Bridging Loan Guide 2026: How It Works & When to Use One

Bridging Loan Complete Guide: How They Work and When to Use Them

On this page ▾

You’ve found the property you want to buy. The timing is right, the price works, and you’re ready to move. The problem: your current house hasn’t sold yet. You need funds now, but they’re tied up in equity you can’t access until settlement.This is the exact situation a bridging loan is designed for. It’s a short-term financing solution that lets you purchase a new property before your existing one sells. But bridging loans carry genuine risk if the market moves against you, and the mechanics are worth understanding before you commit.This guide covers how bridging loans work, what they actually cost at current rates, and the scenarios where we’d recommend a different approach entirely.

What is a bridging loan?

A bridging loan is a short-term loan that “bridges” the funding gap between buying a new property and selling your existing one. Rather than waiting until your old home settles, the lender advances funds against both properties simultaneously. You carry two mortgages for a short period, until your existing property sells.Most major Australian lenders (ANZ, CommBank, NAB, and Westpac) offer bridging loans with a maximum term of 12 months. That 12-month window is the time you have to sell your existing property and repay the bridging component. We see clients underestimate how fast 12 months moves when a property isn’t selling.Closed vs open bridging loans

The bridging loan market uses two structures:Closed bridging loan: You already have an unconditional contract of sale on your existing property and know the settlement date. The exit is defined. This is lower risk for the lender and typically easier to approve.| Closed Bridging | Open Bridging |

|---|---|

| Unconditional sale contract in place | No sale contract yet |

| Settlement date known | Property listed or about to be listed |

| Lower risk | Higher risk |

| Faster approval, clearer terms | Lender may require evidence of active listing |

Who uses bridging finance?

The most common users of bridging finance in Australia:- Owner-occupiers upsizing and wanting to avoid the disruption of renting between properties

- Owner-occupiers downsizing who’ve found a new home before their existing one is sold

- Property investors who need to act quickly on an opportunity before a sale settles

- Borrowers in auction-heavy markets (Western Sydney included) where timing is tight

How a bridging loan works

The mechanics are straightforward, but the numbers can get large quickly. Here’s the step-by-step process:

The mechanics are straightforward, but the numbers can get large quickly. Here’s the step-by-step process:- You apply for a bridging loan before or at the same time as making an offer on the new property

- The lender assesses both properties: their values, your equity position, and your capacity to service the combined debt

- You settle on the new property using the bridging funds

- You now own both properties simultaneously and carry what’s called “peak debt”, the combined loan balance

- You sell the existing property. The sale proceeds repay the bridging loan component

- You’re left with the “end debt”, your ongoing home loan on the new property

The bridging loan timeline

The 12-month maximum is firm at all four major banks. ANZ is categorical: the term cannot be extended. Westpac says an extension may be considered subject to credit approval, but don’t rely on it. If you’re not confident you can sell within 12 months in your current market, that’s a serious reason to reconsider.Some lenders start charging a higher rate after the first three months. Westpac’s bridging rate rises by 1.00% p.a. after month three, which changes the cost equation sharply if the sale drags.Peak debt explained

