How Much Can I Borrow? Borrowing Power Guide

How much can I borrow: the complete guide

You’ve found a property you like. The listing says $850,000. Your real estate agent says you can “definitely afford it.” Your friend who bought two years ago says the same thing. But can you? And more importantly — should you borrow that much?

Those are two different questions. “How much can I borrow” is a calculation. “How much should I borrow” is a strategy. This guide walks you through both.

We’ll explain exactly how Australian lenders calculate your borrowing capacity, what factors affect it, how government schemes change the deposit equation, and what the gap between bank approval and smart borrowing actually looks like. If you want a specific figure for your situation, speak to our mortgage brokers directly. We have access to 52+ lenders and can give you a clear picture of your borrowing power within 24 hours.

How is borrowing capacity calculated?

On this page ▾

Borrowing capacity — sometimes called borrowing power — is the maximum loan amount a lender will approve based on your financial position. Lenders don’t use a simple income multiple to arrive at this figure. They run a serviceability assessment: a detailed test of whether your income, after tax and all your expenses, leaves enough surplus to service the proposed loan.

The serviceability model

The correct name for what lenders calculate is Uncommitted Monthly Income (UMI) — or, in some lenders’ terminology, Net Service Ratio (NSR). The process works like this.

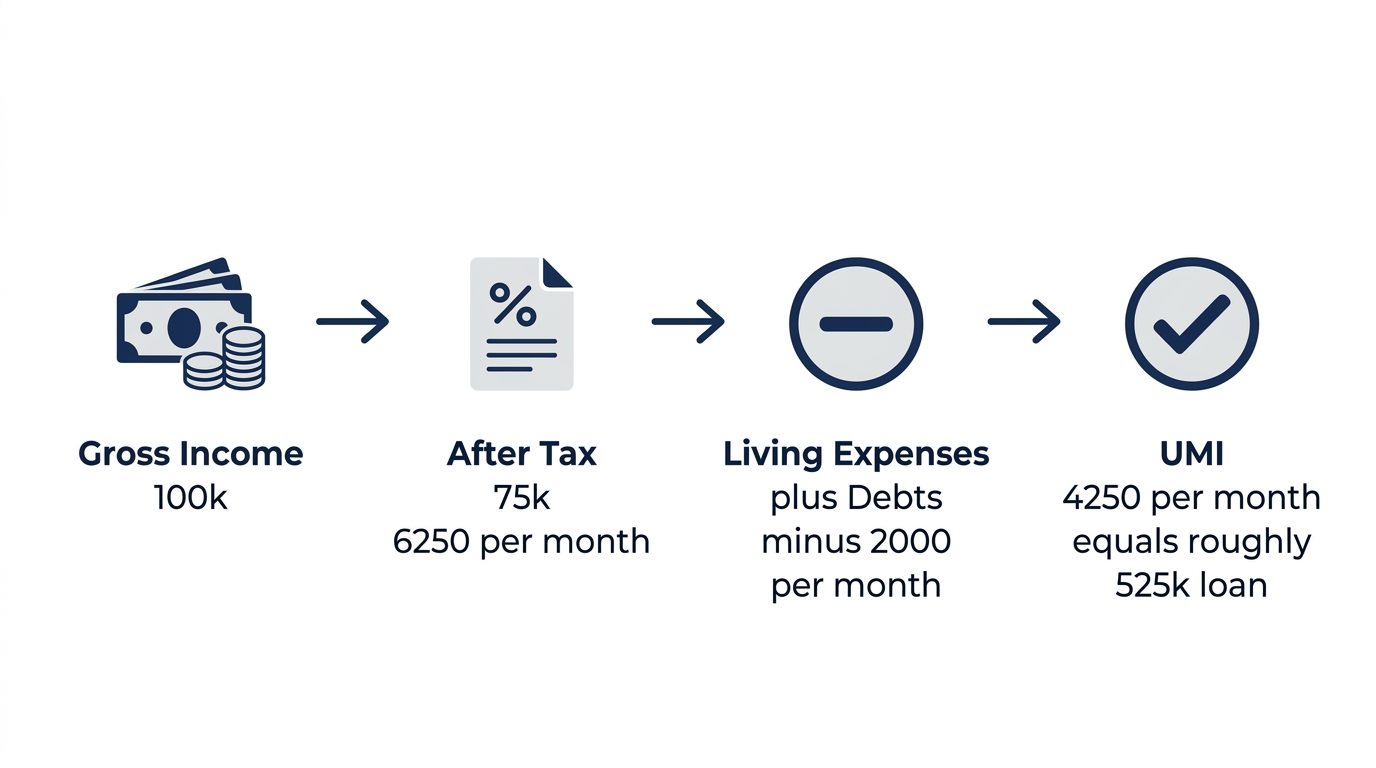

First, your gross income is converted to net income. On a $100,000 salary, after income tax and the Medicare levy, you’re taking home roughly $75,000 per year — about $6,250 per month.

From that net income, lenders deduct your living expenses. They use the Household Expenditure Measure (HEM) as a benchmark — a figure set by the Melbourne Institute that estimates reasonable minimum living costs based on your household size and location. If your actual declared expenses are higher than HEM, lenders use your declared figure.

Then they deduct your existing monthly debt commitments — every dollar of obligation you already carry.

What’s left is your Uncommitted Monthly Income. The proposed loan repayment, assessed at the stress-tested rate, must fit within that surplus.

A worked example: single applicant, $100,000 gross income, no dependants, no existing debts.

- Net monthly income after tax: ~$6,250

- HEM living expenses (single, no dependants): ~$2,000/month

- Existing commitments: $0

- Uncommitted monthly income: ~$4,250/month

