Buying Off the Plan in NSW: Finance, Stamp Duty & the Risks

Buying off the plan in NSW: the finance, the stamp duty, and the risks banks rarely mention

On this page ▾

- What does buying off the plan mean?

- How off-the-plan finance actually works (and where it goes wrong)

- The valuation shortfall risk no bank page admits

- Managing the pre-approval gap from contract to settlement

- Off-the-plan stamp duty in NSW: deferral, not a discount

- Sunset clauses and your NSW legal protections

- Why is buying off the plan risky? The honest list

- Western Sydney case studies

- Is buying off the plan a good investment?

- How to protect yourself before you sign

- Frequently asked questions

Search “buying off the plan”, and the first thing you find is worry. A Reddit thread at the top of the page. Forum posts asking why you should never do it. Plenty of reasons to be nervous, and not many straight answers about the money.

Here is the gap nobody fills. The government pages explain your legal rights well. The bank guides walk you through deposits. But no single page connects the two and tells you the part the banks are quietest about: that the loan you arrange today may not be the loan that settles in two years, and that the property’s valuation at settlement can land below the price you agreed. That is where off-the-plan purchases go wrong, and it has very little to do with the contract.

This guide covers what buying off the plan actually means, how the finance works, where it breaks, and the NSW rules that protect you. We have arranged off-the-plan loans across Western Sydney since 2001, and the lessons below come from watching settlements go smoothly and watching a few go sideways.

What does buying off the plan mean?

Buying off the plan means signing a contract to purchase a property that has not been built yet, or is only partly built. You commit based on architectural plans, floor layouts, and a schedule of finishes rather than a finished home you can walk through. You pay a deposit to secure it, then the balance at settlement, which only happens once construction finishes and the plan is registered.

That gap between signing and settlement is the whole story. It can run anywhere from twelve months to three years, and almost every risk and benefit of buying off the plan traces back to it.

How off-the-plan finance actually works (and where it goes wrong)

When you buy an established home, the timeline is short. You get pre-approval, you buy, you settle within six to eight weeks, and the loan you were approved for is the loan that funds the purchase.

Off the plan breaks that timeline apart. You sign now and settle much later, so the finance happens in two separate stages with a long, exposed gap in the middle. Understanding those two stages is how you avoid the traps. If you want to line up a home loan that fits your purchase before you sign anything, that conversation should happen before you put pen to a contract, not after.

The deposit: cash deposit vs deposit bond

On exchange you pay a deposit to the developer. In NSW, this is typically around 10% of the purchase price, sometimes negotiable down to 5%, and the balance falls due at settlement once the plan is registered. The deposit is held in a trust or controlled-money account and cannot be released to the developer before settlement, which is one of the protections we cover further down.

Here is the catch with a cash deposit on an off-the-plan purchase. You could be tying up $58,000 or $85,000 of your savings for eighteen months or longer, money you cannot touch and cannot earn much on while you wait. For a lot of buyers, that is the difference between buying now and buying later.

This is where a deposit bond earns its place. A deposit bond is a guarantee from an insurer that stands in for the cash deposit. You pay a fee rather than handing over the cash, the developer accepts the bond as security, and you keep your savings working until settlement. It only works if the developer agrees to it before the contract is signed, so raise it early. A deposit bond does not reduce what you owe; it changes when and how you fund the deposit.

Why your pre-approval won’t last until settlement

This is the single most misunderstood part of buying off the plan, and it is the one we spend the most time explaining.

A pre-approval is a lender’s conditional assessment of how much you can borrow. It is not a guarantee, and it does not last forever. Most pre-approvals are valid for three to six months. An off-the-plan property might not settle for twelve to thirty-six months. The arithmetic does not work: your pre-approval will almost certainly expire long before you need the loan.

That means the loan gets fully assessed again at settlement, against the conditions that exist then, not the ones that existed when you signed. Three things can move in that window:

- Interest rates. Lenders assess your borrowing capacity with a serviceability buffer on top of the actual rate. If rates have risen since you signed, the amount you can borrow can fall, even though your income has not changed.

