Australian Government 5% Deposit Scheme: 2026 NSW Guide

Australian Government 5% Deposit Scheme: 2026 NSW Guide

On this page ▾

- What is the Australian Government 5% Deposit Scheme?

- Who is eligible?

- Property price caps for NSW and Western Sydney

- How much deposit do you actually need?

- Which lenders offer the scheme?

- Stacking the scheme with other NSW first home buyer help

- 5% Deposit Scheme vs Help to Buy vs guarantor loans

- How to apply: step by step

- Common mistakes and broker tips

- Frequently asked questions

Saving a 20% deposit on a Sydney property is the biggest obstacle most first home buyers face. On a $900,000 home in Western Sydney, that is $180,000 before you factor in stamp duty, conveyancing fees and moving costs. Most people are looking at a decade of saving before they can meet that bar.

The Australian Government 5% Deposit Scheme cuts that number to $45,000 on the same property.

Under the scheme, eligible buyers can purchase a home with as little as 5% deposit. The federal government guarantees the remaining gap to 20% so lenders treat the loan as fully secured, meaning no lenders mortgage insurance to pay. You own 100% of the property from settlement. The government holds no stake in your home.

As of June 2026, more than 300,000 Australians have used the scheme since it launched in January 2020. Our first home buyer home loans page covers the broader landscape, but this guide goes deep on the 5% Deposit Scheme specifically: the NSW price caps, participating lenders, the October 2025 changes, and how to combine this scheme with other NSW grants to reduce your upfront costs further.

What is the Australian Government 5% Deposit Scheme?

The Australian Government 5% Deposit Scheme lets eligible first home buyers purchase a home with a minimum 5% deposit. A single-parent stream within the same scheme allows qualifying single parents or legal guardians to buy with 2%.

Housing Australia administers the scheme. Banks and lenders on the authorised panel offer it directly to borrowers.

How the government guarantee works (and why you skip LMI)

When you borrow more than 80% of a property’s value, lenders require Lenders Mortgage Insurance. LMI protects the lender, not you. On a $600,000 home with a 5% deposit, you would typically pay $11,000 to $18,000+ in LMI before the scheme (indicative; varies by insurer, lender, and borrower profile).

Under the 5% Deposit Scheme, Housing Australia provides your lender with a guarantee for up to 15% of the property value. This bridges the gap between your 5% deposit and the 20% threshold, so the lender treats your loan as if you have 20% equity. No LMI is required.

The guarantee is not cash. The government doesn’t contribute to your deposit or purchase price. You borrow from a participating lender in the normal way. The guarantee is a Housing Australia commitment to the lender; your parents and family have no involvement and no liability under this scheme. A government “guarantee” is not the same as a family guarantor loan.

What changed on 1 October 2025 (formerly the Home Guarantee Scheme)

On 1 October 2025, the federal government renamed and substantially expanded the scheme. Changes that took effect from that date:

- Income caps removed: there is no longer any income limit for first home buyers applying under the scheme

- Unlimited places: the previous annual cap of 10,000 places was abolished; you can apply at any time

- Expanded property price caps: the NSW Sydney cap increased to $1,500,000

- Unified scheme: the Regional First Home Buyer Guarantee and Family Home Guarantee were absorbed into the main scheme; regional buyers and single parents now access the same scheme through their relevant eligibility stream

If you have read content on a bank’s website about the “Home Guarantee Scheme,” “First Home Guarantee,” or “First Home Loan Deposit Scheme,” those are all previous names for the same program. The scheme page at firsthomebuyers.gov.au now carries the current name exclusively.

Who is eligible?

First home buyers (5% deposit)

To qualify under the first home buyers stream, you must:

- Be an Australian citizen or permanent resident, aged at least 18

- Be a first home buyer, OR have not owned property or land in Australia in the past 10 years

- Have saved a minimum 5% deposit

- Plan to live in the property as owner-occupier (investment purchases are not eligible)

- Apply for a principal and interest owner-occupier home loan from a participating lender (loan term up to 30 years, plus up to 3 years to complete a new build)

- Purchase at or below the price cap for your location

You can apply on your own or jointly with one other person, including a partner, a friend, or a family member.