At a current variable rate of approximately 6.2% (assessed at 9.2% with the 3% buffer), $4,250/month services a loan of roughly $525,000 over 30 years. That’s consistent with the realistic range of $500,000–$600,000 most lenders will approve for a borrower in this position, depending on their specific HEM figure and credit appetite.

What lenders deduct: expenses and commitments

Understanding exactly what goes into the “existing commitments” deduction is where most borrowers get surprised.

Every monthly debt obligation counts, including HECS/HELP repayments (at the compulsory repayment rate based on income), car loans and personal loans, novated lease payments, credit card limits (the full credit limit is used to calculate a minimum monthly repayment — typically 3.8% of the limit — regardless of your actual balance), and existing home loan repayments stress-tested at the assessed rate.

Beyond debt repayments, certain ongoing expenses sit outside HEM and are assessed separately: private school fees, health insurance premiums, and income protection and life insurance premiums. These are treated as additional commitments that reduce your UMI on top of the HEM living expense figure. Other costs like childcare, subscriptions, and general day-to-day spending are typically captured within the HEM benchmark itself — so they’re already accounted for in the base expense figure lenders use.

On credit cards specifically: a $20,000 credit card limit adds roughly $760/month to your assessed commitments (3.8% of $20,000). That $760/month in reduced UMI translates to approximately $95,000–$120,000 less borrowing capacity. Cancelling unused credit cards before you apply is one of the most effective — and most overlooked — ways to improve your position.

Stress testing and interest rate buffers

Since October 2021, APRA has required Australian lenders to assess serviceability at the loan contract rate plus 3 percentage points. If your proposed loan rate is 6.2%, repayments are stress-tested at 9.2%.

Here’s the part that catches most borrowers off guard: the 3% buffer doesn’t just apply to the new loan. It applies to every home loan in the assessment. If you have an existing investment property loan at 6.0%, that loan’s repayments are also assessed at 9.0% when a lender is calculating how much you can borrow for a new purchase. The buffer stacks across your entire home loan portfolio.

This is why borrowers with investment properties often find their borrowing capacity lower than expected — the stress testing of existing loans compounds the effect on serviceability for new borrowing.

