Investment Property Depreciation Schedule: 2026 Broker Guide

Investment property depreciation in 2026: what every property investor needs to know before applying for a loan

On this page ▾

- What investment property depreciation actually is, in plain English

- The 2017 rule change every existing investor needs to know

- New build vs established: a side-by-side cash-flow comparison

- How depreciation affects your borrowing capacity and serviceability

- When to commission a depreciation schedule

- What a quantity surveyor’s report contains and why a $440 to $770 fee returns thousands

- Depreciation × negative gearing: the combined annual deduction worked out

- What this means at tax time

- What to do this week if you’ve never had a depreciation schedule

- Frequently asked questions

Depreciation is the single most underclaimed tax deduction in Australian property investment. The ATO allows it. Your accountant can lodge it. The numbers are real. Yet most investors who bought after 9 May 2017 either skip the schedule altogether or claim a fraction of what they are entitled to.

This guide is for property investors who own a rental, are about to buy one, or are about to refinance. We explain how depreciation actually works, what changed in 2017, what a quantity surveyor’s report covers, and the part nobody else covers in plain English: how depreciation flows through to lender serviceability and your borrowing capacity for the next investment loan.

Mortgage World Australia has been arranging investment property loans since 2001. Patrick O’Brien owns multiple investment properties and has personally walked through every section of this guide in conversations with clients. The financing angle in section 5 is what brokers see, and quantity surveyors don’t.

If you need the broader picture on lending and structure first, our investment property loans guide covers the loan side. This article covers the depreciation side.

What investment property depreciation actually is, in plain English

Depreciation is a tax deduction that recognises the loss of value of a building and the assets inside it as they age. It splits into two parts under the Income Tax Assessment Act 1997.

