Help to Buy Scheme: How Australia’s Shared Equity Scheme Works

Help to Buy Scheme Australia: How the Government’s Shared Equity Scheme Works

On this page ▾

- What Is the Help to Buy Scheme?

- Help to Buy Eligibility: Who Qualifies?

- Property Price Caps by State

- What Homes Can You Buy Under Help to Buy?

- Which Lenders Offer the Help to Buy Scheme?

- How to Apply: Step-by-Step

- Help to Buy vs. the 5% Deposit Scheme: Which Is Right for You?

- Ongoing Obligations and How to Exit

- Worked Example: $850,000 Property in Western Sydney

- Frequently Asked Questions

The Help to Buy scheme launched in December 2025. It sounds simple: the government funds up to 40% of the purchase price, you put down 2%, and borrow the rest. But there’s a catch — you share the capital gains when you sell. If you’re comparing it to the Australian Government 5% Deposit Scheme (formerly the First Home Guarantee), that changes the calculation entirely.

This guide covers how the scheme works, who qualifies, the property price caps, and the trade-offs that no government brochure will spell out for you. After 25 years in home finance, we’ve seen how these policy decisions play out. Here’s what we’d recommend.

What Is the Help to Buy Scheme?

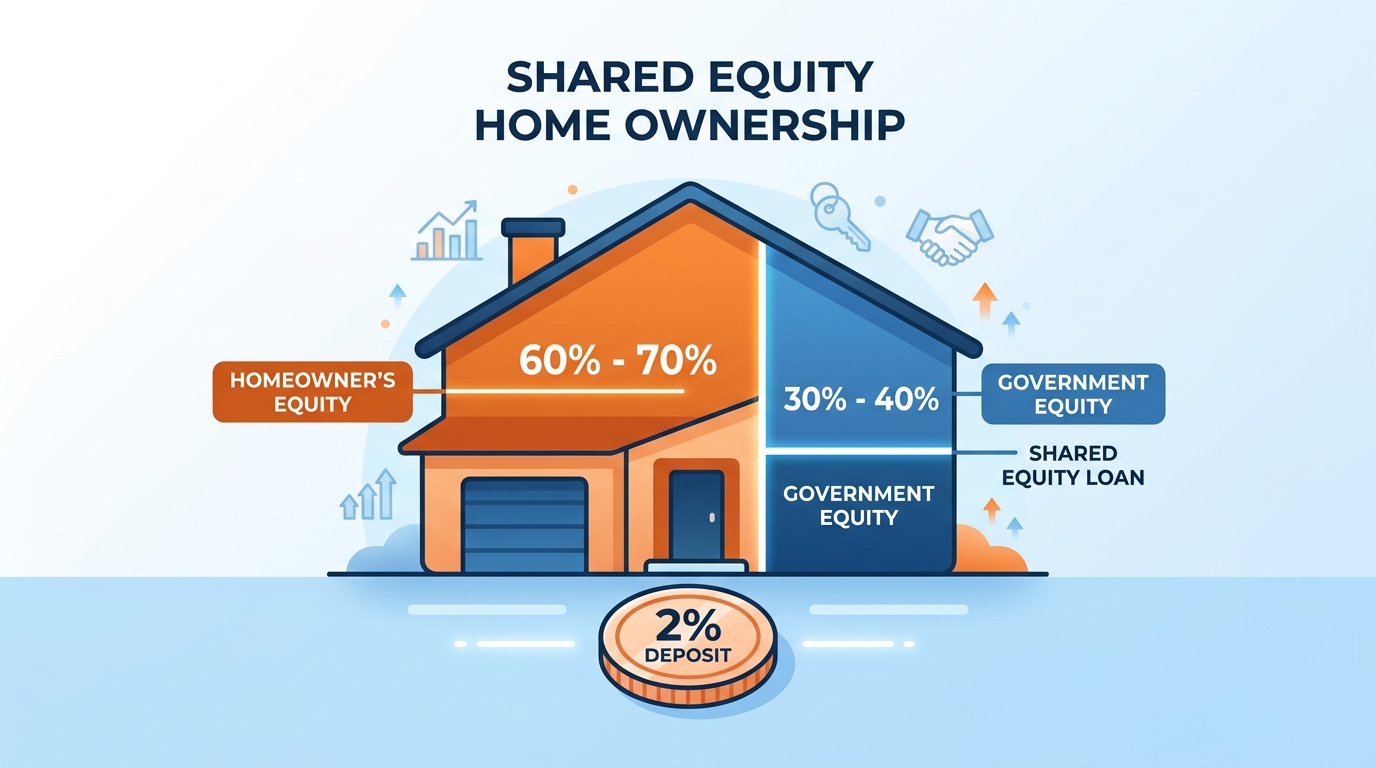

Help to Buy is a shared equity scheme administered by Housing Australia. The government co-owns part of your home — up to 40% for a new build, 30% for an existing property. You buy the rest. You’ll need a 2% deposit and a home loan. No Lenders Mortgage Insurance (LMI) is payable, even though you’re borrowing above 80% of the purchase price.

How shared equity works (and why it’s different from a loan)

The government’s contribution isn’t a loan. There’s no interest charged on it and no monthly repayments. Instead, the government holds a registered equity interest in your property — similar to a second mortgage on title. When you sell, or when you choose to buy out the government’s share, Housing Australia receives its proportionate percentage of the property’s value at that time.

If you buy with a 30% government contribution and your home grows in value, the government’s 30% grows too. Smaller upfront cost — but capital gains are shared in proportion.

Government contribution: 40% new homes, 30% existing homes

| Property type | Government equity contribution | Your minimum deposit |

|---|---|---|

| New home | Up to 40% | 2% |

| Existing home | Up to 30% | 2% |

You don’t have to take the maximum contribution. If you can manage a larger deposit, you can take a smaller government share — which means keeping more of the capital gain when you sell.

Help to Buy Eligibility: Who Qualifies?