One important distinction: the 3% buffer is an APRA requirement that applies to authorised deposit-taking institutions (ADIs) — banks, credit unions, and building societies. Non-bank lenders aren’t regulated by APRA and often use a smaller buffer of 1%–2%. That smaller buffer means a lower stress-test rate, which means the same borrower can qualify for a larger loan with a non-bank lender than with a major bank. This is one of the reasons non-bank lenders are worth considering, particularly for borrowers who are close to their capacity limit with a bank.

The debt-to-income (DTI) ratio is a separate, secondary policy check. From February 2026, APRA limits lenders to extending no more than 20% of new mortgage lending to borrowers with a DTI of 6 or above. In practice, DTI is a guardrail that kicks in after the serviceability calculation — most borrowers hit the UMI ceiling before they hit the DTI ceiling.

Lenders calculate borrowing capacity using a serviceability model: your gross income minus tax gives your net monthly income. From that, they subtract living expenses (benchmarked against HEM) and all existing debt commitments. The remaining uncommitted monthly income must be sufficient to cover your proposed loan repayments, stress-tested at your contract rate plus a 3% APRA buffer. The same 3% buffer applies to any existing home loans being assessed at the same time.

Key factors that affect your borrowing capacity

Income is only one piece of the puzzle. Here’s what else lenders look at when they calculate how much you can borrow.

Your income type matters as much as the dollar amount. PAYG salary is assessed at face value. Bonuses and commissions can count, but usually only at 80% of their two-year average, and only with documented history. Rental income is typically included at 70%–80% of the gross figure to allow for vacancy and costs.

Existing debts chip away at your capacity across the board — car loans, personal loans, HECS/HELP repayments, and credit card limits (the full limit, not your current balance). Every dollar of monthly obligation reduces the loan amount a lender will approve.

Your credit score shapes which lenders will deal with you and on what terms. Defaults, late payments, and credit enquiries from the past five years all reduce your score. If you’re planning to apply in the next six months, check your credit file now — you’re entitled to a free report from Equifax, Experian, and illion once a year each.

Deposit size affects your LVR (Loan-to-Value Ratio — the loan amount divided by the property value). Below 80% LVR, you access standard products without Lenders Mortgage Insurance (LMI). LMI is an insurance policy that protects the lender, not you — and you pay the premium, either upfront or capitalised into your loan. Above 80% LVR, you need LMI, a guarantor, or a government scheme to proceed.

Property type and location introduce constraints that catch buyers off guard. High-density apartments in certain postcodes, rural properties, and areas lenders classify as high-risk often attract LVR caps of 60%–70%, regardless of how strong your financials are. Worth checking early before you fall in love with a property.

Number of dependants matters because lenders use the Household Expenditure Measure (HEM) to estimate your minimum living costs. The more dependants you have, the higher the assumed expenses, and the lower your assessed serviceability.

Age is a factor for longer loan terms. A 55-year-old applying for a 30-year loan faces more scrutiny than someone in their 30s — lenders want to understand how repayments will be managed once employment income stops.

Employment type: PAYG vs. self-employed

This distinction matters more than most borrowers expect.

PAYG employees with permanent roles have their income verified via payslips, tax returns, and employment contracts. The assessment is relatively straightforward — most lenders will use your current gross income with minimal adjustment.

Self-employed borrowers need two years of tax returns and business financials. Lenders assess income conservatively — usually taking the lower of the two years’ net profit, or an average — and some apply additional haircuts to allow for business volatility. On the same income, a self-employed borrower typically qualifies for a smaller loan than an equivalent PAYG borrower.

The solution isn’t to misrepresent your income structure. It’s to find lenders who take a sensible view of self-employed income. Some lenders are far more flexible on this than the major banks — and that’s where having access to 52+ lenders, rather than walking into one bank, makes a material difference.

Credit score and payment history

In Australia, credit bureaus Equifax, Experian, and illion each produce scores using slightly different models. A score above 700 is generally considered good. Below 600, your options narrow materially.

Most lenders check comprehensive credit reporting (CCR), which shows not just defaults and enquiries but also your repayment history across all credit accounts for the past two years. A pattern of late payments — even if accounts are current — can affect how lenders assess your reliability.