- Your circumstances. A new car loan, a change of job, a credit card limit increase, a baby on the way. Anything that affects your income or expenses changes how much a lender will advance.

- The property’s valuation. The lender orders a fresh valuation at settlement. If it comes in below the contract price, you have a shortfall to cover, which brings us to the biggest risk of all.

In reality, a pre-approval for an off-the-plan purchase that may not settle until 1 to 2 years in the future is not worth the paper it is written on.

The practical takeaway: an off-the-plan pre-approval is a starting point, not a finish line. The real work is managing the gap between signing and settlement, so the loan is still there when you need it.

The valuation shortfall risk no bank page admits

Here is the risk you will not find spelled out on a single bank’s website, for an obvious reason. The bank cannot tell you its own valuer might value your property below what you agreed to pay, because that would undermine the loan it wants to write.

But it happens, and on off-the-plan purchases, it happens more than people expect. You agree on a price today. The property settles two years later. The lender’s valuer assesses the finished apartment against the market at settlement, and if the local market has softened, or the building came in with smaller rooms or cheaper finishes than the display suite suggested, the valuation can land under the contract price.

When that happens, the lender lends against the lower of the two figures: the valuation, not the price. The difference is yours to find, in cash, at settlement.

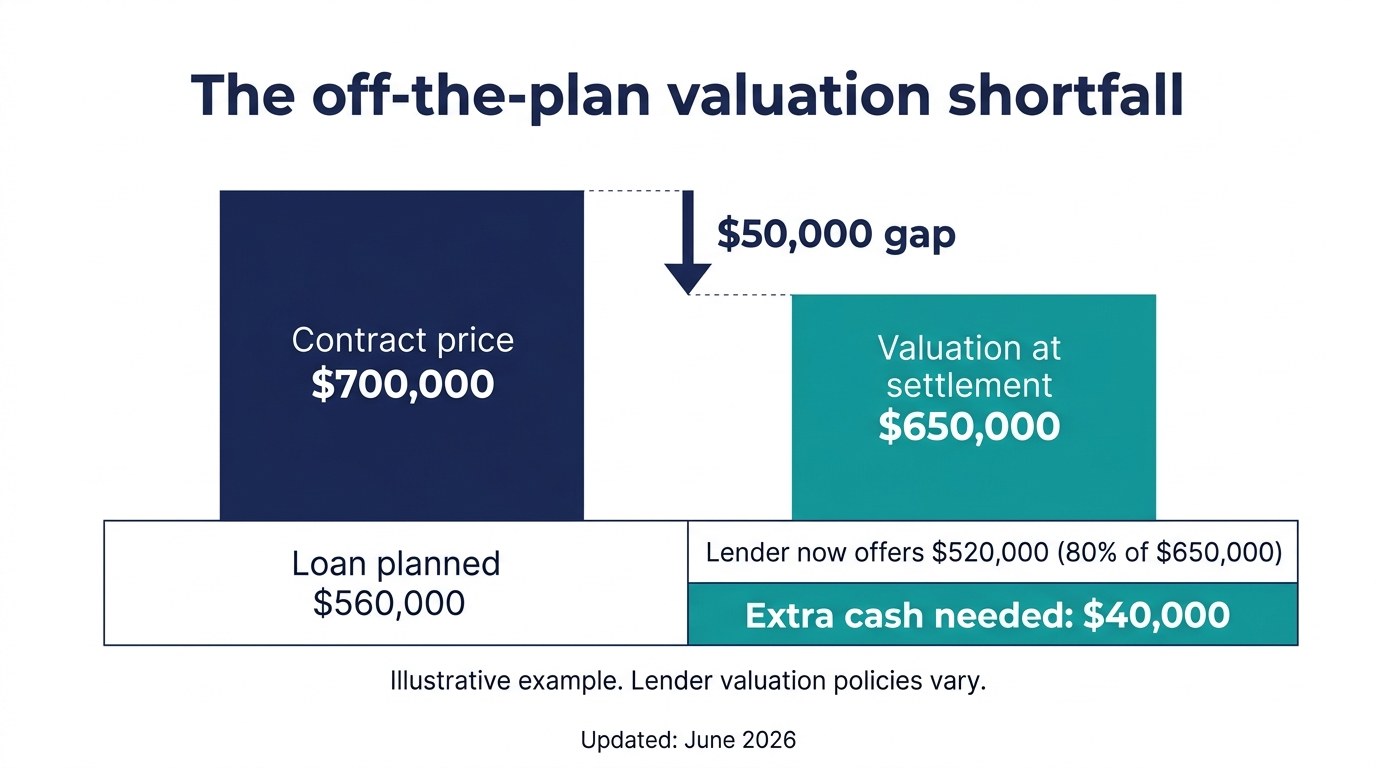

Worked example: a $700,000 Sydney apartment that values at $650,000

Say you signed a contract for a $700,000 apartment with a 20% deposit, planning to borrow the remaining $560,000. That is an 80% loan-to-value ratio (LVR), the amount you borrow divided by the property’s value, and at 80% you avoid lenders mortgage insurance (LMI), the premium lenders charge when you borrow above 80%.

At settlement, the valuation comes back at $650,000, not $700,000. The lender will now lend 80% of $650,000, which is $520,000, not the $560,000 you planned for. You still owe the developer the full $700,000 under the contract. Suddenly, you need to find an extra $40,000 in cash, or borrow above 80% and pay LMI on top.

