NSW Land Tax 2026: Thresholds, Rates & Investor Guide

NSW Land Tax: A Complete Guide for Investors and Homeowners

On this page ▾

- What is land tax in NSW?

- NSW land tax thresholds and rates for 2026

- How is land tax calculated in NSW?

- Who pays land tax in NSW?

- Land tax exemptions and concessions

- When land tax changes the maths on a property purchase

- Ownership structures and land tax planning

- Your annual land tax assessment notice

- How land tax fits a broader investment plan

- Frequently asked questions

Most investors discover NSW land tax when the first assessment notice arrives. By then, the bill is locked in. We have spent 25 years walking clients through how the tax works, why a second property can trigger thousands in ongoing cost the first never did, and how ownership structure can shift the figure by tens of thousands across a portfolio. This guide covers the 2026 thresholds, the calculation, the exemptions, and the broker view of when land tax should change the call on whether you buy at all.

Threshold figures in this article are effective from 1 January 2025, frozen for the 2026 tax year, sourced from Revenue NSW.

What is land tax in NSW?

Land tax is an annual state tax charged by Revenue NSW on the unimproved value of taxable land you own at midnight on 31 December each year. It is not a tax on the building, and it does not apply to every property. It is a tax on land value above a yearly tax-free threshold, set under the Land Tax Management Act 1956 with rates set by the Land Tax Act 1956.

If your combined NSW land value sits below the general threshold of $1,075,000, you owe nothing. Above that, you owe a small fixed amount plus a percentage of the excess. The system mainly captures investors, second-home owners, and corporate or trust holdings, while leaving most owner-occupied homes untouched through the principal place of residence exemption.

Does NSW have land tax?

Yes. NSW has charged an annual land tax under the Land Tax Management Act 1956 for almost seventy years. It is not the same as the wound-back NSW Property Tax that briefly ran under the First Home Buyer Choice scheme, and it is not a council rate. Anyone holding investment, holiday, second-home, or commercial property in NSW can be liable each year their combined holdings exceed the threshold.

How land tax differs from council rates and stamp duty

Three property taxes confuse new investors:

- Transfer duty (formerly stamp duty) is a one-off duty paid when you buy. First home buyers can sometimes reduce or remove it through a stamp duty exemption NSW or other stamp duty concessions for first home buyers.

- Council rates are charged annually by your local council on every property regardless of land value elsewhere.

- Land tax is charged annually by Revenue NSW on your combined NSW land holdings above the threshold. Your home is exempt; investment properties usually are not.

You can owe all three, and investors regularly do.