Income caps: $100,000 individual, $160,000 couples and single parents

Eligibility is based on your taxable income from the previous financial year, as shown on your ATO Notice of Assessment. The income thresholds are:

- Individual applicants: $100,000 per year or less

- Joint applicants or single parents: $160,000 combined per year or less

These thresholds apply at the time of application. Housing Australia conducts ongoing reviews — at least every five years — to assess your income. If your income exceeds the cap for two consecutive financial years, you may be required to repay part or all of the government’s equity contribution, though Housing Australia states you won’t be required to repay until you can afford to do so.

Citizenship, age, and property ownership requirements

To be eligible, you must:

- Be an Australian citizen (permanent residents do not qualify)

- Be 18 years of age or older

- Not currently own, or have previously owned, residential property in Australia (this applies to all applicants on the loan)

- Intend to use the property as your principal place of residence — the scheme is not available for investment properties

Owner-occupier only — why investment properties are excluded

The scheme is designed to build owner-occupier housing, not investment portfolios. If you move out of the property and rent it, you will trigger the exit provisions of the scheme. That means you’ll need to buy back the government’s equity share or sell the property and settle with Housing Australia.

Property Price Caps by State

The scheme applies nationally, with property price caps set by state and territory. For NSW-based buyers — particularly in Western Sydney — the capital city cap of $1,300,000 is relevant:

| State/Territory | Capital cities & major regional centres | Other areas |

|---|---|---|

| NSW | $1,300,000 | $800,000 |

| VIC | $950,000 | $650,000 |

| QLD | $1,000,000 | $700,000 |

| SA | $900,000 | $500,000 |

| WA | $850,000 | $600,000 |

| ACT | $1,000,000 | — |

| NT | $600,000 | $600,000 |

| TAS | $700,000* | $550,000* |

Property price cap figures sourced from Housing Australia, current as at scheme launch (December 2025). Use the postcode tool on the Housing Australia website to check your specific area.

*Tasmania has not yet passed enabling legislation to participate in Help to Buy. Price caps are published but the scheme is not available in Tasmania at the time of writing (April 2026).

What Homes Can You Buy Under Help to Buy?

The scheme covers most residential property types: houses, townhouses, units, and apartments. Both new and existing dwellings are eligible, though the government’s equity contribution differs (40% vs 30%).

