Bank Property Valuation Australia: Process & Low-Val Fix

Bank property valuation Australia: how it works, when it comes in low, and what to do (2026 guide)

On this page ▾

- What is a bank property valuation?

- Why most home loans don’t even need a full valuation

- How a bank valuation works (when one is done)

- The five types of bank valuation: desktop, kerbside, full, AVM, and construction

- How long a bank valuation takes

- What a bank valuation costs and who pays

- Bank valuation vs market value

- What the valuer looks at

- How the big four order property valuations

- Why some lenders value higher than others

- When valuations actually come in low

- What happens if the bank valuation is lower than the purchase price

- The low-valuation recovery playbook

- How to prepare your property for a bank valuation

- What your broker can tell you about the bank’s valuation

- How a mortgage broker helps with valuations

- FAQ

- Speak to a mortgage broker about your valuation

Most home buyers don’t need to worry about the bank valuation. If you’re buying an established property through a real estate agent and borrowing less than 80% of the purchase price, the bank in 2026 will often skip the valuation altogether and accept the contract price as the value. If a valuation is ordered, it is increasingly likely to be a desktop assessment with no inspector ever attending the property. Full valuations have become the exception, not the rule.

That’s not the message most articles on this topic deliver. The internet is full of pieces written to manage worst-case scenarios, and they’ve created a level of anxiety the actual process doesn’t justify. In our 25 years of mortgage broking, established residential purchases come back at contract price 99% of the time.

The bank valuation does become a real story in four specific situations. Off-the-plan apartments. Brand new properties bought through property marketing companies. Some house-and-land packages. And refinances or equity releases where the owner has formed an inflated view of what their home is worth. In those cases, the valuation is the part of the application that decides whether the deal survives, and that is where this guide becomes useful.

This is the working broker’s view of how bank valuations actually run in Australia in 2026 — what they are, when they happen, when they don’t, who orders them, when they come in low, and what to do if yours does.

What is a bank property valuation?

A bank property valuation is an independent assessment of what a property is worth, used by the lender to size the loan against the security. It exists for the bank’s benefit. The number protects the lender from lending more than the property could realistically recover if the loan went bad and the property had to be sold.

The valuer is a qualified, licensed professional with professional indemnity insurance. They sit on the lender’s valuation panel and report to the bank’s credit team. You do not choose them.

Bank valuation vs market appraisal vs automated estimate

These three numbers get confused constantly because the questions they answer sound similar. They aren’t.

A market appraisal is what a real estate agent gives you to win a listing. It is opinion-led and there is no professional indemnity behind it. An automated valuation model (AVM), the kind that powers consumer property apps from the big four, is a statistical estimate generated by a computer using comparable sales data with no inspection. The AVMs in the CommBank, NAB, ANZ, and Westpac apps are all variations of this. A bank valuation is the signed, regulated, indemnified opinion of value used as the basis for credit decisions. When something goes wrong on a deal, the bank valuation is the number that matters.

Why most home loans don’t even need a full valuation

The single most useful thing to understand about bank valuations in 2026 is that the average residential home loan no longer triggers one. Lenders have moved a long way toward streamlined processing, and they now accept the contract price as the value in two very common scenarios:

- The property is being purchased through a real estate agent on the open market

- The loan-to-value ratio is below 80%

When both of those conditions are met, most lenders accept the contract of sale as evidence of value. No valuer attends. No report is written. The loan is sized on the contract price and the application moves directly to credit assessment.

When a valuation is required, it is usually a desktop. A computer pulls comparable sales data and produces a number — typically within a day. Full physical inspections still happen, but they have become the exception. They are reserved for higher-LVR applications, larger loan amounts, unusual property types, regional locations, and the four scenarios covered later in this guide.

This shift has made the home loan process noticeably faster than it was even five years ago. We see this at MWA constantly: borrowers stressed about a valuation that, in their case, the bank is never going to order.

How a bank valuation works (when one is done)

The process is consistent across the big four when a valuation is required.

Who orders it

In most cases, the broker orders the valuation on the bank’s behalf. The broker has ordering access through the lender’s valuation portal, which means the request goes out the same day the application moves into that phase. The broker doesn’t choose which valuation firm gets the job (that’s controlled by the lender’s panel rotation), but the broker can lodge the order, track it, and act as the contact point for the valuer.

When the report comes back, it goes to the broker. The report is technically for the bank’s use, and cannot be shared with a client. Only the valuation amount can be shared by the broker. Trying to obtain the same report directly from the bank, without a broker in the chain, is much harder. That’s a real benefit of going through a broker rather than direct to a lender.

