Home Loan on Maternity Leave: 2026 Lender Guide

Getting a home loan while on maternity leave: what really works in 2026

On this page ▾

- Yes, you can get a home loan while on maternity leave

- What income lenders will count while you’re on leave

- How lenders calculate the savings buffer you’ll need

- Two approaches lenders take to maternity leave applications

- Repayment pause vs new loan: these are two different things

- What you’ll need to provide: the document checklist

- Worked examples: three Sydney scenarios

- Common mistakes that get applications declined

- What banks won’t tell you (the broker view)

- Frequently asked questions

- Talk to a broker who’s done this before

Most banks won’t tell you this clearly: whether you get approved for a home loan while on maternity leave depends almost entirely on which lender’s policy you apply under. Some count your full back-to-work salary the day you submit. Others will only consider your reduced income during the leave period. A few have published parental leave policies. Most don’t, which means the answer your bank gives you isn’t the answer the market gives you.

I’ve placed many of these loans over my 25 years as a broker. Here’s how they work in 2026, what each major Australian lender does (and doesn’t) make public, what documents you need, and the mistakes that get applications declined.

Yes, you can get a home loan while on maternity leave

The short answer: yes, and it’s been getting easier. Lenders are more flexible about counting future return-to-work income than they were a decade ago. The legal framework supports lending to applicants on parental leave: pregnancy and parental leave are protected attributes under section 22 of the Sex Discrimination Act 1984 (Cth), which makes it unlawful to refuse a financial service because someone is pregnant or on maternity leave.

What lenders are required to do, under section 130 of the National Consumer Credit Protection Act 2009, is verify that you can afford the loan repayments throughout the loan term, including during periods of reduced income. That’s why a return-to-work letter is the central document in this kind of application. The bank isn’t gatekeeping; it’s meeting its responsible-lending obligation.

Whether your application succeeds is then a question of two things: your specific financial position, and which lender’s credit policy you apply under.

What income lenders will count while you’re on leave

A few income streams can come into play during maternity leave. Lenders treat them differently:

Return-to-work salary. This is the key variable. The lender wants a letter from your employer confirming your exact return-to-work date, the hours and days you’ll be working, and the gross income you’ll be earning when you return. A vague letter (“Jane is on parental leave and will return at some point”) won’t cut it. The letter has to be specific.

Employer-paid parental leave. Some employers pay full or part-salary during your leave. Bank statements showing those deposits, plus a copy of your employer’s parental leave policy, can support your application.

Government Parental Leave Pay. Services Australia pays $948.10 per week (before tax) at the National Minimum Wage rate. Until 30 June 2026 the scheme provides up to 24 weeks (120 days) of payment. From 1 July 2026 it expands to 26 weeks (130 days). Income tests apply: $180,007 individual or $373,094 family. The payment is taxable. Lender treatment of this income varies. Some lenders accept it as supplementary income, some discount it, some exclude it from serviceability calculations because it’s a finite period rather than ongoing income. This is one of the areas where broker knowledge matters most.

Holiday pay or long-service leave. Some applicants front-load annual leave or long-service leave to bridge the unpaid portion of their parental leave. Lenders treat this as ordinary salary income while it’s being paid.

Partner’s income. Your partner’s permanent income is the other half of the serviceability picture. In dual-income households, a partner on full salary often shoulders most of the serviceability calculation during the leave period.

Rental income from existing property. If you already own an investment property, the rental income is added in (typically at 75 to 80 per cent of gross rent to allow for vacancy and costs).

