Discharge of Mortgage: Australian Guide, Fees & Timeline

Discharge of Mortgage: What You Need to Know

On this page ▾

- What is a discharge of mortgage?

- When do you need to discharge a mortgage?

- How to discharge your mortgage: step by step

- How long does a mortgage discharge take?

- Mortgage discharge fees by lender

- Where to find your lender’s discharge form

- Discharging to refinance vs discharging to sell

- Discharge lodgement fees by state (NSW, VIC, QLD, SA, WA)

- What to do when a discharge stalls

- Do you need a solicitor or conveyancer?

- How a mortgage broker handles your discharge

- Frequently asked questions

The discharge of mortgage is the legal process of removing your lender’s registered interest from your property title. Every time you sell, refinance, or pay off a home loan, this has to happen, and most borrowers don’t give it a second thought until it doesn’t go to plan.

After more than two decades coordinating settlements and refinances, the situations I see come up repeatedly are: borrowers who didn’t submit the discharge authority form early enough and lost their settlement date, and fixed-rate borrowers who got blindsided by break costs they didn’t know to ask about. This guide covers both, along with the fees, the state-by-state registration costs, and exactly where to find each lender’s form.

What is a discharge of mortgage?

A discharge of mortgage is the formal removal of a lender’s registered interest from your property title. When you take out a home loan in Australia, the lender registers a mortgage against your property at your state Land Titles Office. That registration secures their legal claim over the property for the life of the loan. When the loan ends, you must apply to have that registration removed; the discharge of mortgage is that formal application.

Once the discharge is registered at your state Land Titles Office, the lender’s name no longer appears on your Certificate of Title. The property is unencumbered.

Discharge vs release vs title: the terms explained

Three terms come up in the discharge process and are often confused.

A discharge of mortgage is the instrument lodged with the state land registry, the document that formally removes the lender’s registered interest. A title release (sometimes called a security release) is the lender’s internal step, their confirmation that the debt is settled, and they consent to the discharge. A Certificate of Title (or eCT, the electronic version) is the document that records ownership and any registered interests over the property.

In that order, always: debt settled or sale complete, then the lender issues a title release, then the discharge is lodged with the registry. You cannot skip the lender’s internal sign-off, and the registry will not process without it.

When do you need to discharge a mortgage?

Selling, refinancing, paying it off, or releasing a guarantee

A discharge of mortgage is required in four situations:

- Selling your property. The property cannot transfer to a buyer with a lender’s mortgage registered on the title. Your conveyancer coordinates the discharge as part of the settlement.

- Refinancing to a new lender. The outgoing lender must discharge their mortgage before or simultaneously with the incoming lender registering theirs. Both happen at settlement through PEXA.

- Paying the loan off in full. A zero loan balance does not remove the mortgage from the title automatically. You must request the discharge separately.

- Releasing a guarantor. Removing a family guarantee typically requires a partial discharge and may need the lender to reassess the remaining security position before they will agree to release.

One scenario where a full discharge is not required: restructuring your loan with the same lender. A change in repayment type, a rate fix, or a loan split handled internally is a loan variation rather than a discharge, and is typically faster and cheaper.

