Loan Repayment Calculator

Before you commit to a home loan, it helps to know what the repayments actually look like. Use this loan repayment calculator to estimate your monthly or fortnightly home loan repayments from your loan amount, interest rate, and loan term. Whether you are buying your first home, refinancing, or modelling a new investment loan, the figure below lets you sanity-check affordability, compare loan terms, and see how a small change in rate or repayment frequency changes what you really pay.

How to use the Loan Repayment Calculator

- Enter your loan amount. Use the amount you plan to borrow after your deposit, not the property price.

- Enter the interest rate. Use a current illustrative rate as a starting point, then confirm the real rate with a broker.

- Choose the loan term. Most home loans run 25 or 30 years. A shorter term lifts the repayment but cuts total interest.

- Add any ongoing loan fee (optional). If your loan charges an ongoing fee, enter it and how often it applies. Leave this blank for a quick repayment estimate.

- Select the repayment frequency. Monthly, fortnightly, or weekly. Paying more often can shave time off the loan.

- Review the result. The calculator returns your repayment and the total interest you would pay over the life of the loan.

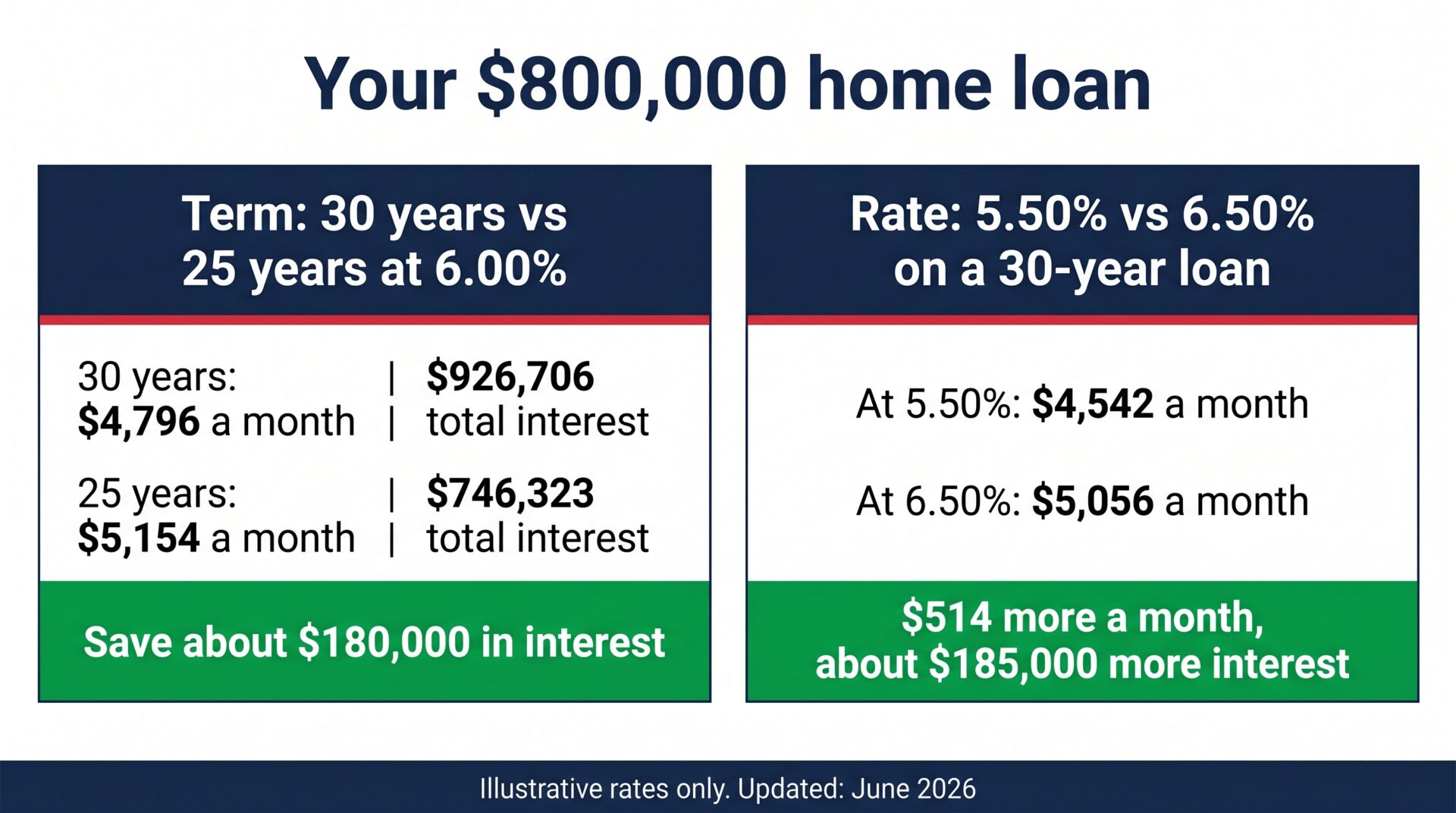

Worked example: an $800,000 Sydney home loan

Take a typical Sydney purchase financed with an $800,000 loan. Here is how two of the inputs change the picture.

The loan term: 30 years vs 25 years (same rate)

At 6.00% over 30 years, the repayment is about $4,796 a month, and you pay roughly $926,706 in interest across the life of the loan. Shorten the term to 25 years and the repayment rises to about $5,154 a month, an extra $358. But the total interest drops to around $746,323. That is roughly $180,000 less interest for paying about $358 more each month. The trade-off is cash-flow headroom now against interest saved later.

The interest rate: a 1% swing

Keep the same $800,000 loan over 30 years and move the rate. At 5.50% the repayment is about $4,542 a month; at 6.50% it is about $5,056. That is roughly $514 a month between them, and about $185,000 over the life of the loan. A 1% difference in rate is real money, which is exactly why the lender and rate you actually qualify for matter more than the calculator’s default figure.

Interest rates shown are illustrative only and do not reflect any specific lender’s current offer. Confirm current rates with a broker before relying on these figures.

What this calculator can’t tell you

The calculator gives you a clean repayment figure. A real loan has a few moving parts it cannot see:

