House and Land Package Financing NSW: A Broker’s Guide

House and Land Package Financing in NSW: A Broker’s Guide

On this page ▾

- What is a house and land package?

- How financing actually works (the two-loan structure)

- NSW stamp duty on house and land packages: the land-only saving

- Government schemes for NSW house and land buyers (2026)

- How much deposit do you need?

- Hidden costs most buyers miss

- Are house and land packages worth it? Pros, cons and risks

- Step-by-step: applying for a house and land package loan in NSW

- FAQ: house and land package financing in NSW

Most buyers walk into a house and land package thinking it is one transaction. It is not. A typical NSW house and land package involves two contracts, two loans, and a financing structure that looks nothing like buying an established home. Done well, it can save you money on stamp duty, open up grants that established homes cannot access, and let you lock in a fixed-price build at today’s prices. Done poorly, the layered financing, builder approval lists, and cash-flow impact of progress payments catch buyers off-guard at the worst moments.

This is the broker view of how house and land package financing in NSW works in 2026, what the schemes are worth, and where the structure quietly trips people up.

What is a house and land package?

A house and land package is a vacant block of land paired with a fixed-price building contract for a home to be built on it. You end up with both, but you usually buy them in two separate steps. Most NSW packages sit in greenfield estates in Western Sydney (Box Hill, Leppington, Marsden Park), the Macarthur growth corridor, the Hunter, and the Central Coast. Some are on smaller infill blocks closer to the city.

Turnkey vs two-contract packages: the structural difference

There are two main structures. The difference matters more than most buyers realise.

In a two-contract structure, you sign one contract for the land and a separate contract for the build. The land settles in your name first. You then start construction with the builder under the second contract. Stamp duty is paid only on the land at land settlement. This is the most common NSW house and land package structure.

In a turnkey package, you sign a single contract with a developer for a completed home delivered ready to move in. The builder typically retains title to the land during construction, and title transfers to you at handover. Stamp duty is calculated on the full purchase price (land plus build) at that point. Turnkey packages are common with larger developers and off-the-plan estates.

The structure changes how stamp duty, the First Home Owner Grant, and your deposit timing work. We unpack each below.

How financing actually works (the two-loan structure)

Forget the “one mortgage” mental model. A two-contract NSW house and land package is funded by two separate loan products that work together: a land loan and a construction loan. (For the full mechanics of a construction home loan, we have a dedicated guide. The summary below is what you need to plan a house and land package.)

Stage 1: the land loan

The land loan funds the land contract. It looks like a standard home loan, but some lenders want to see a building contract or strong evidence of intent to build, because vacant land is harder to value and harder to sell if things go wrong. Some lenders will only fund land with an immediate construction commitment.

Settle the land and then sit on it for a few months, and you are paying principal and interest on a block of dirt while still renting elsewhere. That is real cash out the door. Plan the build start to closely follow land settlement. We have written separately on getting a mortgage on recently registered land, which is a common scenario in new estates where titles are registered late.

