Debt Recycling Australia: How It Works & Whether It’s Right for You

Debt recycling gets misunderstood because most people explain it backwards. They start with the tax benefit and build down to the mechanics. In practice, the loan structure is everything — get that wrong and the tax benefit doesn’t matter. This article covers what actually happens when you set it up, not just the theory.

The concept is straightforward. The execution requires a specific loan structure that most standard mortgages don’t support out of the box.

What is debt recycling?

On this page ▾

Debt recycling converts non-deductible home loan debt into tax-deductible investment debt. Your home loan interest comes from after-tax income — no deduction, no offset. The strategy replaces portions of that mortgage with borrowing the ATO recognises as deductible, because the funds are invested in income-producing assets.

How it works: you make extra repayments on your home loan, redraw those funds into a separate investment loan, invest in shares or ETFs, then use the investment income to accelerate home loan repayments. Over time, your non-deductible debt shrinks and your deductible investment debt grows.

Debt recycling vs negative gearing: these are different strategies

People conflate these two. Negative gearing means borrowing to invest where the interest cost exceeds the investment income — you run at a deliberate loss and offset that loss against your salary. Debt recycling doesn’t require a loss. You’re restructuring existing debt, not creating new net borrowing. The tax benefit comes from converting non-deductible interest into deductible interest.

They can coexist in the same loan structure — a negatively geared investment inside a debt recycling framework — but they’re separate strategies with different mechanics.

Is debt recycling legal?

Yes. The ATO permits interest deductions on borrowings used to earn assessable income under section 8-1 of the Income Tax Assessment Act 1997. The structure has to be set up correctly: the investment loan must be separate from the home loan, and the borrowed funds must go directly to income-producing assets. There’s no ATO ruling against the strategy. The risk is always poor loan structuring, not the concept itself.

