First Home Super Saver Scheme: Complete 2026 Guide

First Home Super Saver Scheme: your complete 2026 guide

On this page ▾

The first home super saver scheme (FHSSS) lets you save for a home deposit inside super, where your contributions are taxed at 15% instead of your marginal rate. For most buyers on middle incomes, that difference adds up to thousands of dollars. But despite being around since 2017, it’s still one of the most underused tools available to first home buyers in Australia.

We work with first home buyers across Western Sydney every week. The FHSSS comes up regularly, and so does the confusion around it. The mechanics trip people up, the rules have changed over the years, and most of what’s written about it gets at least one detail wrong.

This guide covers how the scheme works, who qualifies, what you can contribute, how the tax treatment actually works, and how the FHSSS compares to the other main first home buyer schemes available in 2026.

What is the first home super saver scheme?

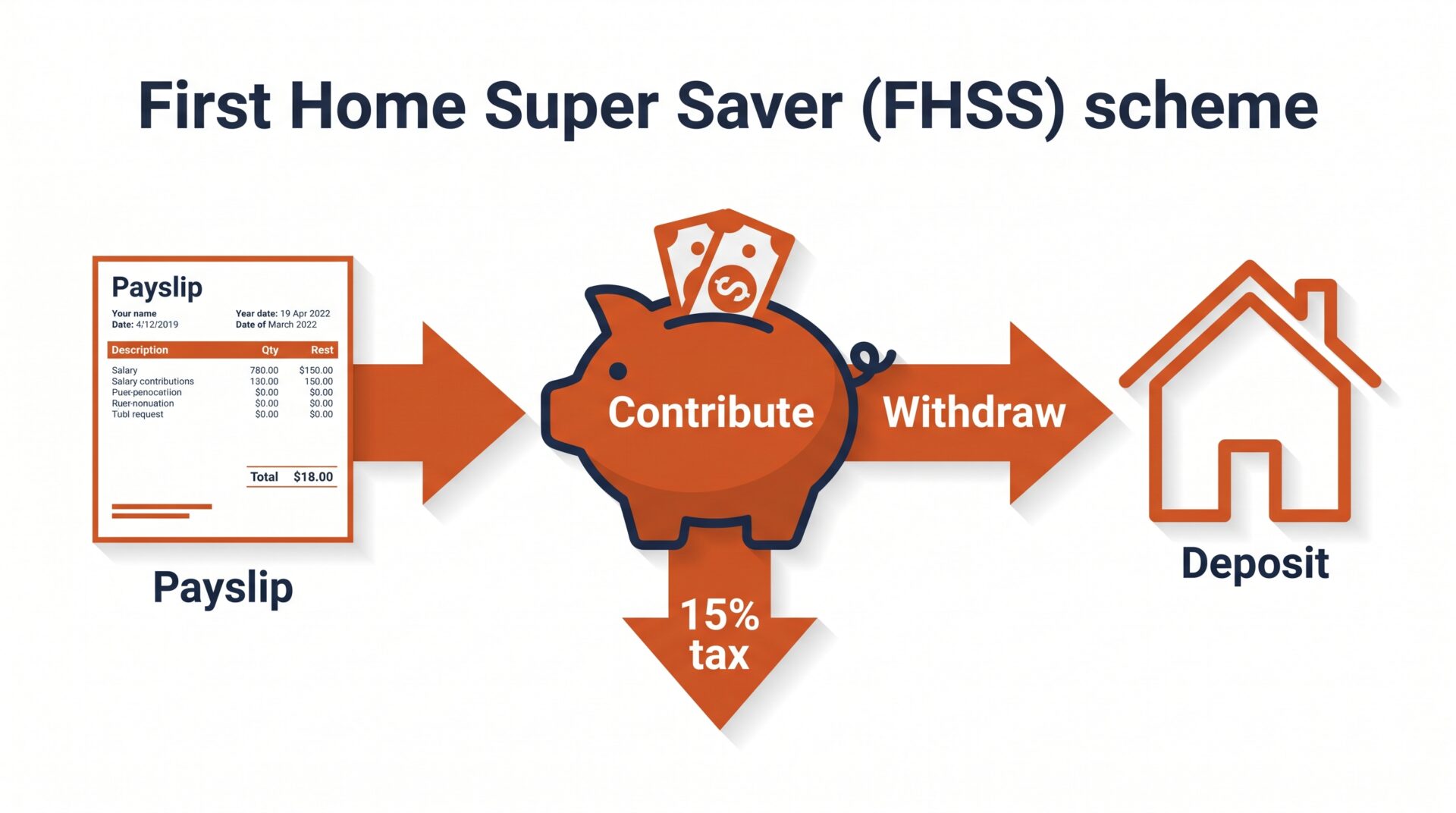

The first home super saver scheme is a federal government program that lets first home buyers make voluntary super contributions and later withdraw those contributions, plus a deemed earnings amount, to use as a home deposit. It launched on 1 July 2017 and is administered by the ATO.

The core mechanism is a tax arbitrage. Voluntary concessional contributions, including salary sacrifice and personal deductible contributions, are taxed at 15% inside super. If your marginal income tax rate is 32% or higher, which covers most workers above $45,000, you save the difference on every dollar contributed. That gap is the advantage.

How it works step-by-step