Step 1 — Inspection (30 to 60 minutes, full only)

For a full valuation, the valuer attends the property and walks through it inside and out. They photograph rooms, measure floor area, note condition, and flag anything unusual — easements, zoning irregularities, structural concerns. For a kerbside, they only inspect the exterior. For a desktop or AVM, no one visits.

Step 2 — Research and report (2 to 3 business days)

The valuer pulls comparable settled sales from the same suburb, ideally within the last six months. They adjust for differences and write up the report with photos, comparables, zoning notes, and the final figure. Two to three days, in our experience.

Step 3 — Delivery to the broker, then the bank

The completed report goes to the broker, who passes it to the lender’s credit team. The credit team uses it to confirm the loan amount, calculate the LVR, and decide whether the application proceeds.

End-to-end, allow 2 to 5 business days from inspection for a full valuation, and around a day for a desktop. If the broker orders the valuation early in the application process, the timeline often runs in parallel with the credit assessment rather than after it.

The five types of bank valuation: desktop, kerbside, full, AVM, and construction

Five valuation types come up in residential lending. Lenders pick based on risk and on what stage the property is at — the lower the perceived risk to the bank, the lighter the valuation.

Desktop valuation (the modern default)

A desktop valuation uses comparable sales data with no physical inspection at all. Lenders use desktops for refinances of well-known properties, low-LVR purchases in established suburbs, and equity releases on existing securities. They are quick, free to the borrower, and they have become the dominant valuation type for residential applications in 2026.

Kerbside valuation

A kerbside valuation involves an external inspection only. The valuer drives past, takes a photo from the street, confirms the property exists and matches the description, and pulls comparables. Kerbsides sit between desktops and full valuations on the risk scale and are now relatively rare.

Full valuation

Full valuations are mandatory for higher-LVR purchases, larger loan amounts, off-the-plan stock, brand new builds without comparable sales history, regional locations, and any application the credit team decides needs eyes on the security. The trigger thresholds vary by lender, but as a rule of thumb, expect a full valuation when the LVR is above about 80%, the loan is well above $1 million, the property is non-standard, or the application is investment with multiple securities. Short-form valuations — a halfway product between desktop and full — are also becoming less common.

Automated valuation model (AVM) — and why it’s not what’s in your CommBank app

The AVM that runs your CommBank app’s property estimate is the same statistical model approach a lender might use for a desktop, but it runs for marketing and customer engagement, not credit assessment. Westpac’s own AVM disclaimer states the estimate is generated without inspection, does not take into account market conditions, and is not a professional valuation. Treat the consumer-app number as a ballpark for your own planning. Do not assume the bank will lend against it.

Construction valuation (TBE — to be erected)

A construction valuation, sometimes called a TBE valuation (short for “to be erected”), is the type used when the property does not yet physically exist. It is the standard valuation for construction loans, off-the-plan apartments, and house-and-land packages. The valuer assesses the property based on the plans, specifications, and contract of sale, and produces an “as if complete” value alongside the underlying “as is” land value.

For staged construction loans, progressive valuations may also be ordered as the build hits each milestone — slab, frame, lock-up, fixing, completion — to confirm the work is on track before the lender releases the next progress payment. TBE valuations are also where the off-the-plan and brand-new low-valuation risk shows up most clearly, because the contract price was set well before the comparable sales evidence existed.

How long a bank valuation takes

When one is required, a full bank valuation typically takes 2 to 5 business days from inspection until the report lands with the credit team. A kerbside or desktop usually turns around in about a day. Allow up to a week end-to-end if the panel is busy or vendor access is delayed.

Going through a broker shortens the perceived timeline. Because the broker initiates the order rather than waiting for the bank’s internal process to reach that step, valuations often complete in parallel with the rest of the credit assessment.

What a bank valuation costs and who pays

For a standard residential home loan, the lender almost always absorbs the valuation cost. It is built into the bank’s application processing, not billed separately to the borrower. This is true for the four big lenders and most second-tier banks.

Three scenarios change this. Low-doc and specialist lending products often itemise the valuation fee separately. Commercial loans and complex investment structures usually pass the cost on. And any disputed or re-instructed valuation the borrower asks for is generally on the borrower.

