Negative Gearing Changes 2026: Investor Guide

On 12 May 2026, Treasurer Jim Chalmers delivered a Federal Budget that will reshape property investment in Australia. The negative gearing changes announced that night are the most significant reform to residential investment taxation in decades. Combined with new capital gains tax rules and a minimum tax on discretionary trusts, the package changes the numbers for most investors assessing their next purchase.

This guide covers what has actually changed, what is protected, how the 12 May 2026 cut-off works in practice, and what these changes mean for your borrowing capacity right now.

What the 2026 Federal Budget actually changes for property investors

On this page ▾

Three reforms at a glance

| Reform | What changes | Start date |

|---|---|---|

| Negative gearing | Restricted to new residential builds for post-cut-off properties | 1 July 2027 |

| Capital gains tax | 50% discount replaced by cost-base indexation plus 30% minimum tax floor | 1 July 2027 |

| Discretionary trust tax | 30% minimum tax on trust income paid at trustee level | 1 July 2028 |

Three things to understand before going further. First, properties you already own are fully grandfathered: negative gearing continues exactly as before until you sell. Second, new residential builds remain fully negatively gearable under the new rules. Third, the cut-off for grandfathering protection was 7:30 PM AEST on 12 May 2026, the exact moment the Budget was handed down.

For background on how negative gearing currently works, our full guide covers the mechanics in detail.

The 12 May 2026 cut-off explained

What “7:30 PM AEST on 12 May 2026” means in practice

The precise time the Treasurer rose to deliver the Budget speech is the dividing line between the old system and the new. Properties you held at that moment are grandfathered. Properties you purchase after that moment will be subject to the quarantine rules from 1 July 2027.

The official Treasury factsheet uses consistent language throughout: “Properties held at announcement (including where a contract has been entered into, but not yet settled) will be allowed to be negatively geared in future years until sold.”

This means the cut-off is not settlement date. It is the date and time the contract was entered into.

What if I had a contract signed before the cut-off?

If you signed a contract to purchase an investment property before 7:30 PM AEST on 12 May 2026 and that property has not yet settled, your property qualifies for grandfathering. The Treasury factsheet treats a signed, unsettled contract as equivalent to holding the property at the time of announcement.

One point the factsheet does not resolve: whether a conditional contract (one that was still subject to finance or building inspection at 7:30 PM on Budget night) qualifies in the same way as an unconditional contract. The phrase used is “contract entered into,” without any qualification on conditionality. Draft legislation is expected to clarify this. If your pre-cut-off contract had outstanding conditions at the time of the Budget, speak to a tax adviser before assuming grandfathering applies.

Negative gearing changes (from 1 July 2027)

What gets quarantined and what stays

From 1 July 2027, rental losses on established residential investment properties bought on or after 7:30 PM AEST 12 May 2026 will be quarantined. Instead of deducting those losses against wages and salary, you can only deduct them against residential property income. This includes rent from other investment properties and, importantly, capital gains when you sell a residential property.

In practice: if your post-cut-off investment property runs at a $12,000 annual loss and you earn $150,000 in wages, that $12,000 cannot reduce your taxable wage income under the new rules. The loss is set aside, carried forward, and can only be used when you have residential property income to absorb it.

The losses are not forfeited. They accumulate year on year and can be used to reduce the capital gain in the year you sell the property.

New-build investment property: negative gearing is still fully available

The single most important carve-out in the Budget: new residential builds are fully exempt from the negative gearing changes. If you invest in a qualifying new build, your losses remain deductible against wages and other income, exactly as they are today.

From a financing and tax perspective, this makes new builds significantly more attractive for investors acquiring property after the cut-off date.

What qualifies as a “new build” (and what doesn’t)

The definition turns on one question: does the property genuinely add new housing supply? The Treasury factsheet is specific.

Qualifies as a new build:

- A newly constructed apartment bought off-the-plan

- Any residential construction on previously vacant land

- A duplex replacing a single house (supply increases from one dwelling to two)

- A property occupied for less than 12 months before its first sale

Does not qualify:

- A knock-down rebuild replacing one house with one house (no net supply increase)

- An extension adding bedrooms to an existing property

- A granny flat added to an established, non-qualifying property

- A property occupied for more than 12 months before first sale

One rule that catches investors: the new-build benefit applies to the first purchaser only. If you buy a property that was originally purchased new by another investor, you cannot access negative gearing or the CGT discount choice on that property. The supply-addition benefit attaches to the original buyer, not subsequent resales.