The FHSSS has two stages: a saving phase and a withdrawal phase.

During the saving phase, you make voluntary contributions to your existing super fund. You can do this through salary sacrifice arranged with your employer, personal contributions you later claim as a tax deduction, or after-tax personal contributions where no deduction is claimed. All three types count toward your FHSSS balance, with slight differences in tax treatment (covered below).

When you’re ready to buy, you apply to the ATO through myGov for an FHSS determination, then submit a release request. The ATO issues a release authority to your super fund, which transfers the eligible amount to the ATO. The ATO withholds tax and sends you the net amount. You then have up to 12 months to sign a contract to purchase or build your first home.

Key differences from standard superannuation

Your ordinary super balance is locked until retirement. The FHSSS creates a pathway to access voluntary contributions early, specifically for a first home deposit.

One thing to understand clearly: when you withdraw under the FHSSS, you don’t receive your actual fund earnings. You receive your eligible contributions plus “associated earnings,” a notional amount the ATO calculates using the Shortfall Interest Charge (SIC) rate. The SIC rate is roughly the 90-day bank bill rate plus 3 percentage points, sitting at approximately 6.65-6.96% per year in early 2026. Your actual investment returns stay in your fund. You might earn more or less than the deemed rate in your fund, but the ATO release is calculated on the SIC rate regardless.

This is a detail that many articles on the FHSSS get wrong. Knowing it helps you plan accurately.