If you are paying directly, expect the following ballpark for the Australian market in 2026:

- Desktop or kerbside: from around $200 to $300

- Full valuation: $400 to $600 or more, depending on property value and location

- Specialist or rural property: $700 plus

Bank valuation vs market value

A property can have two simultaneously valid prices. They are not in conflict — they answer different questions.

| Bank valuation | Market value (agent appraisal) | |

|---|---|---|

| Purpose | Loan security | Sale negotiation |

| Author | Licensed valuer on lender panel | Real estate agent |

| Liability | Professional indemnity | None |

| Timeline | Used at the loan settlement date | Used at listing or contract date |

| Bias | Conservative | Optimistic |

| Cost | Often $0 to borrower | Free (agent listing tool) |

| Sees | Comparable settled sales, condition | Comparable listings, marketing potential |

Why bank valuations are conservative by design

The bank is not asking what the property might fetch in a competitive auction. It is asking what the property would clear for if it had to be sold quickly under pressure, perhaps in a softer market than today’s. That sometimes gets called the forced-sale value. Conservative isn’t pessimistic. It’s what protects the bank from lending against a number that only holds up in perfect conditions.

Why the agent’s appraisal and the bank’s number can disagree

The agent is incentivised to win the listing, which often means quoting a number toward the upper end of plausibility. The bank valuer has the opposite incentive — their professional indemnity is on the line if they over-value. A 3% to 5% gap between the two numbers is not unusual on the higher-risk property types covered later. On established residential property, the bank valuation almost always matches the contract price, which itself was negotiated at market.

When the bank valuation comes in higher than the purchase price

This is rare. In our experience it tends to happen in three specific situations: an off-the-plan property settling more than 12 months after the original contract was signed, where the market has risen in the intervening period; a family purchase where the property is being transferred at a discount; and very occasionally, off-market sales arranged by a real estate agent — we’ve seen this only a handful of times in 25 years.

When it does happen, the loan is still calculated on the lower of the two — the price you have agreed to pay — but you walk in with instant equity. Your LVR works in your favour, which can mean lower or no LMI. The higher number sits there as a tailwind for any future refinance or equity release.

What the valuer looks at

When a full inspection is ordered, the valuer focuses on a small number of inputs.

Location, condition, size, comparable sales

Recent settled sales of comparable properties in the same suburb are the single biggest input. Location accounts for the next biggest slice — postcode, street, position on the street, proximity to transport, school catchments. Condition matters but it is rarely the swing factor. Size, both internal floor area and land, anchors the comparison.

The walk-through factors most borrowers don’t expect

Access, layout flow, and zoning overlays move numbers more than borrowers expect. Flood overlays, bushfire attack level (BAL) ratings, and unusual easements can knock five-figure sums off a valuation. Sub-50-square-metre apartments, unit blocks of four or more, regional or semi-rural properties, and anything with a non-standard title attract conservative valuations as a category.

Proximity to high-voltage power lines and railway lines is another factor borrowers rarely think about until it shows up on the valuation. Some lenders have credit-policy issues with properties that sit too close to either, particularly at higher LVRs. The valuer captures these as environmental factors in the report, which feeds into the lender’s risk assessment.

The risk analysis grid on a short-form valuation report

Short-form valuation reports include a risk analysis grid that most borrowers never see and most articles never mention. The valuer rates the property and the surrounding market against eight categories on a 1 to 5 scale, where 1 is low risk and 5 is high risk:

- Property risk ratings: location/neighbourhood, land (including planning title), environmental issues, improvements

- Market risk ratings: market direction (price), market activity, local/regional economy impact, market segment conditions

Ratings of 1, 2, or 3 are generally fine. The problem starts when the valuer assigns multiple 4s or 5s. Some lenders have policies that decline or restrict applications above 80% LVR when the risk grid carries enough high ratings — even if the headline valuation figure itself comes in at contract price. Power lines, railway lines, flood overlays, and BAL ratings tend to push the environmental issues rating up. A weak local economy or a market in clear retreat pushes the market direction and economy ratings up. The risk grid is the part of the report that decides whether some lenders will fund the loan, and most borrowers never see it.

How the big four order property valuations

Each of the big four runs a slightly different consumer-facing property estimate tool, and a separate, completely walled-off internal valuation process for credit decisions. Borrowers who Google their own bank’s name plus “valuation” are usually looking at one and reading about the other.

The valuation that matters for your home loan is the one ordered by the credit team — usually via the broker on the bank’s behalf — not the one shown in the app. Borrowing capacity sits underneath all of this, see our guide to how much you can borrow for the full mechanics.

Commonwealth Bank — the CommBank Property Report

CBA’s consumer-facing tool is the CommBank Property Report, which offers a price estimate using AVM data and recent sales, with the underlying data licensed from Cotality. The tool is positioned as a research aid, and the disclaimers make clear it is not a bank valuation for credit purposes. If you are mid-application with CBA, the number you see in the app is not the number their credit team is using.