That $50,000 valuation gap has turned into a $40,000 cash problem at the worst possible moment. It is the scenario that catches off-the-plan buyers most often, and it is almost never their fault.

How a 52+ lender panel mitigates a low valuation

This is where working with a broker rather than a single bank changes the outcome.

Not every lender values the same property the same way, and not every lender treats an off-the-plan valuation the same way. Some assess against the contract price where the contract was signed recently at arm’s length. Some use a more conservative valuer. Some have more appetite for a particular building or postcode than others. The valuation that came in $50,000 light at one lender can come in at the contract price at another.

With access to 52+ lenders, we can place the deal with the lender whose valuation policy and risk appetite suit your specific property, rather than being stuck with whatever a single bank’s valuer returns. We have seen the same Western Sydney apartment valued differently by two lenders in the same week. When a valuation comes in short, the answer is often not more cash; it is the right lender. It is important to choose the right lender from the start, not scramble for one after the valuation disappoints.

Managing the pre-approval gap from contract to settlement

Because the loan is reassessed at settlement, the months between signing and settlement are not dead time. They are when you protect the deal.

A few things make the difference between a settlement that funds smoothly and one that falls over:

- Keep your financial position stable. Avoid new debts, large purchases, job changes, or credit card limit increases between signing and settlement. Each one can lower the amount a lender will advance when they reassess.

- Stay in touch with your broker as settlement nears. A loan should be re-lodged and formally assessed in the weeks before settlement, not the day the developer calls. Building in time lets us solve a valuation or serviceability problem before it becomes a crisis.

- Keep a buffer. Hold more cash than the deposit alone. If the valuation comes in short, a buffer is what stops a shortfall from becoming a default.

Once the property settles and you are in, the loan is not locked in stone either. Rates and your equity position change, and many buyers find it worth reviewing whether to refinance once the property settles onto a sharper rate, especially if they accepted whatever was available under settlement pressure.