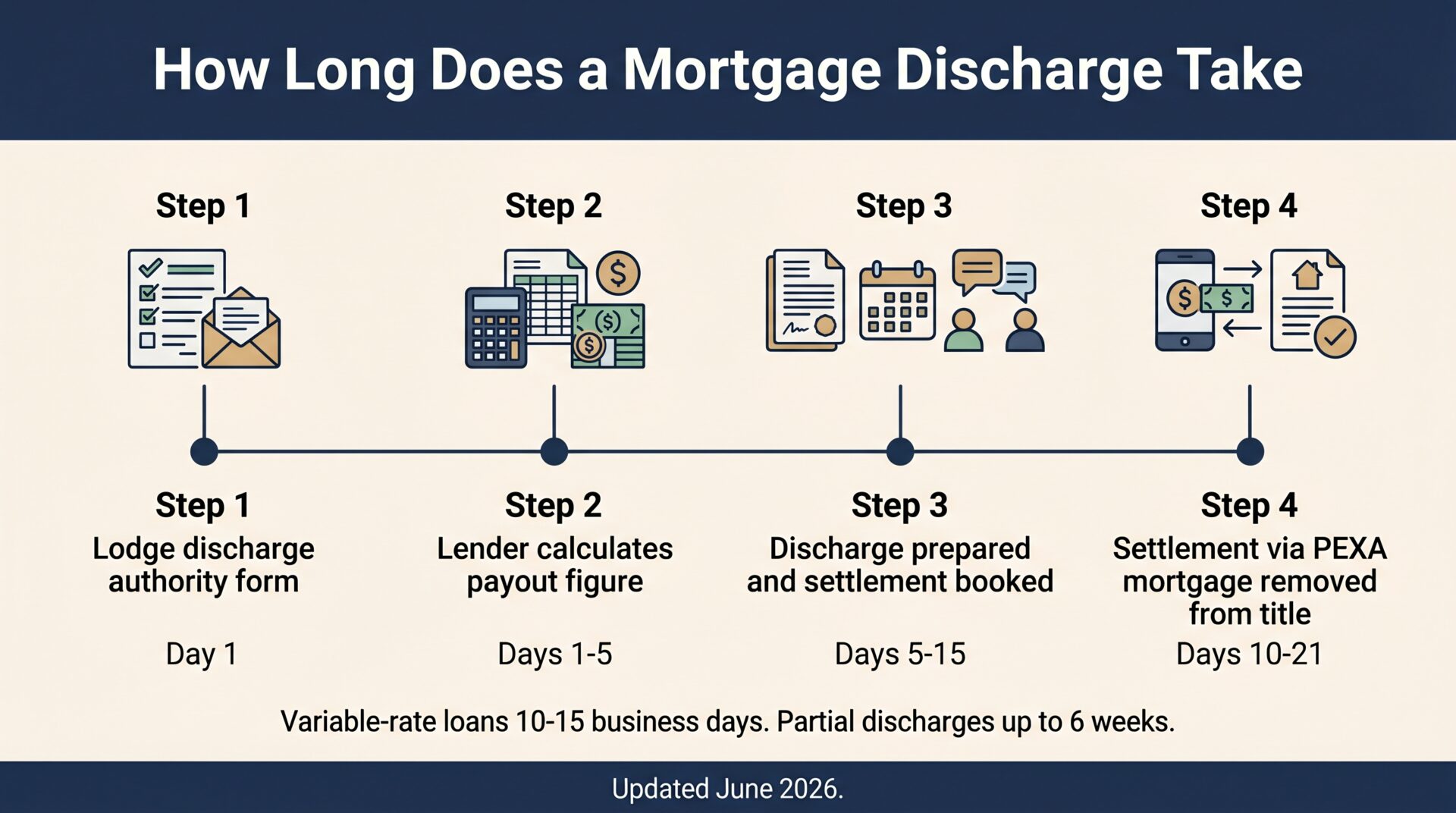

How to discharge your mortgage: step by step

Step 1: lodge a discharge authority form with your lender

Contact your lender and complete their discharge authority form. This form authorises the lender to proceed with the discharge and captures the details they need: all borrowers’ full legal names, the loan account number, the property address, Certificate of Title reference, and bank details for any refund of surplus funds. All borrowers on the loan must sign. If a guarantor is named on the loan, they may also be required to sign.

Submit the form as early as possible. Your lender continues to charge interest until the discharge settles and faces no penalty for processing at their standard pace. For a refinance, lodge the form at the same time as you submit your new loan application.

Step 2: your lender prepares the discharge

Once the form is received, the lender calculates a payout figure: your remaining loan balance, accrued interest to the proposed discharge date, and the administrative discharge fee. For fixed-rate loans, the lender also calculates break costs at this stage.

