that tells you what the property actually costs to hold.

How to calculate rental yield (the formula + worked example)

Two formulas. One for fast comparisons, one for the cash-flow reality.

Gross rental yield formula

Three steps:

- Multiply the weekly rent by 52 to get annual rental income.

- Divide the annual rent by the property’s purchase price (or current value).

- Multiply by 100 to express the result as a percentage.

Formula: Gross Rental Yield = (Annual Rent ÷ Property Price) × 100

Net rental yield formula

Same structure, but the rent is reduced by annual holding costs before you divide.

Formula: Net Rental Yield = ((Annual Rent − Annual Holding Costs) ÷ Property Price) × 100

Annual holding costs typically include council rates, strata levies (for units), insurance, property management fees (usually 6 to 8% of rent), routine maintenance budget (around 1% of property value), vacancy allowance, and land tax if applicable. They do not include mortgage interest. Net yield measures the property’s own performance, not the performance of your loan structure.

Worked example: Parramatta house vs Blacktown unit

The two scenarios below use realistic April 2026 figures for a Parramatta house and a Blacktown unit. Same investor, same deposit, very different yield profiles.

| Input | Parramatta house | Blacktown unit |

|---|---|---|

| Purchase price | $1,600,000 | $550,000 |

| Weekly rent | $700 | $560 |

| Annual rent | $36,400 | $29,120 |

| Gross yield | 2.3% | 5.3% |

| Council rates (est.) | $2,000 | $1,800 |

| Strata (est.) | — | $4,400 |

| Insurance | $1,500 | $600 |

| Maintenance (1% of price) | $16,000 | $5,500 |

| Property management (7%) | $2,550 | $2,040 |

| Land tax (NSW 2026) | $0 | $0 |

| Total holding costs | $22,050 | $14,340 |

| Net yield (pre-interest) | 0.9% | 2.7% |

Two things stand out. The Parramatta house runs at a thin net yield of 0.9% before interest costs. Investors buy properties like this for capital growth, not cash flow, and they know going in that the rent won’t cover the costs. The Blacktown unit delivers a 5.3% gross yield and a net yield of 2.7%, but the strata levy quietly eats nearly half the rental income. Units in buildings with pools, gyms or high-rise structures can carry strata over $1,500 a quarter, which can tip a “high yield” property into negative territory fast.

A quick note on NSW land tax. For the 2026 land tax year, the general threshold sits at $1,075,000 of land value (Revenue NSW, frozen from 2024). Land tax applies to the unimproved land value set by the Valuer General, not the purchase price and not the dwelling value. A $1.6M Parramatta house often has a land value below $1M, which means zero land tax on a first NSW investment property. It scales quickly once you add a second property, because the state aggregates your land holdings. Land tax figures are based on Revenue NSW 2026 thresholds; thresholds and rates are reviewed periodically, so verify current figures at revenue.nsw.gov.au before acting.

Free rental yield calculator

Run your own numbers below. All calculations happen in your browser. Nothing is saved or sent anywhere.

Rental Yield Calculator

Net yield excludes mortgage interest. For a full serviceability view, speak to a mortgage broker.

What is a good rental yield in Australia? (benchmarks by state)