Off-the-plan stamp duty in NSW: deferral, not a discount

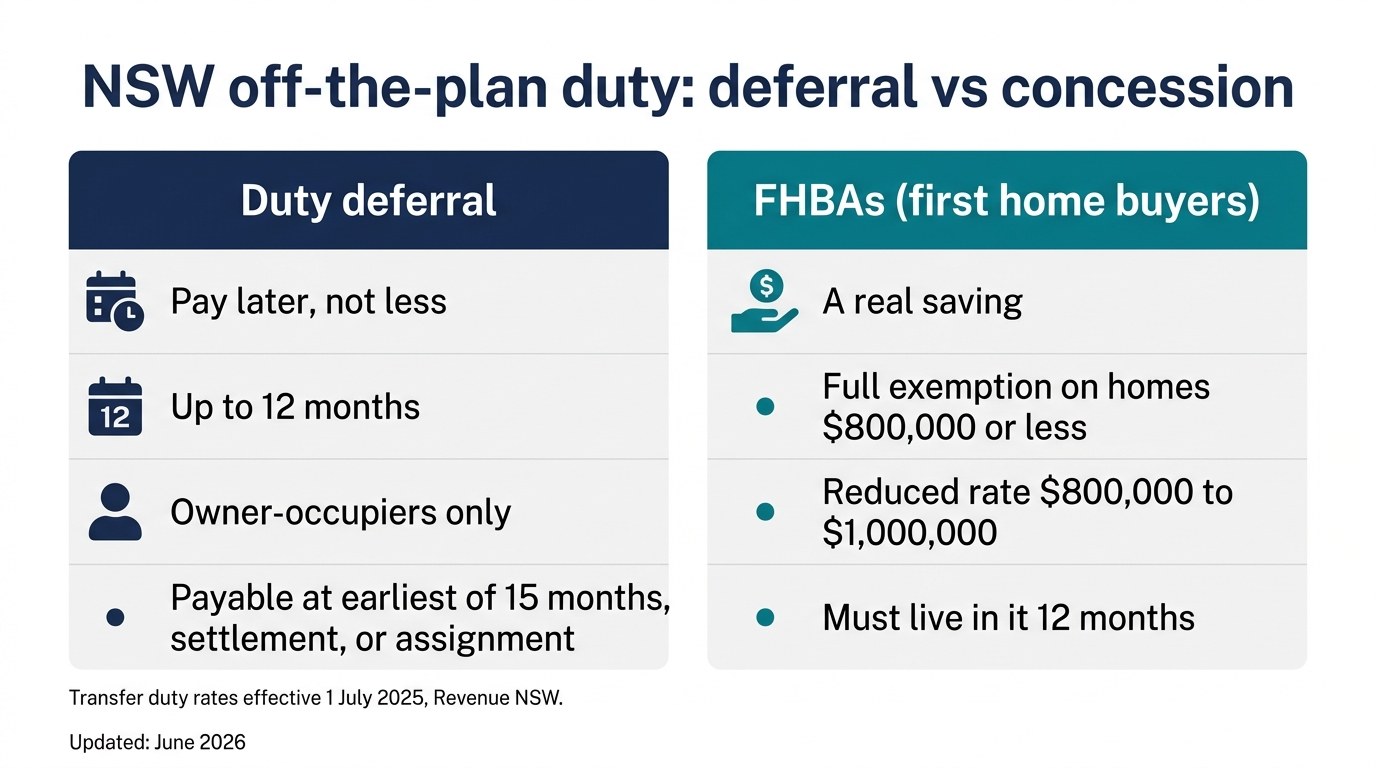

Here is the misconception worth correcting straight away, because a lot of buyers go in believing the opposite. Searches like “tax benefits buying off the plan” and “off-the-plan stamp duty concession” suggest buying off the plan saves you stamp duty in NSW. For most buyers, it does not. What NSW actually offers off-the-plan buyers is a deferral, not a discount.

If you are buying off the plan to live in the property, you may be able to defer transfer duty for up to 12 months under NSW rules. Transfer duty (still widely called stamp duty) is normally payable within three months of signing. The deferral lets you push the payment back, so the duty becomes payable at the earliest of these three points:

- 15 months after you sign the contract (the standard three-month window plus the 12-month deferral), or

- when the property is completed, and settlement occurs, or

- when any part of the contract is assigned to another person.

