Cost of Refinancing in Australia: Every Fee Itemised

Cost of Refinancing in Australia: Every Fee, Itemised

On this page ▾

- What Does It Cost to Refinance a Home Loan in Australia?

- Every Refinancing Cost, Itemised

- Break Costs: The Big One if You Are Mid Fixed Term

- Will Refinancing Re-Trigger LMI?

- Cashback Offers: How Much They Really Knock Off

- Total Cost of Refinancing by Loan Size (Worked Tables)

- How to Work Out Your Break-Even Point

- How to Reduce the Cost of Refinancing

- Is Refinancing Worth It?

- Frequently Asked Questions

Most guides to the cost of refinancing give you a shrug and a range: “anywhere from $500 to a few thousand.” That is not much use when you are deciding whether to switch lenders. The real cost of refinancing a home loan is the sum of a handful of specific line items, and once you see them named with figures, the decision gets a lot clearer.

This guide itemises every fee a broker actually sees at settlement when you refinance, separates the two NSW government charges that catch people out, shows how break costs on a fixed loan are really calculated, and works the total cost of refinancing a home mortgage at $250,000, $500,000 and $750,000, with a break-even figure for each. We have processed these discharges for clients since 2001, so the numbers here are the ones that turn up on the actual statements, not a guess.

What Does It Cost to Refinance a Home Loan in Australia?

Refinancing a home loan in Australia typically costs $400 to $1,500 in upfront fees for a standard owner-occupier. That is mostly your old lender’s discharge fee, two NSW government registration fees of $182.73 each (from 1 July 2026)it the , and any setup fee on the new loan. Break costs on a fixed loan and re-triggered LMI can add far more, so they need their own look.

The itemised table below shows where every dollar goes. The two big variables, break costs and LMI, only apply in specific situations, which is exactly why a flat “$500 to $2,000” range is so unhelpful. Your real number depends on whether you are on a fixed rate and where your loan sits against 80% of your property’s value.