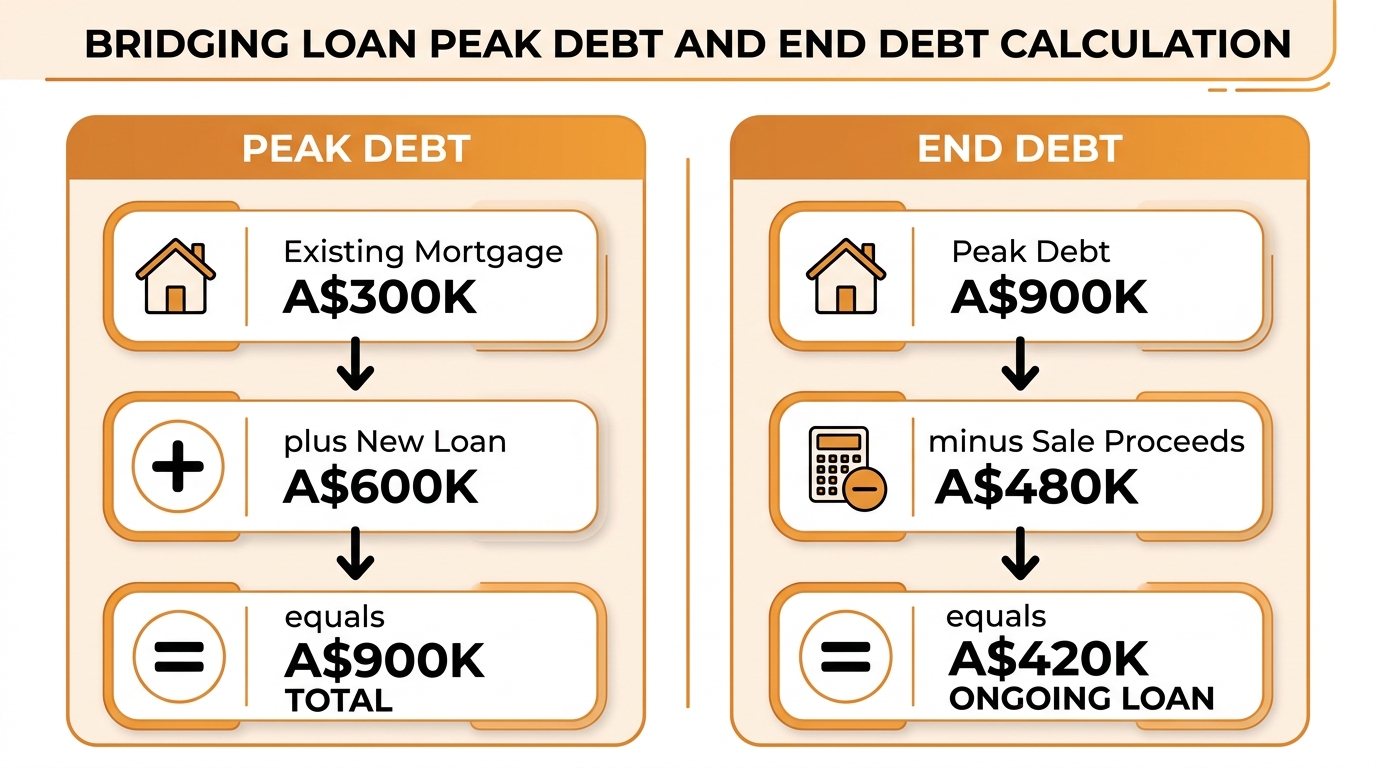

Peak debt is the total you owe across both loans at the same time. It’s calculated as:Peak Debt = Outstanding balance on existing mortgage + New loan amount requiredNote: peak debt is the new loan amount (what you’re borrowing), not the full purchase price. If you put $100,000 deposit toward a $700,000 property, the new loan is $600,000, not $700,000.A worked example:

Peak debt is the total you owe across both loans at the same time. It’s calculated as:Peak Debt = Outstanding balance on existing mortgage + New loan amount requiredNote: peak debt is the new loan amount (what you’re borrowing), not the full purchase price. If you put $100,000 deposit toward a $700,000 property, the new loan is $600,000, not $700,000.A worked example:- Existing property value: $750,000

- Remaining mortgage on existing property: $300,000

- New property purchase price: $900,000

- Deposit applied: $0 (full amount borrowed)

- New loan required: $900,000

- Peak debt: $1,200,000

Interest and capitalisation

During the bridging period, repayments are typically interest-only on the full peak debt. Interest is calculated on the combined loan balance, which can be substantial.How that interest is handled depends on the lender:Westpac and St. George capitalise interest to the loan balance throughout the bridging period. No monthly payments are required on the bridging loan — the interest accumulates and is cleared from sale proceeds when your existing property settles.CommBank and NAB require interest-only repayments at a minimum. Monthly payments are mandatory on both the home loan and the bridging loan; capitalisation is not an option.ANZ requires borrowers to demonstrate they can service interest payments on the full peak debt. If cash flow is a constraint, ANZ will accept savings held in an ANZ account as evidence of capacity to meet interest during the bridging period — but interest is still a cash obligation, not capitalised.This distinction matters for cash flow. Monthly interest payments on a $1.2M peak debt at 6.5% p.a. would be around $6,500 per month. If your income can’t cover that alongside other costs, a capitalisation structure may suit you better, but the total interest owed will be higher because you’re accruing interest on top of interest.The mechanics aren’t complicated. The cost is where people get surprised.Costs and rates