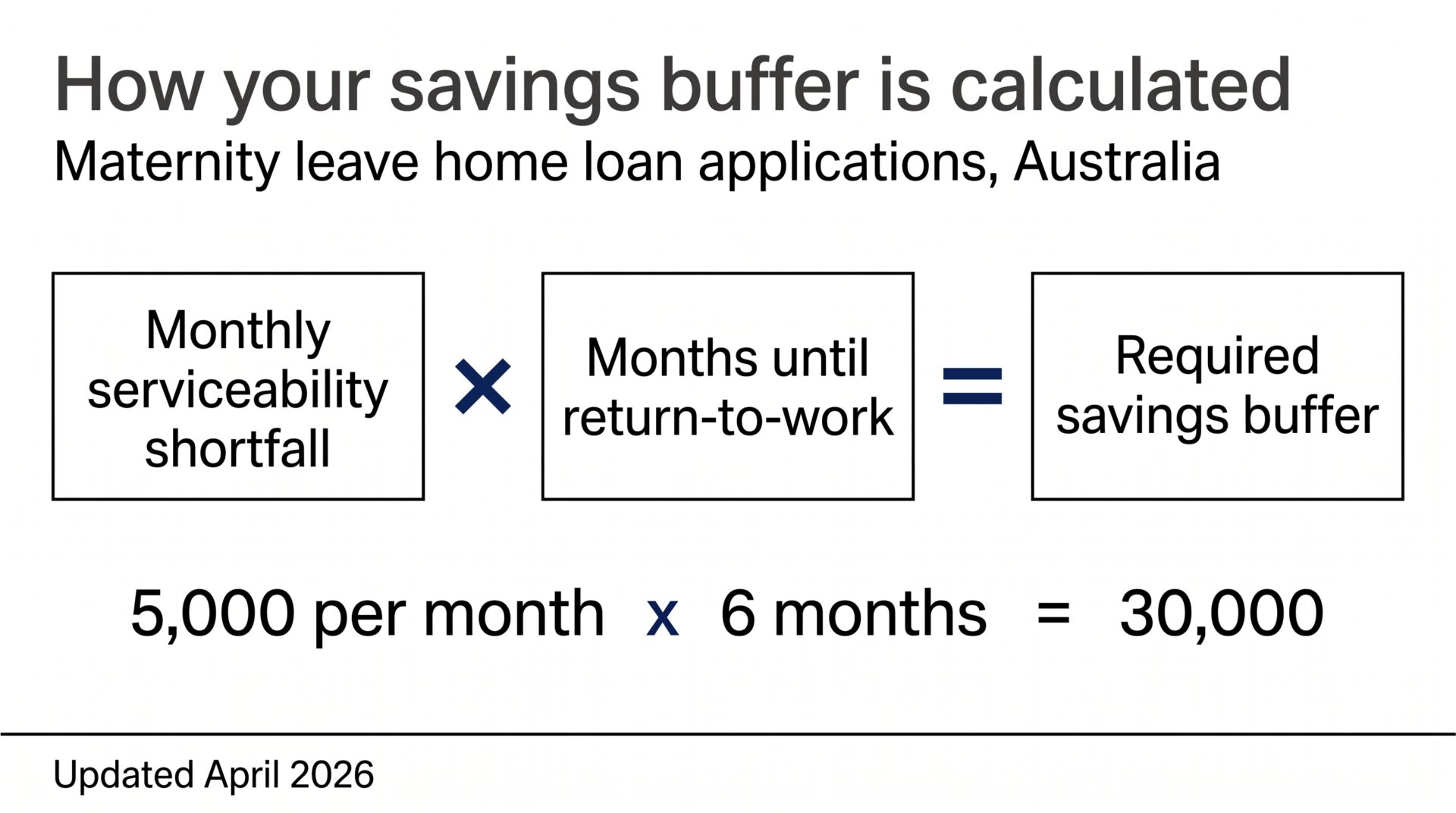

How lenders calculate the savings buffer you’ll need

Even when a lender accepts your return-to-work income, you almost always still have to show savings to cover the period before you return. Here’s what’s actually happening behind the scenes.

When the lender assesses your application, they run two serviceability calculations:

- With your return-to-work income included. This confirms the household will qualify for the loan amount you’re requesting once you’re back at work.