One point that catches buyers out: the 10-year rule. If you owned a home previously but sold it more than 10 years ago, you may still qualify under this scheme. This is different from the NSW First Home Owner Grant, which has its own ownership history test, so check both eligibility rules separately if you are in this situation.

Single parents and legal guardians (2% deposit)

Single parents and single legal guardians of at least one dependent child can purchase with a 2% deposit. Under this stream, Housing Australia guarantees up to 18% of the property value.

This stream is not restricted to first home buyers. If you previously owned a home but do not hold any other property at the time your new home settles, you can apply. The rule is that you must not have an interest in any other property once your new home settles. Prior ownership history does not disqualify you.

No joint applications are allowed for this stream. You must apply as a single applicant. You must also be genuinely single at the time of application; separated but not divorced still qualifies if you do not have a de facto partner.

Regional buyers

Since October 2025, regional NSW buyers access the same scheme with a location-specific price cap of $800,000 for areas outside Sydney and the designated regional centres. There is no separate regional guarantee to apply for; eligibility requirements are the same and only the price cap differs.

The $1,500,000 Sydney cap also extends to Illawarra, Newcastle, and Lake Macquarie. Buyers in Wollongong, Newcastle, or Lake Macquarie apply under the same cap as Sydney metro buyers.

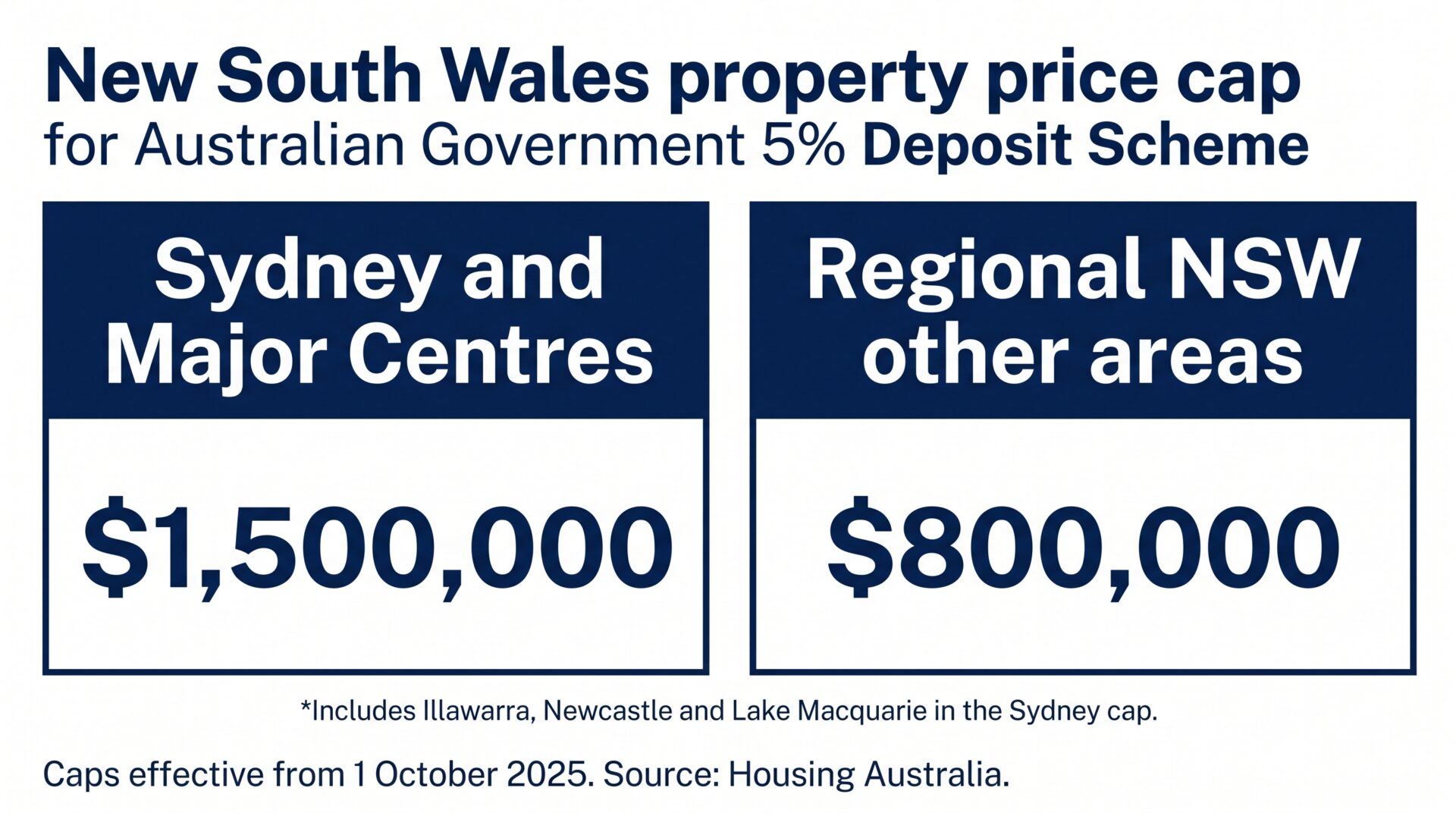

Property price caps for NSW and Western Sydney

Sydney and regional NSW caps

Both caps are effective from 1 October 2025:

| Location | Price Cap |

|---|---|

| Sydney metro | $1,500,000 |

| Illawarra (Wollongong region) | $1,500,000 |

| Newcastle and Lake Macquarie | $1,500,000 |

| Regional NSW (all other areas) | $800,000 |

For Western Sydney suburbs including Blacktown, Parramatta, Penrith, Liverpool, and Campbelltown, the $1,500,000 cap applies. Most purchases in this area sit well within that cap.

For context: Victoria’s capital city cap is $950,000 and Queensland’s is $1,000,000. NSW buyers in the Sydney metro have the highest cap in the country.

