Buying a Second Home with Equity: How It Works in Australia

Buying a Second Home with Equity: How It Works in Australia

On this page ▾

- How does equity work when buying a second home?

- How much usable equity do you have?

- Three ways to access your equity

- Second home vs investment property: what changes for the loan

- Cross-collateralisation vs separate security

- Worked example: using $250,000 of equity to buy a $700,000 holiday home

- NSW considerations: stamp duty, land tax and PPR

- Risks and what most homeowners get wrong

- Frequently asked questions

By Patrick O’Brien, Director and Home Loan Specialist since 2001

Australian property prices have risen sharply through the 2024-2026 cycle, and many homeowners are sitting on more equity than they realise. If you bought five or ten years ago and your mortgage has been ticking down while values have climbed, that gap is the lever that lets you move into a second home without saving a fresh deposit. Whether you’re upgrading into a bigger house, buying a holiday home on the coast, or setting up a place for adult children, the mechanics are the same: you turn paper equity into a usable deposit and the bank funds the rest.

The catch is that the structure matters. Most existing-bank top-ups are simple, but they aren’t always the cheapest way to do this, and they can lock you into an arrangement that costs you flexibility later. This guide explains how the equity calculation works, the three ways to access it, and the choices that separate a clean second-home purchase from one you regret.

This article is for an existing homeowner buying a second residence: a holiday home, family home, or upgrade. If you’re using equity to buy a rental, the path is broadly similar but the loan product, tax treatment, and rate tier differ. See our companion guide on how to use equity to buy an investment property.

How does equity work when buying a second home?

Equity is the difference between your home’s current market value and your outstanding loan balance. When you buy a second home using equity, you draw on that gap to fund the deposit and purchase costs of the new property, and the bank lends you the rest as a separate loan against the second property (or a top-up on the first). How an equity loan works follows the same mechanic in any equity-release scenario.

The lever sits on two numbers: your home’s value, and what banks are willing to lend against it. Most lenders cap the combined position at 80% of your home’s current value, which means a portion of your total equity stays “locked” as a buffer. The amount you can actually pull out is your usable equity, and that number is materially smaller than the total equity figure most homeowners have in their head.

How much usable equity do you have?

Usable equity is the amount a lender will let you draw against your home today. It is not the same as your total equity, and confusing the two is the most common starting-point mistake. Three steps:

- Get a current valuation of your home (a real-estate agent estimate is fine for planning; the bank will order a formal valuation when you apply).

- Subtract your outstanding loan balance.

- The result is your total equity, but only a portion is usable.

For a quick check before talking to a broker, our LVR calculator will run the numbers in seconds.

The 80% LVR rule (and the 90% exception)

Banks cap usable equity at 80% of the property’s value because that’s the threshold above which Lenders Mortgage Insurance (LMI) is triggered. Above 80% LVR, your loan needs LMI to protect the lender against default risk. Below 80%, no LMI. Most second-home buyers want to stay below the LMI threshold to keep costs clean. What your LVR means explains the calculation in full.

The 90% exception: some lenders will let you borrow up to 90% of your home’s value to release equity, accepting LMI on the top-up portion. This is useful if you’re equity-rich but cash-tight on the deposit and the LMI premium is worth paying for the access. We can model both paths and we have access to LMI-waiver products through select lenders.