- Without your return-to-work income included. This calculates how much short of full serviceability you’ll be each month while you’re still on leave.

The gap between calculation 1 and calculation 2 is your monthly serviceability shortfall. The lender then multiplies that monthly shortfall by the number of months remaining in your leave period at settlement to work out how much surplus savings you need to hold.

A worked example

Say the monthly shortfall comes out at $5,000, and there are 6 months left between settlement and your return-to-work date. The lender will want you to evidence $30,000 in surplus savings ($5,000 × 6 months), held separately from any funds being used for the deposit, stamp duty and purchase costs. Held in your name, in a savings account, before the application is submitted.

Some lenders allow you to substitute part of that buffer with confirmed in-leave income, typically employer-paid parental leave, government Parental Leave Pay, or holiday and long-service leave being paid out across the gap. So, if in the same example, you’ll receive $2,000 a month in employer-paid parental leave for those 6 months, the buffer requirement may drop from $30,000 to $18,000 (the $5,000 monthly shortfall less $2,000 of confirmed in-leave income, multiplied by 6 months). Other lenders require the full buffer in cash regardless of in-leave income. The treatment varies by lender, and that policy variation is part of why placement matters.

A few practical points:

- The buffer sits on top of your deposit and costs. It can’t be the same money you’re using to settle.

- Joint applicants can’t double-count income. If both partners’ incomes are used to calculate the loan amount, your partner’s income is already fully allocated to repayments. It can’t also be used to “cover” your shortfall during leave. That’s an industry-wide principle, not a single-lender rule.

- The shorter the gap to return-to-work, the smaller the buffer. Settling close to your return date can materially reduce the savings you need to hold.

Two approaches lenders take to maternity leave applications

Australian lenders fall into two broad camps on how they assess maternity leave applications. Knowing which camp you’re applying under is half the work.

Approach 1: Use your return-to-work income from day one

This is the most common approach. The lender accepts that you’re going to be earning your return-to-work income shortly and uses that figure for the serviceability calculation up front. The savings buffer math from the previous section is what bridges the gap between application and return.

Westpac is the only major Australian bank that publicly states this approach on its consumer website. Westpac’s parental leave page confirms it recognises paid parental leave and back-to-work income on new home loan applications. Other lenders take a similar approach, but their rules sit inside broker-channel credit guidelines rather than on a customer-facing page. That’s where a broker’s value lives: matching your file to the credit policy that actually accepts it.

Approach 2: Use the income you’re actually receiving during leave

Some lenders take a different position. Rather than relying on the return-to-work salary, they’ll use the income you’re currently receiving during the leave period, typically a combination of:

- Employer-paid parental leave, where applicable

- Government Parental Leave Pay (Centrelink, currently $948.10 per week before tax for up to 24 weeks, rising to 26 weeks from 1 July 2026)

- Annual leave or long-service leave being paid out across the leave period

These lenders often discount or limit the in-leave income, commonly using 75 per cent of gross payments, sometimes capped at the equivalent of the return-to-work salary, and may add their own conditions. For example: a maximum total leave period (often 12 months), a requirement that the borrower can show how repayments will be met for any unpaid portion of leave, or a ceiling on LVR.

The advantage of Approach 2 is that it can suit applicants with shorter leave periods, well-funded employer parental leave schemes, or applicants whose return-to-work plans aren’t fully locked in. The trade-off is that the income figures are usually lower than the return-to-work figure, so the loan amount is smaller.

Which one applies to you depends on the lender, not the bank you walk into

You usually can’t tell which approach a given lender uses from their consumer website. Most banks don’t publish their new-loan serviceability rules for maternity leave at all; those rules live in the broker credit policy. The right approach for your file is the one that lets you borrow the amount you need, on terms that work, given your actual circumstances. That’s the placement question a broker is paid to answer.