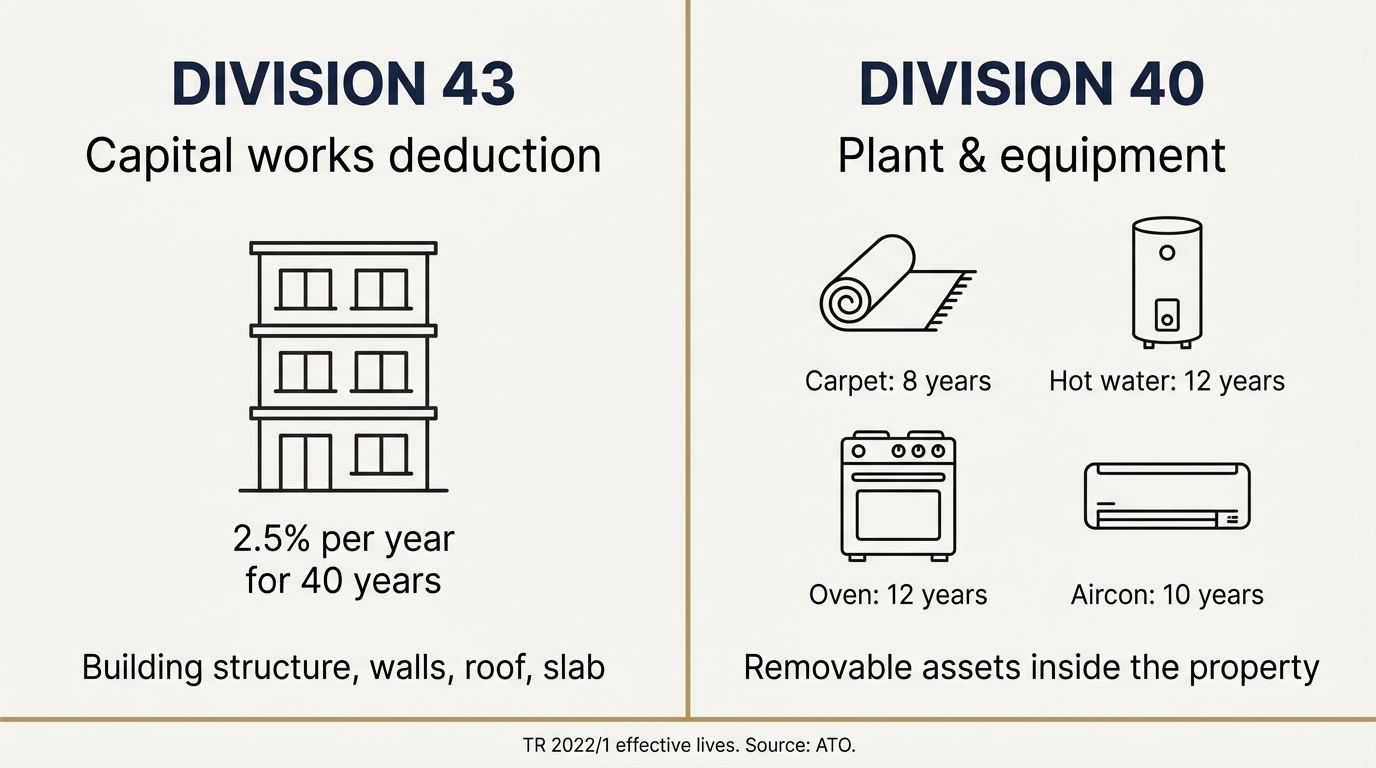

Division 43 capital works deduction: the 2.5% rule for 40 years

Division 43 covers the building itself. The walls, the roof, the slab, the kitchen cabinetry that is fixed in place. For residential rental properties where construction commenced on or after 15 September 1987, the rate is 2.5% per year for 40 years. Multiply 2.5% by 40 years and you reach 100%. That is the building written off in full over the depreciation life.

If construction commenced before 15 September 1987, the building generally cannot be claimed under Division 43. There is a narrow window between 18 July 1985 and 15 September 1987 where residential construction was eligible at 4% over 25 years, but those buildings have already hit the 100% cap and are no longer claimable. Source: ATO, Capital works deductions.

The deduction is calculated on the original construction cost, not the purchase price. If you bought a 2010-built unit in 2024 for $700,000, the relevant figure is what it cost the developer to build it, not what you paid. A quantity surveyor estimates that figure for you.

Division 40 plant and equipment: the moveable assets

Division 40 covers the assets inside the building that have a finite life and are not structural. Carpet, hot water systems, blinds, dishwashers, ovens, air conditioning, smoke alarms, and similar items. Each asset has an effective life set by the ATO under Tax Ruling TR 2022/1.

Common residential effective lives include:

- Carpet: 8 years

- Hot water system: 12 years

- Oven: 12 years

- Dishwasher: 8 years

- Air conditioning, split system or room unit: 10 years

- Blinds: 10 years

- Smoke alarms: 6 years

The deduction can be calculated using either the prime cost method (straight-line, equal amount each year) or the diminishing value method (larger deduction in earlier years, smaller later). Most schedules use diminishing value because it pulls more of the deduction into the years investors care about most.

Why depreciation is a “non-cash” deduction

Every other rental expense involves you actually paying money. Interest on the loan. Council rates. Property management fees. Repairs. You write a cheque. Depreciation is different. You claim a deduction without paying anything that year. The cash stays in your pocket and the tax bill comes down.

That is the whole appeal. A depreciation schedule of $15,000 a year on a property where you have not spent a single extra dollar is, after tax at a 37% marginal rate, $5,550 in cash back to you each year.

The 2017 rule change every existing investor needs to know

This is the most widely misunderstood rule in residential property tax. If you bought a residential investment property after 7:30 PM AEST on 9 May 2017, your Division 40 claim is restricted in a way you may not have realised.

What the Treasury Laws Amendment (Housing Tax Integrity) Act 2017 actually did

The 2017 federal budget introduced amendments that took effect from 7:30 PM AEST on 9 May 2017. The bill passed Parliament on 15 November 2017 and the rules apply to income years commencing on or after 1 July 2017.

The change: investors who exchanged contracts on a residential rental property after that May 2017 cut-off cannot claim Division 40 deductions on the existing, second-hand plant and equipment that was already in the property at purchase. The previous owner already used those assets. The new owner cannot start a fresh decline-in-value claim on them.