- The rate you would actually qualify for. The calculator uses whatever rate you type in. Your real rate depends on the lender, your loan-to-value ratio, loan size, security type, and credit profile. A broker prices your scenario across more than 50 lenders, not a single placeholder figure.

- Whether to fix or stay variable. The calculator assumes one rate for the whole term. A fixed rate usually reverts to a higher variable rate when the fixed period ends, which changes your repayment, and fixed loans often limit extra repayments. See should I fix my home loan for the full picture.

- What extra repayments could save you. This calculator works out your scheduled repayment, but it has no extra-repayment field, so it cannot show what paying a bit more does. The effect is large: on an $800,000 loan at 6.00%, adding about $500 a month pays it off roughly 6 years early and saves in the order of $232,000 in interest (illustrative). To model your own figure, use the Extra Repayment Calculator.

- How an offset account changes things. Money in a 100% offset reduces the interest you pay without being a scheduled repayment at all. The repayment calculator only knows the payments you enter.

- Whether a lender will approve it. A repayment you can afford on paper still has to pass the lender’s serviceability test. APRA-regulated lenders check you could still afford the loan if your rate were three points higher, so a 6.00% loan is tested at about 9.00%. Some non-bank lenders apply a smaller buffer. The calculator shows the repayment; it does not tell you who will say yes.

The calculator gives you the repayment. A broker tells you the rate you would actually get, whether to fix or stay variable, and how to structure the loan so it works for your cash flow.

Related calculators

- Home Loan Offset Calculator: see how an offset account cuts the interest you pay without locking your money away.

- Mortgage Switching Calculator: work out what you would save by refinancing to a lower rate.

- Borrowing Power Calculator: how much you can borrow before you model the repayment.

- Stamp Duty Calculator: the upfront transfer duty to budget for alongside your repayments.

FAQs

Not sure? Have additional questions? Try here

This article contains general information only and does not constitute financial advice. Your personal financial situation, objectives and needs have not been considered. Before acting on any information, you should consider its appropriateness to your circumstances. Speak to a qualified mortgage broker for advice tailored to your situation. Mortgage World Australia Pty Ltd is a credit representative (CR No. 396946) of Mortgage Specialists Pty Ltd (Australian Credit Licence No. 387025).