Redraw vs Offset: Which One Is Right for You?

Most home loan borrowers are offered a choice at some point: a redraw facility or an offset account. Both reduce the interest on your loan. Both let you access your savings when you need them. They work differently, carry different costs, and have tax implications that matter significantly if you plan to invest — and that last point is the real divider.

We see people structure this wrong regularly. Twenty-five years, 52+ lenders, and it still catches people off guard. This guide explains exactly how each feature works, what separates them, and how to decide which suits your situation.

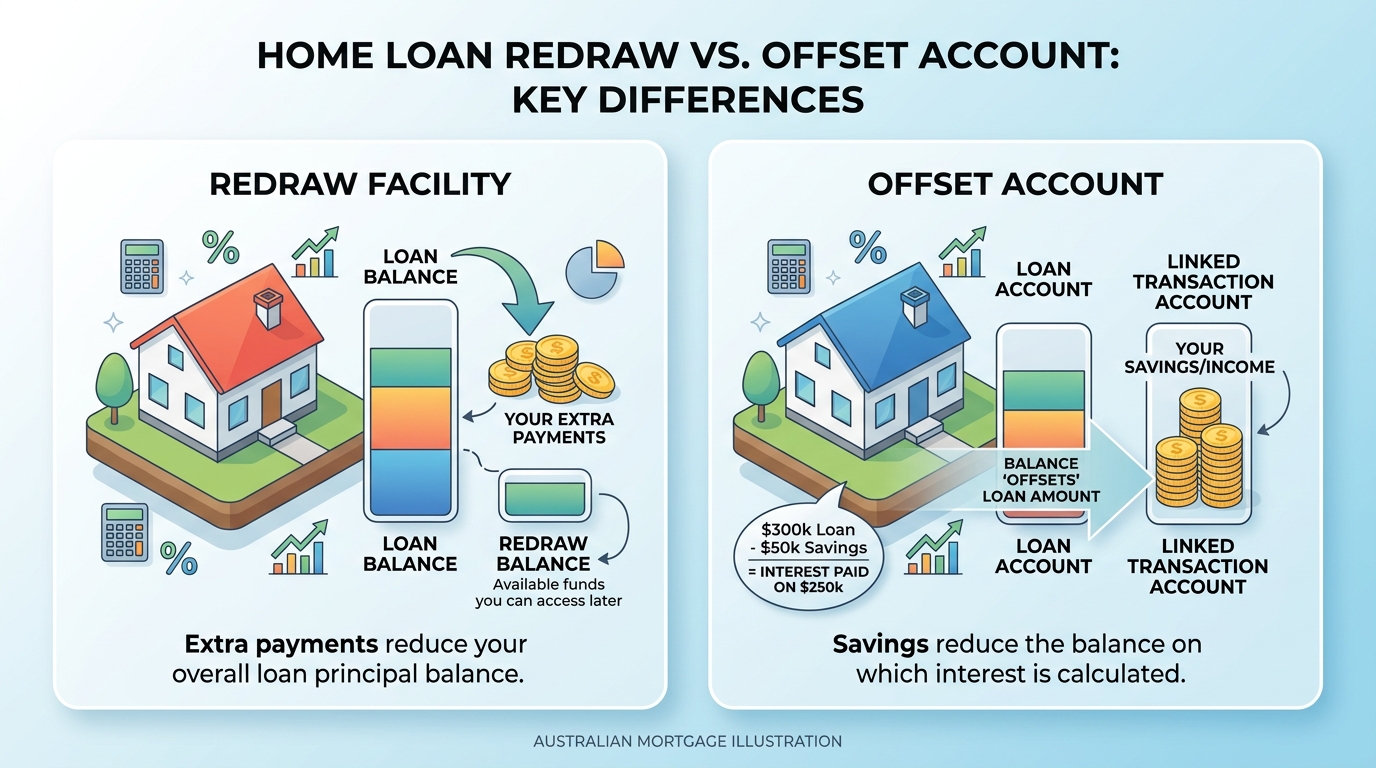

What is a redraw facility?

A redraw facility lets you make extra repayments on your home loan — above your minimum required repayment — and then access those funds later if you need them.

When you pay more than your minimum each month, those extra payments reduce your outstanding loan balance. You’re paying down the principal faster. If circumstances change and you need the money, you can “redraw” it — requesting those extra funds back from the lender.

How does redraw reduce your interest?

Home loan interest is calculated daily on your outstanding balance. Every extra dollar paid against the principal reduces that balance, which means less interest accrues each day.

A straightforward example: a $500,000 loan at 6.0% per annum costs around $82 in interest per day. If you’ve made $30,000 in extra repayments, you’re now paying interest on $470,000 — saving approximately $4.93 per day, or around $1,800 per year. Over a decade of extra repayments, that adds up to $18,000+ in interest saved. That’s how it compounds.

What are the limitations of a redraw facility?

Redraw sounds simple: put extra money in, pull it back when needed. But there are limitations worth understanding before you rely on it:

- Lender discretion over access: Most lenders retain the right to restrict or suspend redraw access. This is standard in the terms of most variable-rate loans. During financial difficulty — either yours or the lender’s — access may be reduced or stopped.