The rule applies to residential rental properties only. Commercial properties are not affected. Source: Treasury Laws Amendment (Housing Tax Integrity) Act 2017; ATO, Limited deductions for residential rental property.

What you can no longer claim if you bought after 9 May 2017

If you bought a 2015-built apartment in 2022 with the original carpet, hot water system, and oven, the Division 40 deductions on those existing assets are off-limits. The previous owner had access to those deductions while they owned the property. You do not.

This is why a lot of post-2017 investors look at their tax return and see a thin depreciation figure, then conclude depreciation is not worth the schedule fee. That conclusion is wrong, because of what they can still claim.

What you can still claim on a post-2017 purchase

Three categories stay open:

- Division 43 capital works on the building. Untouched by the 2017 rule. If the property was built after 15 September 1987, the 2.5% per year capital works deduction continues to apply on the original construction cost.

- New plant and equipment you purchase yourself. If you replace the oven, install a new air conditioner, or recarpet the property after settlement, those new items are yours to claim under Division 40.

- Brand new properties bought directly from a developer. If you are the first owner to use the property and its assets, the second-hand restriction does not apply. Full Division 40 deductions are available on a new build.

The third category is why new builds and off-the-plan purchases are now disproportionately attractive to investors focused on tax outcomes.

New build vs established: a side-by-side cash-flow comparison

The 2017 rule has split the investor market into two cohorts. New-build buyers retain the full depreciation toolkit. Established-property buyers get a thinner stack of deductions but also pay less per square metre. The right answer depends on your goals, and the maths matters.