Bridging loans are more expensive than standard home loans. The margin above a regular variable rate depends on the lender, and the spread is wider than you might expect.Interest rates and fees

Current bridging loan rates from major lenders as at April 2026:| Lender | Rate | Notes |

|---|---|---|

| Westpac | 9.17% p.a. | Rises to 10.17% after month 3. Owner-occupier only. Comparison rate 8.99% p.a. Interest capitalises — no monthly payments. |

| St. George | Contact broker for rate | Owner-occupier only. Interest capitalises — no monthly payments during bridging period. |

| CommBank | ~6.58%–6.73% p.a. | Runs on standard variable rate (SVR); exact rate depends on LVR. Rates are based on IO repayments required monthly. Comparison rate up to 6.80% p.a. |

| ANZ | SVR rate applies | Same rate as standard home loan; contact for current figure |

| NAB | Higher than standard | Flexiplus Mortgage product; get a quote |

How much will it cost?

Using the worked example from above ($1,200,000 peak debt, 10-month bridging period):At 6.5% p.a. (CommBank-range rate): – Monthly interest: ~$6,500 – Total bridging interest over 10 months: ~$65,000At 9.17% p.a. (Westpac rate): – Monthly interest: ~$9,170 – Total bridging interest over 10 months: ~$91,700 (before the month-3 rate step-up)These aren’t hypotheticals. That’s what bridging finance costs right now, at current rates. A broker can help you identify which lender’s bridging product delivers the lowest total cost, given your specific timeline and loan size.Application and legal fees

Most lenders don’t publish a full bridging loan fee schedule publicly. Westpac is the exception. Their published fees:- Establishment fee: $600

- Document processing fee: $100

- Monthly account fee: $8

- Discharge fee: $350 per mortgage

When to use a bridging loan

Buying before selling

The primary use case. You’ve found your next home in a competitive market and can’t wait for your existing property to sell before making an offer. Auction markets (where you must be an unconditional buyer) make simultaneous settlement structurally difficult.A bridging loan lets you act decisively, then sell from a position of having already moved on.Investment property chains

If you’re building a property portfolio and need to acquire a new investment property before selling an existing one, a bridging loan can fund the gap. CommBank explicitly supports investment property bridging. Westpac and St. George do not — both restrict their bridging loans to owner-occupier purposes. Confirm with your broker which lenders are available for your specific investment scenario, as policies vary.For investors, the ability to service the peak debt is a primary lender concern. Rental income on the existing investment property is considered, but so is the combined LVR and debt load.Bridging for renovations

Some borrowers use bridging finance to fund renovations on an existing investment property before sale, borrowing against the post-renovation value. This is a more specialised use case and requires careful lender selection. Not all bridging products accommodate this scenario.The risks: what happens if the property doesn’t sell?

The risks here are real. Bridging loans are not forgiving if the market turns against you.Default and forced sale

If your existing property hasn’t sold when the 12-month term expires, you’re in default territory. Based on CommBank’s published guidance, what typically happens:- A default interest rate is applied (above the standard rate), making repayments even higher

- The lender may step in to arrange the sale of your property

- If the forced sale realises less than the outstanding bridging loan balance, the shortfall is added to your ongoing home loan

Interest accumulation risk

Even if your property sells within 12 months, a slow sale means more months of peak-debt interest. The difference between selling at month three versus month ten can be $40,000–$50,000 in additional interest at these rate levels.A realistic sales timeline assessment before applying matters. What’s the average days-on-market in your suburb? What comparable properties have sold recently, and for how close to the asking price?How brokers mitigate risk

An experienced broker doesn’t stop at finding the loan. They stress-test the scenario:- Is the sale price assumption realistic given current comparable sales?

- Can you service the peak debt interest payments if the sale takes 8 months instead of 4?

- Which lender’s rate structure minimises total cost across the most likely sale timeline?

- Is there an alternative structure (longer settlement, subject-to-sale clause) that avoids bridging altogether?