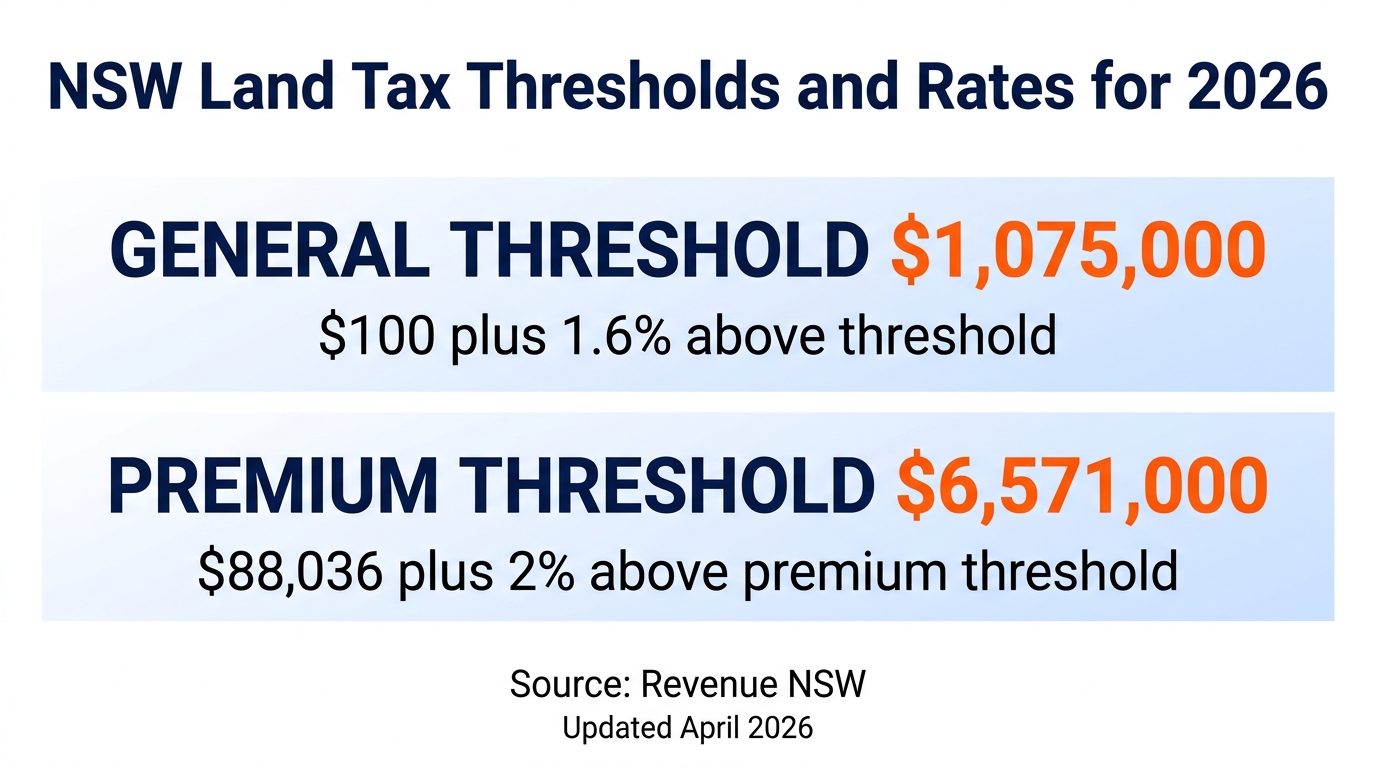

NSW land tax thresholds and rates for 2026

The 2026 land tax year uses the thresholds and rates that took effect from 1 January 2025. The 2024-25 NSW State Budget froze the general and premium rate thresholds for land tax years after 2024, so the figures below apply to the 31 December 2025 taxing date that determines 2026 liabilities.

| Threshold | Land value | Tax payable |

|---|---|---|

| Below general threshold | Up to $1,075,000 | $0 |

| General rate band | $1,075,001 to $6,571,000 | $100 + 1.6% of value above $1,075,000 |

| Premium rate band | Above $6,571,000 | $88,036 + 2% of value above $6,571,000 |

General threshold ($1,075,000) and the threshold freeze

The general threshold has been fixed at $1,075,000 since the 2025 land tax year. Because Revenue NSW averages your land values over three years, owners whose properties have grown in value are now drifting into the threshold without buying anything new. The freeze means there is no automatic indexation pulling the threshold up to compensate. This is the single biggest reason investor land tax bills are climbing: rising 3-year-average land values pushed against a static threshold.

Premium threshold ($6,571,000) and the 2% rate

Above $6,571,000 of combined land value, the premium rate kicks in: $88,036 plus 2% on every dollar over $6,571,000. We see this hit clients with multi-property portfolios, large rural holdings, or single high-value Hills District or Northern Beaches sites where the land value alone runs into the millions. The 2% rate is small per dollar but stacks up fast across a portfolio.

Surcharge land tax for foreign owners

Foreign owners of residential land in NSW pay an additional 5% surcharge land tax on top of any regular land tax owed. The surcharge applies from the 2025 land tax year onwards, replacing the 4% rate that applied during 2023 and 2024. There is no tax-free threshold for surcharge land tax, and there is no pro-rating: if the property is residential and the owner meets the foreign person definition at midnight on 31 December, the full surcharge applies.