Repayment pause vs new loan: these are two different things

Most parental leave information published by banks covers what an existing customer can do with an existing home loan: pause repayments, reduce them by half, dip into a redraw facility. Westpac’s parental leave reduction, NAB’s repayment holiday, RAMS’s parental leave option, and CommBank’s repayment holiday all sit in this category.

That’s a useful product if you already have a home loan with that bank and you’re going on parental leave. It’s not what you need if you don’t have a loan yet and you’re trying to get approved.

A new loan during maternity leave is a credit decision about future serviceability. A repayment pause on an existing loan is a relief feature on a contract you already hold. Don’t confuse them in conversations with banks. If a lender’s parental leave page only describes the second one, ask specifically about the new-loan approval policy, or get a broker to do it for you.

What you’ll need to provide: the document checklist

For lenders that use return-to-work income (Approach 1), the standard package is:

- Your last two payslips before going on leave. This establishes your pre-leave income.

- Your most recent payslip, if you’re still receiving employer-paid parental leave at the time of application. This confirms the current income flow.

- A letter from your employer confirming the exact return-to-work date, whether you’re returning full-time or part-time, and your exact return-to-work income. The letter has to be specific. Vague language (“Jane will return at some point”) gets pushed back. The letter should be on company letterhead with the employer’s ABN and a signature.

- Evidence of savings sufficient to cover the serviceability shortfall during the leave period (the buffer math from earlier in this article).

- Evidence of any income being received during leave. Payslips for employer-paid parental leave, a Services Australia (Centrelink) benefit statement for government Parental Leave Pay, or written confirmation of holiday or long-service leave being paid out.

For lenders using Approach 2 (in-leave income), the documentation focus shifts to evidence of the in-leave income itself (employer-paid parental leave statements, Centrelink benefit statements, payment summaries) and a clear picture of how any unpaid gap will be covered.

Beyond these, every application needs the usual supporting documents: ID, declared household expenses, list of debts and credit limits, and evidence of the deposit and purchase costs.

A specific, well-drafted return-to-work letter is the single most influential document in the file. A vague letter is the most common reason these applications get pushed back for more information.

Worked examples: three Sydney scenarios

These are the kinds of applications I see and place. Numbers are illustrative for April 2026 conditions.

Example 1: First-home buyers in Western Sydney, 12-month leave

Mum, 32, on a $95,000 base salary at a Sydney health-care employer. Returning to work 4 days a week (80 per cent of pre-leave income, so $76,000) at the 9-month mark. Partner on $110,000 PAYG. They want to buy a 3-bedroom townhouse in Penrith for $850,000 with a 12 per cent deposit ($102,000) plus stamp duty and costs. Their loan would be $748,000. LVR is 88 per cent, so LMI applies.

Settlement is targeted at month 3 of the 9-month leave, leaving 6 months of unpaid leave to bridge before the return-to-work income kicks in.

A lender taking Approach 1 (return-to-work income) will run both serviceability calculations:

- Calculation 1, with return-to-work income: Combined household income is $186,000 ($76,000 part-time return income plus $110,000 partner income). At this level, the household qualifies for the loan.

- Calculation 2, without mum’s income, during leave: Just $110,000 partner income. The household is roughly $2,200 per month short of full serviceability.

The 6-month gap multiplied by the $2,200 monthly shortfall equals $13,200. The lender will require around $13,200 in surplus savings, held separately from the deposit, to cover the leave period. If mum is also receiving 14 weeks of employer-paid parental leave plus government Parental Leave Pay during the gap, the lender may reduce the buffer requirement by some or all of that confirmed in-leave income. That policy variation is exactly what determines which lender is the right placement for this file.

See our first home buyer guide for first-home-buyer concessions that may apply on top.

Example 2: Refinancing during maternity leave to a lower rate

Existing $620,000 loan with a major bank at a rate that’s gone up after the 18 March 2026 cash-rate move. Mum is 4 months into a 9-month leave, returning at full hours. Property valued at $980,000 (LVR around 63 per cent). Her employer pays full salary for the first 14 weeks of leave; the rest is unpaid, plus government Parental Leave Pay.