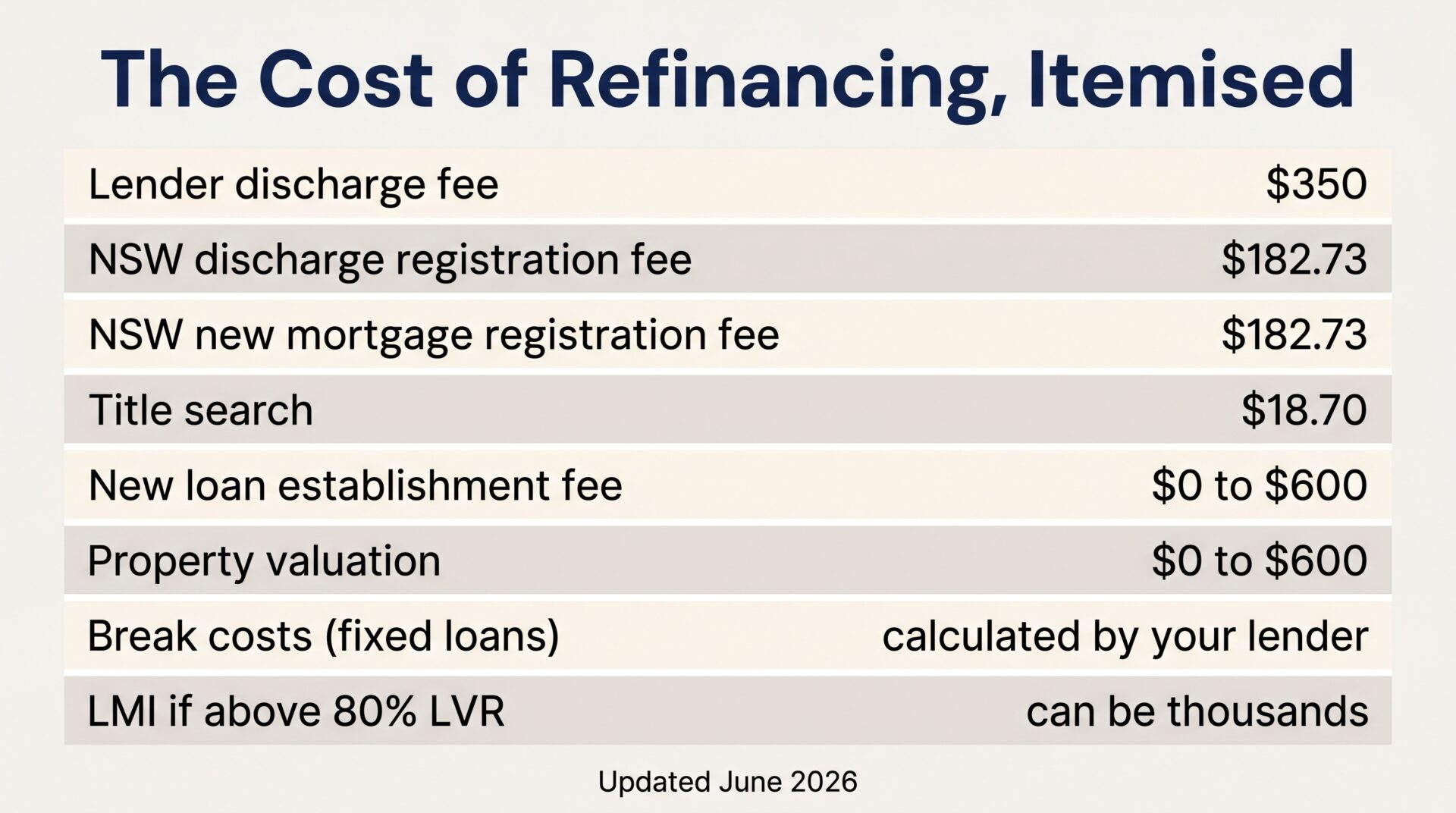

Every Refinancing Cost, Itemised

Here is every line item, with the figure to expect. The two NSW government registration fees are set by NSW Land Registry Services and are the same for everyone. The lender-set fees are ranges because each lender prices them differently, and a good broker can often get several of them waived.

| Cost item | Typical figure | Who sets it |

|---|---|---|

| Lender discharge fee (old loan) | $0 to $400, commonly $350 | Your current lender |

| NSW mortgage discharge registration fee | $182.73 | NSW Land Registry Services |

| NSW new mortgage registration fee | $182.73 | NSW Land Registry Services |

| Title search | About $18.70 (conveyancers may charge $20 to $40) | NSW Land Registry Services |

| New loan establishment / setup fee | $0 to $600 (sometimes up to $1,000 with smaller lenders) | Your new lender |

| Property valuation | $0 for most owner-occupiers; $200 to $600 if charged | Your new lender |

| Break costs (fixed loans only) | Calculated by your lender, can be substantial | Your current lender |

| LMI (if new loan is above 80% LVR) | Thousands, sometimes tens of thousands | Insurer, via new lender |

Discharge fee from your current lender ($0 to $400)

When you leave a lender, they charge a discharge fee to cover the admin of closing your loan and releasing the mortgage. Westpac charges $350, and that is a fair benchmark across the big banks. Some lenders waive it, others charge up to $400. This is separate from the government registration fee below, which trips a lot of people up. Understanding the mortgage discharge process before you start makes the timing and the paperwork far less stressful.

NSW mortgage discharge registration fee ($182.73)

This is a government fee, not a bank fee. To remove your old lender’s mortgage from your property title, the discharge of mortgage has to be registered with NSW Land Registry Services. The sthe tandard dealing fee for that is $182.73, including GST.

NSW Land Registry Services fees are reviewed every year on 1 July. The figures here are effective from 1 July 2026 ($182.73 per dealing, GST inclusive), sourced from NSW Land Registry Services. Dealings lodged before 1 July 2026 are charged the 2025/26 fee of $175.70 each.

NSW new mortgage registration fee ($182.73)

When your new lender’s mortgage is registered against the title, that is a second, identical dealing at $182.73. People often expect “the registration fee” to be a single charge. On a refinance to a new lender, you pay it twice, once to remove the old mortgage and once to register the new one. That is about $365 in government fees alone from 1 July 2026 (2 x $182.73), set under the Real Property Regulation and administered by the NSW Registrar General as the ,regulator. If you refinance internally with your existing lender and the mortgage is varied rather than discharged and re-registered, you may avoid one or both of these.

Title search (about $18.70)

A title search confirms who is on the title and what is registered against it. The official NSW Land Registry Services title search is about $18.70. If your conveyancer or solicitor orders it for you, they may on-charge $20 to $40 as a disbursement to cover their handling. Small either way, but it belongs on the list.