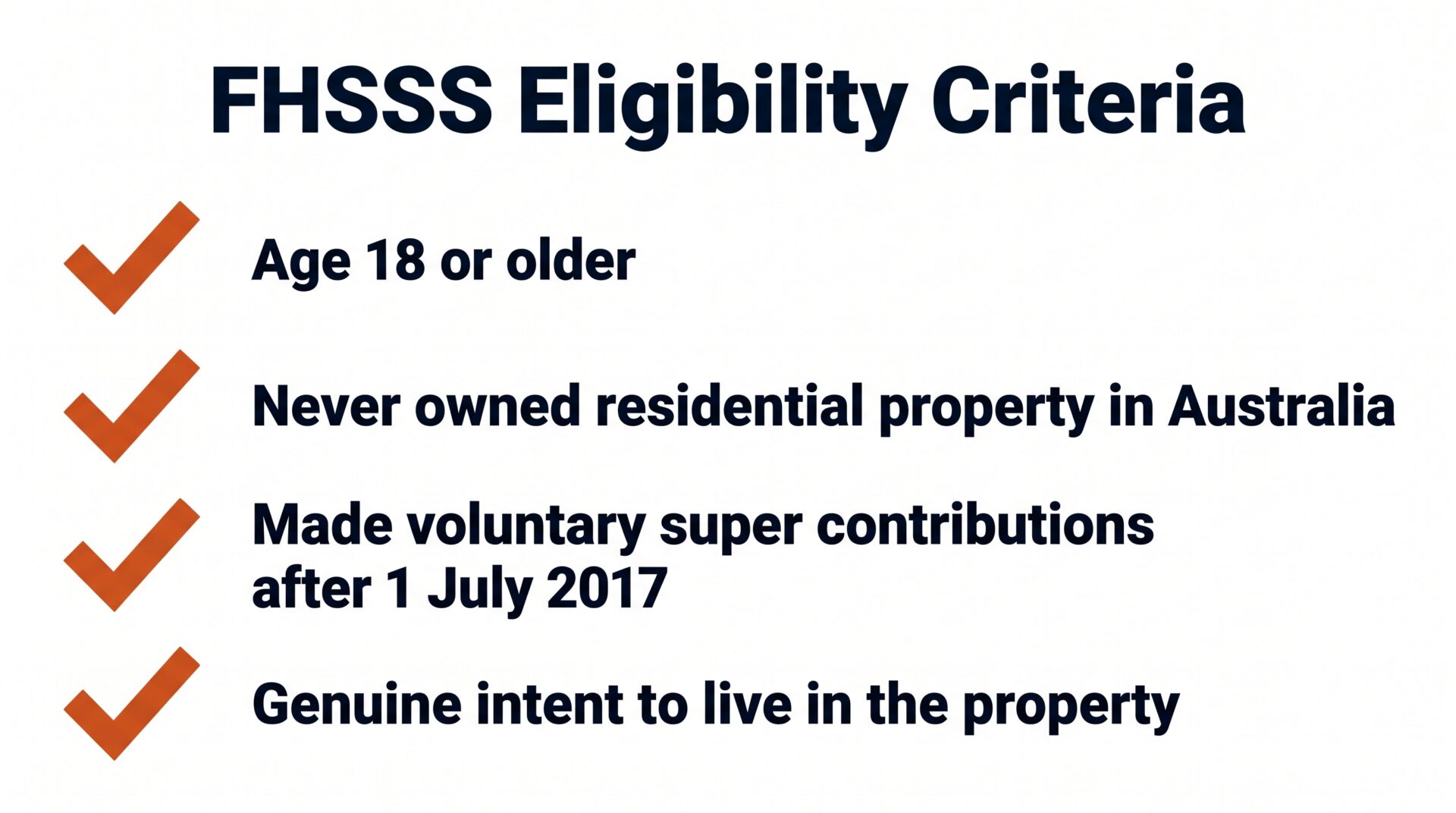

Eligibility requirements

The FHSSS eligibility rules are simpler than most people expect. The one that catches people out most often is the property ownership requirement: if you’ve owned residential property in Australia before, even an investment property, you’re disqualified under the standard pathway.

Age requirement

You must be 18 or older when you submit your FHSS determination request to the ATO. Contributions made before turning 18 still count toward your eligible balance, you just can’t access them until you’re 18.

First home owner status

You must never have owned residential property in Australia. That covers homes, investment properties, and any other residential real estate. There’s a hardship exception (covered later in this article), but for the standard pathway, any prior residential property ownership in Australia disqualifies you.

Eligibility is assessed individually. If you’re buying with a partner and one of you has previously owned property, the other person can still use their own FHSSS contributions toward the deposit. The purchase can be joint, but only the eligible person’s FHSSS funds contribute.

No citizenship or residency requirement

The FHSSS does not require Australian citizenship or permanent residency. Non-residents for tax purposes may face different withholding rates on withdrawal, but there’s no blanket exclusion based on citizenship or visa status.

No income cap

There’s no income limit for the FHSSS. Any income level can participate, provided the first home owner and contribution requirements are met. This makes it different from the Help to Buy scheme, which has income caps.