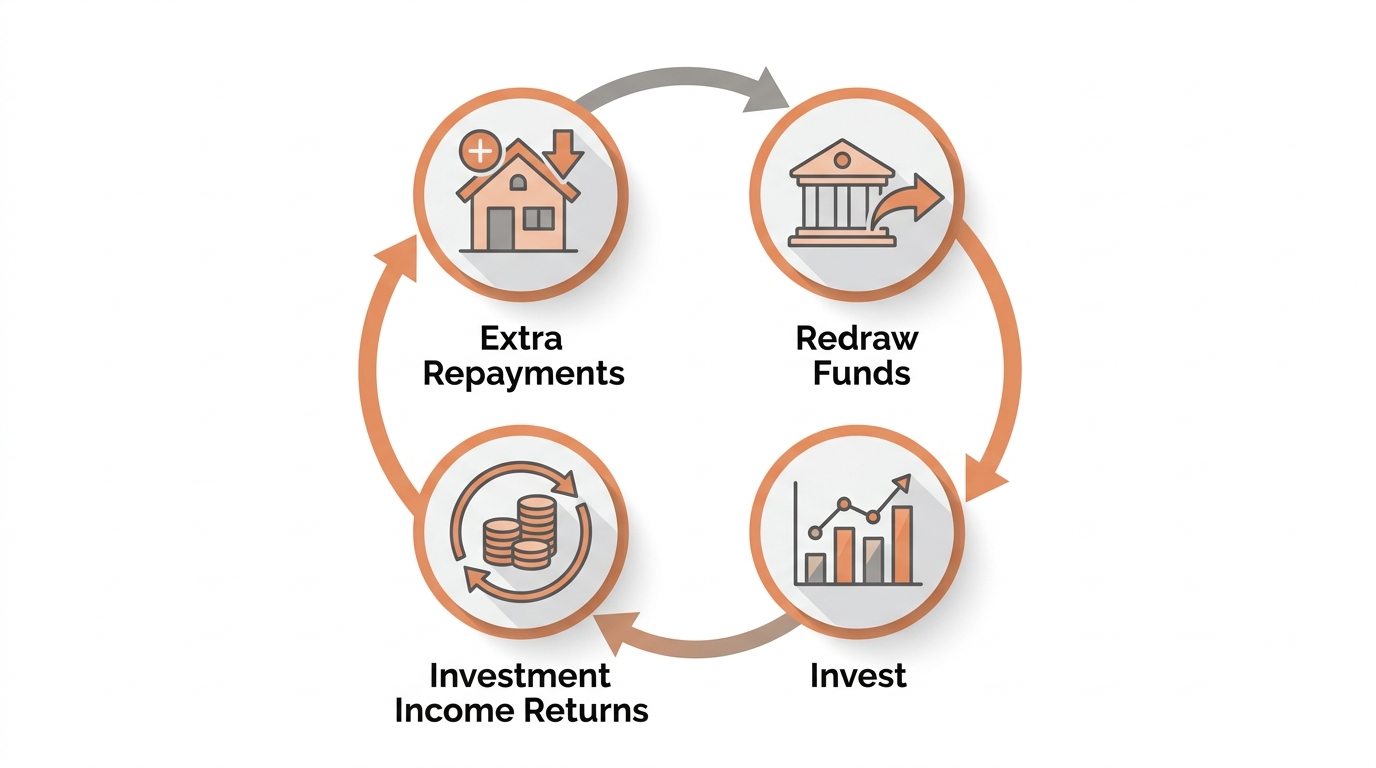

How debt recycling actually works

The cycle works like this:

- Make extra repayments on your home loan to build equity.

- Redraw those funds as a separate, clearly identified investment loan.

- Invest the borrowed funds in income-producing assets — typically shares, ETFs, or managed funds with distributions.

- Direct the investment income back to your home loan and repeat.

Each cycle converts more home loan debt into deductible investment debt. As the portfolio grows, the tax benefit grows with it.

Step 1: Extra repayments above your minimum

This is the engine. How much surplus cash you have above your minimum repayment determines the pace. Some borrowers use employment income. Others wait until the portfolio generates dividends large enough to reinvest. Your home loan needs to allow extra repayments — a variable rate with redraw access is standard.

Step 2: Redraw as a separate investment loan

This is where most people stumble. The funds you redraw must stay completely separate from your home loan. The ATO requires a clear, traceable connection between the borrowed funds and the income-producing investment. If funds get mixed — even briefly — you risk losing deductibility.

The practical solution is a split loan: your home loan and investment loan sit as separate splits under the same facility, with separate account numbers and interest calculations. This creates an auditable paper trail from day one.

Confirm this structure with your accountant before you use it.

Step 3: Invest in income-producing assets

Australian shares, ETFs, listed investment companies, and managed funds with regular distributions are the standard vehicles. Investment property works too, but the mechanics are more involved. The ATO requirement is clear: the asset must generate assessable income. Capital growth alone doesn’t count. You cannot debt recycle into speculative assets or cash.

Step 4: Redirect investment income and repeat

Dividends and distributions go back to your home loan, which builds more equity to redraw and reinvest. The cycle compounds as the portfolio grows.

A real-world debt recycling example

Someone earning $120,000 per year sits at a 30% marginal tax rate (plus 2% Medicare levy = 32% combined, based on 2025–26 ATO rates).

Starting point: $500,000 home loan at 6.2% variable, principal and interest.

Over 18 months, they make extra repayments of $2,000 per month above the minimum — $36,000 total. The home loan drops to $464,000. They then redraw $36,000 as a separate investment loan at 6.5% interest-only, and invest in an ASX 200 ETF yielding 3.5%.

What happens on the investment split annually:

| Amount | |

|---|---|

| Interest on the $36,000 investment loan @ 6.5% | $2,340/year |

| Tax deduction at 30% marginal rate | −$702/year |

| After-tax interest cost | $1,638/year (~$137/month) |

| ETF dividends received @ 3.5% | $1,260/year (~$105/month) |

| Net cost to the borrower | ~$32/month |

That $32 a month doesn’t look like much. But the dividends go back to the home loan, which builds more equity to redraw. As the portfolio grows to $100,000, $150,000, the tax deduction scales with it.

At a 45% marginal rate (income above $190,000), the same $2,340 in interest saves $1,053 per year. That is where the strategy becomes genuinely compelling.