If you have a poor score, that doesn’t end your borrowing capacity. It changes which lenders will deal with you and at what rate. Bad credit home loans exist, but they come at a cost.

Deposit size and LVR

LVR — Loan-to-Value Ratio — is the loan amount divided by the property’s purchase price or valuation, expressed as a percentage. A $600,000 loan on an $800,000 property is 75% LVR.

The 80% LVR threshold is the most important line in home lending. Below it, you access standard products, better rates, and more lenders. Above it, lenders require LMI (or a government guarantee, or a family guarantee arrangement) to protect against the increased default risk.

A larger deposit improves your LVR, which typically unlocks better rates, more lenders, and lower overall loan costs. That said, it’s not always worth waiting to save a 20% deposit — particularly when property prices are rising or government schemes offer a viable path in with less.

Property type and location

Lenders apply what’s called a postcode policy to locations or property types they consider higher risk. This includes regional towns with limited economic diversity, inner-city apartment blocks with high investor ownership ratios, and properties on small parcels of land.

In these cases, the maximum LVR may be capped at 60%–70% — meaning you’d need a 30%–40% deposit regardless of your income. This is worth checking early when you’re evaluating a specific property.

Affordability vs. borrowing capacity: why banks approve more than you should borrow

Here’s something worth being direct about. The amount a lender approves and the amount you should borrow are rarely the same number.

Banks optimise for their risk, not your lifestyle. Their stress test confirms you can technically service the loan if rates rise. It doesn’t measure what a large mortgage does to your savings capacity, your ability to handle unexpected expenses, or your quality of life when a material share of your take-home pay disappears into a repayment.

A useful budgeting benchmark is 30% of gross income toward housing costs. At $100,000 income, that’s $30,000 per year — roughly $2,500 per month. On a 30-year loan at 6.2%, $2,500 per month supports a loan of around $415,000. A bank might approve $500,000 on that income. The $85,000 difference is real. It shows up as fewer holidays, a smaller emergency fund, and more financial stress when anything goes sideways.

If existing debt is dragging down your capacity, it’s also worth asking whether a home loan refinancing strategy to consolidate or restructure could improve your position before you apply for a new loan.

Over 25 years of doing this work, the borrowers who come back stressed aren’t the ones we talked down to a sensible number. They’re the ones who borrowed at the top of their capacity because the bank said yes.

When you speak with our team, the conversation isn’t just “how much can you borrow?” It’s “how much makes sense given what you actually want your financial position to look like?”

Government schemes that increase your borrowing power

Government schemes don’t directly change your income, debts, or credit assessment. But they change the deposit equation — letting you enter the market sooner, with a smaller deposit, or with government equity support that reduces the loan size you need.

Australian Government 5% Deposit Scheme

The Australian Government 5% Deposit Scheme (previously called the First Home Guarantee, renamed on 1 October 2025) allows eligible first home buyers to purchase a property with a 5% deposit, with the government guaranteeing up to 15% of the purchase price.

The guarantee replaces LMI — so you don’t pay insurance premiums, and you don’t need a family guarantee or 20% savings. You borrow from a participating lender in the usual way; the government’s guarantee sits behind the loan at no direct cost to you.

From 1 October 2025, the scheme changed in three important ways:

Income caps were removed. Previously, singles had to earn under $125,000 and couples under $200,000. Those limits no longer apply. Any eligible first home buyer can now access the scheme regardless of income.

Place limits were also removed. The scheme was previously limited to 35,000 places per year. There is now no cap on places.

The NSW property price cap increased to $1,500,000, up from $900,000. This is particularly relevant for buyers in Sydney and major NSW regional centres.

Eligibility is primarily based on being a first home buyer who is an Australian citizen or permanent resident aged 18 or over, purchasing the property to live in as an owner-occupier.

Both this scheme and Help to Buy are also compatible with the NSW First Home Buyer Assistance Scheme (FHBAS), which provides transfer duty concessions — you may be eligible for both simultaneously. To explore first home buyer loans using this scheme, we can confirm your eligibility and match you with a participating lender from our panel.