How to check your suburb

Housing Australia publishes a Postcode Search Tool at firsthomebuyers.gov.au where you enter your postcode and see the exact cap for that address. For most Western Sydney postcodes, you will land on the $1,500,000 cap, but it is worth confirming your specific postcode rather than assuming.

How much deposit do you actually need?

Worked example: 5% deposit on a $600,000 home

| Without scheme | With 5% Deposit Scheme | |

|---|---|---|

| Property price | $600,000 | $600,000 |

| Minimum deposit | $120,000 (20%) | $30,000 (5%) |

| LMI payable | $11,000 to $18,000+ (indicative) | $0 |

| NSW stamp duty (first home buyer) | $0 (full FHBAS exemption under $800,000) | $0 |

| NSW FHOG (new build, purchase under $600,000) | $10,000 grant | $10,000 grant |

A first home buyer needs $30,000 in genuine savings to purchase a $600,000 home under this scheme, rather than the $120,000 that would otherwise be required. Add a $10,000 First Home Owner Grant on a new build and zero stamp duty under the NSW FHBAS exemption threshold, and the upfront cash requirement drops sharply.

The how much deposit you need guide covers genuine savings requirements in more detail, including what lenders actually count as eligible savings.

Worked example: a $900,000 Western Sydney purchase

| Detail | |

|---|---|

| Property price | $900,000 |

| Deposit required (5%) | $45,000 |

| Scheme cap (Sydney metro) | $1,500,000 (this purchase qualifies) |

| LMI saving | $25,000 to $40,000+ (indicative; varies by lender and insurer) |

| NSW stamp duty (first home buyer) | Concessional rate applies ($800,000 to $1,000,000 range). Use the Revenue NSW calculator for the exact figure. |

| NSW FHOG | Not applicable: FHOG applies to new homes under $600,000 only |

The 5% Deposit Scheme applies cleanly to a $900,000 purchase in Western Sydney. The deposit required drops from $180,000 to $45,000. The LMI saving at 95% LVR on a loan of this size is the primary financial benefit. Stamp duty at this price point sits in the concessional band (above the $800,000 full FHBAS exemption, below $1,000,000), so some duty is payable, but less than a non-first-home-buyer would pay.