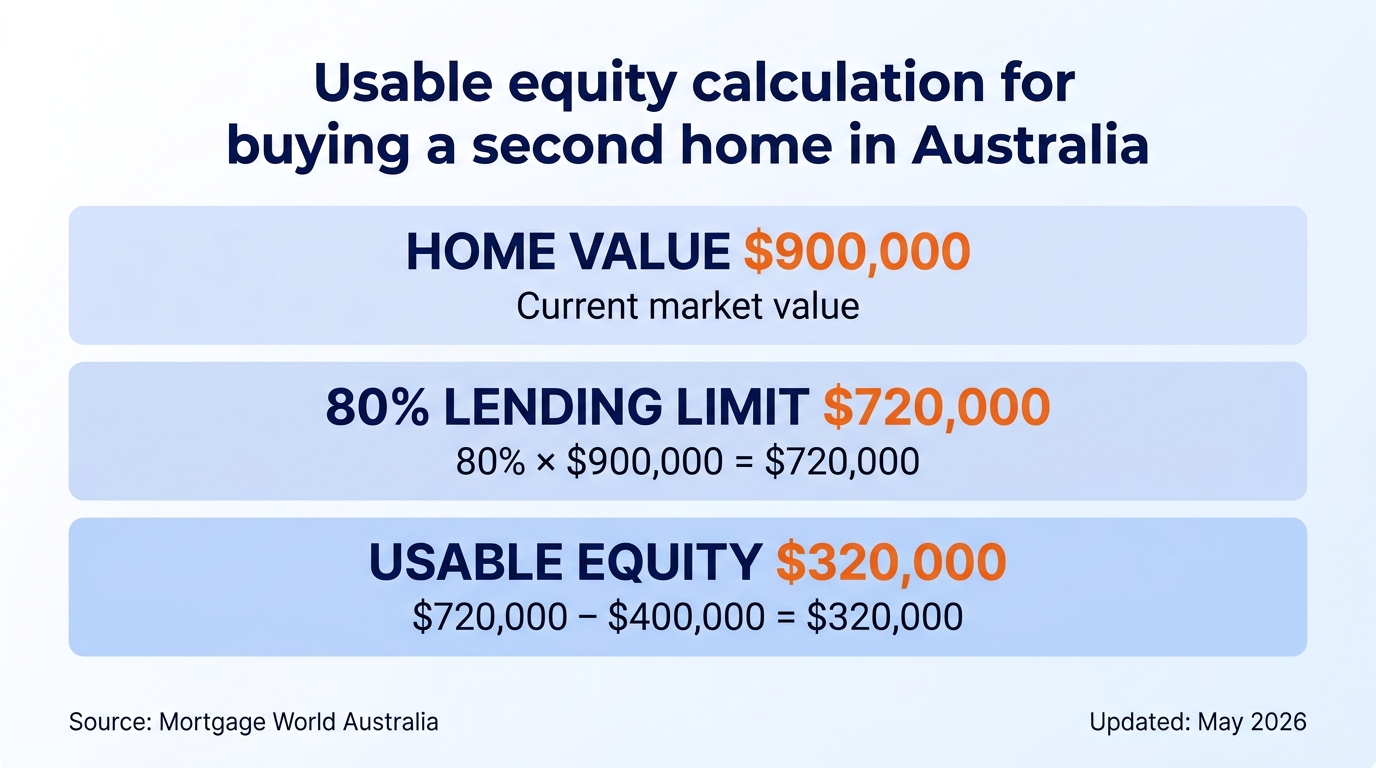

Worked example: $900,000 home, $400,000 loan

- Current market value: $900,000

- Outstanding loan: $400,000

- Total equity: $900,000 − $400,000 = $500,000

- 80% of value: 80% × $900,000 = $720,000

- Usable equity: $720,000 − $400,000 = $320,000

That $320,000 is what you can use as the deposit (and to cover stamp duty and fees) on the second purchase. Total equity says $500,000, but only $320,000 is accessible without crossing the LMI line.

Three ways to access your equity

There are three structures lenders use to release equity for a second property. They look similar on the surface, but they behave differently in cost, complexity, and what they let you do later.

| Structure | Cost / complexity | Best when |

|---|---|---|

| Refinance and top up | Low cost if staying with same lender; medium if changing | Simple second purchase, single-lender comfort, want streamlined repayments |

| Separate (split) loan | Medium cost; cleaner accounting | Second property has different rate tier or you want flexibility to refinance one loan independently |

| Line of credit or redraw | Variable; often higher headline rate | Drawing in tranches (renovation plus deposit), need flexible access |

Refinance and top up the existing loan

You go back to your current lender, or refinance your home loan to a new one, increase the loan against your existing home, and use the cash to fund the second-home deposit and costs. This is the path most banks will offer first. It’s simple, and if you stay with the same lender, the paperwork is light.

The tradeoff: you end up with a single loan that funded two properties. If you ever want to refinance one and not the other, you have to unwind the structure first.

Set up a separate (split) loan against the equity

Instead of topping up the existing loan, you set up a second loan facility against the equity in your home, with its own rate, term, and repayment schedule. The original loan stays as it is. The second loan funds the deposit and costs on the new property, and a third loan funds the balance secured against the second property.

This is often the cleaner structure. Each loan tracks its own purpose, which matters for tax and for future flexibility. It also lets you put the second-property loan with a different lender if their pricing is better for that rate tier, which is something we look at across our 52+ lender panel before recommending the structure.

Line of credit or redraw

A line of credit (LOC) or redraw on your existing loan gives you flexible access to the equity over time. Useful if you’re drawing in stages (a renovation tranche before the second-home deposit, for example). The downside is the headline rate on a dedicated LOC product is typically higher than a standard variable home loan, and lenders have moved away from offering pure LOCs in recent years. Redraw on a standard loan is usually cheaper, but the funds need to be redrawn before you commit to the second purchase.

Second home vs investment property: what changes for the loan

This is where most online guides oversimplify. A second home you live in part-time (holiday home, family home, weekender) is a different animal from an investment property you rent out, and the loan, rate, and tax treatment all shift.