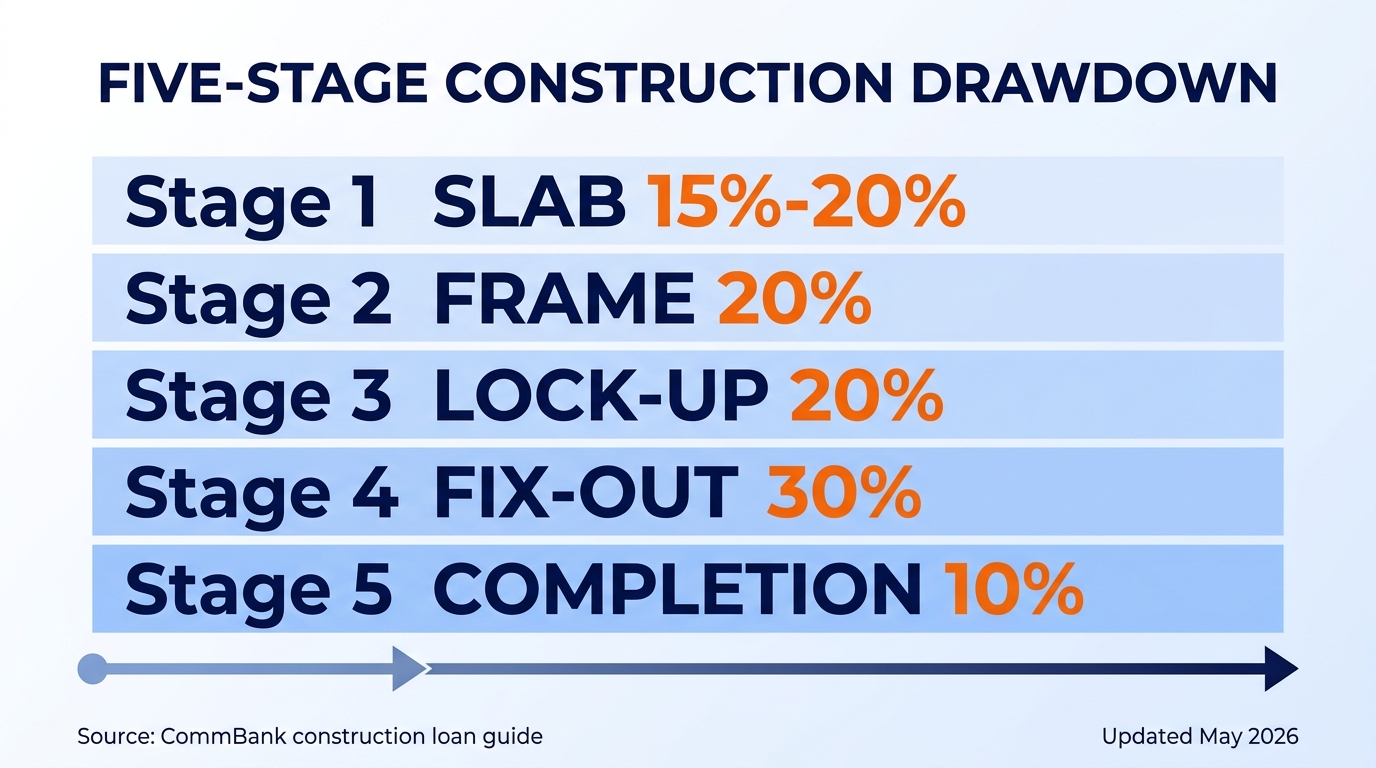

Stage 2: the construction loan and progress payments

The construction loan funds the build. It does not get drawn down in one lump. It gets drawn in five stages tied to the build’s physical progress, with the lender ordering a valuation or inspection before each release. CommBank’s published breakdown is representative of how the big four release funds:

- Slab (foundation poured): about 15% to 20%

- Frame (walls and structures up): about 20%

- Lock-up (windows, doors, roofing): about 20%

- Fix-out (internal fittings and fixtures): about 30%

- Practical completion (final detailing, fencing, clean-up): about 10%

You only pay interest on what has been drawn, not on the full approved limit. So early in the build, your repayments are small. By lock-up, they are noticeable. By fix-out, they are biting. The lender bills interest-only during construction, monthly, on the running drawn balance.

How repayments change from interest-only to P&I after handover

Once the final progress payment lands, the loan switches to whatever repayment type you chose at origination, usually principal-and-interest over a 30-year term that effectively starts at handover. Two things happen at the same time: the full loan balance becomes the basis for repayments, and the contracted term begins. That is the moment the package “feels” like a normal mortgage.

The single biggest budgeting mistake we see is forecasting the post-handover P&I figure off the early-stage interest-only payments. They are not the same number, and the gap can be hundreds of dollars a week.

NSW stamp duty on house and land packages: the land-only saving

In a two-contract NSW house and land package, transfer duty (the official name for NSW stamp duty) is paid only on the land contract. The building contract is a service contract for construction, and is not subject to transfer duty. This is the structural saving most buyers have heard about, and it is the main reason two-contract packages are popular.

In a turnkey (single-contract) package, duty is calculated on the full purchase price of the completed home. There is no land-only saving in that structure.