Find out how much you can borrow before you start looking at properties. Your borrowing capacity determines which price range is realistic, which in turn determines which NSW concessions you can access.

Which lenders offer the scheme?

Participating banks, mutuals and smaller lenders

As of 2026, Housing Australia has 47 lenders authorised on the panel. All four major banks participate:

- ANZ

- Commonwealth Bank

- NAB

- Westpac (including St George, Bank of Melbourne, and BankSA)

The broader panel includes Great Southern Bank, Bendigo Bank, Bank Australia, Newcastle Permanent, and more than 30 other mutual banks and credit unions.

Notable lenders not currently on the panel: ING, Macquarie Bank, HSBC, Suncorp Bank, and AMP Bank. Check the current participating lender list at firsthomebuyers.gov.au before choosing a lender, as the panel can change.

Why a lender’s overlay can change your rate

Here is something the government pages don’t cover: being eligible for the scheme is the first hurdle, not the last. Each participating lender applies its own credit policy on top of the scheme’s eligibility rules. These are called lender overlays, and they vary considerably.

The one I see trip people up most often is the genuine savings test. The scheme requires 5%, but many lenders want to see that deposit sitting in your account for at least three months. Funds received as a gift the week before application won’t count at those lenders.

Income assessment is the other common friction point, particularly for casual or contract workers. Some lenders treat casual income as regular after 12 months in the same role; others require 24 months. The same employment profile can produce different outcomes at different lenders on the same scheme panel.

If you approach one lender directly and they decline on an overlay issue, you might conclude you don’t qualify for the scheme at all. That conclusion may be wrong. A different panel lender with a more suitable credit policy for your situation may approve you on the same scheme. For example, some lenders can accept rental history as genuine savings. There is also a lender that can accept a gift in your bank account for less than three months as genuine savings.

Working with a broker across 52+ lenders means knowing which lender takes a flexible approach to your specific income type, deposit source, or employment structure before you apply, rather than after a declined application.

Stacking the scheme with other NSW first home buyer help

The 5% Deposit Scheme works alongside three other programs, and you can stack all four.

First Home Owner Grant (NSW)

NSW offers a $10,000 cash grant for buyers of new homes. To qualify, the property must be a new build (not an established home), and the purchase price must be $600,000 or less. The cap rises to $750,000 if you are buying vacant land and signing a separate building contract.

The First Home Owner Grant in NSW can be applied at settlement, reducing the cash you need on the day. On a new home under $600,000, stacking it with the 5% Deposit Scheme and the stamp duty exemption cuts the upfront cash requirement sharply. If you are buying outside NSW, see our guide to the first home owners grant by state.

First Home Buyers Assistance Scheme (stamp duty)

The NSW First Home Buyers Assistance Scheme (FHBAS) provides stamp duty relief on both new and established homes. For contracts exchanged on or after 1 July 2023:

- Full exemption: properties at or below $800,000

- Concessional rate: properties above $800,000 and below $1,000,000

The full exemption removes stamp duty entirely. On a $799,000 purchase, the saving is around $30,000. The relief applies to new builds and established homes alike, which catches many buyers off guard.

Speak to us about stamp duty concessions for first home buyers. The Revenue NSW stamp duty calculator gives the exact figure for your purchase price.

First Home Super Saver Scheme

The First Home Super Saver Scheme (FHSS) lets you withdraw voluntary superannuation contributions to use toward your deposit. The cap is $50,000 in total contributions across all financial years, with an annual limit of $15,000 per year.