NAB — NAB Property Insights and the valuation process

NAB’s customer property tool is called NAB Property Insights. It surfaces estimated price ranges and recent sales. NAB’s actual loan valuation runs through its own valuation panel. NAB’s published guidance puts the typical valuation timeline at 2 to 5 business days from inspection.

ANZ — ANZ Property Profile Report

ANZ surfaces a free customer tool called the ANZ Property Profile Report. ANZ’s own description states the report provides a price range estimate and is explicitly not a valuation, not a guarantee of market value, and the price ranges may change daily. Like the others, the credit-grade valuation is ordered separately by ANZ’s credit team.

Westpac — Property Market Research, powered by Cotality

Westpac’s borrower-facing tool is called Property Market Research, and the underlying data is licensed from Cotality, the global property data group formerly known as CoreLogic. Cotality acquired Australia’s RP Data in 2011 and adopted the current name in 2025. Westpac’s own AVM disclaimer states the estimate is generated by a mathematical model without inspection, does not consider market conditions, and is not a professional valuation. Worth knowing: the same Cotality data sits behind much of the Australian property estimation industry, including the reports we run for our own clients.

Why some lenders value higher than others

In our experience, valuations on the same property can land at different numbers across different lenders. Same security, same week, two different valuers off two different panels, two different reports. On established residential property bought through an agent, those gaps tend to be small or nonexistent. On the four scenarios covered next — off-the-plan, brand new builds, H&L, and refinance — the gaps can be material.

This is the angle nothing on the rest of the search results page covers properly, and it is also the angle a broker has unique visibility into.

Valuation panels and suburb-level bias

Each lender’s valuation panel covers different geographic patches and uses different firms. A panel that handles a lot of Western Sydney apartments will have valuers with deeper comp data on stock that another panel only sees occasionally. Some firms run more conservative caveats. Others lean closer to the comp average. The differences add up across enough cases to matter.

Where lender choice materially moves the number

Lender choice tends to move the valuation most on:

- Off-the-plan apartments, especially sub-50-square-metre and studio stock

- Brand new properties without an established sales history

- Unit blocks of four or more units

- Regional and semi-rural properties

- Refinance and equity release applications where the owner is asking the property to support a larger loan

It tends to move the valuation least on routine established-property purchases. If you are buying a three-bed brick home in an established Sydney suburb at a normal market price, you are extremely unlikely to see a meaningful valuation difference between lenders.

How a broker uses this at application stage

Knowing which lender’s panel currently handles which property types favourably is part of the daily reading a broker does. We don’t promise outcomes. We do route the application toward the lender most likely to value the property accurately. For further reading on this, see our piece on choosing the right lender for a better valuation.