To check whether you qualify for any concessions, our NSW stamp duty exemption explainer walks through the eligibility tests in detail.

Worked example: transfer duty on a $750,000 NSW package

Take a $750,000 two-contract package: $400,000 land, $350,000 build. Transfer duty figures are based on rates effective 1 July 2025, sourced from Revenue NSW.

Standard transfer duty on the $400,000 land contract is $12,412. The build contract is not duty-bearing. Total duty: $12,412.

If the same buyer paid $750,000 for an established home (or a turnkey package), standard transfer duty would be $28,162. The land-only structure saves a non-first-home-buyer $15,750 in duty on this package size.

For a quick check on your own scenario, the NSW stamp duty calculator will give you a ballpark.

First home buyer transfer duty concessions in NSW

If you are a first home buyer, the maths flips. The NSW First Home Buyers Assistance Scheme (FHBAS) has two tiers, and they apply different thresholds depending on what you are buying.

For new and existing homes, FHBAS gives a full exemption up to $800,000 and a concessional rate from $800,000 to $1,000,000. For vacant land, the full exemption stops at $350,000, and the concession ends at $450,000.

What this means in practice: a first home buyer purchasing a $750,000 turnkey new build pays $0 transfer duty under FHBAS. A first home buyer signing a two-contract package with $400,000 land and a $350,000 build pays a concessional duty on the $400,000 land contract, because $400,000 is in the $350k-$450k vacant-land taper band. That is more than the turnkey FHB pays in duty, even though the package totals the same dollar amount.

Brokers do not say this loudly enough: for first home buyers in the $600k-$1m price band, the turnkey route can be cheaper on duty than the two-contract route, because FHBAS treats the whole purchase as a “new home”. For non-first-home buyers, a two-contract house and land package is almost always cheaper. Our first home buyer stamp duty concession page has the full FHBAS rules and qualifying criteria.

Government schemes for NSW house and land buyers (2026)

Three federal and state schemes are worth knowing about. They can stack with FHBAS if you qualify, and they directly change how big a deposit you need. Our first home buyer home loans hub covers eligibility for each in more depth.

The Australian Government 5% Deposit Scheme (renamed October 2025)

What used to be called the First Home Guarantee was renamed the Australian Government 5% Deposit Scheme on 1 October 2025, and the rules were widened at the same time. Income caps were removed. Place limits were removed. There is no Lenders Mortgage Insurance, because the government acts as guarantor for the gap between your 5% deposit and a standard 20% LVR.

For NSW house and land packages, the Sydney metro and regional centre price cap is $1,500,000, and the rest-of-state cap is $800,000. For separate-contracts packages, the cap applies to the total of the land price plus the build cost, not just the land contract. A $700,000 land + $500,000 build is fine in Sydney; a $900,000 land + $700,000 build is over the cap.

The scheme can only be applied for through a participating lender as part of a home loan application, not directly with Housing Australia. We have been writing these loans since the original First Home Guarantee era, and the application process is the same now under the new name. Our standalone guide on how to buy a home with a 5% deposit has the full mechanics.

First Home Owner Grant (FHOG) for new builds in NSW

The NSW FHOG is $10,000 for first home buyers building or buying their first new home. The trap with FHOG on house and land packages: there are two different price caps depending on the structure.

For a newly built complete home (turnkey), the cap is $600,000. For vacant land plus a comprehensive home building contract (the two-contract structure), the cap is $750,000. At a $750,000 package price, the two-contract route stays inside the FHOG cap. The same $750,000 as a turnkey is over the $600,000 newly-built cap and is ineligible.

Good luck finding a house and land package for $750,000 in Sydney, though!

This is why structuring matters at the upper end of the FHOG band. We have lost grants for buyers because the contract structure was wrong, not because the price was wrong. Eligibility otherwise requires Australian citizenship or PR status (one applicant), age 18+, no prior home ownership before 1 July 2000, and a 12-month minimum residence after handover.