How to qualify and apply

Lender requirements

Lenders assess four things:- Equity. The new loan typically needs to be at or below 80% LVR of the new property’s value.

- Serviceability. Requirements vary by lender. CommBank, ANZ, and NAB assess serviceability on the full peak debt. Westpac and St. George assess serviceability on the end debt only — because their loans capitalise interest, there are no monthly payments to service during the bridging period. This means borrowers who cannot service the peak debt may still qualify with Westpac or St. George.

- Exit strategy. An unconditional contract of sale is the strongest evidence. Without one, the lender needs to be satisfied you can sell within the bridging term.

- Standard eligibility. Income, credit history, employment: the same checks as any home loan.

Choosing the right lender for your situation

The capitalisation vs repayment distinction matters more than the interest rate when you’re assessing whether you can qualify.Westpac or St. George suits borrowers who cannot comfortably service interest payments on the full peak debt each month. Because interest capitalises, there are no monthly repayments during the bridging period. Serviceability is assessed on the end debt, which is a significantly lower bar to clear. If your income is tight or you want to avoid the cash flow pressure of large monthly interest bills, these two lenders are worth prioritising.CommBank or ANZ suit borrowers with strong cash flow who can service the peak debt monthly. Paying interest as you go avoids compounding, which keeps total interest cost lower if the sale takes longer than expected. ANZ adds flexibility by accepting savings in an ANZ account as evidence of capacity to meet interest obligations.NAB also requires IO repayments and assesses peak debt serviceability. Similar positioning to CommBank — suitable for borrowers with the income to support monthly payments.One trade-off with capitalisation: the total interest cost is higher, because you’re accruing interest on a growing balance. The right lender depends on your cash flow position and how quickly you expect the sale to be completed.The application process

Getting a bridging loan approved typically involves:- Pre-approval: Confirm how much you can borrow and that you meet the lender’s bridging criteria before you make an offer

- Formal application: Valuation of both properties, full income and expense assessment, submission of supporting documents

- Approval and settlement: Once approved, you settle on the new property, and the bridging period begins

- Active sale of existing property: List, sell, and settle within the bridging term

- Repayment of bridging component: Sale proceeds are applied to the bridging loan, leaving your ongoing loan

- Refinancing (optional): Once the bridging period is complete and your ongoing loan is established, it’s worth reviewing whether your refinancing options could deliver a better rate or structure for the long term

Why a broker matters

Banks assess bridging loans against their own criteria. They can only offer their own products at their own rates. A broker working with 52+ lenders can:- Compare rate structures across lenders (a 3% rate difference on $1M peak debt is $30,000 per year)

- Identify which lenders support your specific scenario (investment property, trust structure, complex income)

- Negotiate on rate and fees

- Identify whether bridging is the right structure at all, or whether an alternative gives a better outcome

Bridging loan vs other options

Before committing to a bridging loan, consider whether a different approach achieves the same outcome with less risk.Bridging vs a personal loan

A personal loan is unsecured, typically capped at $50,000–$100,000, and priced at 8%–15% p.a. For a bridging shortfall of $200,000+, personal loans aren’t a realistic substitute. They’re also not considered by lenders as a valid bridge for property purchases.Bridging vs extending your mortgage

If you have sufficient equity in your existing home, a top-up or equity release on your existing mortgage can fund the deposit on the new property without a formal bridging structure. You carry a larger mortgage on the existing home until it sells, at which point you repay the additional borrowing.This is simpler than a bridging loan and avoids the “peak debt” mechanics, but it requires your existing lender to agree to the top-up, and your existing loan to be in a flexible enough structure to allow it.Bridging vs a “subject to sale” clause

Negotiating a “subject to sale” clause in your purchase contract means the purchase is conditional on your existing property selling. This is the safest option, but also the weakest for the vendor. In a competitive market, a “subject to sale” offer will often lose to an unconditional one. It works better in buyer’s markets or in direct negotiations with motivated sellers.Bridging loans for Western Sydney property buyers