Intent to occupy

You must genuinely intend to live in the property as soon as practicable after purchase, for at least 6 of the first 12 months it’s practicable to occupy. This isn’t a technicality. The ATO treats it as a substantive requirement.

Property type

The property must be residential and located in Australia. Houseboats and mobile homes are excluded. Vacant land qualifies if you intend to build and live in the property for at least 6 of the first 12 months of ownership.

Contribution limits and caps

The FHSSS has two limits: an annual cap and a lifetime cap.

Annual and cumulative limits

You can count up to $15,000 in eligible voluntary contributions per financial year toward the FHSSS. The cumulative cap across all years is $50,000 in total contributions.

Both limits apply to contributions made from 1 July 2017 onwards.

| Limit type | Amount |

|---|---|

| Annual eligible contributions | $15,000 per financial year |

| Lifetime cumulative cap | $50,000 total |

A couple buying together can each access up to $50,000, giving a combined maximum of $100,000 in contributions, plus associated deemed earnings on top of that.

What contributions qualify

Two types of voluntary contributions count toward the FHSSS.

Concessional contributions cover salary sacrifice and personal contributions you’ve claimed as a tax deduction. On withdrawal, 85% of these are releasable, the remaining 15% accounts for the contributions tax your fund already paid on the way in.

Non-concessional contributions are personal contributions from after-tax income with no deduction claimed. These are 100% releasable, since tax was already paid before the money went into super.

Employer mandatory contributions, the Superannuation Guarantee, do not count toward the FHSSS. Only what you contribute voluntarily above the SG rate qualifies.

The $15,000 annual cap applies to your combined concessional and non-concessional contributions.

How the associated earnings calculation works

When you withdraw, the ATO adds “associated earnings” to your contributions. This is not your actual fund performance, it’s a deemed amount based on the Shortfall Interest Charge (SIC) rate. For early 2026, that’s approximately 6.65-6.96% per year, reviewed quarterly.

If your fund returned more than the SIC rate, those extra earnings stay in super. If it returned less, you still receive the SIC rate on your FHSSS balance. The deemed rate creates predictability: you can estimate your release amount without guessing at market returns.

How to contribute to your FHSSS

Salary sacrifice contributions

Salary sacrifice is the most common contribution method. You arrange with your employer to direct part of your pre-tax salary into your super fund, bypassing income tax. The fund pays 15% contributions tax instead. The gap between your marginal rate and 15% is your tax saving on contributions.

For someone earning $80,000/year with a marginal rate of 30% plus 2% Medicare levy (32% total), salary sacrificing $15,000 saves roughly $2,550 in income tax compared to receiving that $15,000 as ordinary income.

Watch the concessional contributions cap: salary sacrifice counts toward your $30,000/year concessional cap (2025-26). Exceeding that cap means excess contributions are taxed at your marginal rate, which defeats the purpose.

Personal contributions with a tax deduction

If your employer doesn’t offer salary sacrifice, or you’re self-employed, you can make personal contributions from your take-home pay and claim a tax deduction at tax time. The ATO treats these the same way as salary sacrifice for FHSSS purposes.

To use this method, you need to lodge a “Notice of intent to claim a deduction” with your super fund before you lodge your tax return for that year.

Personal after-tax contributions (non-concessional)

You can also contribute after-tax income without claiming a deduction. These non-concessional contributions are 100% releasable under FHSSS and count toward your $15,000 annual cap. The tax benefit is smaller than concessional contributions, but it gives you flexibility if your concessional cap is already used up through employer contributions or other salary sacrifice.

Employer SG contributions

Your employer’s mandatory super contributions don’t count toward the FHSSS. Full stop.

Tax treatment and benefits

The FHSSS delivers tax savings at two points: when money goes in, and when it comes out.

Tax on concessional contributions going in

Concessional contributions are taxed at 15% in the fund. If your marginal rate is above 19%, which applies at incomes above $18,200, you’re ahead on every dollar compared to receiving it as salary.

