Does HECS Affect Your Home Loan? 2026 Broker Guide

Does HECS debt affect your home loan? What changed in 2025-26

On this page ▾

- Does HECS affect your home loan? The short answer

- What is HECS-HELP debt and why lenders treat it differently

- How HECS reduces your borrowing power

- The 2025-26 HECS changes every borrower should know

- Which lenders apply the HECS serviceability carve-out

- Should you pay off your HECS before buying a house?

- How to maximise your borrowing power with a HECS debt

- How a mortgage broker helps when you have a HECS debt

- FAQ: HECS debt and home loans

HECS-HELP debt does affect your home loan. When you apply for a mortgage, lenders include your compulsory annual HECS repayment as a committed expense in their serviceability assessment. This reduces the income available to service the loan and lowers the maximum amount you can borrow. For most borrowers, that reduction is somewhere between $15,000 and $80,000 in borrowing capacity, depending on income.

Two major changes took effect in 2025. The repayment system shifted to a marginal model from 1 July 2025, cutting annual repayments for most borrowers. And from 30 September 2025, new APRA rules changed how banks handle HECS in serviceability assessments. If you have HECS and are planning to buy, your position today is materially better than it was 18 months ago – and the gap between lenders has widened.

Does HECS affect your home loan? The short answer

Yes. HECS-HELP debt does not appear on your credit report. But it does reduce your borrowing power, because lenders treat your compulsory annual HECS repayment as a committed monthly expense, the same way they treat a car loan repayment. The higher your income, the higher your annual repayment, and the larger the impact on the maximum loan you can get approved.

Since September 2025, the rules have shifted. All banks must now exclude HECS from the debt-to-income ratio they report to APRA. CBA and NAB have also adopted a serviceability carve-out that allows them to exclude your HECS repayments entirely if your balance is close to zero. Whether you benefit depends on which lender you use and how close you are to paying off your debt.

What is HECS-HELP debt and why lenders treat it differently

How HECS repayments are calculated (income thresholds and rates)

HECS-HELP is an income-contingent government loan that covers your university fees. You do not make regular loan repayments. Instead, the ATO deducts a mandatory amount from your salary once your income crosses a threshold. The higher your income, the higher the deduction rate.

From 1 July 2025, the system changed from a flat rate on your total income to a marginal model. You now pay only on income above the $67,000 floor:

| Repayment income | Annual repayment |

|---|---|

| $0 to $67,000 | Nil |

| $67,001 to $125,000 | 15% of income above $67,000 |

| $125,001 to $179,285 | $8,700 plus 17% above $125,000 |

| $179,286 and over | 10% of total income |

Source: ATO Study and Training Support Loans repayment thresholds, 2025-26 income year.

Before 1 July 2025, a borrower earning $80,000 paid approximately $2,800 per year under the old flat-rate system. Under the current rules, they pay 15% x ($80,000 – $67,000) = $1,950 per year. That $850 annual saving translates to roughly $8,500 more borrowing power.

Why your income matters more than your balance

Unlike a personal loan or credit card, your HECS repayment is not based on your outstanding balance. It is based on your income. Two borrowers with identical $40,000 HECS balances but different incomes face very different serviceability impacts.

A borrower earning $70,000 repays $450 per year. A borrower earning $120,000 repays 15% x ($120,000 – $67,000) = $7,950 per year. Lenders see these as materially different ongoing commitments. The higher earner faces the larger borrowing power reduction, even with the same debt balance.

How HECS reduces your borrowing power

Net disposable income and the serviceability test

Lenders assess home loan applications by calculating your net disposable income (NDI) – the income left after tax, living expenses, and committed debt repayments. Every dollar of annual HECS repayment reduces your NDI, which reduces the loan amount the lender will approve. How banks assess your borrowing capacity covers the full mechanics if you want the detail.

How living expenses affect borrowing capacity also matters here. HECS stacks on top of other committed expenses. Borrowers with high declared expenses and large HECS repayments face a compounded reduction in available NDI.

Lenders also apply a 3% serviceability buffer above the loan’s current interest rate. This stress tests repayments at a higher rate and further tightens what they will approve. The buffer applies to the total loan, not just the HECS portion, but it amplifies the impact of a reduced maximum loan amount.

The rule of thumb: roughly 10 times your annual HECS repayment

The rule of thumb brokers use for HECS borrowing power impact is roughly 10 times your annual compulsory repayment. This is a guide, not a guarantee – the actual figure varies by lender and income level – but it gives you a workable planning number.