The First Home Super Saver Scheme runs through the ATO. The FHSS release process has strict timing rules: you must request your release determination before you settle, and ideally before you sign a contract. Missing that window means losing access to those funds for your deposit. Using the FHSS does not affect eligibility for the 5% Deposit Scheme or any NSW state concession. All four programs can stack.

5% Deposit Scheme vs Help to Buy vs guarantor loans

Here is how they compare:

| Feature | 5% Deposit Scheme | Help to Buy | Guarantor Loan |

|---|---|---|---|

| Government role | Guarantees your deposit | Co-purchases equity (up to 40% new, 30% existing) | No government involvement |

| Your ownership | 100% from day one | Shared with government until you buy out their stake | 100% |

| Income caps | None | $100,000 individual; $160,000 joint or single parent | None |

| Citizenship | Citizens and permanent residents | Citizens only | Not applicable |

| Minimum deposit | 5% (2% single parents) | 2% | Can be 0% |

| LMI | Avoided | Avoided (smaller loan size) | Avoided (guarantor secures the gap) |

| Places | Unlimited | 10,000 per year | Unlimited |

The 5% Deposit Scheme suits buyers who have 5% saved, want full ownership from day one, and don’t want to involve family in the loan structure.

The Help to Buy shared equity scheme suits buyers who want to borrow less and are comfortable with the government holding an equity interest until they buy it out over time. Income caps apply, and the scheme is open only to Australian citizens, not permanent residents.

A guarantor home loan suits buyers who have a family member willing to use their own property equity as security. No deposit may be required, and family participation keeps the loan entirely in the private sector. The trade-off is that the guarantor takes on real financial risk.

How to apply: step by step

- Check your eligibility. Review the criteria at firsthomebuyers.gov.au, or speak with a mortgage broker to assess your specific situation before approaching any lender.

- Select a participating lender. You must apply through a Housing Australia-authorised lender. Applications cannot be made directly to Housing Australia.

- Get pre-approved. The lender assesses your income, expenses, credit history, and deposit savings. Once pre-approved, you have 90 days to find a property and sign a contract.

- Find and buy your property. The property must be at or below the price cap for your location and be an eligible property type (house, townhouse, apartment, unit, off-the-plan purchase, or land and build package).

- Settle. The lender lodges the guarantee documentation with Housing Australia at settlement. You contribute your 5% deposit (or 2% if you qualify under the single parent stream) plus standard settlement costs.

You will need standard home loan documentation: identification, proof of income, bank statements showing your savings history, and a completed Home Buyer Declaration form for Housing Australia.

Worth knowing before you choose a lender: the scheme doesn’t set interest rates. The rate you pay depends on which lender you use. Two buyers on the same scheme with the same deposit and income can pay materially different rates depending on which participating lender they choose. Comparing rates across the panel before you commit is worth the time.

Common mistakes and broker tips

Applying to only one lender. Each participating lender has its own credit policy. If one lender declines your application due to an overlay issue, another panel lender may approve you under its own policy, particularly for casual workers, contractors, and borrowers with variable or irregular income.

Confusing the FHOG with the 5% Deposit Scheme. The NSW First Home Owner Grant ($10,000) and the 5% Deposit Scheme are separate programs with different eligibility rules. The FHOG applies only to new homes under $600,000. The 5% Deposit Scheme applies to new and established homes up to $1,500,000 in Sydney.

Not checking whether the FHBAS applies. Many buyers focus on LMI savings without realising they also qualify for a full stamp duty exemption on purchases under $800,000. The saving is around $30,000 on a $799,000 purchase.

Underestimating the genuine savings test. Your 5% deposit needs to look like genuine savings to the lender. Funds in a savings account for three months or more generally qualify. A large transfer from a parent shortly before application will not satisfy most lenders’ test, even though it satisfies the scheme’s 5% requirement. There is one lender that will accept a large transfer from a parent into your account.

Using the wrong price cap. The $1,500,000 cap applies to Sydney metro, Illawarra, Newcastle, and Lake Macquarie. Regional NSW uses an $800,000 cap. Check your postcode on the Housing Australia Postcode Search Tool before assuming which cap applies.