Break costs and the discharge fee are not the same thing. The discharge fee is the administrative charge for processing the discharge. Break costs are a separate amount, calculated on the interest differential between your fixed rate and current market rates for the remaining fixed term. Both appear on the payout figure but are listed separately.

The payout figure is valid for a fixed period, commonly 30 days. If settlement is delayed past the expiry date, the lender recalculates the figure, which adds processing time and may produce a different amount.

Step 3: settlement and lodgement via PEXA

Most Australian discharges are processed electronically through PEXA (Property Exchange Australia), the digital settlement platform that connects lenders, conveyancers, and state Land Titles Offices. For a sale or refinance, the discharge of the outgoing mortgage and the registration of any new incoming mortgage are lodged simultaneously at settlement. PEXA reduced standard discharge timeframes from around 40 business days to approximately 20.

Paper lodgement is still available through some lenders and in some circumstances, but it typically costs more at the registry level and takes longer.

Step 4: the mortgage is removed from your title

Once the discharge is registered by the Land Titles Office, the lender’s interest is formally removed from your Certificate of Title. For a refinance, this happens at the same moment as the new lender registers their mortgage, so there is no gap between the old and new security interests. Your conveyancer can confirm the clearance by conducting a title search after settlement.

How long does a mortgage discharge take?

A standard variable-rate discharge takes 10 to 21 business days from the date the completed discharge authority form is received by the lender. Major banks typically complete within 10 to 15 business days. Non-bank lenders may take up to 21 business days. Partial discharges, where one property is released from a multi-property loan, can take up to six weeks because the lender generally orders a new valuation first.

The practical rule: submit the discharge authority form at least four weeks before your intended settlement date. For a sale, give the signed form to your conveyancer as soon as the contracts exchange. For a refinance, submit it at the same time as your new loan application.

If your fixed rate is ending, the break cost calculation adds processing time. Always request a written break cost estimate before submitting the discharge authority form.