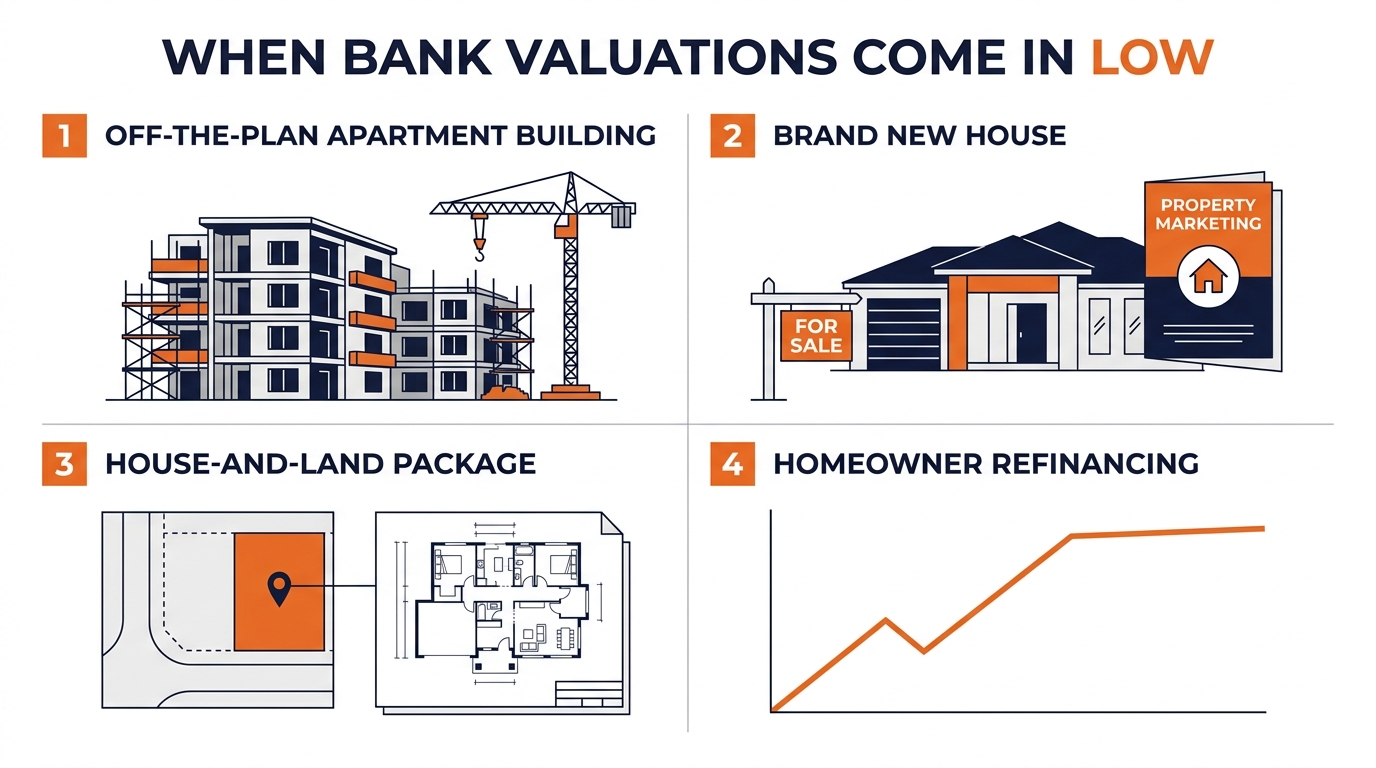

When valuations actually come in low

The four scenarios where low valuations happen often enough to plan for.

1. Off-the-plan apartments

Off-the-plan is the single most common source of low valuations. The contract price was set during the marketing phase, often well before construction completed, and frequently above the price the secondary market will support by the time settlement comes around. By the time the bank’s valuer attends, the comparable sales tell a different story to the contract. Sub-50-square-metre stock, oversupplied corridors, and developments where the marketing pushed pricing aggressively are the highest-risk subset.

2. Brand new properties bought through property marketing companies

Brand new properties marketed through property investment firms or buyer’s agents — the kind sold with rental guarantees, depreciation projections, and weekend information sessions — frequently come back below contract. The marketing margins, the developer commission, and the agent commission all sit inside the contract price. A bank valuer comparing against the surrounding existing market will not include those costs. We’ve seen valuations come in 5% to 10% below contract on stock of this type.

3. House-and-land packages

H&L sometimes runs into the same issue, especially in newly developing suburbs where comparable settled sales of completed homes don’t yet exist. The land contract and the build contract are valued separately. The combined contract value can outpace what a valuer can support against the early sales in the estate.

4. Refinance and equity release

Refinances and equity releases are the other major source. The owner has formed a view of their property’s value — often based on what neighbours have asked, or what the agent down the road quoted at a kerbside — and that view tends to run optimistic. Valuers tend to run conservative. The gap between the two becomes the gap between the loan amount the owner expected and the loan amount the bank will fund.

This is also where lender selection has the most upside. Different lenders’ valuation panels can land on materially different numbers on the same refinance security. We have moved equity release applications between lenders mid-process specifically to access a panel that has historically valued the suburb or property type higher.

What happens if the bank valuation is lower than the purchase price

This is the worked example, with real numbers.

You have a contract to buy at $850,000 — say, an off-the-plan apartment in Parramatta, settling 18 months after the original contract was signed. You have $170,000 saved as a deposit, which is a clean 20%. You assume a $680,000 loan, an 80% LVR, and no LMI.

The bank valuation lands at $820,000.

The loan amount does not automatically reduce. You still need to fund the $850,000 purchase. With $170,000 of your own money in, the loan is still $680,000. The lender now sizes that loan against the lower of valuation or price, which is $820,000.

The LVR mechanics

Your loan-to-value ratio recalcs as $680,000 ÷ $820,000 = 82.9%. Just under 83%.

Above 80% is the threshold that matters. The clean 20% deposit purchase has quietly become a high-LVR loan. Model this on our LVR calculator or read the full mechanics in our guide to loan-to-value ratio (LVR).

The LMI trigger you didn’t budget for

LMI is the insurance the lender takes out, at the borrower’s expense, to cover the bank above 80% LVR. The premium is calculated by the LMI insurer — in Australia that’s most often Helia (the company formerly known as Genworth Australia, rebranded in 2022) or QBE LMI — using the loan amount, the LVR, the loan term, and the occupancy type.