The property must become your principal place of residence — you must move in within a reasonable timeframe after settlement. Off-the-plan purchases are eligible, provided settlement occurs and the property meets the price cap at the time.

Which Lenders Offer the Help to Buy Scheme?

At the time of writing (April 2026), two lenders are participating:

- Commonwealth Bank of Australia (CommBank)

- Bank Australia

Why only two lenders — and what that means for your options

This is the most significant practical constraint of the scheme. If neither CommBank nor Bank Australia can offer you a competitive rate, or if your financial situation requires a specialist lender — for example, you’re self-employed, have variable income, or need a non-standard loan structure — you’re limited.

A mortgage broker with access to 52+ lenders can structure your loan outside the scheme if that produces a better outcome. For most borrowers with straightforward income and clean credit, CommBank or Bank Australia may be perfectly adequate. But it’s worth modelling both scenarios before committing.

Government schemes tend to expand participating lender panels over time. If more lenders join, that constraint eases.

How to Apply: Step-by-Step

Step 1: Check your eligibility Confirm your income against the prior year’s ATO Notice of Assessment, verify you meet the citizenship and property ownership conditions, and check the price cap for your target area.

Step 2: Speak to a mortgage broker This is the step the government’s own page recommends, and for good reason. A broker who understands Help to Buy can compare it against the Australian Government 5% Deposit Scheme, calculate your borrowing capacity under both lenders, and flag any issues with your application before you apply. Home loan pre-approval through the right lender matters here.

Step 3: Get conditional approval (90-day window) Apply directly through CommBank or Bank Australia for a Help to Buy loan. Conditional approval gives you a 90-day search window.

Step 4: Find a home within the price caps In NSW, you have up to $1,300,000 in the capital city region. Properties must be on the eligible dwelling list — standard residential, not commercial.

Step 5: Settlement and joining the scheme At settlement, Housing Australia’s equity contribution is drawn down and applied to the purchase. The government registers its equity interest on the property title. You receive the keys and move in as owner-occupier.

Available places are capped at 10,000 per year nationally, allocated on a first-come basis. Apply early in the financial year.

Help to Buy vs. the 5% Deposit Scheme: Which Is Right for You?

No lender or government website will give you this comparison directly — both sides have a stake in promoting their own scheme. Here’s how the two actually stack up:

| Feature | Help to Buy | Australian Government 5% Deposit Scheme |

|---|---|---|

| Deposit required | 2% minimum | 5% minimum |

| Government contribution | Up to 40% equity stake | Guarantees the 20% gap (no deposit of that portion required) |

| Do you own 100% from day one? | No — shared equity | Yes |

| LMI payable? | No | No |

| Income cap | $100k individual / $160k joint | No income cap (removed 1 Oct 2025) |

| Lender choice | 2 lenders | 33+ lenders |

| Share capital gains with government? | Yes | No |

| Annual place limit | 10,000 | Unlimited (as of 1 Oct 2025) |

| Income cap (ongoing) | Reviewed at least every 5 years | No income cap |

| Property type restrictions | Owner-occupier only | Owner-occupier only |

When Help to Buy makes sense: You can only save a 2% deposit, you meet the income cap, and you’re willing to give up a portion of future capital appreciation to get into the market sooner. The NSW cap of $1.3M gives reasonable access to Sydney property.

When the 5% Deposit Scheme may be better: You can save 5% and prefer to own 100% of your home from settlement. You want access to a wider lender panel (33+ participating lenders vs. two). Your income exceeds the Help to Buy cap — the 5% Deposit Scheme removed its income cap on 1 October 2025, so there’s no upper income limit. You’re buying in a market where capital growth is expected to be strong and you want to keep the full upside.

When neither scheme is optimal: You’re self-employed with variable income, or you need a lender who specialises in complex applications. In that case, saving a full deposit or using a guarantor loan may give you more flexibility.

We can also help you understand stamp duty exemptions in NSW — because stamp duty applies even with Help to Buy, and NSW first home buyers may be eligible for concessions separately.