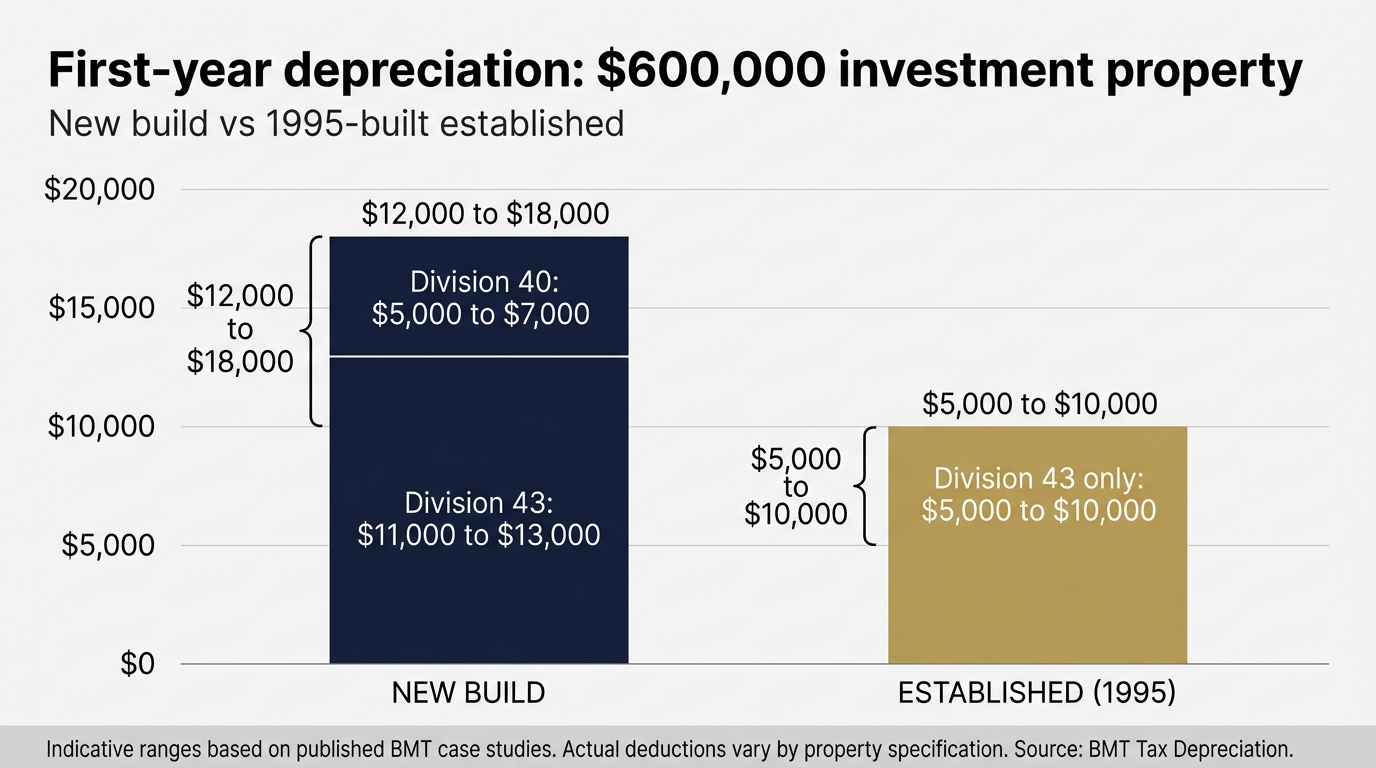

Worked example: $600,000 investment property, new build vs 1995-built established

Take a $600,000 investment property. We want the first-year combined depreciation deduction.

New-build apartment, $600,000, year-one depreciation:

Based on published BMT case studies for similar new-build properties, a first-year combined deduction of $12,000 to $18,000 is realistic for a $600,000 new-build apartment or townhouse. The Division 43 portion sits around $11,000 to $13,000 (2.5% on a $440,000 to $520,000 construction cost). The Division 40 portion adds another $5,000 to $7,000 in year one using the diminishing value method weighted to the early years.

Established 1995-built apartment, $600,000, year-one depreciation:

Construction is post-1987 so Division 43 still applies, but the 2017 rule blocks the original plant and equipment. Year-one deduction sits around $5,000 to $10,000, almost entirely Division 43 capital works. Roughly half of what a new build delivers in the first year.

The gap closes over time. Division 40 plant and equipment deductions taper off after the first 5 to 7 years for a new build. By year 10, both properties are mostly running on Division 43 alone. But across the first 5 years, the cumulative gap is meaningful: a new build can run $25,000 to $40,000 ahead of the established property in cumulative deductions.

If you are buying new, our construction loan guide covers how the financing works during the build phase.

What this does to your after-tax holding cost

Translate that to cash. At a 37% marginal rate, an extra $7,500 of first-year deduction returns $2,775 in cash. Five years of similar gaps compound into a $10,000 to $15,000 after-tax cash advantage for the new-build investor.

That advantage is not a reason to buy new for its own sake. New builds carry premiums, lower yields, and developer-margin risk. But for a buyer choosing between two otherwise comparable options, the depreciation profile is a real number that belongs in the spreadsheet, not a footnote. Use the rental yield calculator to model the after-tax cash flow before you commit.

How depreciation affects your borrowing capacity and serviceability

Here is the part most articles get wrong. The myth: “If I claim a big depreciation deduction, my taxable income drops and the bank will cut my borrowing capacity.” That is not how lenders assess investment property serviceability. Depreciation on your rental property does not reduce what you can borrow.

How lenders calculate rental income for serviceability

When a lender assesses your borrowing capacity, they treat the rental property as an income-producing asset with its own income line. Most lenders take your gross annual rent and apply a shading factor, typically 80%, sometimes 70%, occasionally 75% with conditions, to allow for vacancy, repairs, property management, and rates. That shaded figure is the rental income they use for serviceability.

Worked example. $32,000 gross annual rent on a $600,000 investment property. At 80% shading the lender uses $25,600 as assessable rental income. Whether you claim $5,000 or $20,000 in Division 43 and Division 40 deductions on your tax return, the lender’s rental income line stays the same. Depreciation does not enter the calculation.

This is the part most QS firms and accountants don’t say out loud: claiming depreciation does not reduce your borrowing capacity on the investment property. The non-cash nature works in your favour. You get the tax benefit on your return without losing rental income on your loan application.