For an owner-occupier loan of $680,000 at an LVR just under 83% over a 30-year term, indicative 2026 LMI premiums typically land somewhere in the $7,500 to $8,500 range. Investor occupancy and longer terms push the upper end higher. Run the exact figures through our LMI guide for the full breakdown.

A valuation $30,000 below contract has cost roughly $7,500 to $8,500 the borrower had not budgeted for, plus the loan now sits above 80% LVR. That’s the moment the recovery playbook starts.

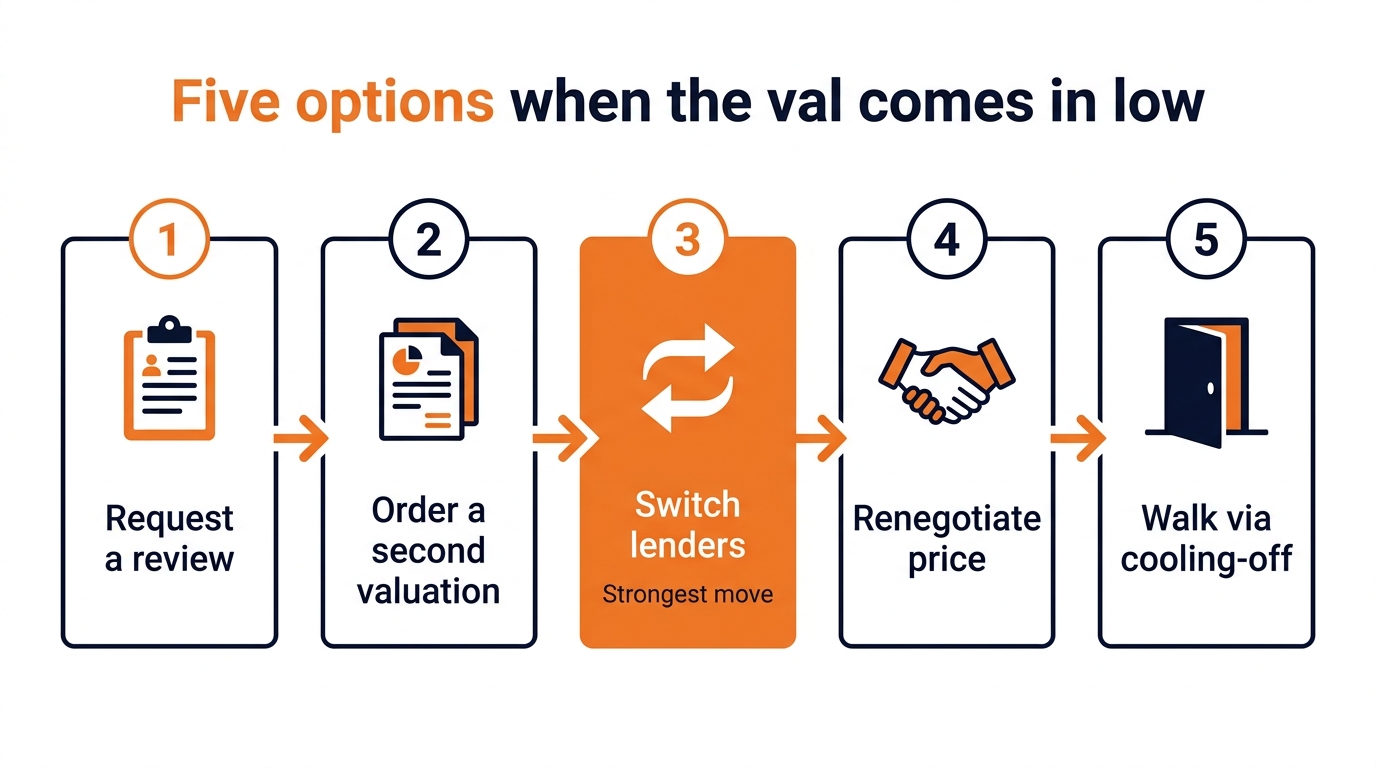

The low-valuation recovery playbook

Five real options. Each works in different situations.

Option 1 — Request a valuation review with comparable sales evidence

Technically possible, but be realistic about the success rate. The lender accepts a request to review the valuation, the original valuer revisits the file with comparable settled sales the borrower or broker supplies, and the valuer either holds or moves the number. In practice, holds outnumber movements by a significant margin. Challenging a valuation is normally a futile exercise.

If you do go this route, stick to settled sales (not listings), stay within the last six months, and keep the comparables genuinely like-for-like — same suburb, similar size, similar condition. We supply the comparable sales pack ourselves rather than asking the client to assemble it. The honest framing: a review is worth attempting if the comparables you have access to are clearly stronger than the ones the valuer used. Otherwise, skip ahead to Option 3.