Ongoing Obligations and How to Exit

Buying back the government’s share

You can make voluntary equity payments to Housing Australia at any time to reduce the government’s stake. These can be done in increments — you don’t need to buy out the full share at once. Each payment reduces the registered equity interest proportionally.

If your income exceeds the threshold for two consecutive financial years, you may be required to buy back the government’s share. Housing Australia states you won’t be required to repay until you can afford to do so.

What happens if you sell or exceed the income limit

When you sell, the government receives its percentage of the gross sale price. If you bought at $850,000 with a 30% government contribution and sell for $1,100,000, the government receives $330,000 — not the original $255,000 it contributed. Capital appreciation is shared in proportion to the equity split.

This is a real cost to factor in. In a rising Sydney market over 5–10 years, the government’s share of your gain could easily exceed the upfront deposit savings. If you’re buying somewhere with strong capital growth expectations, model both scenarios with a broker before you commit.

Worked Example: $850,000 Property in Western Sydney

| Scenario | Without Help to Buy (20% deposit) | With Help to Buy (2% deposit, 30% govt) |

|---|---|---|

| Property price | $850,000 | $850,000 |

| Your deposit | $170,000 | $17,000 |

| Government contribution | — | $255,000 (30%) |

| Your loan | $680,000 | $578,000 |

| Approx. monthly repayment (6.5% p.a., 30yr) | ~$4,300 | ~$3,650 |

| LMI payable | No (80% LVR) | No |

| Your ownership % | 100% | 70% |

The scheme saves $153,000 in upfront deposit requirements and reduces your monthly repayments by around $650. The cost: 30% of any future capital gain goes to Housing Australia when you sell.

Frequently Asked Questions

How much does the government contribute?

The government contributes up to 40% of the purchase price for a new home and up to 30% for an existing home. You contribute a minimum 2% deposit and borrow the remainder. No LMI is payable.

Can I use Help to Buy with other government grants?

Help to Buy cannot be combined with the Australian Government 5% Deposit Scheme (formerly the First Home Guarantee) — both are applied at purchase and target the same deposit gap. It may be used alongside the First Home Owner Grant (FHOG) and stamp duty concessions for first home buyers, which are administered separately by state governments. Speak to a mortgage broker to confirm which combination applies to your situation.

What does it mean if the government owns 30% of my home?

The government holds a registered equity interest — similar in structure to a second mortgage on title. You own the property, live in it as normal, and don’t pay rent on the government’s share. When you sell, or when you buy back the equity, Housing Australia receives its percentage of the property’s value at that time. Capital gains are shared in proportion.

Can I buy out the government’s share over time?

Yes. You can make voluntary equity payments to Housing Australia to progressively increase your ownership stake. There’s no requirement to buy out the full share at once. As you pay down the equity, the government’s registered interest reduces accordingly.

What happens when I sell a Help to Buy property?

The government receives its proportionate share of the sale proceeds. If you entered with a 30% government contribution and the property has grown in value, Housing Australia receives 30% of the sale price — not just the original dollar amount contributed. Factor this into your long-term financial plan before entering the scheme.

This article is general information only and does not constitute financial advice. The Help to Buy scheme eligibility rules, price caps, and participating lenders are subject to change. Speak to a qualified mortgage broker about your individual circumstances before making any financial decision.

Patrick O’Brien | Director and Home Loan Specialist since 2001, Mortgage World Australia. Access to 52+ lenders. Speak to us about first home buyer loans.

Patrick is a Director and a Home Loan Specialist. He has been helping Australians with home loans since 2001. Prior to working as a mortgage broker Patrick was employed by Macquarie Bank for 3 years and also worked as an accountant for a publicly listed company. Patrick’s qualifications include:

Bachelor of Business, UTS Sydney. Majored in accounting and sub-majored in Finance and Marketing.

Diploma of Finance and Mortgage Broking Management FNS50310

Certificate IV in Financial Services (Finance/Mortgage Broking) FNS40804

Ready to Take the Next Step?

Whether you’re looking to buy your first home, refinance, or explore investment opportunities, Mortgage World Australia is here to help.

Fill out the contact form below, and one of our expert mortgage brokers will be in touch shortly to discuss your needs and guide you through your options.

Get Started Today!