Lender categorisation, rate tiers, and LMI thresholds

Under APRA’s tightened definition of an owner-occupier loan, most lenders classify a second home that is not your primary residence as investment for rate-tier purposes, even if you don’t rent it out. Investment rates are typically 0.20% to 0.40% above owner-occupier rates, which on a $450,000 new loan adds roughly $900 to $1,800 a year in interest.

Lender policy varies. A small number of lenders will treat a holiday home that isn’t rented as owner-occupied, which can save you tens of thousands across the life of the loan. This is exactly the type of policy nuance that benefits from a broker drawing across multiple lenders rather than a homeowner walking into their existing bank and accepting the first offer. LMI rules apply the same way on either path: above 80% LVR triggers LMI, and investment-loan LMI premiums are typically 10% to 20% higher than owner-occupier premiums at the same LVR. See avoid paying LMI for the structures that keep you below the threshold, and LMI waivers for professional-borrower exemptions.

Tax treatment of the interest (deductible vs not)

The deductibility rule follows the use of the funds, not the security. Per ATO Taxation Ruling TR 2000/2, where you draw equity from your home to buy a second property, the interest on the drawn portion is deductible only if the second property is genuinely income-producing. A holiday home you keep for personal use does not produce assessable income, so the interest is not deductible. An investment property that is rented or genuinely available for rent does, so the interest is deductible.

This is the most-confused point in the cluster. The fact that the equity comes from your home does not change the answer. What matters is what the second property is used for.

Cross-collateralisation vs separate security

When a single lender holds security over both properties, that’s cross-collateralisation. It looks tidy on paper because everything sits with one bank, but it removes flexibility you usually want to keep.

Why most brokers recommend keeping properties separate

Five reasons cross-collateralisation usually makes the borrower worse off:

- Sale of one property triggers a revaluation of the remaining security, and the lender may require part of the loan to be paid down before releasing the title.

- Refinancing one property to a different lender is blocked until the cross-collat structure is unwound, which is fiddly and time-consuming.

- A drop in one property’s value can reduce your accessible equity on the other, even when the second property’s value is unchanged.

- All your loans concentrated with one lender removes any leverage to negotiate or move. The lender knows you’re locked in.

- The bank benefits from the structure; you don’t. Stand-alone security against each property gives you the same access to funds with materially more flexibility.

Cross-collateralisation explained walks through this in more depth with worked examples. The default position we take across our client book is stand-alone security on each property, unless there’s a specific reason to do otherwise.

Worked example: using $250,000 of equity to buy a $700,000 holiday home

Putting it together. Your existing home is worth $900,000 with a $400,000 loan, so you have $320,000 in usable equity. You’re buying a $700,000 holiday home on the NSW coast.

| Item | Amount |

|---|---|

| Purchase price | $700,000 |

| NSW transfer duty (stamp duty) | $25,912 |

| Conveyancing, registration, transfer fees | approx $2,000 |

| Loan establishment / valuation fees | approx $800 |

| Total to fund | approx $728,712 |

| Equity drawn from existing home (deposit + costs) | $278,712 |

| New loan secured against the holiday home | $450,000 |

The $450,000 new loan is 64% LVR on the $700,000 second property, comfortably under the 80% LMI threshold. The $278,712 of equity drawn is below the $320,000 usable-equity ceiling on the existing home. No LMI on either loan.

At an indicative variable investment-property rate of 6.49% over 30 years, the $450,000 loan repays at approximately $2,840 a month (rates indicative as at May 2026; comparison rate 6.51% based on a secured loan of $150,000 over 25 years; WARNING: comparison rate is true only for the example given. Confirm current rates with a broker). Run your own loan amount, rate, and term through our loan repayment calculator to estimate the new repayment for your structure.

Transfer duty figures are based on rates effective 1 July 2025, sourced from Revenue NSW.

NSW considerations: stamp duty, land tax and PPR

NSW-specific rules change the maths on a second home in ways that catch people out.

Stamp duty on the second purchase (rates effective 1 July 2025)

A $700,000 purchase falls in the $372,000 to $1,240,000 transfer-duty band. Duty payable: $11,152 base, plus $4.50 for every $100 above $372,000, totalling $25,912. First-home buyer concessions don’t apply because you already own a home, but stamp duty concessions for first home buyers is the right resource if you’re helping a child or sibling work out their numbers.

Principal place of residence (PPR) exemption when you own two homes

You can only claim one PPR exemption worldwide per family for NSW land tax purposes. A holiday home or family home that isn’t your principal residence is subject to land tax once your aggregate non-exempt land value crosses $1,075,000 (2026 land tax year, frozen at this level by the 2024-2025 NSW State Budget). The rate is $100 plus 1.6% of the land value above the threshold.