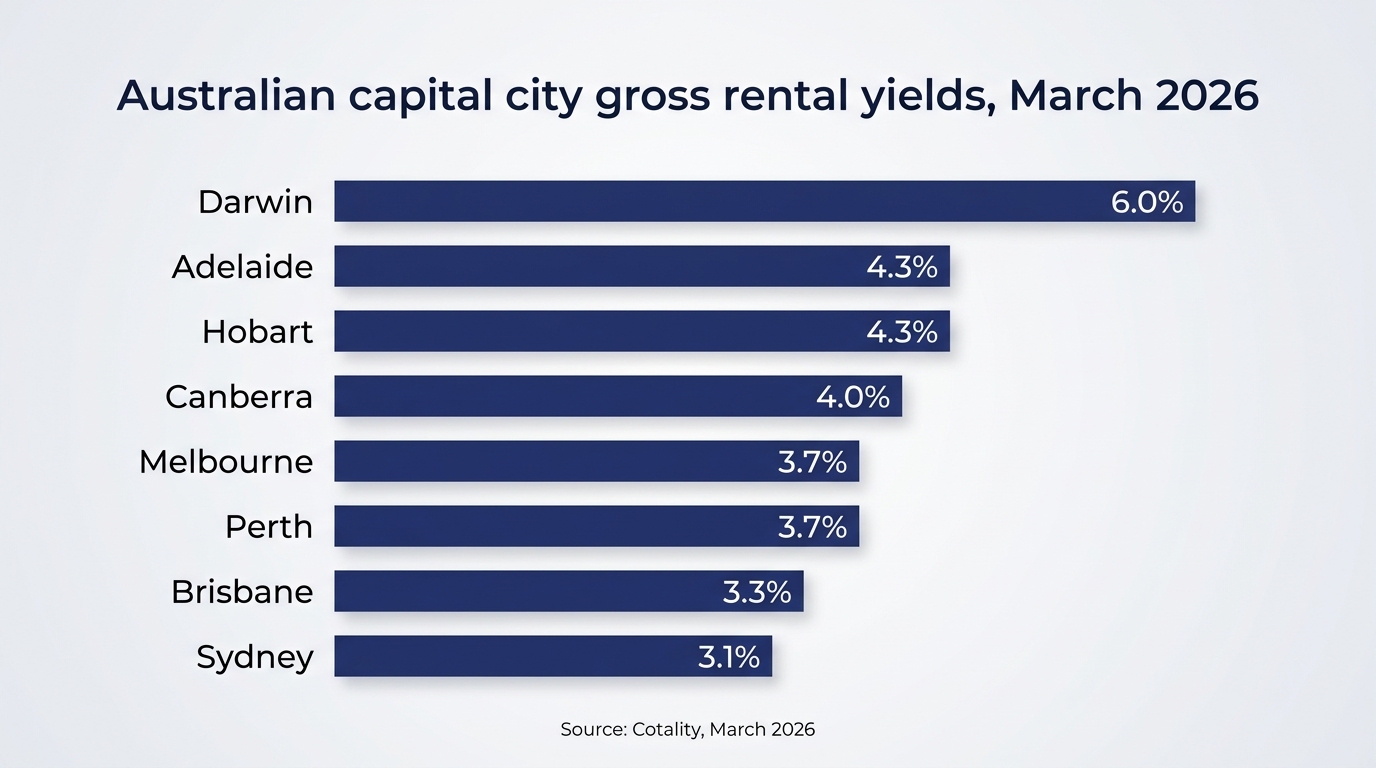

"Good" is relative to the market. A 3% gross yield is normal in inner Sydney. In Darwin it'd be well below average. The benchmark table below shows combined dwelling yields for every Australian capital as at March 2026, per Cotality's Home Value Index and Quarterly Rental Review (Cotality is the renamed CoreLogic).

Gross yield benchmarks by capital city

| Capital city | Combined gross yield | What it tells you |

|---|---|---|

| Sydney | 3.1% | Lowest in the country; price-driven, capital growth market |

| Melbourne | 3.7% | Slight uplift on Sydney; similar growth-over-yield dynamic |

| Brisbane | 3.3% | Value growth outpacing rents; yields sit near Sydney and Melbourne |

| Adelaide | 4.3% | Consistent performer; strong unit yields |

| Perth | 3.7% | Held up despite strong recent price growth; still above the capital city average |

| Hobart | 4.3% | Smaller market; yield holds up despite cooling prices |

| Darwin | 6.0% | Highest yield of any capital; slower long-term growth |

| Canberra | 4.0% | Stable; driven by public sector tenant demand |

| National | 3.57% | National average, all dwellings |

Gross rental yields as at March 2026, per Cotality. Combined dwellings include houses and units.