Some lenders will refinance during the leave period if the return-to-work income is documented and the LVR is below 80 per cent. A 0.4 per cent rate reduction on a $620,000 loan saves around $1,500 in interest in the first year alone, and waiting until return-to-work means absorbing months of higher repayments first. See our refinance guide for the standard refinance documents.

Example 3: Buying with a guarantor

Mum, 29, returning at 3 days a week (60 per cent of pre-leave income) at the 8-month mark. Single applicant. Modest deposit. A parent who is prepared to provide a security guarantee using equity in their unencumbered Sydney property.

A guarantor structure can let the applicant avoid LMI and access lender policies that wouldn’t accept a single-applicant maternity leave file on its own. The guarantor’s serviceability isn’t being assessed; their property security is. For parents trying to buy on a single income while on leave, this is often the structure that gets the deal across the line. See our guarantor home loan guide for how it works.

Common mistakes that get applications declined

In my experience, the failed applications usually share one of these features:

Going to your own bank first. Your bank’s policy is one bank’s policy. If the answer is no, the answer might still be yes elsewhere.

A vague return-to-work letter. The letter has to state the exact return date, hours, and gross income on return. “Will return at some point” is not enough.

Insufficient savings buffer. If the lender requires a buffer to cover the unpaid portion of leave, that money has to be visible in a savings account. Aim for at least 3 months of full repayments held separately from the deposit.

Forgetting the higher post-baby living expenses. Banks use the Household Expenditure Measure (HEM) plus declared expenses. With a child in the household, expenses are higher than they were before. Being honest about this prevents an awkward decline at the assessment stage.

Skipping pre-approval. Get pre-approval before signing a contract. The standard property-search advice applies here with extra force: a maternity leave file is more complex, and it pays to know your number before you fall in love with a property. See our pre-approval guide for the process.

What banks won’t tell you (the broker view)

The most useful thing I’ve learned over 25 years of placing these loans is that “no” from one bank means almost nothing. Lenders’ credit policies on this topic vary widely, and most of the actual rules (the percentage of return-to-work income counted, the maximum leave period accepted, the documentation required) live in broker credit guidelines, not on the bank’s customer-facing website.

When the Australian Banking Association’s CEO Anna Bligh spoke about this in November 2022, she was clear that banks have anti-discrimination obligations and responsible-lending verification obligations sitting side by side. Verification is the law. Discrimination is not. The Sex Discrimination Act 1984 protects you from being declined because of pregnancy or parental leave; the National Consumer Credit Protection Act requires the bank to verify you can afford the loan throughout its term. These two things coexist.

What this means practically: if your bank says no, ask whether the no is about you or about the bank’s policy on maternity leave. They’re different answers. A broker can take the same file to a lender whose policy actually fits.

If you’d like to talk through where your file would land, I’m happy to help. It’s a 15-minute phone conversation to scope the realistic options.

Frequently asked questions

Is it possible to get a home loan on maternity leave?

Yes. Several Australian lenders consider applications from borrowers on maternity leave, and Westpac publicly states it recognises paid parental leave and back-to-work income on new home loan applications. The application requires a specific return-to-work letter from your employer, evidence of any employer-paid parental leave, and a savings buffer to cover the unpaid portion of leave. The right lender for your file depends on your specific income, leave length, deposit, and household serviceability.

Will being on maternity leave affect getting a mortgage?

It can affect how lenders calculate your borrowing capacity, because some banks reduce or exclude maternity leave income from serviceability, while others count it in full. It does not, on its own, disqualify you. Pregnancy and parental leave are protected attributes under section 22 of the Sex Discrimination Act 1984 (Cth), which makes it unlawful to refuse a financial service on those grounds.

Can you get a loan while on maternity leave?