Tax rates based on ATO 2025–26 financial year rates. ETF yield is illustrative at 3.5%, consistent with current ASX 200 ETF distributions — actual yields vary. Check current rates at ato.gov.au before making financial decisions.

The tax benefit — why it scales with income

The core benefit is converting non-deductible interest into deductible interest. Your home loan interest comes from after-tax money with no offset. The investment loan interest reduces your taxable income dollar for dollar each year.

The effective benefit depends entirely on your marginal tax rate. At 30%, every $1,000 of investment loan interest costs $700 after the deduction. At 45%, it costs $550. The strategy works at lower income levels, but the numbers become substantially more compelling above $120,000.

ATO rules on interest deductibility

The ATO requires three things for interest deductibility under section 8-1 ITAA 1997:

- The borrowed funds must be invested in income-producing assets.

- The funds cannot be mixed with personal or non-investment use.

- The investment loan must be clearly identifiable as separate from the home loan.

The nexus between the borrowed funds and the investment purpose must be established at the time of borrowing. Retroactively claiming personal funds were used for investment doesn’t work.

The structural mistake that kills deductibility

Loan contamination is the most common reason this strategy fails. You redraw from your home loan, the funds pass through the same account, get used for something else — or just sit there too long — and you can no longer cleanly defend the deductibility. The ATO will challenge the nexus between the loan and the investment.

The fix: a clean split loan structure with each split carrying a dedicated purpose and a separate account number. Redrawn funds go directly to a brokerage or managed fund account. No passing through personal accounts, if possible. No detours.

What loan structure do you need?

Not every home loan supports debt recycling. You need one that allows redraws and ideally supports a split facility.

Split loans vs redraw facilities

A split loan divides your mortgage into separate accounts. Split 1 for the home (non-deductible). Split 2 for the investment (deductible). Interest is calculated independently for each, and the purpose is unmistakable to the ATO.

A standard redraw facility can work, but carries contamination risk if the same account handles both personal and investment transactions. Some lenders structure redraws to go directly to a separate investment account, which reduces the risk — but confirm the mechanics with your lender and accountant first.

For a detailed comparison of how redraw and offset facilities work in practice, see our redraw vs offset account guide.

Which lenders actually support this

Most major banks and many non-bank lenders support split structures in principle. The practical details vary: maximum splits allowed (some cap at two), fees per split, whether you can have an offset account on the investment split, and whether redraws can be directed to a separate account.

This is where a broker adds genuine value. With access to 52+ lenders, we can identify which loan products actually support a debt recycling structure without administrative friction — and which will create contamination risk or cap your growth.

Who should actually consider this

When it works

Debt recycling makes sense if you have:

- A home loan with a meaningful balance remaining — generally $300,000 or more

- Surplus cash flow above minimum repayments. Genuine surplus, not aspirational. Typically $1,000–$2,000 per month, sustained over years.

- A marginal tax rate of 30% or above

- A 10+ year investment horizon

- Real comfort with investment volatility, knowing the investment loan is secured against your home

When it doesn’t

This strategy is unsuitable if you have:

- Cash flow that fluctuates or is consistently tight

- Retirement within 5–10 years — you can’t absorb a significant market correction

- A fixed rate loan that restricts extra repayments

- No clear income-producing investment in mind

The real risks

Leverage and market falls

You’re borrowing to invest. If the investment falls 30%, the loan balance doesn’t fall with it. A $100,000 ETF portfolio drops to $70,000, but you still owe $100,000. The interest obligation keeps running regardless of performance.

This is manageable for investors with genuine 10+ year horizons and the stomach for drawdowns. It’s a different experience for people who think they’re comfortable with volatility until a 25% correction hits the portfolio.

Cash flow sustainability

Early in the strategy, when the portfolio is small relative to the interest cost, you’re funding part of the gap from your own pocket. Run the numbers first — the ~$32 monthly net cost in the example above needs to be genuinely sustainable at your actual income and expense levels, not just on paper.