SMSFs, commercial property, widely-held trusts: the other exclusions

The changes do not apply to SMSFs, commercial property, or widely-held trusts:

- SMSFs: superannuation funds, including self-managed superannuation funds, are excluded from the changes. SMSF property investment continues under existing arrangements.

- Commercial property: the negative gearing changes apply to residential property only. Commercial property investors retain full existing deductibility.

- Widely held trusts: most managed investment trusts, including listed property trusts and REITs, are excluded.

How carry-forward losses work in the new system

Under the quarantine model, any losses that exceed your available residential property income in a given year are carried forward automatically. There is no time limit.

When you sell the property, remaining carry-forward losses reduce the capital gain in that year. The Treasury factsheet illustrates this with a worked example: an investor accumulates carry-forward losses over several years and uses them to reduce the taxable gain at sale.

For investors planning to hold for the long term and sell at a gain, the losses are not wasted. The tax benefit is deferred, not eliminated. The cash-flow and year-to-year tax position changes materially compared with the current system, but the economics of the investment are not as different at sale as the headlines suggest.

Capital gains tax: from 50% discount to indexation

The 30% minimum tax floor explained

From 1 July 2027, the 50% CGT discount will no longer apply to gains accruing after that date. Instead, gains are reduced by CPI-based cost-base indexation (the same method used from 1985 to 1999) and then subject to a 30% minimum tax floor.

The minimum floor means that regardless of your marginal tax rate, you will pay at least 30% on the real, inflation-adjusted gain. For investors in the top tax bracket, indexation will often produce a lower taxable amount than the 50% discount, depending on the inflation rate and holding period. For investors in lower tax brackets, the 30% minimum may represent a higher effective rate than the old discount did. That is the counterintuitive catch most commentary has missed.

These changes apply to all CGT assets: property, shares, and other investments held by individuals, partnerships, and trusts. This is not a residential-property-only measure.

For a full breakdown of capital gains tax on investment property, our guide covers the existing rules, with the 2026 Budget changes noted.

Cost-base reset at 1 July 2027: why the valuation matters

For existing property owners, the transition rules create a clean split at 1 July 2027.

The gain from your original purchase price to the property’s market value at 1 July 2027 is still taxed under the existing 50% CGT discount. The gain from 1 July 2027 to your eventual sale price is taxed under the new indexation rules.

To apply this split, you need to establish what your property was worth at 1 July 2027. The ATO will offer two methods:

- A formal independent valuation as at 1 July 2027

- An ATO apportionment formula that estimates the 1 July 2027 value based on the property’s growth rate across the full holding period

Getting a valuation in place well before July 2027 is worth planning now. The difference between a high and low valuation at the reset date directly affects how much of your future gain falls under the more favourable pre-2027 discount.

Pre-2027 vs post-2027 gains: split treatment for existing properties

The Treasury factsheet provides a worked example to illustrate. An investor buys a property for $800,000 in 2022. They sell it for $1,600,000 in 2032. ATO tools establish the 1 July 2027 value was $1,131,371.

- Pre-2027 gain: $1,131,371 minus $800,000 = $331,371. Apply 50% CGT discount. Taxable amount: $165,685.

- Post-2027 gain: $1,600,000 minus $1,131,371 = $468,629. Reduced by CPI indexation and subject to 30% minimum floor.

The total tax outcome blends both regimes. The exact result depends on your marginal rate, CPI between 2027 and 2032, and whether the minimum floor applies.

Discretionary trust changes (from 1 July 2028)

The 30% minimum tax at trustee level

If you hold investment property through a discretionary trust structure, a separate measure takes effect from 1 July 2028.

Discretionary trusts will be subject to a 30% minimum tax on their taxable income, paid by the trustee. The stated intent is to stop income splitting: parking trust distributions with lower-tax-rate beneficiaries to shrink the family’s tax bill.

Treasury is still consulting on how the collection mechanism will work. The policy direction is locked in; the mechanics are not.