New loan establishment / setup fee ($0 to $600)

Your new lender may charge an establishment or application fee to set up the loan. For the major banks,securities this runs $0 to $600. It is often waived on packaged or basic products, and lenders frequently waive it entirely to win refinance business. Some smaller or non-bank lenders go higher, occasionally up to $1,000, so always check the specific product. This is one of the fees we routinely get waived for clients across our panel of 52+ lenders.

Property valuation ($0 for most owner-occupiers)

The new lender needs to value your property to confirm the loan-to-value ratio (LVR), which is your loan amount divided by the property’s value, written as a percentage. For a standard owner-occupier refinance, the lender usually orders an automated or desktop valuation and absorbs the cost, so you pay $0. A full valuation, more common on investment properties or unusual securities, can cost $200 to $600 if you are charged for it.

Break Costs: The Big One if You Are Mid Fixed Term

If you are partway through a fixed-rate term, break costs are the single most important number in your decision, and the one most likely to be misunderstood. A break cost is not a flat fee. It can be a few hundred dollars or tens of thousands, depending on your loan and what wholesale interest rates have done since you fixed.

How break costs are actually calculated

When you fix a rate, your lender effectively locks in funding at the wholesale (swap) rate of the day. If you break the fixed term early and wholesale rates have fallen since you fixed, the lender loses the margin it expected, and the break cost recovers that loss. The calculation, sometimes called the economic cost, multiplies the difference between the wholesale rate when you fixed and the current wholesale rate, by your remaining fixed term, by your loan balance, then converts that to today’s dollars.

In plain terms: the more your loan balance, the longer your remaining fixed term, and the further wholesale rates have fallen since you fixed, the bigger the break cost. If wholesale rates have risen since you fixed, your break cost can be close to zero. Only your lender can quote the exact figure, and the quote is usually valid for just a couple of business days. ASIC’s Moneysmart switching home loans guide is a good neutral reference and links to a switching calculator.

Worked example: breaking a fixed rate early

Take a $500,000 balance with 2 years left on a fixed term, where wholesale rates have fallen about 1% since you fixed. As a rough illustration, the lender’s loss is in the order of 1% of $500,000 per year, for 2 years, which points to a break cost in the low five figures, around $10,000. This is illustrative only. The inputs that matter are your balance, your remaining fixed term, and the movement in wholesale rates, and your lender does the precise sum. The lesson: if you are on a fixed rate, always ask your lender for a break-cost quote before you do anything else. It can change the entire decision.

Will Refinancing Re-Trigger LMI?

Lenders Mortgage Insurance (LMI) is a one-off insurance premium that protects the lender, not you, when your loan is above 80% of the property’s value. LMI only applies above 80% LVR. If your new loan sits at or below 80% LVR, this section does not apply to you. If it sits above, LMI can be the single largest cost of refinancing, easily dwarfing every other line item.

The catch is that LMI is not transferable between lenders. If you paid LMI on your current loan and you refinance above 80% LVR, you generally pay it again with the new lender. You cannot carry the old policy across. You may be able to claim a partial refund of the original premium if you switch early, so it is worth asking your current lender.

Worked example: pushing a $400,000 loan above 80% LVR

Say your property is valued at $480,000 and you want to refinance a $400,000 loan. That is an LVR of $400,000 / $480,000, or about 83%. Because that is above 80%, the new lender will require LMI, which on a loan this size can run into several thousand dollars. Knowing your equity position before you apply is critical, and our guide to how much you can borrow walks through how lenders assess it. If you are close to the 80% line, even a small extra repayment or a higher valuation can keep you under it and save the LMI entirely.

Cashback Offers: How Much They Really Knock Off

Lenders sometimes run refinance cashback offers to win your business, and when they do, they typically sit in the $2,000 to $4,000 range. A $3,000 cashback comfortably covers the full upfront cost of a standard owner-occupier refinance, which is the whole point: the lender is buying your loan. Offers come and go, and most majors withdrew their cashbacks in 2023 and 2024, so never assume one is available. Our guide to refinance cashback offers tracks what is current. Just be sure the loan stacks up on rate and features once the cashback is spent. A one-off $3,000 means little if the ongoing rate is half a percent higher.