Local market context

Property timing challenges are common in Western Sydney. Suburbs like Parramatta, Blacktown, and Greystanes have strong competition at the mid-market price points where most upgraders are active. Auction clearance rates vary, but the speed required to secure a quality property often outpaces a seller’s ability to settle on their existing home first.For buyers moving between the Hills District, Parramatta corridor, and the outer western suburbs, a 3–6 month settlement gap is common. Bridging finance is a legitimate tool in this market, provided the existing property is priced realistically and actively marketed from day one of the bridging period.Working with an independent broker

When a client comes to us with a bridging scenario, the first thing we look at isn’t which bank to use. It’s whether bridging is actually necessary, or whether a longer settlement or equity release gets the same result with less risk.MWA’s brokers have access to 52+ lenders. That means we’re not limited to a single bank’s bridging loan product. We can compare rates, structures, and eligibility rules across the market and match your scenario to the right lender.If you’re considering bridging finance for a property move in Western Sydney, we can assess your position, model the peak debt and interest costs, and help you decide whether bridging is the right call or whether another structure serves you better.Speak to our mortgage brokers about home loans in Western Sydney or contact a mortgage broker in Parramatta if you’d like to talk through your specific situation.Frequently asked questions

What’s the difference between a closed and an open bridging loan?A closed bridging loan is used when you already have an unconditional contract of sale on your existing property and know the exact settlement date. An open bridging loan has no set sale date. You typically have a maximum of 12 months to sell. Open bridging loans carry more risk because the exit date is uncertain.Can you lose your house with a bridging loan?Yes, in a worst-case scenario. If you cannot sell your existing property within the bridging period, the lender can step in to arrange the sale, and a default interest rate applies. If sale proceeds are less than the outstanding bridging balance, the shortfall is added to your ongoing loan. To reduce this risk, only use a bridging loan in a reasonable market with a realistic selling timeline.How long can you have a bridging loan?With Australia’s major banks (ANZ, CommBank, NAB, and Westpac), the maximum bridging loan term is 12 months. This is consistent across all four lenders. ANZ is categorical that the term cannot be extended. Some lenders may consider an extension subject to credit approval, but it’s not guaranteed.Do you pay interest on a bridging loan during the term?Yes. Repayments are typically interest-only on the full peak debt during the bridging period. Depending on the lender, interest is either charged monthly as a cash payment (ANZ) or capitalised to the loan balance until the property sells (Westpac). CommBank gives borrowers a choice between the two.Can you refinance a bridging loan?Bridging loans are short-term by design and aren’t typically refinanced. Once the existing property sells, the bridging component is repaid, and you’re left with an ongoing home loan (the end debt). If you need to change lenders, speak to a mortgage broker who can model the options.Is a bridging loan interest tax-deductible?It depends on the purpose. If you use a bridging loan to purchase an investment property that’s rented or available for rent, the interest relating to that investment component should be deductible under the ATO’s general interest expense rules (source: ato.gov.au, updated 23 June 2025). Interest on the owner-occupied portion is not deductible. Mixed-purpose loans require apportionment. Get tax advice specific to your circumstances.This article contains general information only and does not constitute financial advice. Your personal financial situation, objectives and needs have not been considered. Before acting on any information, you should consider its appropriateness to your circumstances. Speak to a qualified mortgage broker for advice tailored to your situation. Mortgage World Australia Pty Ltd is a credit representative (CR No. 396946) of Mortgage Specialists Pty Ltd (Australian Credit Licence No. 387025).Interest rate information is current as at April 2026 and subject to change. Always confirm current rates directly with your lender.

Patrick is a Director and a Home Loan Specialist. He has been helping Australians with home loans since 2001. Prior to working as a mortgage broker Patrick was employed by Macquarie Bank for 3 years and also worked as an accountant for a publicly listed company. Patrick’s qualifications include:

Bachelor of Business, UTS Sydney. Majored in accounting and sub-majored in Finance and Marketing.

Diploma of Finance and Mortgage Broking Management FNS50310

Certificate IV in Financial Services (Finance/Mortgage Broking) FNS40804

Ready to Take the Next Step?

Whether you’re looking to buy your first home, refinance, or explore investment opportunities, Mortgage World Australia is here to help.

Fill out the contact form below, and one of our expert mortgage brokers will be in touch shortly to discuss your needs and guide you through your options.

Get Started Today!