Option 2 — Order a second valuation through the same lender

If the first valuation was a desktop or kerbside, asking for a full inspection is reasonable. The credit team can re-instruct, and the new valuer attends the property. Costs vary — sometimes the lender covers it, sometimes the borrower pays. A second full valuation through the same lender on the same security is harder to get if the first was already a full.

Option 3 — Switch lenders (the broker’s strongest move)

This is the one no one writes about, and it is also the move that actually works most of the time. Different lenders use different valuation panels, and the same property can come back at a noticeably different number through a different panel. Switching lenders means a new valuation through a different panel of valuers, which is exactly the lever that fixes most low-val situations on the high-risk property types.

There is a quiet advantage here that comes with using a broker. With most lenders, we can order a valuation upfront — before we lodge the application — to confirm the number is sufficient. We then know whether that lender’s val will support the loan before we submit anything formally. This saves time, and it also avoids an unnecessary credit enquiry on the borrower’s file from a lender whose valuation was never going to work. On the off-the-plan, brand new, H&L, and refinance scenarios, this is often the difference between a smooth approval and a stalled application.

Option 4 — Renegotiate the purchase price

If the bank valuation is $30,000 below contract and the deal is contingent on finance, the seller has a problem too. The agent has had a buyer pull in finance. Going back to the vendor with the bank’s number is not always possible, but it is worth trying — particularly if the property has been on the market for a while, the vendor is motivated, or the comparable sales the valuer used are fresh and credible.

Option 5 — Walk

If none of the above fixes the gap, the contract itself may give you an exit. Most residential non-auction purchases in NSW have a cooling-off period. A finance clause, if you negotiated one into the contract, gives a different route. The mechanics differ by state and by contract type, so this is the moment to call your conveyancer or solicitor, not Google. If you are still at the pre-approval stage rather than under contract, walking is far cleaner.

How to prepare your property for a bank valuation

You cannot manufacture a higher valuation. You can avoid the things that drag the number down.

For purchases: access, presentation, comparable sales you supply

Make sure the valuer can attend at the booked time. Vendor or tenant access falling through is the single most common reason for a slipped timeline. Tidy presentation is not the deciding factor, but a property that is clean, lit, and easy to photograph reads as cared-for. Where a renovation has been completed in the last 12 months, supply receipts and photos through your broker. Provide a brief comparable sales sheet if you have done the work.

For refinances or equity releases: what actually moves the number

For a refinance or equity release on an investment, most of the same applies, plus one more: if you have done substantial renovations or extensions since the last valuation, the property may now warrant a full inspection rather than a desktop. The full inspection sees the work; the desktop won’t.

This is also where lender selection has the largest payoff. The same security can come back at materially different numbers through different lenders’ panels. If your existing lender’s desktop has come in below your expectations, that is precisely the moment a broker can route the file to a lender whose panel has historically been more accurate on your suburb or property type.

What your broker can tell you about the bank’s valuation

The valuation report itself is the bank’s property and brokers are not permitted to share the physical report with clients. What we can share is the valuation amount, and any flags or issues raised in the report — for example, comments about access, condition, environmental factors, or anything that pushed the risk grid up. That is enough to act on.

Going direct to the bank, without a broker in the chain, is a different story. Lenders are reluctant to release valuation information to borrowers at all — they didn’t commission the report on the borrower’s behalf, and releasing it exposes the lender to potential third-party reliance issues. The broker-channel benefit is not access to the document itself; it is having someone in your corner who has read the report, can interpret what it means for your application, and can act on the issues it raises.

How a mortgage broker helps with valuations

The valuation is one of the few parts of the home loan process where independent advice has a meaningful effect on the outcome. Three concrete things a broker brings:

Independent property data before you commit. We have direct access to Cotality property reports — the same data source that sits behind much of the Australian property estimation industry, including some of the big four’s consumer tools. Before you put in an offer or sign an off-the-plan contract, we can run a Cotality report on the property to give you a defensible third-party number to anchor your negotiation against. It is not a bank valuation, but it is the same automated valuation data the major lenders license.

Lender selection at panel level. We know which lender’s panel currently treats which property types favourably. That mostly matters on the four scenarios where low valuations happen — off-the-plan, brand new, H&L, and refinance/equity release. With access to 52+ lenders, we can route the application toward the panel most likely to return an accurate number, and switch lenders mid-process if the first val comes back low.