Total Cost of Refinancing by Loan Size (Worked Tables)

Here is what the upfront cost actually adds up to at three common loan sizes, with a net cost after a typical cashback and a break-even figure. Each table assumes a standard owner-occupier refinance below 80% LVR (so no LMI), no fixed-rate break cost, the lender absorbing the valuation, and the new lender waiving the setup fee, which is a realistic outcome when a broker negotiates. Government fees use the figures effective 1 July 2026.

The break-even is the net cost divided by your monthly interest saving. These assume a 0.50% rate reduction, which is a conservative, illustrative figure. Your actual saving depends on the gap between your old and new rate.

Refinancing a $250,000 home loan

| Item | Amount |

|---|---|

| Lender discharge fee | $350 |

| NSW discharge registration | $182.73 |

| NSW new mortgage registration | $182.73 |

| Title search | $18.70 |

| Establishment fee (waived) | $0 |

| Valuation (lender-absorbed) | $0 |

| Total upfront cost | $734.16 |

| Less typical cashback | $3,000 |

| Net cost | You are ahead by about $2,266 |

| Monthly saving at 0.50% on $250,000 | About $104 |

| Break-even | Immediate (cashback covers the cost) |

At this loan size a typical cashback more than covers every fee, so you are in front from day one and a 0.50% rate cut saves roughly $1,250 in interest over the first year.

Refinancing a $500,000 home loan

| Item | Amount |

|---|---|

| Lender discharge fee | $350 |

| NSW discharge registration | $182.73 |

| NSW new mortgage registration | $182.73 |

| Title search | $18.70 |

| Establishment fee (waived) | $0 |

| Valuation (lender-absorbed) | $0 |

| Total upfront cost | $734.16 |

| Less typical cashback | $3,000 |

| Net cost | You are ahead by about $2,266 |

| Monthly saving at 0.50% on $500,000 | About $208 |

| Break-even | Immediate (cashback covers the cost) |

The fees are the same as at $250,000 because most of them are flat, government-set charges. The saving doubles, so a 0.50% rate cut here is worth roughly $2,500 in the first year on top of the cashback.

Refinancing a $750,000 home loan

| Item | Amount |

|---|---|

| Lender discharge fee | $350 |

| NSW discharge registration | $182.73 |

| NSW new mortgage registration | $182.73 |

| Title search | $18.70 |

| Establishment fee (waived) | $0 |

| Valuation (lender-absorbed) | $0 |

| Total upfront cost | $734.16 |

| Less typical cashback | $3,000 |

| Net cost | You are ahead by about $2,266 |

| Monthly saving at 0.50% on $750,000 | About $313 |

| Break-even | Immediate (cashback covers the cost) |

If no cashback is available, the picture still works quickly: at $750,000 a 0.50% rate cut saves about $313 a month, so the $734 in fees pays for itself in roughly 2.3 months. The bigger the loan, the faster refinancing pays off, which is why it is so often worth it on larger balances even without an offer.

How to Work Out Your Break-Even Point

The break-even point is the moment your interest savings have covered the cost of switching. The maths is simple: add up your total upfront cost, subtract any cashback to get your net cost, then divide that net cost by your monthly interest saving. The answer is how many months until refinancing has paid for itself.

For example, if your net cost is $734 and your new rate saves you $200 a month, your break-even is $734 / $200, or about 3.7 months. After that, the savings are yours to keep. This is the right way to decide whether to refinance, and it is far more reliable than any blanket rule. You may have heard of the “2% rule”, the idea that you should only refinance if you can drop your rate by 2%. That is an American convention with no basis in Australian lending. A 0.30% saving on a large loan can be well worth it, while a 2% saving on a tiny balance near the end of its term may not be. Work the break-even, not a rule of thumb. If break costs or LMI apply, add them to your upfront cost before you divide. That is exactly where break-even maths saves people from an expensive mistake.

How to Reduce the Cost of Refinancing

Most of the avoidable cost of refinancing sits in the lender-set fees, and that is where a broker earns their keep:

- Get the setup and application fees waived. Lenders competing for your loan will often drop them entirely.

- Use the lender’s free valuation. For standard owner-occupier loans, the valuation is usually absorbed, so there is no reason to pay for one.

- Time a fixed-rate switch carefully. If you are on a fixed rate, get a break-cost quote first. Waiting until the fixed term ends can save the entire break cost.

- Stay at or under 80% LVR. Keeping your loan below 80% of the property value avoids LMI, the largest single cost. A higher valuation or a small extra repayment can get you there.