At current 2025-26 repayment rates:

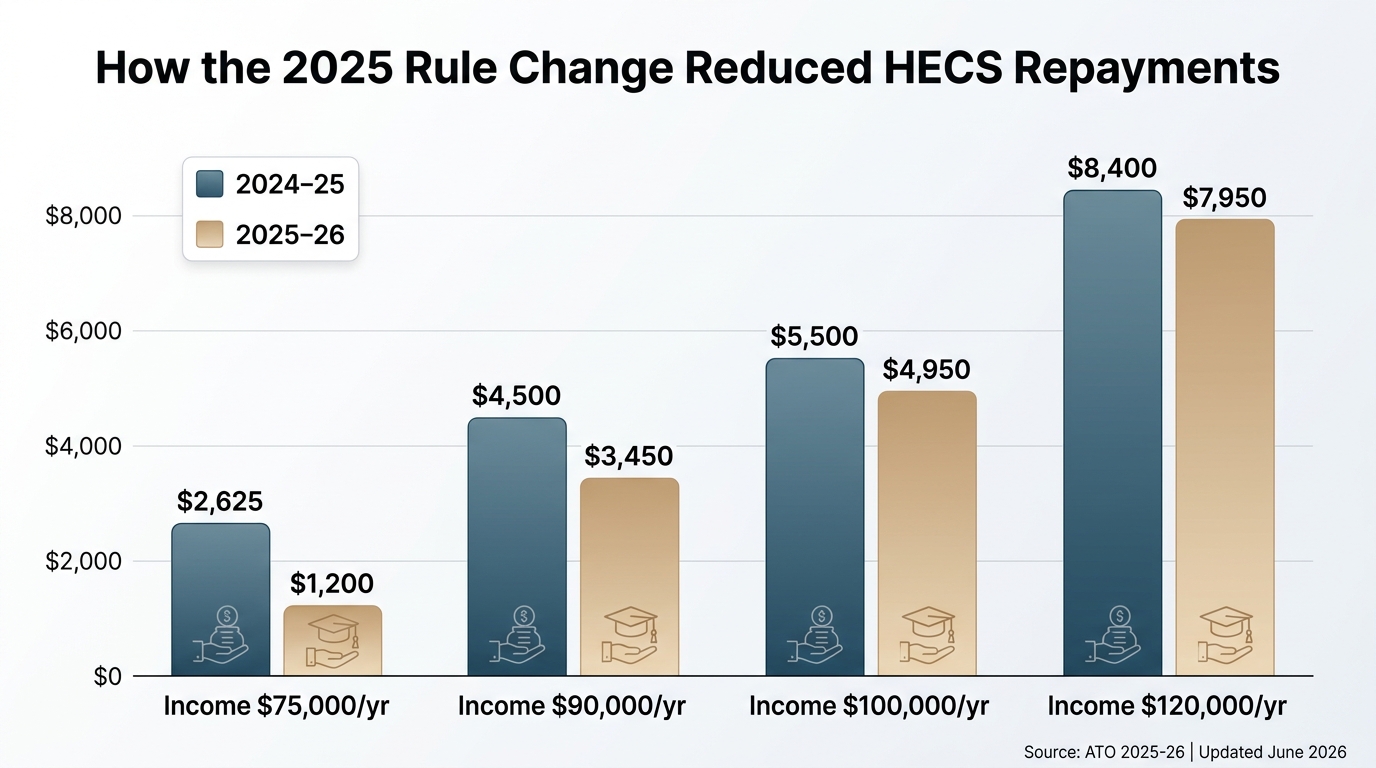

- Borrower earning $75,000: annual repayment = 15% x $8,000 = $1,200. Borrowing power reduction: approximately $12,000.

- Borrower earning $90,000: annual repayment = 15% x $23,000 = $3,450. Borrowing power reduction: approximately $34,500.

- Borrower earning $120,000: annual repayment = 15% x $53,000 = $7,950. Borrowing power reduction: approximately $79,500.

Under the old 2024-25 flat-rate system, the $90,000 borrower would have paid approximately $4,500 per year – around $45,000 in reduced borrowing power. The 2025 rule change alone restored roughly $10,500 in borrowing capacity at that income level.

Use our borrowing power calculator to estimate your specific position.

Worked example: $40,000 HECS, two different lender outcomes

Consider a borrower: 31 years old, $95,000 gross income, $40,000 HECS balance, no other debt.

Annual HECS repayment (2025-26): 15% x ($95,000 – $67,000) = $4,200/year

Using the 10x rule, this reduces borrowing power by approximately $42,000 at a lender applying the standard assessment. A lender that has not adopted any carve-out will include that $4,200 in the serviceability calculation.

With $40,000 outstanding and a $4,200 annual repayment, full payoff is roughly 9-10 years away (not accounting for indexation). That is well outside the CBA 12-month carve-out window. NAB’s $20,000 balance threshold also does not apply here.