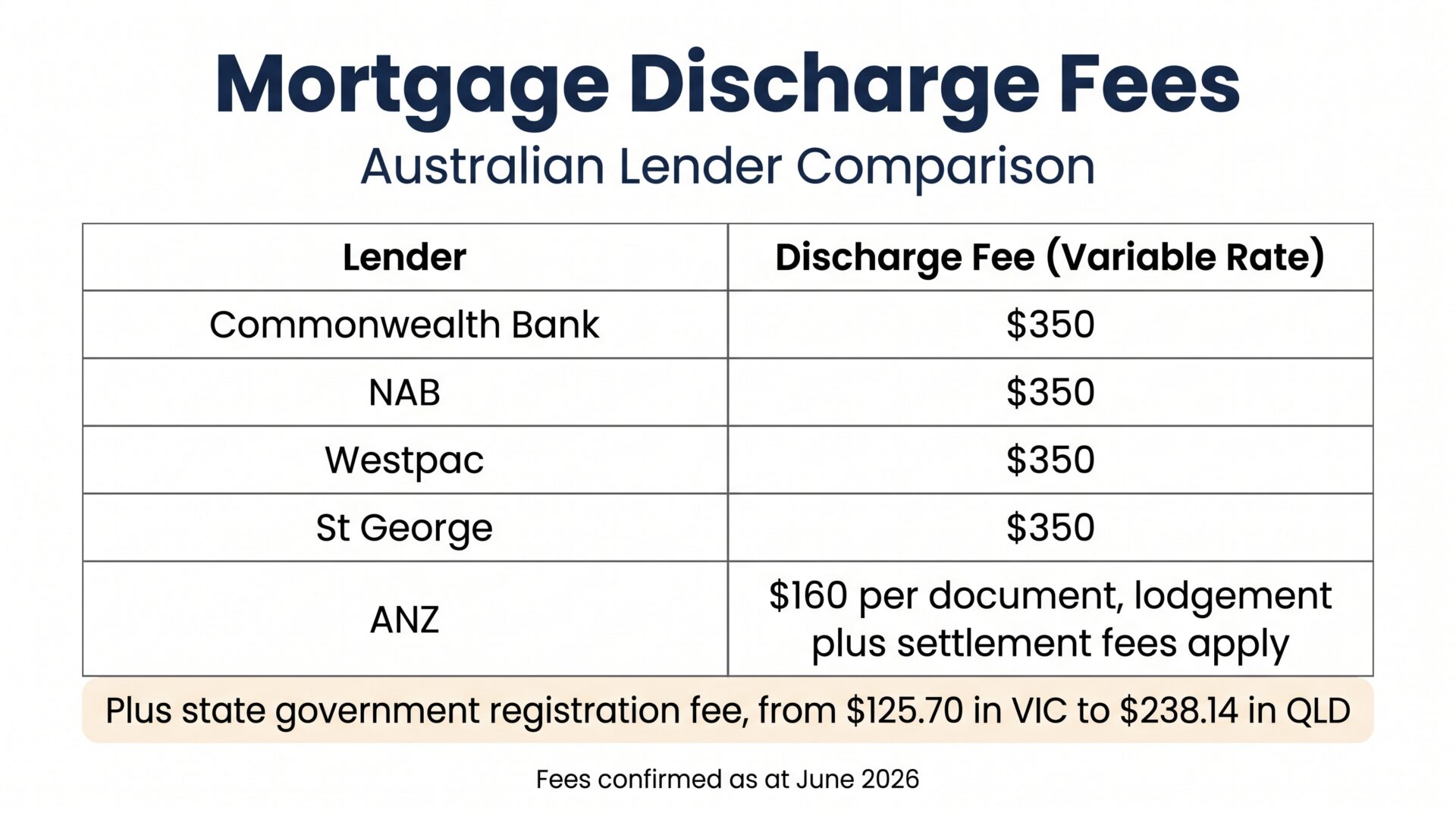

Mortgage discharge fees by lender

Every major lender charges an administrative fee to process your discharge. This is separate from the state government registration fee, which is covered in the next section.

| Lender | Discharge Fee (Variable Rate) | Notes |

|---|---|---|

| Commonwealth Bank (CBA) | $350 | Confirmed: CBA Home Loan Fees PDF, March 2026 |

| St George | $350 | Confirmed: St George website |

| Bank of Melbourne | $350 | Same Westpac Group fee structure |

| Bank of SA | $350 | Same Westpac Group fee structure |

| NAB | $350 | Confirmed from NAB fees page |

| Westpac | $350 | Confirmed from Westpac fees page |

| ANZ | $160 lodgement + $160 settlement per document | ANZ charges per-document fees rather than a single discharge fee; total likely $320, confirm with ANZ |

| Macquarie | $400 | Confirmed in the Macquarie product guide |

| ING | $250 + legal costs | Confirmed in ING’s post settlement fees & charges guide |

| Other lenders | $150 to $500 | Varies by lender |

For fixed-rate loans, break costs are charged in addition to the discharge fee and can be substantially higher. Always request a written break cost estimate before submitting the discharge authority form.

Fees are indicative as at June 2026. Always confirm the exact fee with your lender before proceeding.

Where to find your lender’s discharge form

Each lender uses their own discharge authority form. There is no universal document across Australian lenders.

The best way to find your lender’s discharge form is to Google search “<lender name> discharge form”.

Some lenders publish the discharge form on their website, while others require you to call them to request it, particularly when refinancing.

Discharging to refinance vs discharging to sell

The paperwork is the same either way. The coordination and priorities differ.

When you are refinancing, the discharge of your outgoing loan and the registration of your new lender’s mortgage happen simultaneously at settlement. The new lender’s solicitor manages this process, coordinating both lenders in the PEXA workspace. A mortgage broker handling a home loan refinance will request your discharge authority form at application, time the payout figure request to keep it valid through to settlement, and monitor both lenders to protect your settlement date.