Speed, ordering, and interpretation. Because we order the valuation on the bank’s behalf, the request goes out faster than waiting on the bank’s internal queue. With most lenders we can also order an upfront valuation before lodging the application, so we know whether the number will support the loan before we touch your credit file. When the report comes back, we cannot share the document itself, but we can tell you the figure, walk you through any flags or risk issues raised, and act on them.

FAQ

How long does a bank valuation take in Australia?

When one is required, a full bank valuation typically takes 2 to 5 business days from inspection until the report lands with the credit team. A kerbside or desktop usually turns around in about a day. For many established residential purchases under 80% LVR, the bank skips the valuation and accepts the contract price.

How much does a bank valuation cost?

When the bank orders the valuation as part of a standard residential application, the lender almost always absorbs the cost. If you order one privately, expect to pay from around $200 for a desktop or kerbside up to $600 or more for a full inspection.

Who pays for the bank valuation?

For most standard residential applications, the bank pays. The borrower typically pays in three situations: low-doc or specialist lending products, commercial or investment loans above certain thresholds, and disputed re-valuations the borrower has requested.

Are bank valuations lower than the purchase price?

Almost never on established residential properties bought through a real estate agent. In our 25 years of broking, that is where 99% of valuations come back in line with the purchase price. Low valuations cluster in four specific situations: off-the-plan apartments, brand new properties bought through property marketing companies, some house-and-land packages, and refinances or equity releases where the owner has overestimated their property’s value.

Can I challenge a bank valuation?

You can submit comparable sales the original valuer didn’t use, and the lender will arrange a review, but the success rate on valuation challenges is very low. In most cases the better move is to order a fresh valuation through a different lender, which uses a different valuation firm. Challenging a valuation through the original lender is normally a futile exercise.

What happens if the bank valuation is lower than the purchase price?

The loan amount is recalculated against the lower valuation, which pushes your LVR up. If that pushes the LVR above 80%, lenders mortgage insurance is triggered. You then have five options: request a valuation review, order a second valuation, switch lenders, renegotiate the purchase price, or exit the contract through cooling-off or a finance clause.

Can my broker share the bank’s valuation report with me?

No. Brokers are not permitted to share the physical valuation report with clients. The report is the bank’s. What a broker can share is the valuation amount, and any flags or issues raised in the report — for example, comments on access, condition, environmental factors, or risk-rating concerns. That is normally enough information to act on. Trying to obtain the report directly from the bank, without a broker in the chain, is generally not possible either.

Can I order a second bank valuation?

Through the same lender, sometimes. If the first valuation was a desktop or kerbside, asking for a full inspection is reasonable. A second full valuation through the same lender on the same security is harder to get. The cleaner option is a fresh application with a different lender, which automatically triggers a new valuation through that lender’s panel.

Speak to a mortgage broker about your valuation

If you’re buying off-the-plan, signing on a brand new property through a marketing company, going through an H&L package, or refinancing on the basis of your own estimate of equity — the four cases where low valuations actually happen — speak to Mortgage World Australia before you commit. We run independent Cotality reports on the property, we know which lenders value honestly on which property types, and with access to 52+ lenders, we can route the application to the panel most likely to value the property accurately.

If the val on your file has already come in low, we read the report, walk through the five recovery options, and tell you which is most likely to work for your specific deal. If the existing lender’s val can’t be fixed, we move the application to a lender whose panel will value the property accurately.

For Western Sydney buyers, our team operates from Greystanes and works with clients across Parramatta, Blacktown, Wentworthville, and the rest of Western Sydney.

This article contains general information only and does not constitute financial advice. Your personal financial situation, objectives and needs have not been considered. Before acting on any information, you should consider its appropriateness to your circumstances. Speak to a qualified mortgage broker for advice tailored to your situation. Mortgage World Australia Pty Ltd is a credit representative (CR No. 396946) of Mortgage Specialists Pty Ltd (Australian Credit Licence No. 387025).

Patrick O’Brien, Director and Home Loan Specialist since 2001

Patrick is a Director and a Home Loan Specialist. He has been helping Australians with home loans since 2001. Prior to working as a mortgage broker Patrick was employed by Macquarie Bank for 3 years and also worked as an accountant for a publicly listed company. Patrick’s qualifications include:

Bachelor of Business, UTS Sydney. Majored in accounting and sub-majored in Finance and Marketing.

Diploma of Finance and Mortgage Broking Management FNS50310

Certificate IV in Financial Services (Finance/Mortgage Broking) FNS40804

Ready to Take the Next Step?

Whether you’re looking to buy your first home, refinance, or explore investment opportunities, Mortgage World Australia is here to help.

Fill out the contact form below, and one of our expert mortgage brokers will be in touch shortly to discuss your needs and guide you through your options.

Get Started Today!