A foreign owner of a $2,000,000 residential investment property would pay regular land tax of $14,900 plus surcharge land tax of $100,000, for a combined annual cost of $114,900. NSW does not have a separate “absentee owner” surcharge (that concept exists in Victoria, not NSW). The operative test in NSW is whether the owner is a foreign person under the Surcharge Land Tax provisions of the Land Tax Act 1956.

How is land tax calculated in NSW?

Revenue NSW takes the unimproved land value of every taxable property you own at midnight on 31 December, sums those values, subtracts the threshold, applies the rate, and issues an assessment notice in the following months. Tax is charged for the full year following the taxing date, so there is no pro-rating for properties bought or sold partway through the year.

The general-threshold formula with worked example

The formula in the general rate band is simple:

Land tax = $100 + 1.6% x (combined land value – $1,075,000)

Worked example: a Parramatta investment property with an unimproved land value of $1,500,000 (purchase price approximately $1,900,000):

- Excess over threshold: $1,500,000 – $1,075,000 = $425,000

- Tax on excess: $425,000 x 1.6% = $6,800

- Add fixed component: $6,800 + $100 = $6,900 per year

That is $133 per week the property must clear in surplus rent before it earns its first dollar for the investor. On a $1,900,000 purchase generating a 4% gross yield ($76,000 per year), land tax alone consumes about 9% of gross rent before any other holding cost.

The premium-threshold formula with worked example

In the premium band, the formula is:

Land tax = $88,036 + 2% x (combined land value – $6,571,000)

For combined land value of $7,000,000: ($7,000,000 – $6,571,000) x 2% + $88,036 = $96,616 per year. The fixed $88,036 component is the bracket-creep penalty for crossing the premium threshold; the 2% rate then applies only to the dollars above $6,571,000.

What is the unimproved land value, and how is it set?

Land tax is based on the unimproved land value, not the price you paid for the property and not its current market value. The NSW Valuer General sets each property’s land value as at 1 July each year. Revenue NSW then takes the average of the most recent three Valuer General valuations and uses that 3-year average as the assessed land value for the upcoming taxing date.

The 3-year averaging smooths single-year valuation jumps, but it also means your land tax bill keeps climbing for two more years after the market cools. Investors are often blindsided by this lag. The land value can be objected to within 60 days of the Valuer General’s notice, and we recommend doing so when valuations look out of line with the data-driven property investing comparables for the area.

Who pays land tax in NSW?

Most homeowners pay nothing. The principal place of residence exemption removes the family home from the assessed value entirely. Land tax mainly catches:

- Investors with one or more rental properties whose combined NSW land values exceed $1,075,000

- Owners of holiday homes, second homes, or vacant land

- Trusts, companies, and SMSFs holding NSW property

- Foreign persons holding residential land in NSW (subject to surcharge land tax)

- Joint owners whose combined holdings push them past the threshold

Investors, developers, and second-home owners

If you own one investment property in a Sydney suburb where the land value is below the threshold, you may pay no land tax. Buy a second one. Add the two land values together. If the combined figure is above $1,075,000, the entire excess is taxed.

This is the trap we walk most second-property investors through. We see it most often with clients buying second properties in Parramatta and Blacktown, where individual land values run $600,000 to $900,000 each. One property: nil land tax. Two properties: a four-figure annual bill. The second purchase needs to clear that ongoing cost on top of every other holding expense to stay cash-flow viable.

Trusts, companies, and SMSFs – different rules

Holding property through a trust or company changes the calculation, sometimes for the worse:

- Special trusts (most discretionary trusts and unitised trusts that fail the fixed trust definition) get no threshold. They pay land tax at 1.6% on every dollar of land value up to the premium threshold, then 2% above. A discretionary trust holding a single $700,000 land-value property still pays $11,200 a year, where an individual would pay nothing.

- Fixed trusts that meet the strict Revenue NSW definition can pass the threshold through to their unit holders.