Where the depreciation add-back actually applies: self-employed and business income

There is a depreciation add-back in lender serviceability, but it applies to a different income source entirely. If you are a self-employed business owner, sole trader, or company director drawing income from your own trading entity, the profit on your tax return is the figure lenders use as your assessable employment income. Some lenders will then add back depreciation claimed at the business level (vehicles, plant, equipment, fitout) to recognise that it is a non-cash expense and the actual business cash flow is stronger than the profit figure suggests.

That add-back is on your business depreciation, not on the investment property’s depreciation schedule. They are two different deductions and two different lender conversations.

For self-employed property investors, the practical implication splits cleanly:

- Rental property depreciation: claim it freely. It does not affect serviceability. There is no penalty for a strong depreciation schedule on your investment property.

- Business depreciation in your own trading entity: ask your broker which lenders accept 100% of the add-back. Some lenders limit the amount of depreciation that can be added back.

What does change borrowing capacity for property investors

The lender levers that actually affect investor borrowing capacity:

- Gross rental income and the shading factor your lender applies (80%, 70%, or 75% with conditions)

- Existing investment debt, repayment structure (interest-only or principal-and-interest), and the stress-rate buffer (APRA 3% for prudentially regulated lenders, 1% to 2% for non-bank lenders)

- Living expenses and number of dependents

- Personal income from PAYG, dividends, or business profit, with any allowable add-backs applied at the business level

If you are weighing your next investment finance, see our investment property loans guide for the structural side. Depreciation belongs in your tax conversation, not your serviceability conversation. The lender choice still matters because different lenders apply different shading rates, treat existing investment debt differently, and assess living expenses differently. That is the broker conversation worth having before you apply.

When to commission a depreciation schedule

Timing matters. Get the schedule wrong, and you leave thousands of dollars on the table.

The “soon after settlement” rule

Westpac’s investment property page says it clearly: the best time to get a tax depreciation schedule drawn up is soon after settlement on the property. We agree. Within 4 to 6 weeks of settlement is the practical window. Here is why.

The first-year deduction is calculated on a pro-rata basis from the date you took ownership. If you settle on 1 March, you get four months of depreciation in that financial year. If you commission the schedule six months after settlement, you have already missed nothing on the calculation, but you have lodged a tax return without the deduction and now need to amend.

Schedules also take 2 to 3 weeks from inspection booking to delivery. If you want the deduction in your first tax return after settlement, work backwards from your accountant’s lodgement deadline.

Backdating: claiming for previous years you missed

If you have owned the property for a few years and never had a schedule, you have not necessarily lost the deductions. The ATO allows individual taxpayers to amend prior-year returns generally within 2 years from the date of assessment. Some taxpayers have a 4-year window. Talk to your accountant.

For most investors, that means 2 years of backdated deductions, plus the current year, can be recovered through a tax return amendment. On a $15,000 annual deduction at a 37% marginal rate, that is $11,000 to $16,000 in cash recovered, less the schedule cost.

Renovations: get the schedule before you start

This is the timing rule almost nobody knows. If you are about to renovate, commission the schedule first, before you start work. Assets you have been depreciating yourself (carpet, oven, hot water system, blinds) carry a written-down value. When you scrap them, the remaining undeducted value can be claimed in full as a balancing adjustment. But only if a quantity surveyor has documented the asset and its written-down value before it goes in the skip.

This applies to assets you have been depreciating. For post-2017 second-hand purchases, the original plant and equipment was already excluded from your Division 40 claim under the 2017 rule, so there is no scrap value to lose on those items. The scrap-value deduction is in play for: pre-2017 purchases, brand-new properties bought from the developer, and assets you installed yourself since settlement.

Renovate first, schedule second, and you forfeit that scrap-value deduction. We have seen investors lose $4,000 to $8,000 this way.

What a quantity surveyor’s report contains and why a $440 to $770 fee returns thousands

A depreciation schedule is a tax document. The ATO requires it to be prepared by a “suitably qualified person” when the original construction cost is not known, which is the situation for almost every investor who bought from a previous owner.