Houses vs units: which delivers better yield?

Units consistently deliver higher gross yields than houses across every capital city. The national split as at March 2026 sits at roughly 3.0% for houses and 4.3% for units. The maths works in units' favour. Unit prices sit further below house prices than unit rents sit below house rents, so the rent-to-price ratio runs higher on units. The trade-off is that houses have historically outperformed units on long-run capital growth, and body corporate fees chip away at unit cash flow.

How lenders treat rental yield in serviceability

This is the part that changes the deal. The lender isn't going to use the full rent in your loan assessment. Knowing which lenders discount the rent least can be the difference between a deal getting approved and a deal getting declined.

Why lenders shade rental income (the 80% rule)

Lenders don't treat your $700 a week as $700. They shade it, usually by 20 to 30%, to cover vacancy, management fees, maintenance and general prudence. Most major Australian lenders sit at 80% shading: they'll use 80% of the gross rent in their serviceability calculation. A small number of lenders apply 70 or 75%, and some specialist lenders accept 80 to 90% in specific scenarios. The industry default to assume: 80%.

One worth flagging: CBA caps the usable gross yield in serviceability at 8% of the property's value. If you're buying a genuine high-yield property, say a regional unit at 10% gross, CBA will only count rental income up to that 8% cap. Rare to hit this in Sydney or Melbourne, but it surfaces when investors look at high-yield regional or interstate opportunities. In our experience running investor scenarios across 52+ lenders, a broker who knows which lenders don't have this cap can unlock tens of thousands in borrowing capacity.

What this means for your borrowing capacity

On $36,400 a year in rent at 80% shading, the lender assesses $29,120 as assessable rental income. At a 6% serviceability interest rate over 30 years, that supports roughly $400,000 of additional debt on top of your salary. At 70% shading, the same rent supports closer to $350,000. That $50,000 gap is the difference between buying in Parramatta and buying in a cheaper corridor. It's the single biggest reason to have your rental income tested across multiple lenders before you put in an offer.

If you want to see where you land, our how much can I borrow guide runs through the full serviceability picture, and the borrowing power calculator gives you a quick estimate.

Rental yield vs capital growth: which should investors prioritise?

Both, but at different stages of a portfolio. High-yield properties pay you to hold them. The rent covers most or all of the costs, and you can scale faster without the cash flow squeeze. High-growth properties make you rich over time. The capital gain compounds, and the rent is secondary.

Most experienced investors want a mix. The early properties are often growth-focused (inner-capital, lower yield, stronger long-run equity), and later additions lean higher-yield to free up serviceability for the next purchase. The tax side matters too. Negative gearing in Australia offsets a low-yield property's shortfall against your income, and investment property capital gains tax rules reward holding for more than 12 months with a 50% discount on the gain.

For first-time investors, the rentvesting strategy lets you buy where the yields make sense and rent where you want to live. It's a strategy we see working well for Western Sydney professionals priced out of their home suburb.

5 ways to improve the rental yield on an existing property

Across the investor clients we've helped at Mortgage World Australia, five levers show up again and again when an existing property isn't pulling its weight on yield.

- Review the rent annually. A lot of landlords leave rents below market because raising them feels awkward. A $20 a week lift on a $500 property is a 0.21% yield improvement, and the tenant often expects it.

- Target short-to-medium-stay where zoning allows. Furnished corporate, student or NDIS rentals can deliver 1.5 to 2.5x standard rental yields. Council and strata rules vary; check before committing.

- Add a bedroom or granny flat. A compliant granny flat in Western Sydney can add $400 to $600 a week of rent to an existing property. Depreciation kicks in on the new build too, and you can often fund the build by using existing equity to buy or build.