- Companies are assessed at the standard rates and get one threshold per company. Related companies are grouped and share one threshold across the group.

- Complying SMSFs get the standard threshold under the same rules as individuals. Non-complying funds are treated as special trusts.

If you are weighing structures, get specific advice before you buy: how to structure your investment property ownership and which lender accepts the structure are the two questions that decide whether the strategy actually works. For SMSF home loans, the choice between bare trust structures and direct holdings interacts with land tax treatment and lender appetite differently. For more on this, see our SMSF property loans and lender panel guide.

Joint owners and the secondary deduction

Buying jointly with a spouse, sibling, or parent does not give you two thresholds. It gives you one. Revenue NSW treats joint owners as a single entity (the “primary taxpayer”) and applies one threshold to the jointly held land. Each individual owner is then reassessed on their share of the joint property plus any property they own solely, with a deduction calculated to prevent double-counting.

Net result: joint ownership rarely creates a second threshold; it just shifts where the liability sits. The only way to access additional thresholds is through separate, unrelated ownership structures, and the running costs often exceed the saving.

Land tax exemptions and concessions

The exemption regime keeps most homeowners out of the tax entirely. It is also where strategic property structuring can lawfully reduce a portfolio’s exposure.

Principal place of residence (your own home)

Your principal place of residence (PPR) is exempt from land tax. To qualify, the property must be your home and you must have continuously used and occupied it solely for residential purposes since 1 July before the relevant taxing date. A strata-titled apartment qualifies as a PPR.

Important 2026 change: from the 2026 land tax year onwards, the resident claiming the PPR exemption must hold a total ownership interest of at least 25% in the property. This matters for anyone in a fragmented-ownership arrangement, for example where one spouse holds 90% and the other 10% but only the 10% owner lives there. If the resident’s ownership share falls below 25%, the PPR exemption no longer applies and the land becomes taxable.

For rentvesting guide clients, the PPR exemption does not cover the investment property because nobody using the exemption is living in it. The investment is taxable from day one.

Primary production land

Land used dominantly for primary production with a profit-making purpose is exempt. The dominant-use test is strict; occasional grazing or hobby farming is unlikely to qualify. Genuine farming operations, including some peri-urban properties around the Hills District and outer western Sydney, can satisfy the test where the income, intent, and land use line up.

Build-to-rent (50% reduction)

Eligible build-to-rent (BTR) properties receive a 50% reduction in land value for land tax purposes (not a 50% reduction in tax payable, though the effect is similar). To qualify, the parcel must contain at least 50 self-contained dwellings used specifically for BTR, and construction must have commenced after 1 July 2020. The Land Tax (Build-to-rent Concessions) Amendment Act 2025, which received assent on 23 September 2025, established a new ongoing scheme with no time limit alongside the existing time-limited concession.

Charities, boarding houses, retirement villages

Other exemptions cover charities, boarding houses, aged care facilities, retirement villages, childcare services, caravan parks, and qualifying non-profit organisations, each with its own eligibility test under the Land Tax Management Act 1956.

When land tax changes the maths on a property purchase

Most land tax explainers stop at the formula. The broker view goes further. Land tax is a cost that should sit alongside loan repayments, rates, and management fees in the buy-or-don’t-buy call on the next property.

Worked example: a $1.5M Parramatta investment property

Take the $1,500,000 land-value Parramatta property from the calculation example above. The annual land tax is $6,900, or $133 per week. Over ten years, with no inflation, that is $69,000 of pre-tax holding cost from land tax alone. Refinancing to release equity from this property to fund a third purchase requires the rental yield to absorb the land tax and the new debt service together. We walk clients through this calculation with residential investment loans so the numbers are transparent before settlement, not after the first assessment lands.

Worked example: two properties pushing past the threshold

Two properties whose individual land values sit just below the threshold but whose combined value crosses it:

- Property 1: $700,000 land value

- Property 2: $600,000 land value

- Combined: $1,300,000

Pre-second-property: zero land tax. Each property is below $1,075,000 individually.