Thinking income caps still apply. Before 1 October 2025, buyers above a certain income were ineligible. That restriction was removed. If you were told you earned too much under the old scheme, re-check your eligibility under the current rules.

Frequently asked questions

Which banks are part of the 5% deposit scheme?

All four major banks participate: ANZ, CommBank, NAB, and Westpac (including St George, Bank of Melbourne, and BankSA). The full authorised panel has 47 lenders as of 2026, covering the major banks, their subsidiaries, and dozens of mutual banks and credit unions. ING, Macquarie, HSBC, Suncorp, and AMP Bank are not currently on the panel. Apply through any participating lender; you cannot apply to Housing Australia directly.

What is a 5% deposit on a $600,000 house?

5% of $600,000 is $30,000. Under the scheme, that is enough to buy the property without paying LMI. Without the scheme, you would need a 20% deposit ($120,000) to avoid LMI on a purchase of that size.

How many Australians have used the 5% deposit scheme?

More than 300,000 Australians have bought or built a home under the scheme since it launched in January 2020, per Housing Australia’s March 2026 report. The Housing Australia homepage showed 315,000+ as of June 2026.

Is the 5% Deposit Scheme the same as Help to Buy?

No. The 5% Deposit Scheme is a deposit guarantee: the government guarantees your deposit, you own 100% of your home, no income caps apply, and places are unlimited. Help to Buy is a shared equity scheme: the government co-purchases up to 40% of a new home (30% for existing), income caps of $100,000 for individuals and $160,000 for joint applicants apply, and places are capped at 10,000 per year.

What is the 5% deposit scheme 2026?

The Australian Government 5% Deposit Scheme is a federal program administered by Housing Australia. Eligible first home buyers can purchase with a 5% deposit and avoid LMI because the government guarantees up to 15% of the loan value. It was renamed from the Home Guarantee Scheme on 1 October 2025 and now has unlimited places, no income caps, and expanded NSW price caps up to $1,500,000.

How does the 5% deposit scheme work?

Housing Australia provides a guarantee to your lender for the difference between your deposit (as low as 5%) and 20% of the property value. The lender treats the loan as if you already have 20% equity and does not require LMI. The government holds no stake in your home. You own 100% from settlement.

If you want to know which panel lender suits your income type, employment structure, and deposit source, that is exactly the kind of assessment we do before recommending anyone. Speak to a mortgage broker in Western Sydney before you apply.

This article contains general information only and does not constitute financial advice. Your personal financial situation, objectives and needs have not been considered. Before acting on any information, you should consider its appropriateness to your circumstances. Speak to a qualified mortgage broker for advice tailored to your situation. Mortgage World Australia Pty Ltd is a credit representative (CR No. 396946) of Mortgage Specialists Pty Ltd (Australian Credit Licence No. 387025).

Written by Patrick O’Brien, Director and Home Loan Specialist since 2001. Mortgage World Australia has access to 52+ lenders and has helped thousands of NSW borrowers navigate first home purchase since 2001. Ready to explore your options? Speak to a mortgage broker in Western Sydney.

Patrick is a Director and a Home Loan Specialist. He has been helping Australians with home loans since 2001. Prior to working as a mortgage broker Patrick was employed by Macquarie Bank for 3 years and also worked as an accountant for a publicly listed company. Patrick’s qualifications include:

Bachelor of Business, UTS Sydney. Majored in accounting and sub-majored in Finance and Marketing.

Diploma of Finance and Mortgage Broking Management FNS50310

Certificate IV in Financial Services (Finance/Mortgage Broking) FNS40804

Ready to Take the Next Step?

Whether you’re looking to buy your first home, refinance, or explore investment opportunities, Mortgage World Australia is here to help.

Fill out the contact form below, and one of our expert mortgage brokers will be in touch shortly to discuss your needs and guide you through your options.

Get Started Today!