- No debit card or direct access: Redraw isn’t a transaction account — you can’t spend directly from it. Funds need to be transferred to a separate account, usually within 1–3 business days.

- Minimum redraw amounts: Many lenders set a floor — often $500 per transaction, sometimes higher.

- Not available on fixed-rate loans: Most fixed-rate loans cap or block extra repayments entirely during the fixed term. Redraw during that period is usually unavailable.

- Tax consequences for investors: This is the most important limitation. We cover it in full below.

What is an offset account?

An offset account is a separate transaction account linked directly to your home loan. The balance held in the account is “offset” against your loan balance before interest is calculated each day.

Unlike redraw, your money stays in a bank account — your account. You can access it via debit card, internet banking, or BPAY. There is no application process, no transfer delay, no lender approval required.

How does an offset account work?

The arithmetic is straightforward. If your loan balance is $500,000 and you have $50,000 sitting in your offset account, you pay interest on $450,000. The lender charges interest as though you owe $50,000 less, even though your actual loan balance remains at $500,000.

That $50,000 in your offset is effectively earning a return equal to your loan’s interest rate — in this case, 6.0% — without the interest being counted as taxable income. That’s typically better than a savings account, where the interest you earn is taxable.

The $50,000 remains yours. You can spend it tomorrow if you need to.

Full offset vs partial offset: what’s the difference?

A full offset account reduces your loan balance dollar-for-dollar. Every dollar in the account directly reduces the principal on which interest is charged.

A partial offset account only offsets a percentage of your savings balance — sometimes 40%, sometimes less. These are far less effective and are now uncommon in competitive home loan products.

When comparing loans, confirm explicitly whether the offset is full or partial. Some basic variable loans advertise an “offset feature” that is in fact a partial offset — delivering a fraction of the interest savings the name implies.

Redraw vs offset: key differences at a glance

| Feature | Redraw Facility | Offset Account |

|---|---|---|

| How it works | Extra repayments reduce loan balance | Separate account balance reduces interest charged |

| Access to funds | Transfer required; 1–3 business days; lender restrictions apply | Instant — debit card, internet banking, BPAY |

| Interest saving | Yes — on extra repayments made | Yes — on the daily account balance |

| Tax implications for investors | Complex — redrawn funds may lose deductibility | Cleaner — loan balance stays intact for deductibility |

| Available on fixed-rate loans | Rarely, and often capped | Rarely |

| Annual fee | Usually none | Often $300–$400/yr as part of a loan package |

| Lender control over access | Yes — lender can restrict or suspend | No — it’s a bank account you control |

Is it better to have money in offset or redraw?

The honest answer: offset usually wins. Here’s why — and the one case where it doesn’t.

The interest saving is equivalent to redraw, but your money stays fully accessible without lender restrictions, and the tax position is significantly cleaner if you ever plan to rent out the property.

The main reason to choose redraw is cost. Offset accounts typically sit inside a loan package that charges $300–$400 per year. If your savings balance is modest — say, under $15,000 — the interest saving may not cover the fee. In that case, a basic variable loan with redraw and no annual fee may deliver better overall value.

At $50,000 in an offset account against a 6.0% loan, you save $3,000 per year in interest. An annual package fee of $395 still leaves you $2,605 ahead. The numbers favour offset as your balance grows.

Tax implications of redraw vs offset

This is where choosing the wrong product costs real money — and where broker advice provides something a bank simply cannot: guidance that isn’t tied to selling their own products.

Both redraw and offset reduce the interest you pay on your home loan. But home loan interest on your primary residence is not tax-deductible. That changes the moment your property becomes an investment.

Why offset is generally better for investors

When you rent out your home — or plan to convert it to an investment property — the interest on your home loan becomes potentially tax-deductible. Here’s the critical moment: your loan balance when the property becomes a rental is what the ATO lets you claim interest on.

With an offset account, your loan balance remains at its original level. If you’ve had $50,000 sitting in your offset for three years, your loan balance is still $500,000. When you convert the property to a rental, you may be able to claim interest on the full $500,000 — even though the offset has been reducing your effective interest charges throughout.

With a redraw facility, extra repayments directly reduce your outstanding balance. If you’ve made $50,000 in extra repayments and your balance sits at $450,000 when the property becomes a rental, your deductible interest base is $450,000. You’ve permanently reduced your deductibility by $50,000.

What happens when you redraw to fund an investment property?

We see the most expensive mistakes here. Someone redraws to buy an investment property and doesn’t understand how the ATO sees the transaction.

The scenario: you’ve made $80,000 in extra repayments over several years. You decide to purchase an investment property and redraw that $80,000 to use as part of the deposit. The logic seems sound — the money was reducing your loan interest, now it’s going to work in a new asset.

The problem is how the ATO views the transaction. Interest deductibility follows the purpose of the borrowing. When funds are redrawn and used for a purpose that is not income-producing — including a deposit on a new owner-occupied home — the interest on the redrawn portion is not deductible, even if the original property is now generating rent.