Now take the same borrower with $15,000 HECS instead. At NAB, the balance falls under $20,000. NAB excludes the HECS repayment from its serviceability calculation entirely, subject to ATO documentation. That restores approximately $42,000 in borrowing capacity compared to a lender still applying the full haircut. The difference between a $15,000 and $40,000 HECS balance, at the same income, can be $40,000+ in approved loan size – just from lender policy.

The 2025-26 HECS changes every borrower should know

Three changes took effect between July and October 2025 – and most of what you’ll find online still describes them as upcoming. They’re not. They’re current law, and they change the maths.

APRA’s new DTI rule: HECS excluded from your debt-to-income ratio

From 30 September 2025, APRA’s updated reporting standard (ARS 223.0) requires all banks to exclude HELP debt from the debt-to-income (DTI) ratio they report to the regulator. This applies to every HECS borrower – no minimum balance, no threshold. Your HECS balance no longer inflates the DTI figure APRA uses to supervise bank lending.

This is a reporting change, not a serviceability change. It means APRA’s systemic risk metrics no longer treat HECS as high-risk debt. It does not by itself change how your repayments are counted in your individual serviceability assessment – that is addressed separately by the carve-out below.

The serviceability carve-out for near-payoff borrowers

Separately, APRA updated its serviceability guidance (APG 223) to allow banks, by exception, to exclude HECS repayments from their internal serviceability calculations for borrowers expected to repay in the near term. APRA’s guidance anchors on 12 months as the standard it considers “not unreasonable.” This is optional – each bank decides whether to adopt it.

CBA and NAB have confirmed policies. CBA excludes HECS from serviceability for borrowers within 12 months of full repayment. NAB excludes it where the balance is $20,000 or less, subject to verified ATO documentation (effective 31 July 2025).

For qualifying borrowers, the benefit is real and immediate. If your $4,200 annual repayment is excluded, the lender treats it as $0 in the serviceability calculation, restoring the full ~$42,000 in borrowing power.

The 20% HECS reduction (applied July 2025)

In July 2025, the Australian Parliament passed the Universities Accord (Cutting Student Debt by 20%) Act 2025. The 20% reduction was applied retroactively to all HECS-HELP debt balances as at 1 June 2025, before that year’s indexation was calculated. The ATO completed processing for most borrowers before the end of 2025.

Over 3 million Australians had their balance cut by 20% as a result. A $50,000 debt became $40,000. That year’s indexation of 3.2% then applied to the reduced balance, compounding the benefit. For borrowers close to a lender’s carve-out threshold, the reduction may have brought them under the cutoff.

The indexation environment has improved

HECS indexation is applied on 1 June each year. Recent rates:

| Year | Indexation rate |

|---|---|

| 2023 | 3.2% (reduced from original 7.1%) |

| 2024 | 4.0% (reduced from original 4.7%) |

| 2025 | 3.2% |

| 2026 | 2.8% |

Source: ATO Study and Training Support Loans indexation rates.

Since the 2024 budget, indexation is capped at the lower of CPI or the Wage Price Index. The 2023 spike to 7.1% prompted the reform. With 2026 indexation at 2.8%, the urgency around timing applications to avoid June indexation is much lower than it was in 2022-23.

Which lenders apply the HECS serviceability carve-out

Lender policies differ. Below is what can be confirmed from public sources:

| Lender | Carve-out? | Trigger |

|---|---|---|

| CBA | Yes | Borrower within 12 months of full repayment |

| NAB | Yes | Balance $20,000 or less, ATO documentation required (from 31 July 2025) |

| ANZ | Not publicly confirmed | – |

| Westpac | Not publicly confirmed | – |

APRA’s guidance is optional. Other lenders may have adopted different policies. These policies are not always published on lender websites. A broker who tracks credit policy across 52+ lenders will know which banks have adopted the carve-out and at what threshold – which can save you weeks of back-and-forth with individual banks.

Should you pay off your HECS before buying a house?

When paying it off makes sense

There are three situations where clearing HECS first is the right call:

- Your balance is just above a lender’s carve-out threshold. A targeted lump-sum payment to get under $20,000 (for NAB) can unlock more borrowing power than the amount spent.

- Your income is high enough that your annual repayment is large – a $120,000 earner repays $7,950/year, equivalent to roughly $79,500 in reduced borrowing capacity.

- You have already saved your full deposit and have surplus cash that is not contributing to avoiding LMI. Using it to clear HECS is productive in that case.

When to keep the cash for your deposit

For most first home buyers, keeping cash for the deposit beats paying off HECS.

A 20% deposit on a $750,000 property is $150,000. If you are short by $20,000, paying that amount toward HECS does not solve the deposit gap – it creates a new one. The cost of a smaller deposit (LMI, higher LVR pricing) typically exceeds the borrowing power benefit of eliminating the HECS repayment. Work out how much deposit you need before making this call.