The construction-cost estimation method

When historical construction costs are not available (which is most cases), the quantity surveyor uses construction-cost-estimation methods to back-calculate what it would have cost to build the property at the time of construction. The estimate factors in the building’s specifications, finishes, regional construction costs, and the year of build. This estimate becomes the Division 43 base.

The ATO recognises quantity surveyors as a profession qualified to estimate construction costs, per Tax Ruling TR 97/25. Architects, engineers, and certain other professions also qualify, but quantity surveyors are the standard.

What to look for: AIQS membership and Tax Practitioners Board registration

Two markers matter when choosing a firm.

The first is membership of the Australian Institute of Quantity Surveyors (AIQS). AIQS sets professional standards and is the recognised peak body for the profession.

The second is registration with the Tax Practitioners Board (TPB) as a registered tax agent, or operating under one. The QS fee is fully tax-deductible in the year you pay it, but only if the firm is a registered tax agent or works under one. The major firms (BMT, Washington Brown, Depreciator, Deppro) all meet both bars. Smaller QS firms sometimes do not. Ask before you engage.

We have a long-standing referral relationship with Depreciator. Their schedules start at $440 with no inspection required for properties where they can work from documentation, or $715 inclusive of an inspection. Our clients can book directly through that link.

Prime cost vs diminishing value: the choice your QS report will offer

A residential schedule will typically present both calculation methods so your accountant can pick the one that suits you. Prime cost spreads the deduction evenly across the asset’s effective life. Diminishing value front-loads the deduction.

For most investors planning to hold for 5 to 10 years, diminishing value is the better choice because it gets cash flowing earlier in the holding period. But the choice matters less than people think. Both methods deduct the same total amount over the asset’s life. Only the timing differs.

This article explains depreciation conceptually, but the schedule itself must be prepared by a qualified quantity surveyor (preferably AIQS-registered and a registered tax agent). What you read here is not a substitute for a QS report.

Depreciation × negative gearing: the combined annual deduction worked out

Depreciation does not just reduce your rental income. It feeds into the negative gearing calculation, and that is where the real after-tax leverage lives.

How depreciation increases your negative gearing loss without changing cash position

Negative gearing happens when your total rental property expenses exceed your gross rental income. The shortfall is a tax loss you can offset against your other income (employment, business, dividends).

Depreciation counts as an expense for that calculation, but it does not cost you any cash. So adding depreciation to the expense pile increases the negative gearing loss on paper without changing what you actually spend or earn day-to-day.

Worked example: $35,000 loss without depreciation, $52,000 with

A $600,000 investment property with an 80% LVR loan at 6.4% interest looks like this in a typical year:

- Gross rent: $32,000

- Interest: $30,720

- Council, water, insurance, property management, repairs: $7,500

- Cash expenses total: $38,220

- Cash shortfall (negative cash flow): $6,220

That cash shortfall is the negative cash position. Now layer in $17,000 of depreciation on a new build:

- Total deductible expenses: $38,220 + $17,000 = $55,220

- Less gross rent: $32,000

- Tax loss: $23,220

The tax loss is what you offset against your other income. The cash shortfall is what comes out of your bank account. The depreciation moves the tax loss above the cash shortfall by exactly the depreciation amount.

After-tax savings at 30%, 37%, and 45% marginal rates

The cash benefit depends on your marginal rate. At each of the three brackets most investors fall into:

| Marginal rate | $20,000 of extra deduction returns | $17,000 deduction returns |

|---|---|---|

| 30% (income $45,001 to $135,000) | $6,000 | $5,100 |

| 37% (income $135,001 to $190,000) | $7,400 | $6,290 |

| 45% (income above $190,000) | $9,000 | $7,650 |

Australian individual tax brackets reflect rates effective from 1 July 2024 following the Stage 3 tax cuts. Source: ATO, Individual income tax rates.

Higher-income investors benefit more from depreciation per dollar of deduction. That is why depreciation is one of the levers that disproportionately favours investors already at the 37% or 45% bracket. For a deeper dive on how the negative gearing maths interacts with capital growth strategy, see our investment property loans guide.