You’ve increased your loan balance by $80,000. You’re paying interest on it. But that interest portion is not deductible because the redrawn funds were used for personal purposes. The ATO is clear that it is the use of the funds — not the nature of the property the loan is secured against — that determines deductibility.

This is a well-documented tax trap, and one that borrowers using offset accounts tend to avoid entirely, because their savings were never part of the loan balance to begin with.

If you’re considering using redraw funds for any investment purpose, speak to a qualified accountant before proceeding. The rules are specific, your documentation matters, and getting it wrong is expensive.

What are the negatives of a redraw facility?

The main disadvantages of a redraw facility compared to an offset account are:

- Lender control over access — the bank can legally restrict your ability to redraw. This is written into most loan contracts. During periods of financial stress, you may find access limited at precisely the moment you need it.

- No instant access — funds must be transferred to a separate account, typically taking one to three business days. You cannot spend directly from redraw.

- Tax complications for investors — redrawn funds used for non-investment purposes result in a portion of the loan losing its tax deductibility. This is a permanent consequence, not a timing issue.

- Not available on fixed-rate loans — if you’re on a fixed rate, redraw is generally unavailable or capped at a very low threshold during the fixed term.

- Minimum transaction amounts — many lenders impose a floor of $500 or more per redraw transaction, limiting how you can access the funds.

Which is better: redraw or offset?

The right answer turns on your specific circumstances. Here’s a practical framework.

When a redraw facility makes sense

Redraw suits borrowers who:

- Want to keep loan costs down and avoid annual package fees

- Maintain a smaller savings buffer (typically under $15,000–$20,000) where a package fee would erode most of the interest saving

- Are disciplined with extra repayments and rarely need to access those funds

- Are confident the property will remain their primary residence

A basic variable loan with redraw and no annual fee can deliver solid value in these circumstances. The interest saving mechanism is the same — only the access terms differ.

When an offset account makes sense

An offset account suits borrowers who:

- Maintain a significant savings balance (generally $30,000 or more)

- Want unrestricted, instant access to their savings

- Have any prospect of renting out the property in the future — even loose plans

- Are investing in property and want to protect maximum loan deductibility

- Receive irregular lump sums (bonuses, tax returns, commissions) and park them temporarily to reduce interest

As the offset balance grows, the interest saving accelerates. Borrowers who pay off their home loan faster often do so by consistently directing income through their offset account.

Can you have both offset and redraw?

Yes. Many variable-rate home loans include both features simultaneously. They serve different roles:

- The redraw facility tracks additional principal repayments you’ve made

- The offset account holds everyday savings separately from the loan

Some borrowers use their offset for an emergency fund and day-to-day cash flow, while also making structured extra repayments that reduce the principal in redraw. This approach maximises the interest reduction from both directions.

The critical point: understand the tax footprint of each feature before you act. If you’re planning to convert the property or use equity for a residential investment loan, speak to your accountant about the structure before you start making extra repayments.

If your current loan doesn’t include the features you need, refinancing your home loan is often straightforward — and may also secure a better rate in the process.

Frequently Asked Questions

What happens to redraw when your loan is paid off?

When the loan’s fully paid off, redraw closes. Any funds you’d added above the minimum get credited back to you at settlement — nothing sits there once the loan is discharged.

Is a redraw facility available on fixed-rate loans?

Usually not, or only in very limited form. Fixed-rate loans typically restrict additional repayments to protect the lender’s hedging position. Most lenders cap extra repayments at $10,000 to $20,000 per year during a fixed term, and redraw access is often suspended entirely for that period. Check the specific product terms before making large extra repayments on a fixed loan — break costs can apply if you exceed the cap.

Does having an offset account cost more?

In most cases, yes. Offset accounts typically come packaged with a “professional” or “package” home loan that charges an annual fee — usually between $300 and $400 per year. This fee generally includes the offset account, a credit card, and sometimes a transaction account or other features. As a guide: at a 6.0% variable rate, you need roughly $7,000 sitting in the offset to save enough interest to cover a $400 annual fee. Above that balance, you come out ahead each year.

Can I use redraw funds to buy an investment property?

The tax position depends on how the funds are used. If redrawn funds go directly toward an income-producing investment — for example, as a deposit on an investment property — the interest on that redrawn amount may be deductible, because the purpose of the borrowing is investment. However, if the funds are used for a mixed purpose, or for personal use (such as a deposit on a new owner-occupied home), the deductibility of that portion is likely lost. This is not a simple calculation — always confirm your position with a registered tax agent before proceeding.

Choosing the right loan structure

Redraw vs offset is one of those decisions that looks minor on paper but has real consequences — both in day-to-day convenience and in long-term tax outcomes. At Mortgage World Australia, we help borrowers structure their home loans to match their actual goals, with access to 52+ lenders and options across the full spectrum from basic variable loans to full package products with offset.

Call us. We’ll model both options for your situation and show you the actual cost difference. That’s what 25 years of doing this looks like — we can usually give you a clear answer in a single conversation.

General information only — not personal advice. Tax rules change and your situation is unique. Always speak to a qualified accountant before you restructure, especially if investment property is part of the plan.

Patrick O’Brien, Director and Home Loan Specialist, Mortgage World Australia. In the industry since 2001.