The higher your income, the larger the saving:

| Annual income | Marginal rate (incl. Medicare) | Contributions tax | Tax saving per $15,000 contributed |

|---|---|---|---|

| $45,001-$135,000 | 32% | 15% | $2,550 |

| $135,001-$190,000 | 39% | 15% | $3,600 |

| $190,001+ | 47% | 15% | $4,800 |

Tax rates as of the 2025-26 financial year

That number surprised us when we first ran it for a client. On $15,000 contributed annually at the 39% marginal rate, you’re saving $3,600 in tax compared to saving the same amount from your after-tax income. Over three or four years, that’s a material difference in your deposit size.

Low-income earners also benefit. If your income is below $37,000, the Low Income Super Tax Offset (LISTO) may refund your contributions tax up to $500, effectively making concessional contributions tax-free on the way in.

Tax on withdrawal

When you withdraw, the released amount (concessional contributions and associated deemed earnings) is included in your assessable income for that year and taxed at your marginal rate. The ATO then applies a 30% FHSS tax offset, which cuts the effective tax rate down.

The ATO withholds tax at the time of release based on your estimated marginal rate less the 30% offset, or at 17% if your rate can’t be determined. You reconcile this at tax time.

Non-concessional contributions released under FHSSS are not assessable income. You already paid tax on them before they went in. Only concessional contributions and associated deemed earnings are taxable on the way out.

How the tax benefit adds up against saving outside super

A buyer on a $90,000 salary who salary-sacrifices $15,000 per year:

Inside FHSSS: $15,000 goes into super, taxed at 15%, so $12,750 effectively goes toward the deposit (with the fund absorbing $2,250 in tax). Plus deemed earnings accumulate over the saving period.

Outside super: that same $15,000 of gross salary would be taxed at 32% before it becomes savings, leaving roughly $10,200 after income tax.

That’s approximately $2,550 more entering the deposit pool per year, before any return. Over three years ($45,000 contributed), the contribution advantage alone is around $7,650, plus the deemed earnings differential during the saving period.

Withdrawal tax partially reduces this gain, but for most first home buyers, the net benefit of saving through the FHSSS versus a standard savings account is several thousand dollars. Run the ATO’s FHSS calculator at ato.gov.au for a figure specific to your income and timeline.