What this means at tax time

A few practical points your accountant will deal with, but worth knowing.

Where depreciation goes on your return

Depreciation flows through the rental property schedule on your individual tax return. Capital works deductions go in one line. Plant and equipment deductions go in another. Your accountant transcribes the figures from the QS schedule.

The QS fee is itself tax-deductible

The fee you pay the quantity surveyor is fully deductible in the year you pay it. It does not get capitalised into the property’s cost base. A $600 schedule fee at a 37% marginal rate has an after-tax cost of $378.

Capital gains tax cost-base reduction at sale

Here is the catch most investors do not see until they sell. Capital works deductions claimed under Division 43 reduce the property’s CGT cost base on disposal, per s110-45 of the Income Tax Assessment Act 1997. If you have claimed $50,000 in Division 43 over 10 years and you sell with a $200,000 gross capital gain over your original cost, the gain calculation lifts to $250,000. After the 50% CGT discount on a 12-month-plus holding, the taxable gain becomes $125,000.

Plant and equipment deductions claimed under Division 40 do not reduce the property’s cost base. They are handled separately as a balancing adjustment when each asset is disposed of.

The CGT clawback feels like a sting, but the maths almost always still favours claiming. You deduct at your marginal rate (30% to 45%) during the holding period. You pay back at the discounted CGT rate (15% to 22.5% effective after the 50% discount). The time value of money also works in your favour: dollars saved today are worth more than dollars taxed in 10 years. Across most realistic holding periods, depreciation produces a net positive tax outcome even after the cost-base impact.

For a full picture, our investment property capital gains tax guide covers the CGT side.

What to do this week if you’ve never had a depreciation schedule

If you own an investment property and have never commissioned a depreciation schedule, here is the four-step checklist.

- Commission a schedule. Use an AIQS-registered quantity surveyor who is also a registered tax agent. Depreciator starts at $440 with no inspection required, where documentation allows; BMT and Washington Brown sit higher at $700 to $770 with full inspection. Our clients can book through the Depreciator link above.

- Lodge the deduction in this year’s return and amend prior years where possible. The ATO’s 2-year amendment window (4 years for some taxpayers) means most investors can recover 2 years of missed deductions plus the current year. Talk to your accountant about which years are open.

- Review the schedule alongside your overall tax position. Your accountant takes the schedule and lodges the deduction. Your broker takes the tax return and reads it for borrowing capacity. The two roles connect at the tax-return line, not at the depreciation line. If you are also self-employed, that is where the business-level depreciation add-back becomes a real conversation.

- Refinance or apply for the next investment loan with the right lender choice in mind. Don’t go to your existing bank by default. The 52+ lender panel we have access to includes lenders with different rental-income shading rates, different stress-rate buffers, and different policies on existing investment debt. The right lender for property #2 may not be the lender on property #1.

Mortgage brokers in Australia operate under the Best Interests Duty (ASIC RG 273, in force from 1 January 2021). That means we are legally required to recommend the loan and lender that best suits your circumstances, not the lender that pays us best. For property investors, that obligation cuts straight to the lender choice for the next loan.

Book a free 15-minute investor strategy call, and we’ll walk you through where your current lender sits on rental-income shading and stress-rate policy, and what your borrowing capacity looks like for the next purchase.

Frequently asked questions

What is depreciation on an investment property?

Depreciation is a non-cash tax deduction that recognises the wear and tear of the building (Division 43 capital works) and the assets inside it (Division 40 plant and equipment). You don’t pay it like you pay interest or council rates. You just claim it on your tax return, which reduces your taxable rental income and your overall tax bill.

What is the depreciation rate for an investment property?

Buildings depreciate at 2.5% per year for 40 years if construction commenced on or after 15 September 1987. That is the Division 43 capital works deduction. Plant and equipment items inside the property (carpet, hot water systems, ovens, dishwashers, air conditioning) depreciate over their ATO-set effective lives, typically 8 to 12 years for residential rental items under TR 2022/1.

How much depreciation can I claim on my investment property?