Yes. The two key documents are an employer letter confirming your exact return-to-work date and gross income, and bank statements showing a savings buffer to cover any serviceability shortfall during the unpaid portion of your leave. A broker who works across multiple lender credit policies is the most efficient way to find the lender whose rules fit your circumstances.

Can you get approved for a loan on maternity leave?

Yes, when the file is placed with a lender whose credit policy accepts back-to-work income, and when the supporting documents (return-to-work letter, payslips, parental leave evidence, savings statements) demonstrate the household can service the loan throughout the leave period and after return. Pre-approval before signing a contract is strongly recommended.

Do banks count government Parental Leave Pay as income?

Treatment varies. Some lenders accept Centrelink Parental Leave Pay as supplementary income, some discount it, and some exclude it from serviceability calculations because it’s a finite-period payment rather than ongoing income. The current rate is $948.10 per week before tax for up to 24 weeks (rising to 26 weeks from 1 July 2026), subject to income tests of $180,007 individual or $373,094 family.

How much savings do I need to have in the bank?

Lenders calculate this by running two serviceability assessments, one with your return-to-work income included and one without. The gap between them is your monthly shortfall. They then multiply that monthly shortfall by the number of months left in your leave period at settlement to work out the buffer you need. As a worked example: a $5,000 monthly shortfall over a 6-month gap equals $30,000 in required surplus savings, held separately from any funds being used to complete the purchase. Some lenders allow part of that buffer to be substituted with confirmed in-leave income, such as employer-paid parental leave or government Parental Leave Pay. Others require the full amount in cash regardless.

Can I refinance while on maternity leave?

Yes, at lenders whose credit policies allow it. Refinancing during maternity leave is sometimes easier than buying because the LVR is often lower (existing equity), and the borrower’s history with the existing lender is evidence of repayment behaviour. The income documentation is the same: return-to-work letter, payslips, and parental leave evidence.

Is it discrimination if a bank declines me because of maternity leave?

A bank declining a loan because of pregnancy or maternity leave per se would be unlawful discrimination under section 22 of the Sex Discrimination Act 1984 (Cth). A bank declining because the household, by its own credit-policy serviceability assessment, cannot demonstrate affordability throughout the loan term is acting on its responsible-lending obligation under the National Consumer Credit Protection Act 2009. The line between these two reasons matters. If you believe a decline is the first kind, you can lodge a complaint with the Australian Human Rights Commission.

Talk to a broker who’s done this before

I’ve placed many of these loans for parents on maternity leave across Sydney and across Australia. If you’re on leave or about to go on leave and you want to know whether buying or refinancing makes sense in your specific situation, book a 15-minute phone call. It’s free, there’s no pressure, and you’ll walk away knowing exactly where your file would land.

This article contains general information only and does not constitute financial advice. Your personal financial situation, objectives and needs have not been considered. Before acting on any information, you should consider its appropriateness to your circumstances. Speak to a qualified mortgage broker for advice tailored to your situation. Mortgage World Australia Pty Ltd is a credit representative (CR No. 396946) of Mortgage Specialists Pty Ltd (Australian Credit Licence No. 387025).

Patrick is a Director and a Home Loan Specialist. He has been helping Australians with home loans since 2001. Prior to working as a mortgage broker Patrick was employed by Macquarie Bank for 3 years and also worked as an accountant for a publicly listed company. Patrick’s qualifications include:

Bachelor of Business, UTS Sydney. Majored in accounting and sub-majored in Finance and Marketing.

Diploma of Finance and Mortgage Broking Management FNS50310

Certificate IV in Financial Services (Finance/Mortgage Broking) FNS40804

Ready to Take the Next Step?

Whether you’re looking to buy your first home, refinance, or explore investment opportunities, Mortgage World Australia is here to help.

Fill out the contact form below, and one of our expert mortgage brokers will be in touch shortly to discuss your needs and guide you through your options.

Get Started Today!