The arithmetic favours paying HECS only when you have surplus savings above your deposit target, not when the choice is one or the other.

How to maximise your borrowing power with a HECS debt

A few practical steps before you apply:

Declare your HECS accurately on the application. Lenders verify it through payslips, so any discrepancy creates problems in the assessment – there is no upside to underreporting.

Get your ATO balance statement before applying. For NAB’s carve-out, this documentation is a hard requirement, not optional. Request it early so it does not delay your application.

If your balance is just above a carve-out threshold, consider a voluntary repayment. Paying down from $22,000 to $19,500 to qualify for NAB’s $20,000 limit costs $2,500 and can restore $40,000+ in borrowing capacity. That is a strong return on $2,500.

Apply with multiple lenders in mind. APRA guidance is optional, which means Lender A may include your $4,200 HECS repayment in full while Lender B excludes it entirely. A broker covering 52+ lenders can tell you which bank gives you the best outcome for your specific numbers.

For additional levers beyond HECS, see ways to increase your borrowing capacity.

How a mortgage broker helps when you have a HECS debt

HECS policy differs by lender, and most lenders do not publish their approach clearly. A NAB application with an $18,000 HECS balance can produce a substantially larger maximum loan than the same application at a lender that has not adopted the APRA carve-out. The gap can be $40,000 or more on the same income and deposit.

At Mortgage World Australia, we work across 52+ lenders and know which banks apply the carve-out, at what thresholds, and what documentation they require. Before you apply, we can model both paths – full HECS included versus carve-out eligible – so you know exactly where to lodge.

We also run the numbers on voluntary repayments. Paying down $3,000 to cross a lender’s threshold is only worth it if the maths stacks up for your situation. Sometimes it does. Sometimes keeping the cash makes more sense.

If you have HECS and are planning to buy, get in touch before you apply. The difference between lenders is real, and for first home buyers where the deposit is already stretched, choosing the right bank for your HECS balance can be the difference between approved and not.

FAQ: HECS debt and home loans

Can I buy a house if I have HECS debt?

Yes. Having a HECS-HELP debt does not prevent you from getting a home loan. Lenders assess HECS as part of your overall financial picture, but it is not a disqualifying factor. What it does is reduce your maximum borrowing power by treating your annual repayment as a committed expense in the serviceability test. The size of that reduction depends on your income and your outstanding balance.

Should I pay off HECS before buying a house?

It depends on your balance and how close you are to your deposit target. If paying off HECS would reduce your deposit below 20% of the purchase price, in most cases the better move is to keep the cash and accept the reduced borrowing power. If you have surplus savings above your deposit target, a strategic repayment to get under a lender’s carve-out threshold – such as NAB’s $20,000 limit – can unlock considerably more borrowing capacity than the cash spent. A mortgage broker can model both options for your specific numbers.

Does HECS debt affect my credit score?

No. HECS-HELP debt does not appear on Australian credit reports (Equifax, Illion, Experian). The ATO is not a credit provider under the Privacy Act, so your balance is not included in your credit file. However, lenders will ask you to declare your HECS on the loan application form, and they verify it through your payslips, which show the HECS repayment withholding as a separate line item alongside income tax.

How much HECS do I pay on $70,000?

Under the current 2025-26 rules, a borrower earning $70,000 pays: 15% x ($70,000 – $67,000) = $450 per year. Under the old 2024-25 flat-rate system, the same income attracted approximately $1,750 per year (2.5% of $70,000). The shift to a marginal model cut the repayment burden considerably for borrowers in the $67,000 to $90,000 income range.

This article contains general information only and does not constitute financial advice. Your personal financial situation, objectives and needs have not been considered. Before acting on any information, you should consider its appropriateness to your circumstances. Speak to a qualified mortgage broker for advice tailored to your situation. Mortgage World Australia Pty Ltd is a credit representative (CR No. 396946) of Mortgage Specialists Pty Ltd (Australian Credit Licence No. 387025).

By Patrick O’Brien, Director and Home Loan Specialist since 2001.

Patrick is a Director and a Home Loan Specialist. He has been helping Australians with home loans since 2001. Prior to working as a mortgage broker Patrick was employed by Macquarie Bank for 3 years and also worked as an accountant for a publicly listed company. Patrick’s qualifications include:

Bachelor of Business, UTS Sydney. Majored in accounting and sub-majored in Finance and Marketing.

Diploma of Finance and Mortgage Broking Management FNS50310

Certificate IV in Financial Services (Finance/Mortgage Broking) FNS40804

Ready to Take the Next Step?

Whether you’re looking to buy your first home, refinance, or explore investment opportunities, Mortgage World Australia is here to help.

Fill out the contact form below, and one of our expert mortgage brokers will be in touch shortly to discuss your needs and guide you through your options.

Get Started Today!