The withdrawal process

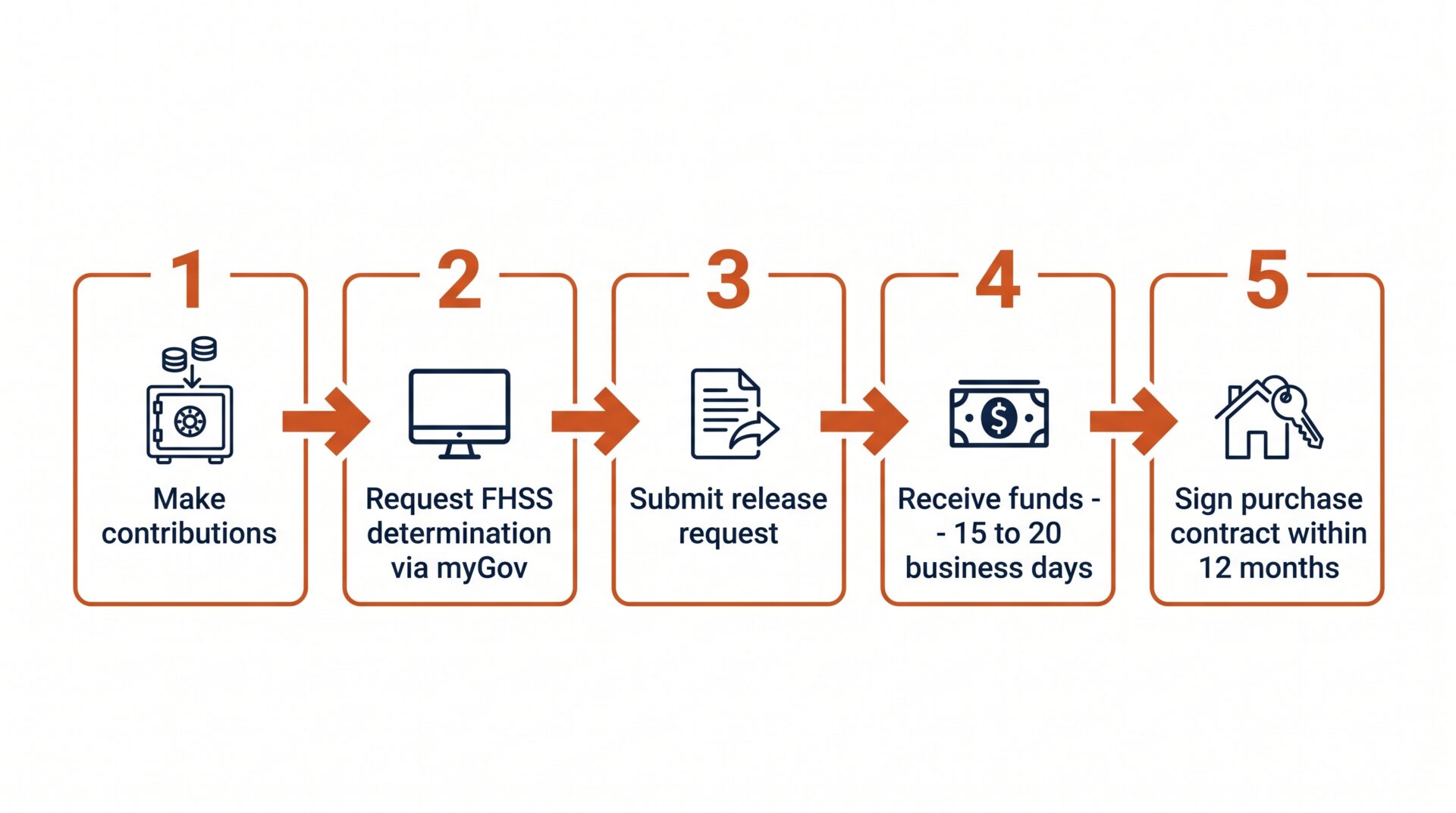

The withdrawal process has more steps than people expect. Here is how it works in practice.

Withdrawal eligibility checklist

Before requesting a withdrawal, confirm:

- You’re 18 or older

- You’ve never owned residential property in Australia (or hold a hardship exception)

- You’ve made eligible voluntary contributions after 1 July 2017

- You haven’t previously requested an FHSS release (one per person, lifetime)

- You genuinely intend to live in the property you’re buying

Step-by-step application process

- Log in to myGov and access ATO Online Services.

- Request an FHSS determination. The ATO pre-fills most data from your super fund records. Review it carefully and make sure all eligible contributions are captured.

- The ATO issues your determination, showing the maximum releasable amount.

- When you’re ready to buy, submit a release request via ATO Online Services.

- The ATO issues a release authority to your super fund.

- Your fund releases the funds to the ATO.

- The ATO withholds tax and sends the net amount to your nominated bank account.

Timeline to purchase

For FHSS determinations made on or after 15 September 2024 (the current rule), you can sign a purchase or construction contract as early as 90 days before your release request date, and up to 12 months after it.

In practice: don’t request your release until you’re actively searching. You have a 12-month window after receiving the funds to sign a contract. If you need more time, you can apply to the ATO for a 12-month extension.

From submitting a release request to receiving funds typically takes 15 to 20 business days. Don’t plan around receiving funds the week you want to make an offer.

What happens to unused funds

If you never request a release, your FHSSS contributions stay in your super fund as ordinary super. No penalty, no action required. The money works toward your retirement instead.

If you request a release but don’t end up buying, you can recontribute the released amount (less any tax withheld) to super within 12 months of your release request date and notify the ATO. This avoids additional FHSS tax. If you keep the funds without buying and without recontributing, an additional FHSS tax applies to the retained amount.