There’s a transitional concession if you buy a new PPR between 1 July and 31 December and still own the previous home on 31 December: both homes can be exempt for that single land tax year. The concession runs for one year only.

The practical implication: a holiday home with a low land value may not trigger land tax in isolation, but any other NSW land you own (a second investment, a vacant block, a share in family land) counts toward the threshold.

Risks and what most homeowners get wrong

The mechanics are straightforward; the misunderstandings are predictable.

- “Total equity equals usable equity.” No. The 80% LVR rule reserves a buffer. Plan from the usable figure.

- “The interest is deductible because the loan is secured against my home.” No. Deductibility follows the use of funds. Holiday home equals not deductible. Investment property equals deductible.

- “A holiday home gets owner-occupier rates.” Usually not. Most lenders treat a non-PPR second home as investment. Some don’t. Check before you commit to a lender.

- “Cross-collat is fine because it’s all one bank.” It removes flexibility you’ll want later when you sell, refinance, or restructure.

- “Serviceability is the same everywhere.” APRA-regulated banks stress-test at 3 percentage points above the loan rate. Many non-bank lenders apply 1% to 2% buffers. Borrowing capacity isn’t a fixed number; it depends on which lender does the maths.

Borrowing capacity for a second property is calculated on net surplus, which is your income, less living expenses, less servicing on existing debt at the stress-test rate. It is not a multiple of income. This is where a broker who knows lender policy across the panel matters: at the same household profile, you can pass at one lender and fail at another.

Frequently asked questions

How does equity work when buying another house? You draw the difference between your home’s current value and your outstanding loan, capped at 80% of the value, and use it as the deposit and costs on the second purchase. The bank lends the balance against the second property, leaving you with two loans (or one combined loan if the structure isn’t split).

How much equity do you need to buy a second home? Enough to cover the deposit (typically 20% of the second property’s price), plus stamp duty, conveyancing, and fees. On a $700,000 purchase in NSW, that’s roughly $170,000 to $180,000. Drawing more is possible if you accept LMI above 80% LVR.

How much equity can I use to buy a second home? Up to your usable-equity figure: 80% of your home’s current value, minus your outstanding loan. On a $900,000 home with a $400,000 loan, that’s $320,000.

How much equity do you need for a second mortgage? “Second mortgage” in Australian usage usually means a second loan secured against the same property, not a loan to buy a second home. The equity you need is similar: enough to cover the new loan amount plus costs, while keeping combined LVR under 80% if you want to avoid LMI.

Is it worth using equity to buy a second home? For most existing homeowners with $250,000-plus in usable equity, yes, because you avoid the multi-year saving cycle for a fresh deposit. The structure choice (top-up vs split loan vs different lender) is where the value of the decision sits. Get the structure right and you save tens of thousands across the life of both loans.

What’s the broker advantage on a second-home loan? Lender policy varies on owner-occupier classification, investment loadings, LMI premiums, and serviceability buffers. Across our 52+ lender panel, we identify which lender suits your structure and your cash position, rather than accepting your existing bank’s first offer. See our steps to buying a home for the full second-purchase process.

Ready to use the equity in your home? Speak to one of our mortgage brokers at Mortgage World Australia. Since 2001, we’ve helped Australian homeowners structure second-property purchases across upgraders, holiday homes, family homes, and investment property paths.

This article contains general information only and does not constitute financial advice. Your personal financial situation, objectives and needs have not been considered. Before acting on any information, you should consider its appropriateness to your circumstances. Speak to a qualified mortgage broker for advice tailored to your situation. Mortgage World Australia Pty Ltd is a credit representative (CR No. 396946) of Mortgage Specialists Pty Ltd (Australian Credit Licence No. 387025).

Patrick is a Director and a Home Loan Specialist. He has been helping Australians with home loans since 2001. Prior to working as a mortgage broker Patrick was employed by Macquarie Bank for 3 years and also worked as an accountant for a publicly listed company. Patrick’s qualifications include:

Bachelor of Business, UTS Sydney. Majored in accounting and sub-majored in Finance and Marketing.

Diploma of Finance and Mortgage Broking Management FNS50310

Certificate IV in Financial Services (Finance/Mortgage Broking) FNS40804

Ready to Take the Next Step?

Whether you’re looking to buy your first home, refinance, or explore investment opportunities, Mortgage World Australia is here to help.

Fill out the contact form below, and one of our expert mortgage brokers will be in touch shortly to discuss your needs and guide you through your options.

Get Started Today!