Help to Buy: shared-equity option

Help to Buy is a separate federal scheme. The government takes an equity share of up to 30% for an existing home or 40% for a new build, in exchange for a 2% minimum deposit. NSW caps are $1,300,000 Sydney and regional centres, $800,000 rest of the state. Unlike the 5% Deposit Scheme, Help to Buy still has income caps: $100,000 for singles, $160,000 for couples or single parents. Places are limited to 10,000 a year.

For a new-build house and land package within the price caps and income caps, Help to Buy gives the deepest deposit relief, but you give up an equity share in your home. For most working buyers, the 5% Deposit Scheme works out cheaper over a typical hold period because there is no equity given up.

How much deposit do you need?

Without any scheme, the standard maths applies: 20% to avoid Lenders Mortgage Insurance, or 5% to 10% with LMI. For a $750,000 package, that is $150,000 saved or $37,500 to $75,000 with LMI added on top of the loan.

With the 5% Deposit Scheme: $37,500 on a $750,000 package, no LMI. With Help to Buy: $15,000 minimum deposit, no LMI, but the government takes an equity share. Genuine savings (your money, not gifted or borrowed) are required by every lender we work with, with most wanting to see at least 5% as genuine and seasoned for three months.

A quick way to test what your numbers actually look like: our borrowing power calculator will give you a realistic ceiling. For a deeper read on deposit timing and structure, how much deposit you need to purchase property covers the trade-offs.

One non-obvious point: lenders apply different serviceability buffers. The big four use APRA’s 3 % buffer on top of the actual rate when assessing whether you can service the loan. Some non-bank lenders apply 1-2%. On a $700,000 loan, that gap can mean $50,000 to $80,000 of extra borrowing capacity. This is a key reason brokers often place house and land deals outside the big four.

Hidden costs most buyers miss

Builder fixed prices are usually fixed for the contracted inclusions only. The line items that drift include site costs (slope, soil, retaining), connections (water, sewer, power, NBN, gas if applicable), driveway and landscaping, fencing, window coverings, flyscreens, letterbox, clothesline, and council compliance fees. On Box Hill and Marsden Park deals we have settled in the last 18 months, $25,000 to $60,000 of “post-contract” cost is the normal range when the buyer thought everything was included.

There is also council Section 7.11 contributions in some LGAs, the BASIX certificate cost, the home owner’s warranty insurance, and progress-inspection valuation fees from the lender. None of these is huge individually, but they aggregate fast.

The biggest cash-flow miss: paying rent while the build is running. If you are renting at $700 a week and the build runs 11 months, that is $33,000 of holding cost that does not show up anywhere in the contract. Always model that in.

Are house and land packages worth it? Pros, cons and risks

Pros: lower stamp duty in two-contract structures, eligibility for FHOG and FHBAS-vacant-land concessions, fixed-price build at today’s pricing, brand-new home with full builder warranty, depreciation upside if it is an investment.

Cons: long settlement timelines (10 to 18 months from start to handover is typical), exposure to builder solvency risk, variation cost creep, holding costs while building, and the cash-flow shape of interest-only-into-P&I that catches first-time builders.

Risks worth naming directly: builder insolvency mid-build, settlement delays where land titles register later than expected, valuation shortfalls at lock-up or completion (rare but happens), and post-handover defects where the builder is slow to respond.

What banks won’t tell you about builder approval lists

Every lender has a list of builders they will and will not lend against. Some lists are public; most are not. Sign with a builder who is not on your lender’s panel, and you may have to switch lenders to get the construction loan funded. We have had to do this mid-deal more than once. The cleanest path: choose your lender first, get builder approval confirmed, then sign the building contract.

The other thing banks do not flag: many lenders will not fund certain builder structures, like staged-payment schedules that are too front-loaded, or contracts where the builder owns the land at handover (a turnkey concern). Our piece on the 3 pitfalls with construction loans covers the contract-level traps in detail.

Step-by-step: applying for a house and land package loan in NSW

The fastest, cleanest order:

- Get pre-approval from a lender that fits your scenario (scheme eligibility, builder panel match, serviceability buffer). This is where a broker saves you from redoing applications.

- Choose the land and the builder. Confirm the builder is on your lender’s approved panel before signing anything.