Beneficiary tax credits: what investors still get back

Non-corporate beneficiaries (individuals and most other entities receiving trust distributions) will receive non-refundable tax credits for the trustee-level tax paid. These credits reduce your personal income tax payable on the distribution.

The credits are non-refundable. If the credit exceeds your tax liability, the difference is not returned to you as cash. The design ensures the combined effective rate does not fall below 30%, without creating double taxation.

Corporate beneficiaries are specifically excluded from credits. This prevents the minimum tax from being converted into refundable franking credits.

For investors currently holding property through a discretionary trust, the three-year period from 1 July 2027 offers CGT rollover relief for restructuring into a company or fixed trust without triggering a CGT event. Reviewing your investment property ownership structure with a tax adviser before mid-2027 is worth scheduling now.

What this means for your borrowing capacity

How these changes in negative gearing will affect your borrowing capacity is something that I haven’t seen discussed.

How lenders currently factor negative gearing into serviceability

When a lender assesses your borrowing capacity for an investment property, most of them don’t simply compare your income against your expenses. They add back the tax saving from a negatively geared property and treat it as effective income for the purposes of their serviceability calculation.

The reasoning is sound: if your investment property runs at a $15,000 annual loss but your resulting tax refund is $6,750, your real cash-flow cost is $8,250, not $15,000. Lenders who factor this in calculate a higher borrowing capacity than lenders who don’t.

For interest-only investment property loans, this add-back has historically made a meaningful difference to the maximum loan amount an investor qualifies for.

Why some applications are already being declined post-12 May

Here is what many investors don’t know yet: lenders are already adjusting. We are aware of at least one application declined in the days immediately following the Budget because the property’s contract of sale was signed after 7:30 PM on 12 May 2026. That lender advised that negative gearing benefits would not be factored into the serviceability assessment for a post-cut-off property.

No lender has formally published a policy update. But the market signal is clear: lenders are beginning to distinguish between pre-cut-off properties (where negative gearing is preserved and the add-back remains) and post-cut-off established properties (where negative gearing will be quarantined from 1 July 2027, and the add-back is at risk).