- Capture a cashback when one is on offer, but judge the loan on its ongoing rate, not the one-off payment.

With access to 52+ lenders, we can line up which ones are currently waiving fees and running cashbacks, and match that against the rate and features you actually need.

Is Refinancing Worth It?

For most borrowers with a reasonable loan balance, refinancing is worth it, because the upfront cost is modest, often a few hundred dollars after a cashback, while the interest saving compounds for years. The honest answer, though, is that it depends on three things: whether you are on a fixed rate with break costs, whether your loan is above 80% LVR and would re-trigger LMI, and how big the rate gap is. Run the break-even and you will know.

The trap is loyalty. Staying with your existing lender out of habit can quietly cost you thousands a year if your rate has drifted above the market. The best way to check is to compare your current rate against the market on a like-for-like basis, which means looking at the comparison rate, the figure that includes most fees so you can compare loans fairly. Our explainer on how comparison rates work shows how to read them, and you can start the numbers with our guide to refinancing your home loan.

Refinancing should save you money, not surprise you with costs. Talk to a mortgage broker at Mortgage World Australia and we will run the numbers on your loan, including any break costs and LMI, before you switch. Explore our home loan options to see where to start.

Frequently Asked Questions

How much does it cost to refinance in Australia?

For a standard owner-occupier, expect $400 to $1,500 in upfront fees: your old lender’s discharge fee (commonly $350), two NSW government registration fees of $182.73 each, a small title search, and any setup fee on the new loan, which is often waived. Break costs on a fixed loan and re-triggered LMI can add far more, so get those quoted if they apply.

What are the government fees to refinance in NSW?

Two NSW Land Registry Services dealing fees of $182.73 each (effective 1 July 2026; $175.70 each for the 2025/26 year): one to register the discharge of your old mortgage and one to register your new lender’s mortgage. That is about $365 in total government fees. A title search adds about $18.70. These are set by NSW Land Registry Services and are the same for every borrower.

Do I pay LMI again when I refinance?

Only if your new loan is above 80% of the property’s value. LMI applies above 80% LVR, and it is not transferable between lenders, so refinancing above 80% generally means paying it again. If your loan is at or below 80% LVR, no LMI applies. You may be able to claim a partial refund of your original premium if you switch early, so ask your current lender.

How are break costs calculated?

Break costs on a fixed loan are not a flat fee. Your lender calculates an economic cost based on your loan balance, your remaining fixed term, and how far wholesale interest rates have moved since you fixed. If rates have fallen, the cost can be substantial; if they have risen, it can be near zero. Only your lender can give you the exact figure, usually valid for a couple of business days.

Can I refinance my home loan with the same bank?

Yes. You can refinance internally by moving to a different product with your current lender, which can avoid the discharge and re-registration fees because the mortgage is varied rather than discharged. The downside is that you only see one lender’s pricing. Switching to another lender opens up the whole market, which is often where the bigger savings are. A broker can compare both paths for you.

How long until refinancing pays for itself?

Divide your net cost (upfront fees minus any cashback) by your monthly interest saving. If a cashback covers your fees, you are ahead immediately. Without one, a 0.50% rate cut on a $500,000 loan saves about $208 a month, so $734 in fees pays off in under 4 months. Larger loans break even faster.

This article contains general information only and does not constitute financial advice. Your personal financial situation, objectives and needs have not been considered. Before acting on any information, you should consider its appropriateness to your circumstances. Speak to a qualified mortgage broker for advice tailored to your situation. Mortgage World Australia Pty Ltd is a credit representative (CR No. 396946) of Mortgage Specialists Pty Ltd (Australian Credit Licence No. 387025).

Patrick is a Director and a Home Loan Specialist. He has been helping Australians with home loans since 2001. Prior to working as a mortgage broker Patrick was employed by Macquarie Bank for 3 years and also worked as an accountant for a publicly listed company. Patrick’s qualifications include:

Bachelor of Business, UTS Sydney. Majored in accounting and sub-majored in Finance and Marketing.

Diploma of Finance and Mortgage Broking Management FNS50310

Certificate IV in Financial Services (Finance/Mortgage Broking) FNS40804

Ready to Take the Next Step?

Whether you’re looking to buy your first home, refinance, or explore investment opportunities, Mortgage World Australia is here to help.

Fill out the contact form below, and one of our expert mortgage brokers will be in touch shortly to discuss your needs and guide you through your options.

Get Started Today!