Post-second-property: ($1,300,000 – $1,075,000) x 1.6% + $100 = $3,700 per year.

The second property triggers a $3,700 ongoing cost the first one never carried. Until that purchase, the investor was inside the no-tax band. After it, every year of holding costs the portfolio nearly $4,000 in land tax. We use the borrowing power calculator and a manual cash-flow check to see whether the second purchase can absorb that hit while remaining serviceable.

Cash-flow impact and the rental-yield trade-off

Land tax belongs in the yield calculation alongside council rates. A property generating $30,000 in net rent before land tax becomes a $26,300 net property after a $3,700 bill. That is a meaningful haircut. Picking the best suburbs for investment property means treating land value as a separate variable from purchase price: land value drives land tax, purchase price drives stamp duty and loan size. Two properties with identical yields can have materially different long-run costs once land tax enters the equation.

Ownership structures and land tax planning

Structure choice is the most powerful lever investors have on land tax across a multi-property portfolio. It is also the most expensive lever to operate, so the saving has to be material to justify the structure.

Why a unit trust or company can change your liability

A fixed unit trust that meets Revenue NSW’s strict definition can pass the land tax threshold through to its unit holders. Done correctly, this preserves a threshold inside a structure that would otherwise be a special trust with none. Done incorrectly, the deed fails the test and the structure is taxed as a special trust at 1.6% on every dollar with no threshold. Legal cost matters; lender appetite for trust-held property varies sharply.

Company ownership has trade-offs the other way: a company gets one threshold (not multiple), and related companies are grouped under one threshold. For commercial investment loans where the asset sits inside a corporate structure for liability or tax reasons, the land tax treatment is part of the holding-cost analysis from day one.

Joint ownership versus tenants in common

Both joint tenants and tenants in common are treated as joint owners for NSW land tax purposes. The TIC versus joint tenants distinction matters for estate planning and stamp duty, not for the land tax assessment. The temptation to split ownership between family members to access two thresholds usually fails the Revenue NSW grouping rules.

When SMSF property is taxed differently

A complying SMSF gets the standard threshold under the same rules as an individual. The land tax treatment is one factor among several in deciding whether buying property with SMSF is worthwhile. Lender appetite for SMSF-held property is narrower than for individuals or trusts, so the structure, the lender, and the land tax position all need to align before you commit.

Your annual land tax assessment notice

Revenue NSW issues land tax assessment notices each year covering the liability calculated as at the previous 31 December taxing date.

When notices arrive (January-April issuing window)

Revenue NSW starts sending assessment notices from January each year, with most NSW investors receiving theirs over the first few months of the year. The notice shows the combined land value, the threshold applied, the tax payable, and the due date. Many investors only realise they owe land tax when this notice lands.

60-day payment terms and payment plans

You have 60 days from the date you receive the notice to pay in full and receive an early-payment discount, or to set up an interest-free payment plan within that window. Outside the 60-day window, payment plans may still be available but interest applies. You can pay through Land Tax Online or via the standard Revenue NSW payment options listed on the notice.

What to do if you didn’t receive an assessment

If you suspect you should have received a notice but didn’t, contact Revenue NSW directly. You can also retrieve a copy of any prior assessment via Land Tax Online. Penalties may apply where Revenue NSW investigates undisclosed liabilities, so if you have bought into the threshold band and the notice has not arrived, follow up rather than wait.

How land tax fits a broader investment plan

Land tax is one cost in a portfolio strategy that also includes serviceability, equity, refinancing, and tax deductibility. Looking at it in isolation usually leads to the wrong call.

Why a broker reviews land tax alongside borrowing capacity

A bank’s serviceability calculation does not always factor in your full land tax liability when assessing the next purchase. We do. The cost of holding the existing portfolio, including the land tax bill the next property will trigger, changes how banks assess borrowing capacity for the deal in front of you. Buying a property that pushes the combined holdings into a higher land tax band may erode serviceability for the property after that. Modelling the next two purchases together, not just the next one, is how we plan portfolio growth at MWA.