Comparing FHSSS with other schemes

The FHSSS is a savings tool. The other two main schemes in 2026 work differently. The Australian Government 5% Deposit Scheme is a lender guarantee: it lets you buy with a 5% deposit without paying LMI. The Help to Buy scheme is a shared equity scheme, where the government buys a stake in your property alongside you.

These can be used in combination. Knowing what each one actually does is the starting point.

FHSSS vs the Australian Government 5% Deposit Scheme

The 5% Deposit Scheme went through a major change on 1 October 2025. Income caps were removed. Waitlists were removed. The scheme is now effectively open to any first home buyer who meets the property price cap requirements. (The scheme was previously called the First Home Guarantee and, before that, the First Home Loan Deposit Scheme. The current name is the Australian Government 5% Deposit Scheme.)

Under the scheme, the government guarantees up to 15% of your purchase price, so you only need a 5% deposit to buy without Lenders Mortgage Insurance. You still borrow the full loan amount. The government doesn’t contribute cash; it provides a guarantee to the lender.

| Feature | FHSSS | 5% Deposit Scheme |

|---|---|---|

| Government role | Tax benefit on savings | Lender guarantee (no LMI) |

| Minimum deposit | Helps you build one | 5% (2% for single parents) |

| Income cap | None | None (removed October 2025) |

| Property price cap | None | Yes, location-specific |

| Australian citizenship or PR required | No | Yes |

| One-off or ongoing obligation | One-off withdrawal | Ongoing owner-occupier condition |

| Places available | Unlimited | Unlimited (from October 2025) |

The 5% Deposit Scheme has property price caps that vary by location. In NSW capital city and major regional areas, the cap is $1,500,000. In the rest of NSW, it’s $800,000. Check the official postcode search tool at firsthomebuyers.gov.au for exact caps in your target area.

The two schemes work well together. You build your deposit through FHSSS, paying less tax on the way in, then use those funds as your 5% deposit when applying for the scheme guarantee. For buyers with two or three years before they want to buy, this is the combination worth planning around.

FHSSS vs Help to Buy

The Australian Government Help to Buy scheme opened for applications in December 2025. It works differently from both the FHSSS and the 5% Deposit Scheme: the government becomes a co-owner of your property, contributing up to 40% of the purchase price for new homes or up to 30% for existing homes.

You need a 2% minimum deposit. The government holds equity in your property until you buy out their share, sell the property, or stop meeting eligibility conditions.

| Feature | FHSSS | Help to Buy |

|---|---|---|

| Government role | Tax benefit on savings | Co-purchaser (equity stake) |

| Minimum deposit | Helps you build one | 2% |

| Income cap | None | $100,000 individual / $160,000 couple |

| Property price cap | None | Yes, location-specific |

| Australian citizenship required | No | Yes |

| Government becomes co-owner | No | Yes, up to 40% |

| Total places available | Unlimited | 10,000 places per year |

Help to Buy has 10,000 places per year and income caps the 5% Deposit Scheme no longer has. One thing to factor in: the government holds equity in your property until you buy them out. If you buy in an area with strong capital growth, you’re sharing that upside.

If you’re above the thresholds ($100,000 individual, $160,000 for couples and single parents), Help to Buy is not available to you. If you’re under them and want the maximum buying power with the smallest deposit, it’s a scheme worth looking at alongside FHSSS.

Tasmania has not yet passed enabling legislation for Help to Buy. The scheme is not available there as of April 2026.

Can you combine schemes?

FHSSS with the 5% Deposit Scheme: yes. Save through FHSSS, withdraw your tax-advantaged deposit, apply for the scheme guarantee. Many of the first home buyers we work with take this route. It’s a well-tested approach that works.

FHSSS with Help to Buy: the interaction between the two schemes hasn’t been clearly defined, and Help to Buy carries ongoing obligations (the government remains a co-owner until you buy them out). Before assuming you can use both, speak to a mortgage broker and get confirmation from the scheme administrator. This is not a decision to base on a blog article.

Early access and financial hardship

The FHSSS normally requires you to have never owned property. There is one exception.