- Sign the land contract, then the building contract. Apply for FHBAS, FHOG, and any federal scheme through your lender.

- Settle the land. Land loan starts. Lodge for FHOG at first drawdown (typically the slab stage) per your lender’s process and Revenue NSW timing.

- Construction begins. Lender releases progress payments at slab, frame, lock-up, fix-out, and practical completion. Interest-only billed monthly on the drawn balance.

- Practical completion and handover. Final progress payment lands, loan converts to P&I.

Our companion guide house and land package loan advice for fast approval has the lender-by-lender approval timing if you want to compare.

FAQ: house and land package financing in NSW

How do house and land package repayments work?

During construction, you pay interest-only each month on the running drawn balance, not on the full approved limit. Repayments start small (after the slab draw is taken) and grow as more of the loan is released at frame, lock-up, fix-out, and completion. After the final progress payment, the loan converts to your chosen repayment type (usually principal-and-interest) over a 30-year term that effectively starts at handover.

What are the risks of house and land packages?

The main risks are builder insolvency mid-build, settlement and title-registration delays in greenfield estates, cost variations beyond the fixed-price contract, valuation shortfalls at progress payment stages, and the cash-flow shock when interest-only repayments convert to principal-and-interest at handover. Choosing a lender with a strong builder panel and a buffer in your budget for variations and rent during the build mitigates most of them.

Do you have to pay stamp duty on house and land packages in NSW?

In a two-contract structure (the typical NSW arrangement), transfer duty is paid only on the land contract, not the building contract. On a $750,000 package split as $400,000 land and $350,000 build, that is $12,412 in duty under the rate table effective 1 July 2025. In a turnkey single-contract package, duty is calculated on the full purchase price ($28,162 on a $750,000 turnkey). First home buyers may pay zero duty under FHBAS, depending on the structure and price.

What are the benefits of buying a house and land package?

Lower stamp duty in two-contract structures (land-only valuation), eligibility for the $10,000 NSW First Home Owner Grant on new builds (with structure-specific price caps), access to the 5% Deposit Scheme up to $1.5m in Sydney with no LMI, fixed-price build pricing locked in at signing, brand-new home with full builder warranty, and depreciation upside for investors. The trade-off is a longer settlement timeline and more layered financing than buying an established home.

How long do house and land packages take to build?

Typical NSW build times run 9 to 14 months from slab to handover, with another 3 to 6 months between land settlement and slab in newer estates where titles register late. Plan on 12 to 18 months from contract signing to keys in hand. Lock in temporary accommodation for at least that period, and budget for it.

What is the catch with house and land packages?

The catch is usually one of three things: site cost overruns and post-contract variations the builder did not include in the headline price, builder approval issues with your lender, or cash-flow stress from holding costs (rent, interest-only payments, lender fees) over the 12-to-18-month build period. None of them are deal-breakers if you go in eyes-open and structure the financing properly.

This article contains general information only and does not constitute financial advice. Your personal financial situation, objectives and needs have not been considered. Before acting on any information, you should consider its appropriateness to your circumstances. Speak to a qualified mortgage broker for advice tailored to your situation. Mortgage World Australia Pty Ltd is a credit representative (CR No. 396946) of Mortgage Specialists Pty Ltd (Australian Credit Licence No. 387025).

Patrick is a Director and a Home Loan Specialist. He has been helping Australians with home loans since 2001. Prior to working as a mortgage broker Patrick was employed by Macquarie Bank for 3 years and also worked as an accountant for a publicly listed company. Patrick’s qualifications include:

Bachelor of Business, UTS Sydney. Majored in accounting and sub-majored in Finance and Marketing.

Diploma of Finance and Mortgage Broking Management FNS50310

Certificate IV in Financial Services (Finance/Mortgage Broking) FNS40804

Ready to Take the Next Step?

Whether you’re looking to buy your first home, refinance, or explore investment opportunities, Mortgage World Australia is here to help.

Fill out the contact form below, and one of our expert mortgage brokers will be in touch shortly to discuss your needs and guide you through your options.

Get Started Today!