Offset Account: How It Works & How Much You’ll Save

Offset account: how it works and how much you’ll save

On this page ▾

By Patrick O’Brien, Director and Home Loan Specialist, Mortgage World Australia (since 2001)

An offset account is a transaction account linked to your home loan. Every dollar you hold in it reduces the balance your lender uses to calculate interest. You’re not earning interest on your savings, you’re reducing the interest you owe. For most borrowers with consistent savings, the math is compelling.

We’ve set up offset accounts across hundreds of client loans over two decades. The most common reaction when clients first see the savings calculation is: “Why didn’t my bank explain this properly?” This guide answers that question and walks you through everything you need to know.

What is an offset account?

An offset account is a bank account linked directly to your mortgage. The balance in that account is “offset” against your loan balance when your lender calculates interest.

If your loan balance is $500,000 and you have $30,000 in your offset account, your lender calculates interest on $470,000, not $500,000. The $30,000 has effectively cancelled out $30,000 of your loan for interest purposes.

Your required repayments don’t change. The offset account doesn’t pay down your loan directly. But because you’re paying less interest each month, more of each repayment goes toward the principal. The loan pays off faster.

Most offset accounts today are full offset accounts: every dollar you hold reduces your loan balance dollar-for-dollar. Older loans sometimes use a partial offset, which caps the amount you can offset at 50% of the loan balance. Check your loan documentation or contact your lender if you’re unsure which type you have.

How do offset accounts work?

How interest calculations work with an offset

Australian home loans use daily rest interest. Your lender calculates the interest charge every single day based on your outstanding loan balance. The charges accumulate and are added to your account each month.

With an offset account linked, the daily calculation works like this:

Daily interest = (Loan balance minus offset balance) x annual interest rate divided by 365

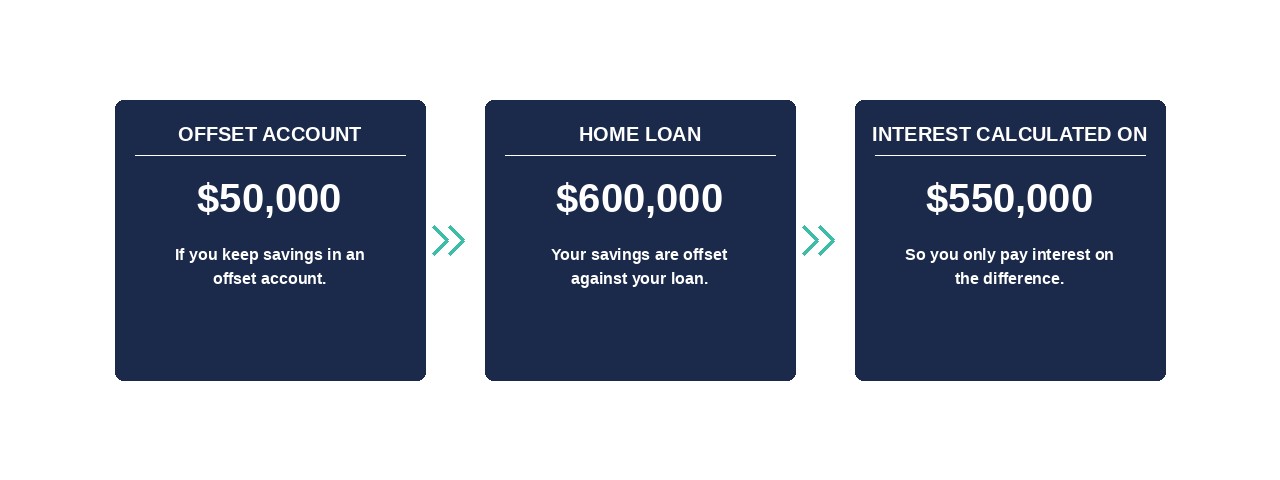

Here’s how that plays out on a $600,000 loan at 6%:

| Scenario | Loan balance | Offset balance | Effective balance | Daily interest |

|---|---|---|---|---|

| No offset | $600,000 | $0 | $600,000 | $98.63 |

| $50,000 offset | $600,000 | $50,000 | $550,000 | $90.41 |

The difference is $8.22 per day, or about $250 per month. Your minimum repayments stay the same in both scenarios. But in the offset scenario, $250 more of each repayment reduces your principal rather than paying interest. Over a 30-year loan, that compounds substantially.

Routing your salary through your offset account amplifies this effect. Even if money comes in and goes out within a few weeks, those days where the balance is high are reducing your daily interest charge. The benefit is proportional to both the balance and how long it sits there.

Why banks offer offset accounts

Banks offer offset accounts because they keep your money in their system. Your savings sit in a linked transaction account, which means your day-to-day banking stays with the same institution. The bank earns from your transaction behaviour, and you benefit from reduced interest. Both sides win.