You still pay the full duty. You just pay it later. You get a timing benefit on the cash, but you owe every dollar all the same. For an off-the-plan buyer, that can still be genuinely useful, because it means you are not paying duty years before you have keys, but it is not the saving people often assume.

Transfer duty figures are based on rates effective 1 July 2025, sourced from Revenue NSW. NSW transfer duty brackets are indexed annually, so confirm current figures before you budget. If you want to see how NSW compares to other states, our guide to how stamp duty compares state by state lays it out.

The 12-month duty deferral and who qualifies

The deferral is for owner-occupiers, not investors. To qualify on a contract exchanged on or after 1 July 2023:

- Each purchaser must be an Australian citizen, a permanent resident, hold a partner (provisional) visa subclass 309 or 820, or be a New Zealand citizen on a subclass 444 visa who has been in Australia at least 200 days in the 12 months before exchange. If any purchaser is a foreign person, the deferral is not available.

- The property must be your principal place of residence. At least one purchaser must move in within 12 months of settlement and live there continuously for at least 12 months.

- It is not available to trusts or companies, and vacant land only qualifies if the contract states a home will be built before settlement.

Permanent members of the ADF who are enrolled to vote in NSW are exempt from the residence requirement, for transactions on or after 19 May 2022.

First home buyers: the FHBAS exemption on off-the-plan purchases

This is the one that is a genuine saving, and it is separate from the deferral. Under the First Home Buyers Assistance Scheme (FHBAS), eligible first home buyers can get a full or partial exemption from transfer duty. That reduces or eliminates the duty itself, rather than just delaying it.

For transactions entered into on or after 1 July 2025, the current FHBAS thresholds for new or existing homes are:

- A full exemption (no duty at all) on homes valued at $800,000 or less.

- A reduced, concessional rate on homes valued above $800,000 and up to $1,000,000.

- Standard duty applies above $1,000,000.

Vacant land has its own thresholds: a full exemption up to $350,000 and a concessional rate between $350,000 and $450,000. As with the deferral, at least one eligible purchaser must move in and occupy the property as their principal place of residence for a continuous 12 months.

The two schemes work independently, and that matters for a first home buyer buying off the plan. You may be able to use the FHBAS to reduce or remove the duty, and defer what is left under the off-the-plan rules. If you are buying your first home, our guide to first home buyer home loans walks through how the deposit, the schemes, and the loan fit together.

Sunset clauses and your NSW legal protections

The legal side of buying off the plan in NSW is genuinely strong, and it has improved a lot since the reforms that took effect on 1 December 2019. Those reforms came through the Conveyancing Act 1919, as amended by the Conveyancing Legislation Amendment Act 2018, and they tightened the rules around disclosure and sunset clauses considerably.

A sunset clause is a date in the contract by which the development must be finished. If it is not, the contract can be rescinded. The old worry was that a developer could deliberately let a project drift past the sunset date, cancel the contracts, and resell the now more valuable apartments at a higher price. NSW closed that loophole. A developer now needs the buyer’s written consent, or an order from the NSW Supreme Court, to rescind under a sunset clause. As a buyer, you do not need court approval to hold the developer to the contract. You can read the NSW Government guidance on buying off the plan for the full set of protections, and the Registrar General’s note on the off-the-plan contract reforms from 1 December 2019 for the detail.

Cooling off, deposit protection and disclosure statements

Several other protections sit alongside the sunset-clause rules:

- Cooling-off period. Off-the-plan contracts carry a 10-business-day cooling-off period, longer than the usual 5 for an established home. If you rescind within it, you forfeit 0.25% of the purchase price.

- Deposit protection. Your deposit is held by the stakeholder in a trust or controlled-money account and cannot be released to the developer before settlement. A bank guarantee or deposit bond can replace cash only if the developer agrees before the contract is signed.

- Disclosure and material particulars. The developer must give you a disclosure statement and a registered plan at least 21 days before settlement. If a material particular changes in a way that adversely affects you, you must be notified, and you then have 14 days to act. If you choose to settle despite the change, you can claim compensation, capped at 2% of the purchase price.