Hardship criteria

The ATO can grant FHSSS eligibility to someone who has previously owned property if:

- A financial hardship event caused them to lose all their property interests in Australia, AND

- They have not acquired any subsequent property interest in Australia since that loss.

Financial hardship isn’t self-defined. The ATO assesses each case individually. Events like foreclosure, mortgagee-in-possession sale, or a forced sale due to serious financial distress may qualify. Voluntarily selling a property to upgrade, downsize, or move doesn’t qualify.

How to apply for hardship access

Submit the ATO’s “First Home Super Saver Scheme – hardship application form” directly to the ATO. If approved, you proceed through the standard FHSSS contribution and withdrawal process. Check the ATO website for current processing timeframes when you apply.

Common questions

Can I use the FHSSS if I’ve owned property before?

In most cases, no. The FHSSS requires you to have never owned residential property in Australia. The hardship exception applies to people who lost all property ownership through a genuine financial hardship event and haven’t owned anything since. If you previously sold an investment property, sold a home to rent, or disposed of property voluntarily, you don’t qualify.

What if I don’t use my FHSSS funds to buy a home?

If you never request a release, your contributions stay in your super fund. No penalty. If you request a release but don’t buy, you have 12 months to recontribute the net funds to super and notify the ATO, which avoids additional FHSS tax. Keep the funds without buying and without recontributing, and additional FHSS tax applies to the retained amount.

Can I combine the FHSSS with the Australian Government 5% Deposit Scheme?

Yes. You save through FHSSS to build a tax-advantaged deposit, then use those withdrawn funds as your 5% deposit when applying for the scheme guarantee. Many of the first home buyers we work with take this route.

Is there an income limit for the first home super saver scheme?

No. The FHSSS has no income cap. Any income level can participate, provided you meet the first home owner status, age, and contribution requirements.

How long does the FHSSS withdrawal process take?

From submitting a release request, the typical timeline to receiving funds is 15 to 20 business days, depending on how quickly your super fund processes the release authority from the ATO. Build in time. Don’t plan to receive funds and make an offer in the same week.

Getting help from a mortgage broker

The FHSSS makes the most sense if you have at least two years before you want to buy and you’re contributing at or near the $15,000 annual limit. For buyers on shorter timelines, or those already close to their deposit target, the tax benefit may not be enough to justify the complexity of the withdrawal process.

Our mortgage brokers work with first home buyers across Western Sydney every week. We can run the numbers on your specific situation: what FHSSS contributions would add to your deposit, which other schemes you qualify for (including the stamp duty concessions available to first home buyers in NSW), and what your realistic purchase timeline looks like based on current lender conditions.

Speak to a mortgage broker at Mortgage World Australia to get a clear picture.

This article contains general information only and does not constitute financial advice. Your personal financial situation, objectives and needs have not been considered. Before acting on any information, you should consider its appropriateness to your circumstances. Speak to a qualified mortgage broker for advice tailored to your situation. Mortgage World Australia Pty Ltd is a credit representative (CR No. 396946) of Mortgage Specialists Pty Ltd (Australian Credit Licence No. 387025).

Author: Patrick O’Brien, Director and Home Loan Specialist since 2001

Patrick is a Director and a Home Loan Specialist. He has been helping Australians with home loans since 2001. Prior to working as a mortgage broker Patrick was employed by Macquarie Bank for 3 years and also worked as an accountant for a publicly listed company. Patrick’s qualifications include:

Bachelor of Business, UTS Sydney. Majored in accounting and sub-majored in Finance and Marketing.

Diploma of Finance and Mortgage Broking Management FNS50310

Certificate IV in Financial Services (Finance/Mortgage Broking) FNS40804

Ready to Take the Next Step?

Whether you’re looking to buy your first home, refinance, or explore investment opportunities, Mortgage World Australia is here to help.

Fill out the contact form below, and one of our expert mortgage brokers will be in touch shortly to discuss your needs and guide you through your options.

Get Started Today!