Offset accounts are usually packaged with annual fees, typically $300 to $400 per year on a home loan package. Whether that cost makes sense depends on your offset balance. At a 6% interest rate, you need roughly $6,000 to $7,000 sitting in your offset account just to break even on a $400 annual fee. Most borrowers with consistent savings well exceed that threshold.

Key benefits of offset accounts

Reduced interest payments (savings example)

The savings are straightforward to calculate. At a 6% interest rate, every $10,000 in your offset account saves approximately $50 per month:

$10,000 x 6% divided by 12 months = $50/month saved

Scale that up to a realistic household scenario:

$600,000 loan at 6%, 30-year term

| Offset balance | Monthly interest saving | Annual saving |

|---|---|---|

| $20,000 | ~$100 | ~$1,200 |

| $50,000 | ~$250 | ~$3,000 |

| $100,000 | ~$500 | ~$6,000 |

These figures are for a single year. Because the savings reduce the principal faster, the loan balance in year two starts lower, which means interest charges in year two are also lower. The savings compound across the loan term.

A borrower with $50,000 consistently in their offset account on a $600,000 loan at 6% would typically save around $80,000 to $100,000 in total interest over 30 years and cut two to four years from the loan term, assuming the offset balance stays consistent and the rate doesn’t change significantly.

If you’re on a fixed-rate loan, check whether your lender allows offset accounts during the fixed period before you lock in your rate. Most major Australian banks offer offset primarily on variable-rate loans. Some restrict the feature entirely during a fixed term or cap the offset benefit.

The 6% rate used throughout this guide is for illustrative purposes. Your actual saving depends on your loan rate. Check your current rate with your lender or a mortgage broker for figures specific to your loan.

Access to your money

Offset account funds are completely accessible. You can withdraw them at any time for any reason, no approval required.

This matters more than most people realise. If you put $30,000 of extra repayments directly into your mortgage, that money is inside the loan. To access it, you need to request a redraw, which some lenders restrict or charge fees for, and which isn’t always instant. If you hold that same $30,000 in an offset account, it’s available immediately through standard banking.

For households with irregular income (commission-based income, bonuses, self-employment), this liquidity is worth having. You can park lump sums in the offset account, reduce your interest charge while they’re there, and move the money when you need it. No formal redraw process needed.

The tax advantage over a savings account

Here’s a comparison most people don’t think to make.

Your offset account reduces interest at your home loan rate. If your rate is 6.2%, the interest saved on money sitting in your offset works at that same 6.2%, not the lower rate a savings account pays. A high-interest savings account might advertise 4.5%, which sounds close, but there are two reasons it falls well short.

First, the savings account rate is already lower. Second, the interest you earn in a savings account is taxable income. At the 45% marginal rate (plus 2% Medicare levy), a $50,000 balance earning 4.5% generates $2,250 in interest annually. After tax, you keep around $1,192. That’s an effective return of about 2.4%.

The offset account saves you 6.2% on that same $50,000, and that saving is not income. The ATO doesn’t tax money you didn’t earn. Every cent stays in your pocket.

So the real comparison isn’t 6.2% vs. 4.5%. It’s 6.2% (tax-free) vs. roughly 2.4% to 3.0% depending on your marginal rate. The higher your income, the bigger the gap.

For most borrowers in the 32.5% tax bracket or above, an offset account outperforms a savings account by a significant margin on an after-tax basis. This is one reason financial advisers often recommend keeping liquid savings in an offset account rather than a separate high-interest account.