The behavioural risk no one talks about

Debt recycling requires consistent execution over many years: extra repayments, regular redraws, reinvestment, and disciplined redirection of income back to the home loan. For 10+ years.

The investors who succeed are the ones who set it up correctly, automate what they can, and leave it alone through market cycles. The ones who struggle are those who stop halfway through. Markets fall, cash flow tightens, and the cycle pauses. Restarting it properly is harder than continuing.

Discuss this with a financial adviser before you commit. If you don’t have a genuine conviction to stay the course over the full investment period, the strategy will underperform what the numbers suggest.

How a mortgage broker fits in

The investment logic is straightforward. Getting the loan structure right is not. The split setup — lender selection, correct structuring, clean ATO paper trail from day one — is where this strategy either works or fails.

A broker’s job is to identify lenders whose products genuinely support the structure you need, review your current loan to determine whether it can be restructured without a full refinance, and set up the splits correctly from the outset. Not all lenders offer suitable products, and some that do in principle have practical limits — capped splits, no offset on investment accounts, redraw restrictions — that make the strategy impractical to execute properly.

The loan setup happens before any conversation with a financial adviser about which investments to hold. At Mortgage World Australia, we work across 52+ lenders and can identify which product actually suits your situation.

Speak to a mortgage broker at Mortgage World Australia to review your loan options.

Frequently asked questions

Is debt recycling actually worth it?

For the right person, absolutely. If you have genuine surplus cash flow, a home loan with a meaningful balance, a 30%+ marginal tax rate, and a long investment horizon, the compounding effect over 10+ years is substantial. If you’re cash-flow tight, close to retirement, or uncomfortable with leverage and investment volatility, the case is much weaker. It’s not a universal strategy — but for those it suits, it’s one of the most tax-efficient wealth-building approaches available to Australian homeowners.

Do I need both a financial planner and a mortgage broker?

Yes, this is recommended. A mortgage broker structures the loan correctly — the split, lender selection, redraw mechanics, and the paper trail the ATO requires. A financial adviser determines which investments to hold, manages the portfolio, and integrates the strategy into your broader financial plan. These are separate functions. Most people who execute this successfully over the long term work with both.

Can you debt recycle with an investment property?

Yes, though the mechanics are more complex. The investment property loan needs to be a separate facility from your home loan, and the rental income needs to flow back to the home loan to complete the cycle. Property also introduces stamp duty, transaction costs, and liquidity constraints that shares or ETFs avoid. The fundamentals are the same; the execution is more involved and requires closer coordination between your broker, accountant, and financial adviser.

Does debt recycling speed up your home loan repayment?

The strategy reduces the non-deductible portion of your debt over time, but your total debt level may not change significantly in the short term. What changes is the character of the debt: less non-deductible home loan, more tax-deductible investment loan. Your home loan balance reduces as you make extra repayments; your investment loan grows as you redraw and reinvest. Net borrowing stays similar, but the after-tax cost of that borrowing decreases. Over a long timeframe, if the investment portfolio grows sufficiently, it can eventually retire the remaining home loan balance entirely.

Patrick O’Brien is a Director and Home Loan Specialist at Mortgage World Australia, with 25+ years’ experience structuring investment loans across a range of lenders.

General information only — not financial or tax advice. Speak with a qualified financial adviser and your accountant before implementing a debt recycling strategy. Individual circumstances vary.

Patrick is a Director and a Home Loan Specialist. He has been helping Australians with home loans since 2001. Prior to working as a mortgage broker Patrick was employed by Macquarie Bank for 3 years and also worked as an accountant for a publicly listed company. Patrick’s qualifications include:

Bachelor of Business, UTS Sydney. Majored in accounting and sub-majored in Finance and Marketing.

Diploma of Finance and Mortgage Broking Management FNS50310

Certificate IV in Financial Services (Finance/Mortgage Broking) FNS40804

Ready to Take the Next Step?

Whether you’re looking to buy your first home, refinance, or explore investment opportunities, Mortgage World Australia is here to help.

Fill out the contact form below, and one of our expert mortgage brokers will be in touch shortly to discuss your needs and guide you through your options.

Get Started Today!