- Renegotiate outgoings. Property management fees, insurance and strata contracts are rarely re-shopped. Two or three calls a year can save 5 to 10% on holding costs, which flows directly through to net yield.

- Buy better next time. Yield at purchase is easier to improve than yield after settlement. Use the benchmarks above and look at suburbs with strong yield profiles before you commit.

Frequently asked questions about rental yield

Is 4.5% a good rental yield?

A 4.5% gross rental yield is solid in the Australian context. It sits above the March 2026 national average of 3.57% (per Cotality) and well above Sydney's combined 3.1%. Whether it's right for you depends on strategy. High yield often comes with slower capital growth, and a 4.5% gross yield can still run cash-flow negative once interest, strata, rates and management fees are counted.

Is 3% rental yield bad?

A 3% gross yield is below the Australian national average but is normal in blue-chip Sydney and Melbourne suburbs. Investors buying in these markets typically accept low yields in return for stronger long-term capital growth. A 3% yield becomes a problem when it's paired with a stretched serviceability position. The rent won't cover the interest, and the lender knows it.

What is the 2% rule and does it apply in Australia?

The 2% rule is a US real estate heuristic: monthly rent should be at least 2% of the purchase price (equivalent to a 24% annual gross yield). It does not apply in Australia. No Australian capital comes close. Darwin leads at 6.0% gross yield (Cotality, March 2026). Australian investors should use local benchmarks, not imported US rules of thumb.

What is a realistic rental yield in Australia?

For combined dwellings in the capital cities as at March 2026 (Cotality): Sydney 3.1%, Melbourne 3.7%, Brisbane 3.3%, Adelaide 4.3%, Perth 3.7%, Hobart 4.3%, Darwin 6.0%, Canberra 4.0%. Unit yields typically run 1 to 1.5 percentage points higher than houses in each city. Regional markets can push gross yields above 7% in some suburbs.

Do lenders use rental yield when assessing my loan?

Yes, but they discount the figure. Most major Australian lenders assess 70 to 80% of gross rental income in their serviceability calculation to cover vacancy, management fees and maintenance. Some lenders apply additional caps. CBA, for example, will not use rental income that implies more than 8% gross yield on the property's value. Your broker can tell you which lender treats your specific scenario most favourably.

Ready to run the numbers on your next investment?

Rental yield is the opening question, not the final answer. The serviceability test, the lender's shading rules, the holding cost reality. They all sit on top of the headline yield figure and decide whether a deal actually works.

If you're weighing up an investment purchase, talk to our mortgage brokers. We'll run your scenario across 52+ lenders, show you which ones treat your rental income most favourably, and tell you what you can borrow before you put in an offer. You can also see our specialist residential investment loans page for how structure, rates and features differ on investor debt.

Patrick O'Brien, Director and Home Loan Specialist since 2001.

This article contains general information only and does not constitute financial advice. Your personal financial situation, objectives and needs have not been considered. Before acting on any information, you should consider its appropriateness to your circumstances. Speak to a qualified mortgage broker for advice tailored to your situation. Mortgage World Australia Pty Ltd is a credit representative (CR No. 396946) of Mortgage Specialists Pty Ltd (Australian Credit Licence No. 387025).

Patrick is a Director and a Home Loan Specialist. He has been helping Australians with home loans since 2001. Prior to working as a mortgage broker Patrick was employed by Macquarie Bank for 3 years and also worked as an accountant for a publicly listed company. Patrick’s qualifications include:

Bachelor of Business, UTS Sydney. Majored in accounting and sub-majored in Finance and Marketing.

Diploma of Finance and Mortgage Broking Management FNS50310

Certificate IV in Financial Services (Finance/Mortgage Broking) FNS40804

Ready to Take the Next Step?

Whether you’re looking to buy your first home, refinance, or explore investment opportunities, Mortgage World Australia is here to help.

Fill out the contact form below, and one of our expert mortgage brokers will be in touch shortly to discuss your needs and guide you through your options.

Get Started Today!