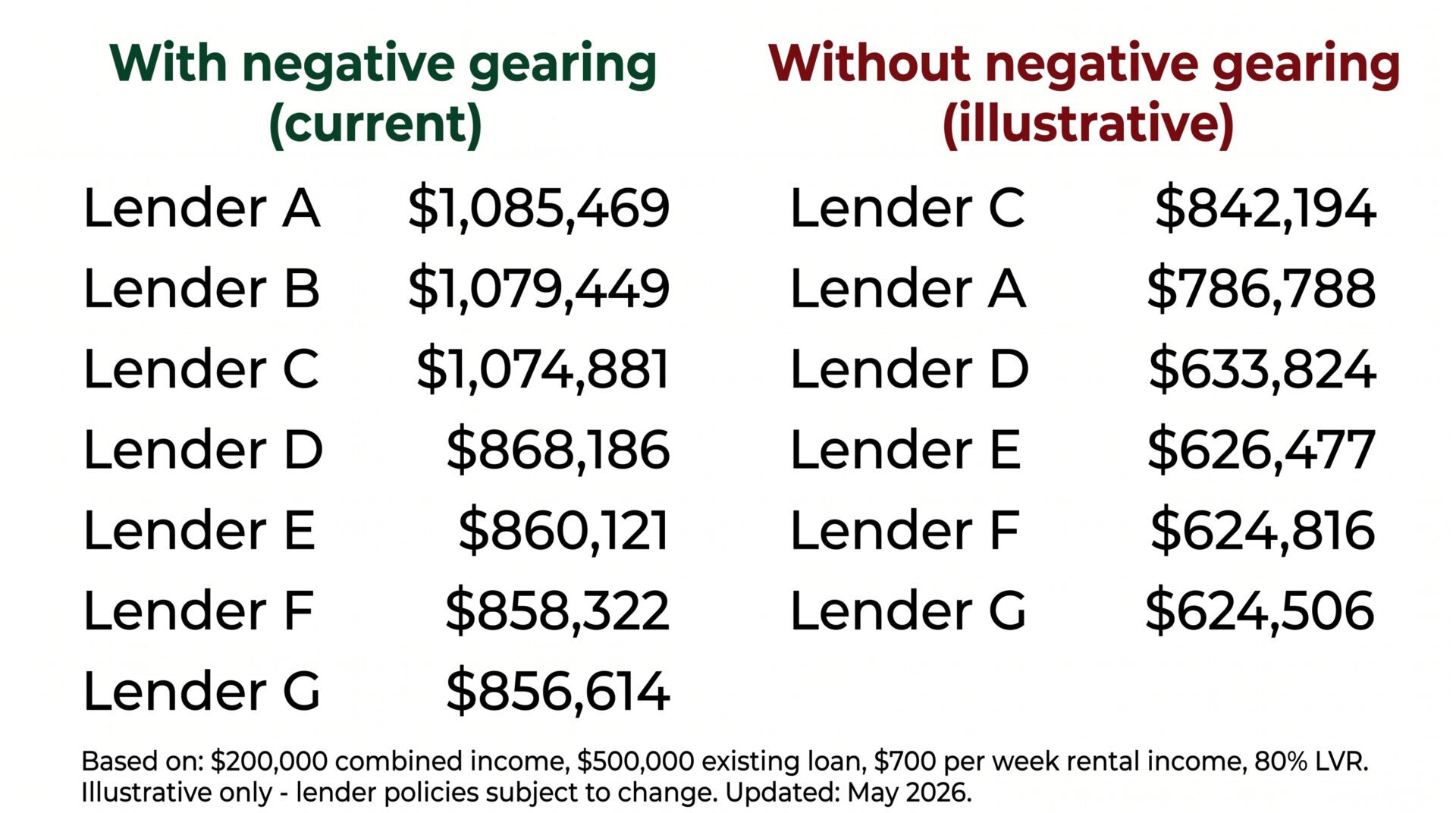

To illustrate the impact, we ran a serviceability comparison for a typical Western Sydney investor couple. Profile: combined gross income of $200,000 ($100,000 each), an existing owner-occupied loan of $500,000 at 6% per annum with 25 years remaining, a $10,000 credit card limit, $4,000 in monthly living expenses, and proposed rental income of $700 per week, borrowing at 80% LVR.

With negative gearing factored in (current approach, pre-cut-off properties):

| Max borrowing capacity | |

|---|---|

| Lender A | $1,085,469 |

| Lender B | $1,079,449 |

| Lender C | $1,074,881 |

| Lender D | $868,186 |

| Lender E | $860,121 |

| Lender F | $858,322 |

| Lender G | $856,614 |

Without the negative gearing add-back (illustrative projection for post-cut-off properties):

| Max borrowing capacity | |

|---|---|

| Lender C | $842,194 |

| Lender A | $786,788 |

| Lender D | $633,824 |

| Lender E | $626,477 |

| Lender F | $624,816 |

| Lender G | $624,506 |

These are not confirmed lender policies. No lender has announced a formal change to their serviceability calculators. These figures show what happens mechanically when the negative gearing add-back is removed from the calculation for this borrower profile. The reduction is approximately $233,000 to $299,000, or roughly 27%, depending on the lender’s model.

What we expect lenders to change in the coming weeks

Most lenders will take four to eight weeks to settle their position on this. Based on what we are seeing now:

- Pre-cut-off properties: serviceability assessed as today, with the negative gearing add-back intact

- Post-cut-off established properties: the add-back is likely to be removed or reduced, either from 1 July 2027 or more immediately for conservative lenders

- New builds: add-back retained, as negative gearing remains fully available on new builds

If you are assessing an investment loan right now and the property is post-cut-off, this is exactly the period where lenders will diverge in their approach. Access to how much you can borrow varies significantly across the 52+ lenders we work with, and that gap is about to widen.

What to do in the next 90 days

Already own property bought before the cut-off? No urgent action required on negative gearing itself. The most valuable thing you can do now is plan for the 1 July 2027 CGT cost-base reset. Organise a valuation at or around that date, keep records, and ask your accountant which method, formal valuation or ATO apportionment formula, will produce the better result for your situation.