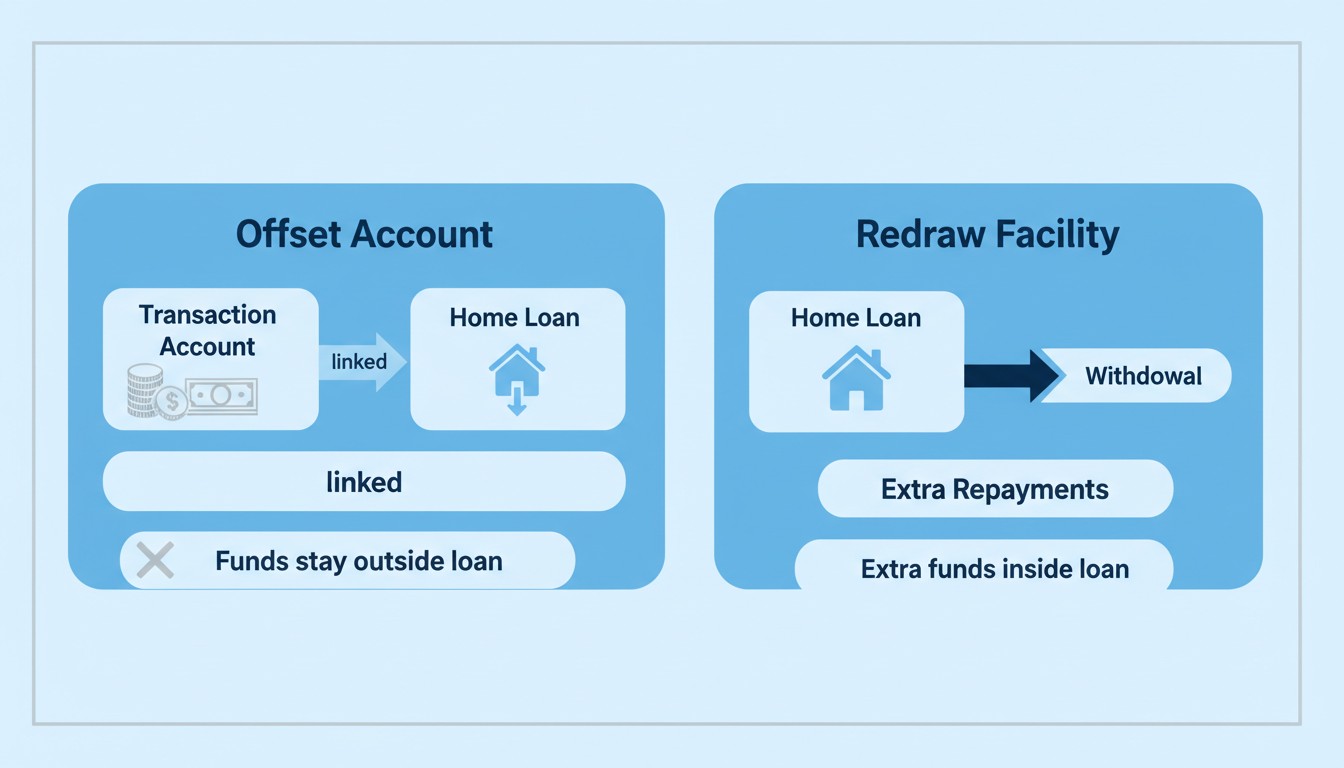

Offset account vs. redraw

Both features let your savings work against your mortgage, but they operate differently. Here’s a direct comparison:

| Offset account | Redraw facility | |

|---|---|---|

| How it works | Separate account; balance reduces daily interest | Extra repayments into loan; access them later |

| Access to funds | Immediate, like a standard bank account | May require lender approval; some restrictions apply |

| Effect on loan balance | Loan balance stays the same | Extra repayments reduce the loan balance |

| Tax implications (investment loans) | Loan balance unchanged; full interest deductibility maintained | Redrawn funds may affect deductibility if used for non-investment purposes |

| Available on fixed-rate loans | Less common; often restricted | Available on most loan types |

| Typical fee | Often part of a packaged loan (annual fee applies) | Often free |

The tax point on investment loans is the most consequential difference, and it’s frequently misunderstood by investors.

When you make extra repayments directly into an investment loan and later redraw that money for personal use (a holiday, a car, home renovations), the ATO may treat those redrawn funds as new private borrowing. That portion of the loan interest is no longer deductible, even though you’re using the same loan account. Your deductible balance shrinks.

An offset account sidesteps this entirely. The loan balance never changes. You’re not making extra repayments into the loan, so there’s nothing to redraw. Your savings sit in a separate account, and the full loan balance remains intact. All of the interest on it stays deductible.

To make this concrete: say you have a $600,000 investment loan and you make a $20,000 extra repayment, then later redraw it for personal renovations. The ATO may treat that $20,000 as private debt. The interest on it (at 6%, roughly $1,200 per year) is no longer deductible. Over 20 years, that’s $24,000 or more in lost deductions. An offset account sidesteps this entirely because you never pay extra into the loan in the first place.

For investors holding multiple properties or planning to access equity later, this distinction can save thousands of dollars in tax deductions annually. It’s one of the main reasons we recommend offset accounts over extra repayments for investment loans. Speak to your accountant about your specific situation before deciding which approach suits your investment loans.

You can also have both. Many loan packages include both an offset account and a redraw facility. They serve different purposes and don’t cancel each other out.

Common questions about offset accounts

What is an offset account and how does it work?

An offset account is a transaction account linked to your home loan. The balance reduces the loan balance your lender uses to calculate daily interest. If you have a $500,000 loan and $40,000 in your offset account, you pay interest on $460,000. Your minimum repayments stay the same, but more of each payment reduces the principal.

How much money can you save with an offset account?