Help to Buy Scheme

The Help to Buy Scheme launched in December 2025. It’s a shared equity arrangement: the government purchases a portion of your home alongside you, which reduces the loan size you need.

For new homes, the government contributes up to 40% of the purchase price. For existing homes, up to 30%. You purchase the remaining share and take out a standard home loan for your portion. Because the loan is smaller, your repayments are lower — and your serviceability assessment becomes easier to pass.

Income thresholds apply: $100,000 per year for individuals, $160,000 per year for couples and single parents. These thresholds are indexed and reviewed annually on 1 July.

The Sydney property price cap is $1,300,000. 10,000 places are available nationally each year — 40,000 over the four-year life of the scheme.

The trade-off is worth understanding before applying. The government retains an equity stake proportional to its contribution. When you sell, refinance, or make structural changes to the property, you repay the government’s share based on the property’s current value — not the original purchase price. If your property grows by $200,000 and the government held a 30% share, it’s entitled to $60,000 of that gain.

This is a co-ownership arrangement, not a grant. Whether it suits your situation depends on your income, how long you plan to hold the property, and whether co-ownership fits your goals. Our brokers can work through the numbers with you.

Borrowing power for investment property loans

Investment lending works differently from owner-occupier lending, but not always in the direction borrowers expect.

If you are purchasing an investment property, the 2026 Federal Budget has changed the equation. For a detailed look at how the 2026 Budget affects investor borrowing capacity, including before-and-after serviceability modelling across seven lenders, see our guide.

Interest rates on investment loans are higher — typically 0.2%–0.5% above equivalent owner-occupier rates. That sounds like it should reduce borrowing capacity, and in isolation it does. But there’s an offsetting factor: the interest on investment loans is tax-deductible. Some lenders factor this tax benefit into their serviceability calculation, which reduces the tax deducted from the borrower’s gross income and increases net income for assessment purposes. Depending on the lender and the borrower’s tax position, this can actually translate into higher borrowing capacity on an investment loan than an equivalent owner-occupier purchase.

Rental income is counted in the serviceability calculation, but conservatively. Most lenders include 70%–80% of gross rental income to account for vacancy, management fees, and maintenance. Some lenders are more generous (up to 90%); others more conservative (60%). This difference can meaningfully affect approval amounts for higher-value properties.

Remember too that the 3% serviceability buffer applies to any existing investment property loans when you’re applying for new finance. If you hold a $600,000 investment property loan at 6%, that loan’s repayments are assessed at 9% in your new application — which can materially reduce your uncommitted monthly income and therefore your available borrowing for the new purchase.

Portfolio complexity matters as well. If you hold multiple investment properties, some lenders cap total portfolio exposure — by number of properties, total lending, or total value as a multiple of income. This affects your ability to keep adding properties over time.

Most lenders will go up to 90% LVR on investment loans with LMI. Without LMI, the typical cap is 80%. Going above 80% adds the cost of LMI to the deal, but it’s available from most major lenders — not just a handful of specialists.

Investment property financing is one of the areas where lender selection matters most. The variance between lenders on investment deals — rates, LVR limits, rental income treatment, and how they account for tax deductibility — is far larger than it is on standard owner-occupier loans. Going to one bank and accepting whatever they offer is a real cost on investment deals.

Getting pre-approved: the next step

Once you have a rough understanding of your borrowing capacity, pre-approval is the logical next step before actively searching for a property.

A pre-approval is a formal assessment by a lender confirming how much they’ll lend you, subject to finding a suitable property. It’s not a final guarantee — conditions can change, property valuations can come in low, and pre-approvals typically expire after 90 days — but it does three things worth understanding.

It confirms your capacity with a real assessment rather than a calculator estimate. Online calculators use assumptions. Pre-approval uses your actual documents: payslips, tax returns, bank statements, and credit reports. The serviceability calculation is run on your actual numbers.

It gives you credibility in the market. Sellers and agents treat pre-approved buyers differently from those who “think” they can probably afford it. At auction, the difference between those two positions is real.