Buying a new investment property after the cut-off? New builds are now the most tax-efficient path. They retain full negative gearing and give you the choice between the 50% CGT discount and the new indexation method at sale. The serviceability advantage, with lenders retaining the add-back for new builds, is likely to compound the tax advantage over the next 12 to 24 months. Lender selection matters more than usual right now.

Holding through a discretionary trust? A three-year CGT rollover period runs from 1 July 2027 (ending 30 June 2030), allowing restructuring into a company or fixed trust without triggering a CGT event. That window extends well beyond the 1 July 2028 trust minimum tax commencement, so there is time to plan properly. Review your investment property ownership structure with a tax adviser before mid-2027. If you also want to refinance your home loan or restructure your debt at the same time, flag that early, as it affects both your borrowing capacity and your options.

If you have a contract signed after 12 May or you are assessing a new build right now, speak to us. Lender policies are diverging faster than most investors realise, and the right lender choice will make a meaningful difference over the next 12 months. Our mortgage brokers have access to 52+ lenders and have been working with Western Sydney investors since 2001.

Frequently asked questions

Is negative gearing being abolished in Australia?

No. Negative gearing is not being abolished. From 1 July 2027, negative gearing on new purchases of established residential investment properties bought after 7:30 PM AEST 12 May 2026 will be quarantined: losses can only be deducted against residential property income, not wages or salary. Negative gearing on new builds remains fully available. Properties held at the Budget announcement are grandfathered.

Can I still negatively gear a new build after the 2026 Budget?

Yes. New residential properties that genuinely add to housing supply remain fully negatively gearable. Off-the-plan apartments, newly constructed homes on vacant land, and duplexes replacing a single dwelling all qualify. The full deduction against wages and other income is retained for new-build investors.

What happens to my carry-forward rental losses when I sell?

Carried-forward rental losses on quarantined properties can be used to offset the capital gain when you sell. The Treasury factsheet confirms this explicitly: losses carried forward reduce residential property income in the year of sale, which includes the capital gain from that property. The losses accumulate until you have residential property income to absorb them.

Is the CGT discount grandfathered in the 2026 Budget?

Partially. For assets held before 1 July 2027, the capital gain accrued up to that date is still taxed under the existing 50% CGT discount. Only gains accruing from 1 July 2027 onwards are subject to the new indexation method and 30% minimum tax floor. You need to establish your property’s market value at 1 July 2027 to apply this split treatment when you eventually sell.

How does the 12 May 2026 cut-off affect my loan application right now?

Lenders are beginning to assess this. We are aware of at least one application declined after the Budget because the lender would not factor in negative gearing benefits for a property purchased after the cut-off. While lender policies have not yet been formally updated, the practical impact on borrowing capacity can be a reduction of around $233,000 to $299,000 for a typical investor profile, depending on the lender’s serviceability model.

The Budget measures discussed in this article had not been legislated as at 14 May 2026. Final details may change before commencement on 1 July 2027 (negative gearing and capital gains tax) and 1 July 2028 (discretionary trust tax). Seek independent tax advice for your specific circumstances.

This article contains general information only and does not constitute financial advice. Your personal financial situation, objectives and needs have not been considered. Before acting on any information, you should consider its appropriateness to your circumstances. Speak to a qualified mortgage broker for advice tailored to your situation. Mortgage World Australia Pty Ltd is a credit representative (CR No. 396946) of Mortgage Specialists Pty Ltd (Australian Credit Licence No. 387025).

Patrick O’Brien, Director and Home Loan Specialist, Mortgage World Australia. In the industry since 2001.

Patrick is a Director and a Home Loan Specialist. He has been helping Australians with home loans since 2001. Prior to working as a mortgage broker Patrick was employed by Macquarie Bank for 3 years and also worked as an accountant for a publicly listed company. Patrick’s qualifications include:

Bachelor of Business, UTS Sydney. Majored in accounting and sub-majored in Finance and Marketing.

Diploma of Finance and Mortgage Broking Management FNS50310

Certificate IV in Financial Services (Finance/Mortgage Broking) FNS40804

Ready to Take the Next Step?

Whether you’re looking to buy your first home, refinance, or explore investment opportunities, Mortgage World Australia is here to help.

Fill out the contact form below, and one of our expert mortgage brokers will be in touch shortly to discuss your needs and guide you through your options.

Get Started Today!