At a 6% interest rate, each $10,000 in your offset account saves approximately $50 per month. A consistent balance of $50,000 saves roughly $250 per month, or $3,000 per year. Over a 30-year loan, that compounds into tens of thousands of dollars in interest saved.

Is an offset account worth it?

It depends on your offset balance and whether your loan includes an annual fee. If your offset account holds $30,000 or more consistently, the interest savings typically outweigh a standard package fee. If your savings are modest, say under $10,000, the maths may not stack up. A mortgage broker can run the numbers for your specific situation.

Can you withdraw money from an offset account?

Yes. Offset account funds are fully accessible at any time. You can withdraw, transfer, or spend freely. The remaining balance continues to offset your loan interest.

What is the difference between offset and redraw?

An offset account holds your funds separately, reducing daily interest without changing your loan balance. A redraw facility lets you access extra repayments you’ve already made into your loan. Offset gives more flexibility and better tax outcomes for investment loans. Redraw is simpler but has tax complications if investment loan funds are later used for personal purposes.

Do all banks offer offset accounts?

No. Most major Australian lenders offer offset accounts, typically on variable-rate loans as part of a packaged product. Offset accounts are less commonly available on fixed-rate loans. Some lenders restrict the feature entirely during a fixed period. Confirm availability before you fix your rate.

Can you have multiple offset accounts?

Some lenders allow multiple offset accounts linked to a single loan. This helps with managing separate savings goals (a holiday fund, an emergency reserve) while all balances contribute to reducing loan interest. Not all lenders offer this, so check with your broker or lender.

Are offset accounts taxed?

Offset accounts don’t earn interest, so there’s no interest income to declare on your tax return. You’re reducing the interest you owe, not earning income. For owner-occupied loans, there are no tax implications. For investment property loans, the interest you continue to pay on the loan remains fully tax-deductible. The offset account does not affect that deductibility, which is one of its key advantages.

Should you use an offset account?

Offset accounts deliver the most value when you have consistent surplus cash in your account. The larger and more stable the balance, the more you save. A balance that fluctuates between $5,000 and $10,000 produces modest savings. A balance that sits at $50,000 or higher produces meaningful ones.

An offset account makes strong sense if you:

- Have a variable-rate home loan and regularly carry $20,000 or more in your transaction account

- Are paid a salary or receive income that sits in your account for days or weeks before you spend it (those days count)

- Own an investment property and want to preserve the tax deductibility of your loan

- Want flexible access to your savings without locking funds into the loan

- Already have a packaged loan that includes offset at no extra cost

An offset account is less valuable if:

- Your savings balance is consistently under $10,000, and your loan has an annual package fee

- You have a fixed-rate loan where offset features are restricted or unavailable

- You have a disciplined investment strategy elsewhere earning more than your mortgage rate after tax (in the current rate environment, that’s a higher bar than it used to be)

There’s no one-size-fits-all answer. Your loan rate, your savings habits, your tax position, and what your lender offers all factor in. That’s exactly the kind of assessment a mortgage broker can run across multiple lenders, not just one.

Get expert advice from a mortgage broker

Offset accounts are a feature. But which lender’s offset account, and which loan package, makes a real difference to the outcome. Full offset, partial offset, fee structure, fixed-rate eligibility — these details add up. We compare products across 52+ lenders, so you don’t have to.

At Mortgage World Australia, we’ve been helping Australians get their home loan structure right since 2001. We work with clients across Parramatta, Western Sydney, Blacktown, Wentworthville, Greystanes, and surrounding suburbs. If you want to know whether an offset account suits your loan and your lender, book a free consultation.

This article contains general information only and does not constitute financial advice. Your personal financial situation, objectives and needs have not been considered. Before acting on any information, you should consider its appropriateness to your circumstances. Speak to a qualified mortgage broker for advice tailored to your situation. Mortgage World Australia Pty Ltd is a credit representative (CR No. 396946) of Mortgage Specialists Pty Ltd (Australian Credit Licence No. 387025).

Patrick is a Director and a Home Loan Specialist. He has been helping Australians with home loans since 2001. Prior to working as a mortgage broker Patrick was employed by Macquarie Bank for 3 years and also worked as an accountant for a publicly listed company. Patrick’s qualifications include:

Bachelor of Business, UTS Sydney. Majored in accounting and sub-majored in Finance and Marketing.

Diploma of Finance and Mortgage Broking Management FNS50310

Certificate IV in Financial Services (Finance/Mortgage Broking) FNS40804

Ready to Take the Next Step?

Whether you’re looking to buy your first home, refinance, or explore investment opportunities, Mortgage World Australia is here to help.

Fill out the contact form below, and one of our expert mortgage brokers will be in touch shortly to discuss your needs and guide you through your options.

Get Started Today!