First-year deductions of $12,000 to $18,000 are typical for a new-build $600,000 investment property. Established properties built after 15 September 1987 commonly produce $5,000 to $10,000 in capital works deductions per year. The exact figure depends on the property’s age, construction cost, and the plant and equipment included.

Is a depreciation schedule worth it for my investment property?

Almost always, yes. A residential schedule costs $440 to $770 from the major firms, and the fee is fully tax-deductible in the year you pay it. A first-year deduction of $15,000 at a 37% marginal rate returns $5,550 in cash, which is several times what the schedule cost. The schedule lasts the life of the property and only needs updating after renovations.

Can I claim depreciation on a second-hand investment property?

If you exchanged contracts after 7:30 PM AEST on 9 May 2017, you can no longer claim Division 40 deductions on second-hand plant and equipment that was already in the property. You can still claim Division 43 capital works on the building if construction commenced after 15 September 1987, plus any new plant and equipment you purchase yourself once you own it.

How does depreciation affect my borrowing capacity?

Investment property depreciation does not reduce your borrowing capacity. Most lenders calculate rental income for serviceability using gross rent shaded by 70% to 80% to allow for vacancy and expenses. Depreciation is a non-cash deduction that affects your taxable income on paper but does not enter the lender’s rental income calculation. The depreciation add-back that some lenders do apply is on self-employed business income (vehicles, plant, equipment in your own trading entity), not on the investment property’s depreciation schedule.

What does a quantity surveyor cost?

A residential schedule typically costs $440 to $770 from the major firms, with entry-level providers advertising from around $300. The fee is fully tax-deductible in the year you pay it, so the after-tax cost at a 37% marginal rate is closer to $277 to $485. BMT and Washington Brown typically sit at the top of the range. Depreciator and Deppro sit lower.

Can I do a depreciation schedule myself?

Only if your property was built before 1985 and you have full historical construction-cost records. Otherwise no. The ATO requires the construction-cost estimate to come from a “suitably qualified person”, which in practice means an AIQS-registered quantity surveyor who is also a registered tax agent or works under one.

Does claiming depreciation increase my CGT bill when I sell?

Capital works deductions you claim under Division 43 reduce the property’s CGT cost base on sale, so you do pay some of it back. Plant and equipment deductions under Division 40 do not reduce the cost base. They are handled separately as a balancing adjustment when the asset is disposed of. Even after the cost-base reduction, the net tax position is almost always still positive once the CGT discount and the time value of money are factored in.

This article contains general information only and does not constitute financial advice. Your personal financial situation, objectives and needs have not been considered. Before acting on any information, you should consider its appropriateness to your circumstances. Speak to a qualified mortgage broker for advice tailored to your situation. Mortgage World Australia Pty Ltd is a credit representative (CR No. 396946) of Mortgage Specialists Pty Ltd (Australian Credit Licence No. 387025).

Depreciation rules and personal tax outcomes depend on your circumstances. The information here is general and is not tax advice. Speak to a registered tax agent or accountant before lodging.

Tax rates, scheme parameters, and quantity surveyor fee ranges in this article are current as at May 2026 and based on Tax Ruling TR 2022/1 (effective lives), Treasury Laws Amendment (Housing Tax Integrity) Act 2017, and ATO published guidance.

Patrick is a Director and a Home Loan Specialist. He has been helping Australians with home loans since 2001. Prior to working as a mortgage broker Patrick was employed by Macquarie Bank for 3 years and also worked as an accountant for a publicly listed company. Patrick’s qualifications include:

Bachelor of Business, UTS Sydney. Majored in accounting and sub-majored in Finance and Marketing.

Diploma of Finance and Mortgage Broking Management FNS50310

Certificate IV in Financial Services (Finance/Mortgage Broking) FNS40804

Ready to Take the Next Step?

Whether you’re looking to buy your first home, refinance, or explore investment opportunities, Mortgage World Australia is here to help.

Fill out the contact form below, and one of our expert mortgage brokers will be in touch shortly to discuss your needs and guide you through your options.

Get Started Today!