It also identifies problems before they derail a purchase. Credit issues, self-employment income that doesn’t stack with a particular lender’s model, or property type restrictions — better to find these out before you’ve found the property you want to make an offer on.

The mortgage pre-approval process with us takes two to five business days. We assess your position across our full panel and recommend the lender most likely to approve you at the best terms — not just the one who’ll say yes.

If you’re planning to buy in the next three to six months, get pre-approved now. If your circumstances change — new debts, a change in employment, an income shift — contact us to reassess. A pre-approval based on outdated information isn’t worth much.

Frequently asked questions

How is borrowing capacity calculated in Australia?

Lenders use a serviceability model, not a simple income multiple. Your gross income is converted to net income (after tax), then living expenses (benchmarked against the Household Expenditure Measure) and all existing debt commitments are deducted. The remaining uncommitted monthly income must cover your proposed repayments, assessed at your contract rate plus a 3% APRA buffer. The same buffer applies to any existing home loans being assessed at the same time.

What factors affect how much I can borrow?

Income, employment type (PAYG vs. self-employed), existing debts (car loans, credit card limits, HECS/HELP, novated leases), expenses assessed outside HEM (health insurance, life insurance, private school fees), credit score, deposit size, property type, number of dependants, and age all affect your borrowing capacity. The HEM figure each lender uses and their specific serviceability policy also vary between lenders.

How do lenders calculate the maximum loan amount?

Lenders calculate your uncommitted monthly income (net income minus living expenses and existing commitments) and determine the largest loan whose stress-tested repayments fit within that surplus. From February 2026, APRA also requires that no more than 20% of a lender’s new mortgage volume goes to borrowers with a debt-to-income ratio of 6 or above. Lender-specific HEM figures and policy settings mean the same borrower can receive different approval amounts from different banks — which is why comparing across lenders matters.

What percentage of income can I spend on mortgage repayments?

Lenders assess this using the uncommitted monthly income model rather than a fixed percentage rule. As a practical budgeting benchmark, keeping total housing costs below 30% of gross income provides meaningful financial resilience — particularly given the gap between what a lender will approve and what leaves room in your budget.

Does being self-employed reduce how much I can borrow?

It can, but it depends heavily on which lender you use. Self-employed borrowers typically need two years of tax returns and are assessed more conservatively. The gap between PAYG and self-employed capacity has narrowed as more lenders offer specialist self-employed products, but finding the right lender for your income structure requires comparing properly across the market.

Ready to find out exactly how much you can borrow? Speak to our mortgage brokers at Mortgage World Australia. We’ll assess your position across 52+ lenders and give you a clear, personalised picture of your borrowing capacity — without the guesswork.

This article contains general information only and does not constitute financial advice. Your personal financial situation, objectives and needs have not been considered. Before acting on any information, you should consider its appropriateness to your circumstances. Speak to a qualified mortgage broker for advice tailored to your situation. Mortgage World Australia Pty Ltd is a credit representative (CR No. 396946) of Mortgage Specialists Pty Ltd (Australian Credit Licence No. 387025).

Patrick O’Brien — Director and Home Loan Specialist, Mortgage World Australia. Operating since 2001.

Patrick is a Director and a Home Loan Specialist. He has been helping Australians with home loans since 2001. Prior to working as a mortgage broker Patrick was employed by Macquarie Bank for 3 years and also worked as an accountant for a publicly listed company. Patrick’s qualifications include:

Bachelor of Business, UTS Sydney. Majored in accounting and sub-majored in Finance and Marketing.

Diploma of Finance and Mortgage Broking Management FNS50310

Certificate IV in Financial Services (Finance/Mortgage Broking) FNS40804

Ready to Take the Next Step?

Whether you’re looking to buy your first home, refinance, or explore investment opportunities, Mortgage World Australia is here to help.

Fill out the contact form below, and one of our expert mortgage brokers will be in touch shortly to discuss your needs and guide you through your options.

Get Started Today!