- Building defects. For class-2 apartment buildings, the Building Commission NSW has powers under the RAB Act 2020 to deal with serious defects for up to 10 years after completion. Residential work over $20,000 generally needs Home Building Compensation cover for buildings up to three storeys.

These are real protections, and they are part of why buying off the plan in NSW is less risky than the forum threads suggest. But notice what they protect: your contract, your deposit, your rights against the developer. None of them protects you from a low valuation or an expired pre-approval. That is the finance side, and it is yours to manage.

Why is buying off the plan risky? The honest list

Buying off the plan can work well. It can also go wrong, and the honest answer to “why is it risky?” is that the long gap between signing and settlement exposes you to things you cannot control. The main risks:

- Valuation shortfall. The property values below the contract price at settlement, leaving you to cover the gap in cash or pay LMI.

- The pre-approval gap. Your finance is reassessed at settlement against current rates and circumstances, and the loan you expected may shrink or fall through.

- Market movement. Property values can fall as well as rise over a two-year build, and you are locked into the price you agreed.

- The finished product. The apartment can differ from the display suite or the renders, in size, finish, or outlook.

- Construction and developer risk. Projects run late, and developers can become insolvent before completion.

- Strata surprises. Strata levies and building quality are unknown until the scheme is up and running.

None of this means do not buy off the plan. It means go in with your eyes open, your finance structured to survive a low valuation, and a buffer set aside. The buyers who get burned are almost always the ones who treated the pre-approval as a guarantee and budgeted to the dollar.

Western Sydney case studies

The following are illustrative worked examples based on the kinds of off-the-plan deals we see across Western Sydney. They are not specific clients, and the figures are rounded for clarity.

Case study 1: $580,000 one-bedroom off the plan

A first home buyer on a single income signs for a $580,000 one-bedroom apartment off the plan, due to settle in about 18 months. Rather than tie up a 10% cash deposit ($58,000) for a year and a half, they use a deposit bond to secure the property and keep their savings invested and accessible. We explore the FHBAS, and because the price sits under the $800,000 full-exemption threshold, the transfer duty is removed entirely, a real saving rather than just a deferral.

The risk is the gap. As settlement approaches, we re-lodge the loan, and the valuation comes in close to contract. Because the position was kept stable and the loan was reassessed early with the right lender, the settlement funds without drama. The deposit bond fee, not a year of locked-up cash, was the only cost of waiting.

Case study 2: $850,000 two-bedroom in Parramatta

An upgrading couple signs for an $850,000 two-bedroom apartment in Parramatta, settling roughly two years out. At settlement, the lender’s valuation lands around $60,000 under the contract price, a classic off-the-plan shortfall. With one bank, that gap would have meant finding tens of thousands in extra cash or copping an LMI bill on the higher borrowing.

Instead, we place the loan with a lender on our panel whose valuation came in materially closer to contract, which kept the borrowing within range and avoided both the cash top-up and the LMI blowout. For an upgrader, the equity in an existing property can also help cover a gap; our guide to buying a second home using your equity explains how that works. The lesson is the one we keep coming back to: when a valuation disappoints, the right lender usually solves what extra cash would otherwise have to.

Is buying off the plan a good investment?

For investors, the calculation is different again. Buying off the plan can suit an investor who wants a brand-new property with depreciation benefits and low early maintenance, and who can ride out the construction period. The deferral does not apply to investors, though, since it is reserved for owner-occupiers, and the valuation-shortfall risk is the same or sharper, because an investor often has less appetite to top up a gap in cash.

If you are weighing an off-the-plan apartment as an investment, the finance structure matters as much as the property. Our investment property loans guide covers how lenders assess investment borrowing and where the policies differ. The same rule holds: get the lender right, and keep a buffer for settlement.

How to protect yourself before you sign

Most off-the-plan problems are avoidable if you set things up properly before you sign. A short checklist:

- Get your finance reviewed before you sign, not after. Understand your borrowing capacity, the valuation risk, and which lenders suit the building.