The discharge fee is a real cost in the refinancing calculation. At $350 for most major banks, it forms part of the switching cost that should be weighed against the ongoing rate saving. Refinance cashback offers from incoming lenders often exceed the discharge fee, but cashback terms and clawback periods vary significantly.

If you’re weighing a switch, work out your break-even point before you lodge the discharge authority, not after. The key reasons to refinance are worth reading first.

When you are selling, your conveyancer coordinates the discharge as part of the home-buying and sale process. They request and submit the discharge authority form, manage the PEXA settlement workspace, and ensure the discharge is registered at the exact moment the sale proceeds are transferred. If the discharge is not ready by the contractual settlement date, the buyer has grounds to reschedule, which may trigger penalty interest clauses in the contract.

Discharge lodgement fees by state (NSW, VIC, QLD, SA, WA)

After the lender prepares the discharge, it is lodged with the relevant state Land Titles Office. Government registration fees apply on top of the lender’s discharge fee.

| State | Registration Fee | Land Titles Authority | Effective Date |

|---|---|---|---|

| NSW | $175.70 (rising to $182.73 from 1 July 2026) | NSW Land Registry Services | 1 July 2025 |

| VIC | $125.70 electronic / $135.80 paper | Land Use Victoria | 2025/26 |

| QLD | $238.14 (rising to $248.04 from 1 July 2026) per mortgage interest | Titles Queensland | 2025/26 |

| SA | $198 per mortgage | Land Services SA | 2025/26 |

| WA | $216.60 per mortgage | Landgate WA | 1 July 2025 |

Government fees are subject to annual review. NSW fees are $175.70 for FY2025/26, rising to $182.73 from 1 July 2026. QLD fees are $238.14 for FY2025/26, rising to $248.04 from 1 July 2026.

Who lodges the discharge? In most states, a licensed conveyancer or solicitor lodges the discharge, not the borrower directly. In Victoria specifically, bank-mortgagee discharges must be lodged by a lawyer or licensed conveyancer; individual borrowers cannot self-lodge for a bank-secured mortgage. PEXA electronic lodgement is standard across NSW, VIC, QLD, SA, and WA for eligible transactions.

What to do when a discharge stalls

Most discharges run without drama. When they stall, the cause is almost always one of three things. Knowing which one can save you a week.

Name mismatches and missing signatures. The most common hold-up: the borrower’s name on the discharge form doesn’t match the name on the original loan records. A maiden name used on one document, a middle name included on another, or a simple spelling variation is enough to stop the process. If there’s a discrepancy, contact the discharge team the same day and provide photo ID that bridges both versions. Don’t wait for them to come back to you; they won’t escalate it on your timeline.

Payout figure expiry. Payout figures are typically valid for 30 days. If settlement slips past that window, the lender recalculates, and the new figure may differ from what you’d budgeted. Lock in a firm settlement date before you request the payout figure, not after.

Identity re-verification on older loans. Some lenders require fresh identity documents for loans that were settled years ago, particularly where borrower details have changed. Have your account number and current photo ID ready before you call; it cuts the back-and-forth time significantly.

A broker handling your refinance can call the outgoing lender’s settlements team directly, usually on a broker priority line. That matters when a file is sitting in a queue; knowing who to call and what to ask accelerates things. I’ve seen stalls that looked like they’d blow a settlement date clear up within a day once the right person was reached.

Do you need a solicitor or conveyancer?

For a sale, yes. A conveyancer coordinates the payout figure request, submits the discharge authority, manages the PEXA settlement workspace, and confirms the title is clear after lodgement, all as part of their standard service. You’re not paying separately for discharge coordination; it’s included.

You do not need a solicitor or conveyancer to coordinate the discharge when refinancing your mortgage. Your new lender will coordinate the settlement and finalisation of your discharge with your outgoing lender.