Refinancing and equity-release implications

When investors use your existing equity to buy an investment property, the land tax position of the new property changes the breakeven calculation. So does refinancing the existing portfolio onto a structure that handles the new land tax bill more efficiently. We help clients weigh whether to refinance your home loan or restructure investment debt around the land tax liability before adding another asset. The right move is rarely “buy now and sort the structure later” once the threshold has been crossed. The broader investment loans guide ties land tax into the wider serviceability and structuring picture.

Frequently asked questions

How much is land tax in NSW?

NSW land tax is $100 plus 1.6% of the combined unimproved land value above the general threshold of $1,075,000, up to the premium threshold of $6,571,000. Above $6,571,000, the rate is $88,036 plus 2% of the value above the premium threshold. A combined land value of $1,500,000 produces an annual liability of $6,900. Threshold figures are effective from 1 January 2025 and frozen for the 2026 tax year, sourced from Revenue NSW.

Do you pay land tax on apartments in NSW?

Yes, but only on your share of the apartment’s land value, not on the building. Each strata-titled lot is allocated a portion of the underlying land value based on its unit entitlement. As with any property, you pay land tax only when your combined NSW holdings exceed the general threshold of $1,075,000 after the principal place of residence exemption is applied. An apartment used as your home is exempt; an investment apartment counts toward the threshold.

Do you pay land tax on your own home in NSW?

Generally no. The principal place of residence exemption removes your home from the assessed land value, provided you have occupied the property continuously since at least 1 July before the taxing date. From the 2026 land tax year onwards, the resident claiming the exemption must also hold at least 25% ownership in the property.

Has the NSW land tax threshold changed for 2026?

No. The general threshold has been frozen at $1,075,000 since the 2025 land tax year, and the premium threshold has been frozen at $6,571,000. The 2024-25 NSW Budget removed the annual indexation of land tax thresholds, so neither figure is scheduled to move for 2026 unless legislation changes.

What happens if I don’t pay my NSW land tax?

Revenue NSW charges interest on overdue amounts and can pursue enforcement action including garnishee orders or property registration charges. Payment plans are available if you contact Revenue NSW within the 60-day notice period. Ignoring an assessment is the most expensive option; engaging early to set up a payment plan is the cheapest.

Can I claim land tax as a tax deduction?

Yes, when the land tax is incurred on a property used to produce rental income. The Australian Taxation Office treats land tax as a deductible holding cost for residential rental property, deductible in the income year the liability relates to (not the year you pay it). Land tax on your principal place of residence is not deductible. This is general information only; speak to your tax adviser for advice on your specific situation.

Patrick O’Brien, Director and Home Loan Specialist since 2001

This article contains general information only and does not constitute financial advice. Your personal financial situation, objectives and needs have not been considered. Before acting on any information, you should consider its appropriateness to your circumstances. Speak to a qualified mortgage broker for advice tailored to your situation. Mortgage World Australia Pty Ltd is a credit representative (CR No. 396946) of Mortgage Specialists Pty Ltd (Australian Credit Licence No. 387025).

Patrick is a Director and a Home Loan Specialist. He has been helping Australians with home loans since 2001. Prior to working as a mortgage broker Patrick was employed by Macquarie Bank for 3 years and also worked as an accountant for a publicly listed company. Patrick’s qualifications include:

Bachelor of Business, UTS Sydney. Majored in accounting and sub-majored in Finance and Marketing.

Diploma of Finance and Mortgage Broking Management FNS50310

Certificate IV in Financial Services (Finance/Mortgage Broking) FNS40804

Ready to Take the Next Step?

Whether you’re looking to buy your first home, refinance, or explore investment opportunities, Mortgage World Australia is here to help.

Fill out the contact form below, and one of our expert mortgage brokers will be in touch shortly to discuss your needs and guide you through your options.

Get Started Today!