- Ask about a deposit bond if you would rather not tie up cash for the build period.

- Budget for a valuation shortfall. Keep a buffer beyond the deposit so a low valuation is an inconvenience, not a crisis.

- Have your solicitor or conveyancer review the contract, the sunset clause, the disclosure statement, and the deposit arrangements.

- Check the FHBAS and the duty deferral if you are eligible, so you know what you are saving and what you are merely delaying.

- Stay financially stable through to settlement, and re-lodge the loan early.

Buying off the plan in NSW is not the trap the forums make it out to be, but it is not the bargain some buyers expect either. The legal protections are strong. The finance is where the real risk sits, and that is the part you can plan for. If you are considering an off-the-plan purchase in Western Sydney, speak to us before you sign. Getting the finance structured right at the start is what keeps the deal alive at settlement.

Frequently asked questions

What does buying off the plan mean?

Buying off the plan means signing a contract to buy a property that has not been built yet, based on plans and a schedule of finishes rather than a completed home. You pay a deposit on exchange and the balance at settlement, which happens once construction finishes and the plan is registered. That can be anywhere from 12 months to 3 years away.

How much deposit do you need to buy off the plan?

In NSW, the deposit is typically around 10% of the purchase price, paid to the developer on exchange, with the balance due at settlement once the plan is registered. Some developers will negotiate to 5%, and many buyers use a deposit bond instead of cash, so they are not tying up savings for the whole build period.

Is there a stamp duty concession for buying off the plan in NSW?

Not a concession in the usual sense. NSW lets eligible owner-occupiers defer transfer duty for up to 12 months, but you still pay the full amount, just later. The real saving comes from the First Home Buyers Assistance Scheme, which can reduce or remove duty for eligible first home buyers, and which works independently of the deferral.

What happens if the valuation comes in low at settlement?

The lender lends against the lower of the valuation and the contract price, so a low valuation leaves you to cover the shortfall in cash or borrow above 80% and pay LMI. Different lenders value the same property differently, so placing the loan with a lender whose valuation policy suits the building can often close the gap without extra cash.

How long does a pre-approval last for an off-the-plan purchase?

Most pre-approvals are valid for three to six months, while off-the-plan properties can take 12 to 36 months to settle. Your pre-approval will almost always expire before settlement, so the loan is fully reassessed at settlement against the rates, valuation, and circumstances that exist then.

Why is buying off the plan considered risky?

The risk comes from the long gap between signing and settlement. Your finance is reassessed at settlement, the valuation can come in below the contract price, the market can move, and the finished apartment can differ from the renders. The legal protections in NSW are strong, but they do not cover the finance risks, which is the part you need to plan for.

This article contains general information only and does not constitute financial advice. Your personal financial situation, objectives and needs have not been considered. Before acting on any information, you should consider its appropriateness to your circumstances. Speak to a qualified mortgage broker for advice tailored to your situation. Mortgage World Australia Pty Ltd is a credit representative (CR No. 396946) of Mortgage Specialists Pty Ltd (Australian Credit Licence No. 387025).

Patrick O’Brien, Director and Home Loan Specialist since 2001.

Patrick is a Director and a Home Loan Specialist. He has been helping Australians with home loans since 2001. Prior to working as a mortgage broker Patrick was employed by Macquarie Bank for 3 years and also worked as an accountant for a publicly listed company. Patrick’s qualifications include:

Bachelor of Business, UTS Sydney. Majored in accounting and sub-majored in Finance and Marketing.

Diploma of Finance and Mortgage Broking Management FNS50310

Certificate IV in Financial Services (Finance/Mortgage Broking) FNS40804

Ready to Take the Next Step?

Whether you’re looking to buy your first home, refinance, or explore investment opportunities, Mortgage World Australia is here to help.

Fill out the contact form below, and one of our expert mortgage brokers will be in touch shortly to discuss your needs and guide you through your options.

Get Started Today!