Another scenario where you can act without a conveyancer: paying off your home loan in full with no concurrent sale. You submit the discharge authority directly to your lender, they process the release, and the discharge is lodged electronically. Even in this case, many borrowers appoint a conveyancer simply to confirm that the title is clear after the discharge is registered.

How a mortgage broker handles your discharge

For a refinance, your mortgage broker coordinates the discharge as part of the loan-switching service. At MWA, that means requesting your discharge authority form at the time of application, submitting it to the outgoing lender at the right moment to keep the payout figure valid, and coordinating the settlement date with both lenders’ legal teams.

Timing matters more than most borrowers realise. A one-month delay on a $500,000 loan at 6.5% costs roughly $2,700 in extra interest before the switch is complete. That’s real money, not a rounding error in the refinancing calculation.

If you’re paying off your home loan entirely and weighing a lump sum payment against closing the account, there are cashflow and tax implications worth working through before you sign anything.

To discuss a refinance or discharge, talk to a mortgage broker at MWA. We work with 52+ lenders and have managed hundreds of discharge and settlement processes.

Frequently asked questions

What does it mean to discharge your mortgage?

To discharge your mortgage means to formally remove your lender’s registered interest from your property title. When a home loan is approved in Australia, the lender registers a mortgage against the property to secure the debt. Once the loan is repaid, refinanced, or the property sold, that registration must be removed by lodging a discharge of mortgage with the state Land Titles Office.

How much does it cost to discharge a mortgage?

The total cost typically falls between $300 and $700, covering your lender’s discharge fee (commonly $350 for major banks on variable-rate loans) and your state government’s registration fee ($125.70 in Victoria to $238.14 in Queensland). Fixed-rate loans may also attract break costs on top of the discharge fee, and break costs can be substantially higher depending on the remaining term and interest rate differential.

How long does a discharge of mortgage take?

A standard discharge takes 10 to 21 business days from the date the completed discharge authority form is received by the lender. Major banks on variable-rate loans typically complete within 10 to 15 business days. Submit the form at least four weeks before your intended settlement date to protect your timeline.

What is the first thing to do when you pay off your mortgage?

Request a discharge of mortgage from your lender. A zero balance doesn’t automatically remove the mortgage from your title. Complete the discharge authority form, confirm the registration fee with your state Land Titles Office, and once it’s lodged, get written confirmation the title is clear.

Can I discharge my mortgage without a broker?

Yes. For a straight payoff with no sale or refinance, you submit the discharge authority directly, the lender processes the release, and the discharge is lodged. For a refinance, the incoming lender’s solicitor typically runs the coordination; a broker adds value mainly by managing the timing between both lenders and chasing stalls before they affect your settlement date.

Patrick O’Brien, Director and Home Loan Specialist since 2001

This article contains general information only and does not constitute financial or credit advice. Your personal financial situation, objectives and needs have not been considered. Before acting on any information, you should consider its appropriateness to your circumstances. Speak to a qualified mortgage broker for advice tailored to your situation. Mortgage World Australia Pty Ltd is a credit representative (CR No. 396946) of Mortgage Specialists Pty Ltd (Australian Credit Licence No. 387025).

Patrick is a Director and a Home Loan Specialist. He has been helping Australians with home loans since 2001. Prior to working as a mortgage broker Patrick was employed by Macquarie Bank for 3 years and also worked as an accountant for a publicly listed company. Patrick’s qualifications include:

Bachelor of Business, UTS Sydney. Majored in accounting and sub-majored in Finance and Marketing.

Diploma of Finance and Mortgage Broking Management FNS50310

Certificate IV in Financial Services (Finance/Mortgage Broking) FNS40804

Ready to Take the Next Step?

Whether you’re looking to buy your first home, refinance, or explore investment opportunities, Mortgage World Australia is here to help.

Fill out the contact form below, and one of our expert mortgage brokers will be in touch shortly to discuss your needs and guide you through your options.

Get Started Today!